Ovarian Cancer Diagnostic Market

Ovarian Cancer Diagnostic Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_709778 | Last Updated : December 17, 2025 |

Format : ![]()

![]()

![]()

![]()

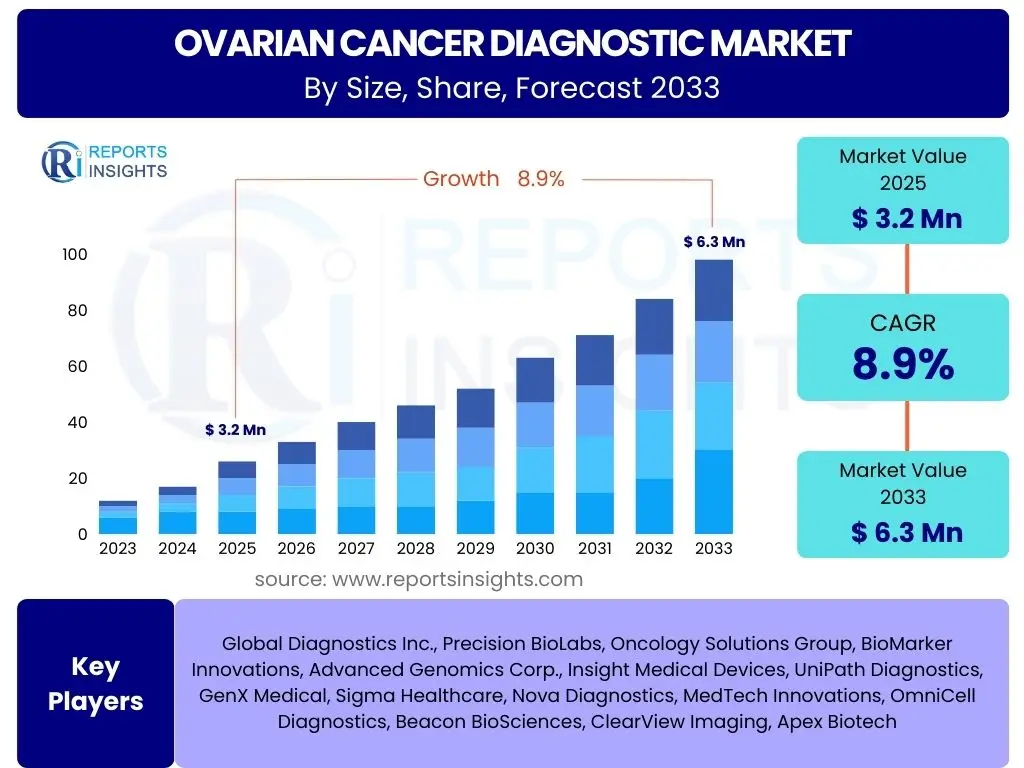

Ovarian Cancer Diagnostic Market Size

According to Reports Insights Consulting Pvt Ltd, The Ovarian Cancer Diagnostic Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 8.9% between 2025 and 2033. The market is estimated at USD 3.2 Billion in 2025 and is projected to reach USD 6.3 Billion by the end of the forecast period in 2033.

The substantial growth in the ovarian cancer diagnostic market is primarily driven by the increasing global incidence of ovarian cancer, coupled with a heightened focus on early detection and improved patient outcomes. Advancements in diagnostic technologies, including novel biomarker discovery and enhanced imaging modalities, are playing a pivotal role in expanding market opportunities. Furthermore, rising awareness campaigns and government initiatives aimed at improving women's health are contributing significantly to market expansion, encouraging regular screenings and timely diagnosis.

This projected growth reflects a robust demand for accurate and non-invasive diagnostic solutions. The market's trajectory is also influenced by an aging global population, which inherently faces a higher risk of developing various cancers, including ovarian cancer. The continuous pipeline of innovative diagnostic tools, from advanced genetic testing to sophisticated liquid biopsy techniques, is expected to maintain this upward trend, positioning the market for sustained expansion over the next decade.

Key Ovarian Cancer Diagnostic Market Trends & Insights

User queries frequently highlight interest in the evolving landscape of ovarian cancer diagnostics, particularly regarding early detection methods, non-invasive techniques, and the integration of advanced technologies. There is a strong focus on understanding how new scientific discoveries are translating into clinical practice, improving diagnostic accuracy and patient prognosis. Users are keen to identify trends that promise less invasive, more specific, and highly sensitive diagnostic tools, moving beyond traditional methods to offer better screening and monitoring options for this aggressive cancer.

The market is experiencing a significant shift towards more refined diagnostic approaches that can differentiate malignant from benign conditions with greater precision. This includes the exploration of multi-marker panels and comprehensive genomic profiling that offer a more holistic view of the disease. Furthermore, the push for personalized medicine is influencing diagnostic strategies, where tests are tailored based on individual patient profiles and tumor characteristics, optimizing treatment pathways from the outset. This paradigm shift underscores the industry's commitment to enhancing diagnostic efficacy and patient-centric care.

- Shift towards minimally invasive diagnostic procedures, such as liquid biopsies.

- Growing adoption of multi-marker panels for enhanced diagnostic accuracy.

- Increasing emphasis on genetic testing (e.g., BRCA1/2, HRD) for risk assessment and companion diagnostics.

- Advancements in imaging technologies, including enhanced ultrasound and AI-assisted interpretation.

- Development of novel biomarkers for early detection and disease monitoring.

- Integration of personalized medicine approaches into diagnostic workflows.

AI Impact Analysis on Ovarian Cancer Diagnostic

Common user questions regarding AI's impact on ovarian cancer diagnostics center on its applications in image analysis, data interpretation, and early detection. Users are particularly interested in how AI can augment existing diagnostic modalities, reduce human error, and accelerate the diagnostic process. There's also curiosity about AI's role in predictive analytics for disease progression and treatment response, as well as its potential to identify subtle patterns in complex genomic data that might otherwise be overlooked by human analysis. The overall expectation is that AI will revolutionize the precision and efficiency of ovarian cancer diagnosis.

Artificial intelligence is rapidly becoming an indispensable tool across various stages of ovarian cancer diagnostics. From enhancing the clarity and interpretability of medical images such as ultrasound, CT, and MRI scans to processing vast amounts of patient data for risk stratification, AI algorithms offer unparalleled analytical capabilities. Its application in pathology, particularly for identifying cancerous cells and assessing tumor characteristics, is also gaining traction, promising more consistent and accurate diagnoses. The ability of AI to learn from large datasets enables the continuous improvement of its diagnostic accuracy, making it a critical component for future diagnostic platforms.

- Enhancement of imaging diagnostics through AI-powered image analysis for improved detection of subtle lesions.

- Accelerated pathology review and precise tumor classification using machine learning algorithms.

- Development of AI models for predictive analytics, forecasting disease progression and treatment efficacy.

- Integration of AI in biomarker discovery, identifying novel patterns in genomic and proteomic data.

- Automation of data interpretation from complex diagnostic tests, leading to faster and more accurate results.

- Support for clinical decision-making by providing comprehensive patient insights and risk assessments.

Key Takeaways Ovarian Cancer Diagnostic Market Size & Forecast

User inquiries about key takeaways from the market size and forecast often focus on understanding the most significant growth drivers, the primary factors influencing market expansion, and the long-term outlook for investment and innovation. They seek concise summaries of the market's potential, highlighting areas of high growth, emerging opportunities, and the overarching implications for healthcare providers, diagnostic companies, and patients. The emphasis is on gleaning actionable insights that inform strategic planning and stakeholder engagement within the evolving diagnostic landscape.

The ovarian cancer diagnostic market is poised for robust expansion, primarily fueled by a confluence of technological advancements, increasing disease prevalence, and a global emphasis on early intervention. The forecast underscores a sustained demand for innovative diagnostic tools that offer greater sensitivity, specificity, and patient convenience. Stakeholders should recognize the critical role of R&D in developing next-generation biomarkers and imaging techniques, as these will be central to capturing market share and improving clinical outcomes. The market's resilience is further supported by a growing awareness of women's health issues and proactive screening initiatives.

- Significant market growth driven by the rising incidence of ovarian cancer and increasing awareness.

- Technological innovation, particularly in liquid biopsy and multi-omics, is a key growth accelerator.

- The shift towards early and accurate diagnosis remains a central theme, impacting market strategies.

- North America and Europe currently dominate, but Asia Pacific presents high growth opportunities.

- Investment in AI and machine learning for diagnostic enhancement is crucial for competitive advantage.

- Regulatory approvals and reimbursement policies will continue to shape market accessibility and adoption rates.

Ovarian Cancer Diagnostic Market Drivers Analysis

The ovarian cancer diagnostic market is significantly propelled by several critical factors, primarily the rising global incidence of ovarian cancer, which naturally escalates the demand for effective diagnostic solutions. Concurrently, increasing awareness programs and early screening initiatives, often backed by government and non-profit organizations, encourage proactive health management among women. These efforts contribute to earlier diagnoses, which are crucial for improving patient prognosis and survival rates.

Furthermore, continuous advancements in diagnostic technologies, including the discovery of novel biomarkers and the development of more sophisticated imaging techniques, are expanding the capabilities and accuracy of ovarian cancer detection. The shift towards non-invasive and minimally invasive diagnostic procedures, such as liquid biopsies, also plays a pivotal role by offering less burdensome and more accessible testing options. These technological leaps, combined with a growing aging population, which is more susceptible to cancer, collectively drive the market forward.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Rising Incidence of Ovarian Cancer | +2.1% | Global, particularly developed regions | Long-term |

| Technological Advancements in Diagnostics | +1.8% | North America, Europe, Asia Pacific | Mid to Long-term |

| Increasing Awareness & Screening Programs | +1.5% | Global, with emphasis on emerging economies | Mid-term |

| Growing Aging Population | +1.2% | Europe, North America, Japan | Long-term |

| Demand for Early Detection Methods | +1.3% | Global | Long-term |

Ovarian Cancer Diagnostic Market Restraints Analysis

Despite the robust growth, the ovarian cancer diagnostic market faces several restraints that could impede its full potential. A primary concern is the high cost associated with advanced diagnostic tests and procedures. Many cutting-edge technologies, while highly effective, come with a significant price tag, making them less accessible in regions with limited healthcare budgets or for uninsured populations. This financial burden can lead to delayed diagnoses or the underutilization of optimal testing methods, particularly in developing countries.

Another significant restraint is the lack of highly specific and sensitive biomarkers for early-stage ovarian cancer. Current biomarkers, such as CA-125, often lack the desired specificity, leading to false positives and unnecessary invasive follow-up procedures. This diagnostic ambiguity creates challenges in clinical practice and can reduce patient confidence in screening programs. Additionally, stringent regulatory approval processes for new diagnostic devices and tests, especially in major markets, can extend development timelines and increase commercialization costs, thereby slowing market penetration of innovative solutions.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Cost of Advanced Diagnostic Tests | -1.5% | Global, particularly emerging markets | Long-term |

| Lack of Specific Early-Stage Biomarkers | -1.0% | Global | Mid to Long-term |

| Stringent Regulatory Approval Processes | -0.8% | North America, Europe | Mid-term |

| Limited Reimbursement Policies | -0.7% | Various regions, including parts of Asia Pacific | Short to Mid-term |

| Ethical Concerns Regarding Genetic Testing | -0.5% | Europe, parts of North America | Long-term |

Ovarian Cancer Diagnostic Market Opportunities Analysis

Significant opportunities are emerging within the ovarian cancer diagnostic market, driven by ongoing research and development in non-invasive screening technologies. The increasing focus on liquid biopsy, for instance, offers immense potential for earlier and less burdensome detection, particularly in asymptomatic individuals at high risk. These innovative approaches promise to address current limitations by providing highly sensitive and specific diagnostic information from readily available bodily fluids, transforming the screening paradigm.

Furthermore, the growing adoption of personalized medicine approaches is creating new avenues for diagnostic test development. Companion diagnostics that guide targeted therapies, genetic profiling for risk assessment, and tests that predict response to specific treatments represent a substantial growth opportunity. Expansion into untapped emerging markets, particularly in Asia Pacific and Latin America, also offers considerable potential due to large patient populations, improving healthcare infrastructure, and increasing disposable incomes. These regions are becoming key targets for market players seeking to diversify their global presence and capitalize on underserved diagnostic needs.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development of Non-Invasive Liquid Biopsies | +2.0% | Global, high adoption in developed markets | Mid to Long-term |

| Integration of AI and Machine Learning in Diagnostics | +1.7% | North America, Europe, progressive Asia Pacific | Mid-term |

| Expansion in Emerging Markets | +1.5% | Asia Pacific, Latin America, MEA | Long-term |

| Growing Demand for Personalized Medicine & Companion Diagnostics | +1.4% | Global, particularly for advanced treatments | Mid to Long-term |

| Technological Advancements in Molecular Diagnostics | +1.3% | Global | Long-term |

Ovarian Cancer Diagnostic Market Challenges Impact Analysis

The ovarian cancer diagnostic market faces significant challenges, primarily stemming from the inherent difficulty in detecting the disease at its early stages due to non-specific symptoms. This often leads to late-stage diagnoses, which severely limit treatment options and worsen patient outcomes. The lack of distinct early symptoms contributes to a low screening uptake among the general population, making it harder to implement effective broad-based early detection programs.

Another major challenge involves the complexity of ovarian cancer heterogeneity. Different subtypes of ovarian cancer respond differently to treatments, and current diagnostic tools may not always effectively characterize these variations. This complexity can hinder the development of universal diagnostic markers and tailored therapeutic strategies. Furthermore, achieving broad market adoption for novel diagnostic tests can be challenging due to factors such as physician skepticism, the need for extensive clinical validation, and the resistance to change from established diagnostic protocols. Overcoming these hurdles requires substantial investment in research, education, and robust clinical evidence.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Late-Stage Diagnosis Due to Non-Specific Symptoms | -1.8% | Global | Long-term |

| Lack of High Sensitivity & Specificity in Current Biomarkers | -1.2% | Global | Mid to Long-term |

| High Development Cost & Time for New Diagnostics | -1.0% | Global, impacts R&D intensive regions | Long-term |

| Reimbursement Challenges for Novel Tests | -0.9% | North America, Europe | Short to Mid-term |

| Regulatory Hurdles for Market Entry | -0.7% | North America, Europe, Japan | Mid-term |

Ovarian Cancer Diagnostic Market - Updated Report Scope

This comprehensive report provides an in-depth analysis of the global Ovarian Cancer Diagnostic Market, offering a detailed understanding of its current size, historical performance, and future growth projections. The scope encompasses a thorough examination of market dynamics, including key drivers, restraints, opportunities, and challenges that are shaping the industry landscape. Special attention is given to the impact of emerging technologies like Artificial Intelligence and liquid biopsy on diagnostic paradigms.

The report meticulously segments the market by diagnostic type, end-user, and geographic region, providing granular insights into various market components and their respective growth trajectories. It also identifies and profiles leading market players, offering a competitive landscape analysis and strategic recommendations for stakeholders. This extensive coverage aims to equip market participants, investors, and healthcare professionals with critical data and strategic intelligence necessary for informed decision-making and capitalizing on market opportunities.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 3.2 Billion |

| Market Forecast in 2033 | USD 6.3 Billion |

| Growth Rate | 8.9% |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Global Diagnostics Inc., Precision BioLabs, Oncology Solutions Group, BioMarker Innovations, Advanced Genomics Corp., Insight Medical Devices, UniPath Diagnostics, GenX Medical, Sigma Healthcare, Nova Diagnostics, MedTech Innovations, OmniCell Diagnostics, Beacon BioSciences, ClearView Imaging, Apex Biotech |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The ovarian cancer diagnostic market is meticulously segmented to provide a detailed understanding of its diverse components and growth opportunities. These segmentations are critical for identifying specific market niches, understanding consumer preferences, and developing targeted strategies for various stakeholders. The market is primarily categorized by diagnostic type, which includes a range of methods from traditional blood tests and advanced imaging to genetic and liquid biopsies, reflecting the technological evolution in the field.

Further segmentation by end-user delineates the primary consumers of these diagnostic services, such as hospitals, specialty clinics, diagnostic centers, and research institutions. This breakdown helps in understanding the demand patterns from different healthcare settings and their specific requirements. Such a granular analysis is essential for market players to tailor their product offerings, sales, and marketing efforts effectively across different channels and patient populations, ensuring optimal market penetration and addressing specific clinical needs.

- By Diagnostic Type:

- Blood Tests (CA-125, HE4, OVA1, ROMA, Others)

- Imaging (Ultrasound, CT Scan, MRI, PET Scan, Others)

- Biopsy

- Genetic Testing (BRCA1/2, HRD, Others)

- Liquid Biopsy

- By End-User:

- Hospitals

- Specialty Clinics

- Diagnostic Centers

- Research & Academic Institutions

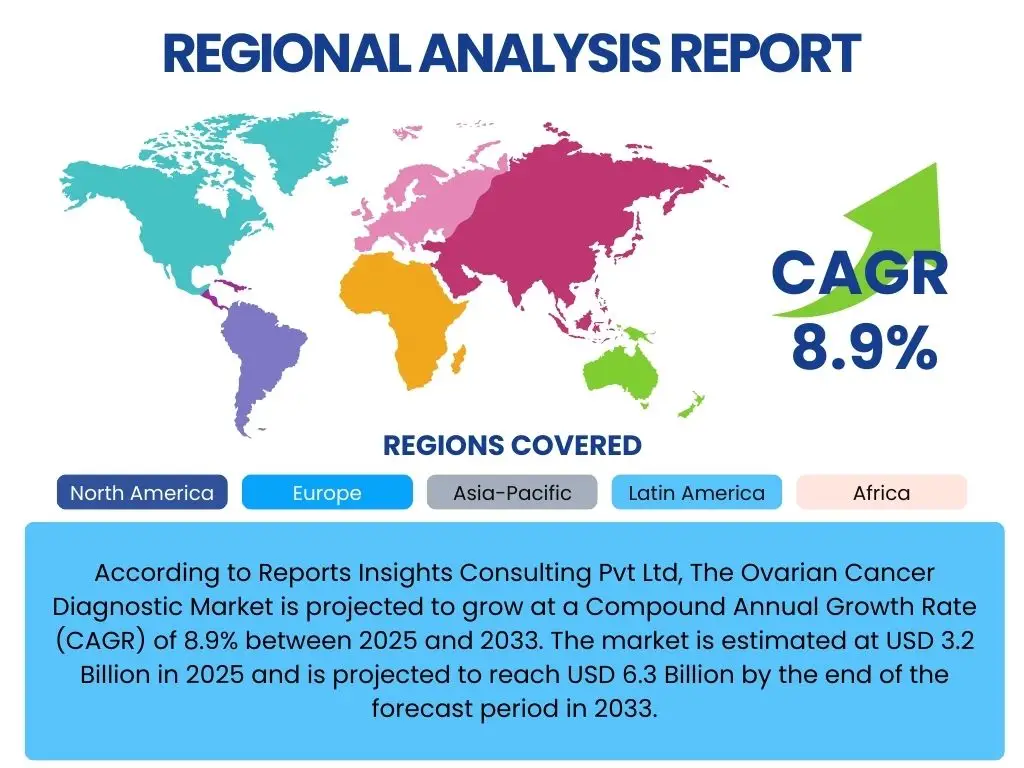

Regional Highlights

North America currently holds the largest share in the ovarian cancer diagnostic market, driven by advanced healthcare infrastructure, high awareness regarding early diagnosis, and significant investments in research and development. The presence of key market players, favorable reimbursement policies, and a high adoption rate of innovative diagnostic technologies further bolster the region's dominance. The United States, in particular, leads in terms of both market size and technological innovation, with a strong focus on personalized medicine and genetic testing.

Europe follows North America, characterized by increasing healthcare expenditure, a growing elderly population, and government initiatives aimed at cancer screening and early detection. Countries like Germany, the UK, and France are pivotal within the European market, showcasing robust demand for advanced diagnostic solutions. Meanwhile, the Asia Pacific region is anticipated to exhibit the highest growth rate during the forecast period, attributed to rising awareness, improving healthcare facilities, increasing disposable incomes, and a large patient pool, particularly in countries like China and India, which are rapidly expanding their diagnostic capabilities.

- North America: Dominant market share due to advanced healthcare infrastructure, high R&D investment, and favorable reimbursement policies.

- Europe: Significant market presence driven by an aging population, rising cancer incidence, and strong government support for healthcare.

- Asia Pacific: Fastest-growing region, fueled by increasing healthcare awareness, improving access to diagnostic services, and expanding medical tourism.

- Latin America: Emerging market with growing investments in healthcare, expanding insurance coverage, and rising awareness about women's health.

- Middle East & Africa: Developing market influenced by increasing healthcare spending, modernization of medical facilities, and rising prevalence of cancer.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Ovarian Cancer Diagnostic Market.- Global Diagnostics Inc.

- Precision BioLabs

- Oncology Solutions Group

- BioMarker Innovations

- Advanced Genomics Corp.

- Insight Medical Devices

- UniPath Diagnostics

- GenX Medical

- Sigma Healthcare

- Nova Diagnostics

- MedTech Innovations

- OmniCell Diagnostics

- Beacon BioSciences

- ClearView Imaging

- Apex Biotech

Frequently Asked Questions

Analyze common user questions about the Ovarian Cancer Diagnostic market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is the current growth rate of the Ovarian Cancer Diagnostic Market?

The Ovarian Cancer Diagnostic Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 8.9% between 2025 and 2033.

What are the primary drivers of growth in this market?

Key drivers include the rising global incidence of ovarian cancer, advancements in diagnostic technologies (e.g., liquid biopsy), and increasing awareness and screening programs for early detection.

How is AI impacting ovarian cancer diagnostics?

AI is significantly impacting diagnostics by enhancing image analysis, accelerating pathology review, assisting in biomarker discovery, and improving predictive analytics for disease progression and treatment response.

Which diagnostic types are showing the most promise?

Minimally invasive methods such as liquid biopsies, advanced genetic testing (BRCA1/2, HRD), and multi-marker blood panels are demonstrating significant promise for improved early detection and characterization.

What are the main challenges facing the market?

Major challenges include the difficulty of early-stage diagnosis due to non-specific symptoms, the lack of highly specific and sensitive biomarkers, and the high cost associated with advanced diagnostic tests.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted