Surge Protection Device Market

Surge Protection Device Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_709522 | Last Updated : December 09, 2025 |

Format : ![]()

![]()

![]()

![]()

Surge Protection Device Market Size

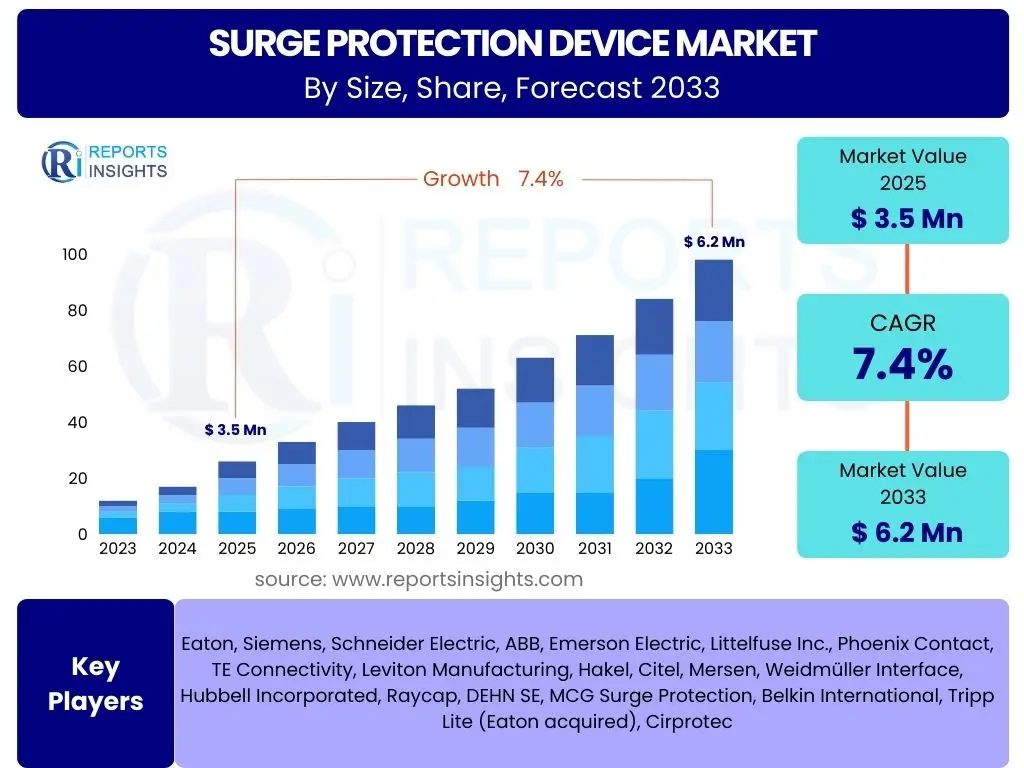

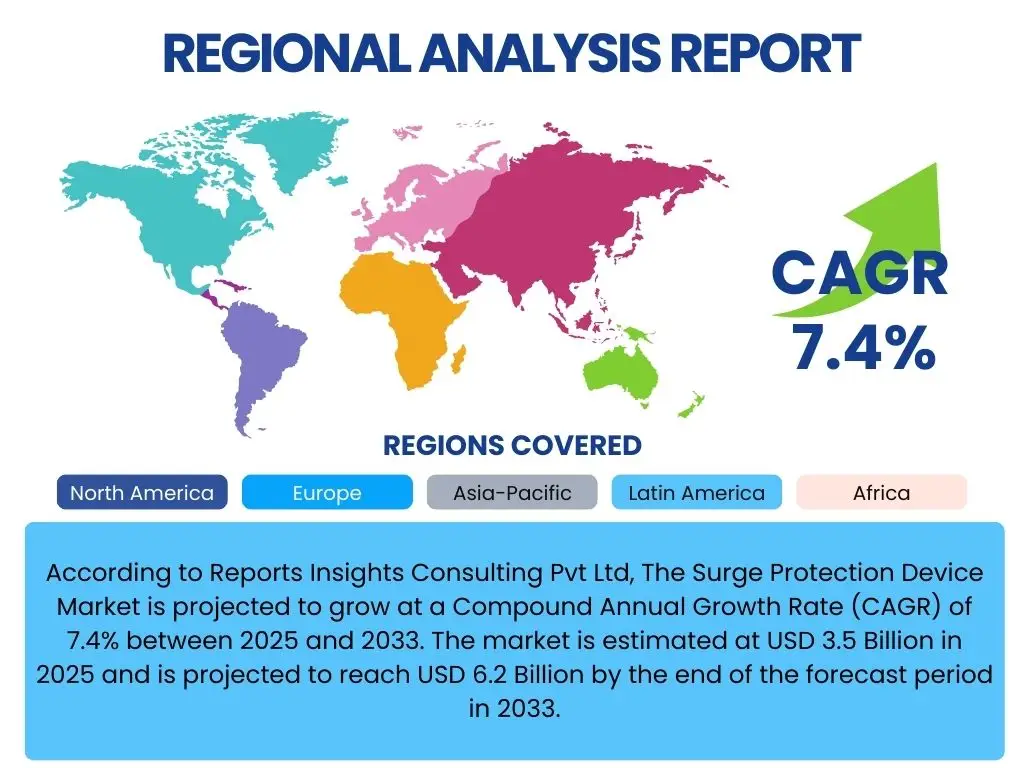

According to Reports Insights Consulting Pvt Ltd, The Surge Protection Device Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 7.4% between 2025 and 2033. The market is estimated at USD 3.5 Billion in 2025 and is projected to reach USD 6.2 Billion by the end of the forecast period in 2033.

Key Surge Protection Device Market Trends & Insights

The Surge Protection Device (SPD) market is currently experiencing significant evolution driven by several macro and micro-economic factors. Users frequently inquire about the underlying forces shaping market dynamics, particularly concerning the increased integration of sensitive electronics and the imperative for robust infrastructure protection. A prominent trend involves the growing adoption of smart grid technologies and renewable energy sources, which introduce new complexities and transient overvoltage risks, thereby escalating the demand for advanced SPD solutions.

Furthermore, the proliferation of IoT devices and the expansion of data centers globally are critical drivers, necessitating higher levels of protection for critical digital infrastructure. Consumers and businesses are increasingly aware of the financial and operational consequences of equipment downtime due to power surges, leading to a greater emphasis on preventive measures. Regulatory mandates and evolving international standards for electrical safety are also compelling industries to upgrade their protection systems, creating a consistent demand for compliance-driven SPD installations across various sectors.

- Increased adoption of smart grid infrastructure and renewable energy systems.

- Rapid growth in data center deployments and cloud computing infrastructure.

- Proliferation of IoT devices and connected systems in residential and industrial settings.

- Stricter regulatory compliance and evolving electrical safety standards globally.

- Growing awareness among end-users regarding the financial implications of power surge damage.

- Technological advancements leading to more compact, efficient, and intelligent SPD solutions.

AI Impact Analysis on Surge Protection Device

Users frequently express interest in how artificial intelligence (AI) might influence the Surge Protection Device (SPD) market, particularly regarding enhanced reliability, predictive capabilities, and smart grid integration. While AI does not directly manufacture SPDs, its impact is increasingly felt through intelligent monitoring, predictive maintenance, and optimized system management within the broader electrical infrastructure. AI-driven analytics can process vast amounts of data from power grids, identifying patterns that precede surge events or indicate potential SPD degradation, allowing for proactive maintenance and replacement strategies. This shift from reactive to predictive maintenance significantly enhances the overall reliability and longevity of protected systems.

Moreover, AI plays a crucial role in the development of adaptive and self-healing smart grids, where intelligent algorithms can anticipate and mitigate electrical disturbances more effectively. This indirect influence drives demand for SPDs that can integrate seamlessly with AI-powered monitoring systems, offering real-time data on their status and performance. As industrial IoT (IIoT) and smart factory initiatives gain traction, AI optimizes energy flow and equipment operation, which in turn necessitates superior surge protection for these sophisticated, interconnected systems, thereby elevating the functional requirements for future SPD designs.

- AI-driven predictive maintenance for SPDs and protected equipment, reducing downtime.

- Enhanced real-time monitoring and diagnostics of SPD performance through AI analytics.

- Integration of SPDs into AI-powered smart grid systems for optimized power distribution and protection.

- Development of more intelligent SPDs capable of communicating data for AI analysis.

- AI's role in optimizing energy management in industrial and commercial settings, increasing demand for robust SPDs.

- Improved fault detection and response mechanisms in electrical networks, indirectly benefiting SPD application.

Key Takeaways Surge Protection Device Market Size & Forecast

Common user questions often revolve around the overarching significance and future trajectory of the Surge Protection Device (SPD) market. The primary takeaway is the consistent and robust growth anticipated across the forecast period, driven by an accelerating global reliance on electrical and electronic infrastructure. This growth underscores the essential role SPDs play in safeguarding sensitive equipment, ensuring operational continuity, and mitigating significant financial losses stemming from power surges. The market's expansion is not merely quantitative but also reflects a qualitative shift towards more sophisticated, integrated, and reliable protection solutions.

Furthermore, the forecast highlights a critical trend: the market's resilience against economic fluctuations, largely due to the indispensable nature of surge protection in modern technological landscapes. The increasing complexity of electrical environments, particularly with the proliferation of interconnected devices and the advent of smart cities, reinforces the long-term upward trajectory of SPD demand. Investors and stakeholders should recognize the sustained necessity for these devices across diverse sectors, positioning the SPD market as a stable and strategically important segment within the broader electrical equipment industry.

- The Surge Protection Device market is poised for significant and sustained growth through 2033.

- Growing adoption of digital technologies and smart infrastructure is a key market accelerator.

- SPDs are becoming indispensable for protecting sensitive electronics in diverse applications.

- Increased awareness and stringent regulatory standards are fueling market expansion.

- Technological innovation is leading to more advanced and efficient SPD solutions.

- The market offers robust opportunities across industrial, commercial, and residential sectors globally.

Surge Protection Device Market Drivers Analysis

The Surge Protection Device (SPD) market is propelled by a confluence of factors, primarily the global increase in the adoption of sensitive electronic equipment across all sectors. As industries and households become increasingly reliant on digital systems, the vulnerability to power surges, whether from lightning strikes, utility switching, or internal load changes, becomes more pronounced. This heightened dependency necessitates robust protection mechanisms to prevent costly downtime, data loss, and equipment damage, directly driving the demand for SPDs.

Another significant driver is the expansion of smart grid initiatives and renewable energy infrastructure worldwide. These complex systems, with their intricate network of sensors, controls, and inverters, are particularly susceptible to transient overvoltages. Furthermore, the rapid growth of data centers, telecommunication networks, and industrial automation demands uninterrupted power quality, making SPDs an integral component of their protection schemes. Evolving regulatory standards and heightened awareness about electrical safety also contribute substantially to market growth.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing Adoption of Sensitive Electronic Equipment | +1.8% | Global, particularly Asia Pacific & North America | Long-term (2025-2033) |

| Expansion of Smart Grid & Renewable Energy Infrastructure | +1.5% | Europe, North America, China, India | Medium to Long-term (2025-2033) |

| Increasing Number of Data Centers & Telecommunication Networks | +1.3% | North America, Asia Pacific, Europe | Long-term (2025-2033) |

| Strict Regulatory Standards & Electrical Safety Compliance | +1.0% | Europe, North America, Japan | Medium-term (2025-2030) |

| Rising Industrial Automation & IIoT Adoption | +0.9% | Germany, China, US, Japan | Long-term (2025-2033) |

Surge Protection Device Market Restraints Analysis

Despite robust growth prospects, the Surge Protection Device (SPD) market faces several notable restraints that could temper its expansion. One significant challenge is the relatively low awareness regarding the necessity and benefits of surge protection, especially in developing regions and among smaller businesses and residential consumers. Many end-users perceive power surges as infrequent or minor events, leading to a reluctance to invest in dedicated protection solutions until after an incident occurs, which hinders proactive adoption.

Another restraint involves the initial higher cost associated with advanced or comprehensive SPD installations, which can be a deterrent for budget-constrained projects or consumers. While the long-term benefits of preventing damage and downtime far outweigh the initial investment, this upfront expenditure can pose a barrier. Furthermore, the presence of low-quality or counterfeit SPD products in the market undermines consumer confidence and can lead to inadequate protection, contributing to a perception that SPDs are unreliable or ineffective, thereby restraining the growth of legitimate market players.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Lack of Awareness & Education Among End-Users | -1.2% | Developing countries in APAC, Latin America, MEA | Long-term (2025-2033) |

| High Initial Investment Cost for Advanced SPDs | -0.8% | Global, particularly budget-sensitive markets | Medium-term (2025-2030) |

| Availability of Low-Quality/Counterfeit Products | -0.7% | Global, especially emerging markets | Long-term (2025-2033) |

| Complexity of Installation & System Integration | -0.5% | Commercial & Industrial sectors | Short to Medium-term (2025-2028) |

Surge Protection Device Market Opportunities Analysis

The Surge Protection Device (SPD) market is rich with opportunities, primarily fueled by the accelerating global transition towards smart infrastructure and sustainable energy solutions. The rapid development of smart cities, which integrate advanced digital technologies into urban services, creates an immense demand for robust and intelligent surge protection for their interconnected grids, public utilities, and building management systems. This extensive network of sensitive electronics requires comprehensive protection to ensure reliability and continuous operation, opening new avenues for SPD manufacturers.

Furthermore, the significant global push for electric vehicle (EV) adoption and the subsequent expansion of EV charging infrastructure presents a substantial growth opportunity. EV charging stations are highly susceptible to voltage fluctuations and surges, necessitating specialized SPDs to protect both the charging equipment and the vehicles themselves. Retrofitting existing residential, commercial, and industrial buildings with updated surge protection, especially in mature economies with aging electrical infrastructure, also represents a considerable untapped market. Emerging economies, driven by rapid urbanization and industrialization, are continuously expanding their electrical grids and adopting modern technologies, creating a fertile ground for new SPD installations.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growth of Smart Cities & IoT Infrastructure | +1.6% | China, India, UAE, North America, Europe | Long-term (2025-2033) |

| Expansion of Electric Vehicle Charging Infrastructure | +1.4% | Europe, North America, China | Long-term (2025-2033) |

| Retrofitting Older Buildings & Infrastructure | +1.1% | North America, Europe, Japan | Medium to Long-term (2025-2033) |

| Untapped Markets in Developing Economies | +1.0% | Africa, Southeast Asia, Latin America | Long-term (2025-2033) |

| Development of Hybrid & Intelligent SPDs | +0.9% | Global | Medium to Long-term (2025-2033) |

Surge Protection Device Market Challenges Impact Analysis

The Surge Protection Device (SPD) market is confronted by several challenges that necessitate strategic navigation for sustained growth. One primary challenge is the intense price competition, particularly from numerous regional and local manufacturers in certain segments. This competition can compress profit margins for established players and make it difficult to invest adequately in research and development for innovative solutions. Maintaining product differentiation and quality in a crowded market remains a constant struggle.

Furthermore, the technical complexity involved in correctly selecting, installing, and coordinating SPDs within a larger electrical system can be a significant hurdle. Incorrect application or poor installation practices can lead to suboptimal protection or even system failures, diminishing the perceived value of SPDs. This demands a high level of technical expertise from installers and consultants. Supply chain disruptions, often exacerbated by geopolitical tensions or global events, can also impact the availability of critical components and raw materials, leading to production delays and increased costs, thereby challenging market stability and pricing.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Intense Price Competition from Local Manufacturers | -1.0% | Asia Pacific, Latin America | Long-term (2025-2033) |

| Technical Complexity in Selection & Installation | -0.8% | Global, particularly SME sector | Medium-term (2025-2030) |

| Supply Chain Volatility & Raw Material Costs | -0.7% | Global | Short to Medium-term (2025-2028) |

| Risk of Obsolescence with Rapid Technological Shifts | -0.6% | Global | Medium to Long-term (2025-2033) |

Surge Protection Device Market - Updated Report Scope

This report offers an in-depth, comprehensive analysis of the global Surge Protection Device (SPD) market, providing critical insights into its current state and future trajectory. The scope encompasses detailed market sizing, segmentation analysis, regional breakdowns, and a thorough examination of key drivers, restraints, opportunities, and challenges influencing market growth from 2025 to 2033. It further investigates the impact of emerging technologies and market trends to deliver a holistic perspective for stakeholders.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 3.5 Billion |

| Market Forecast in 2033 | USD 6.2 Billion |

| Growth Rate | 7.4% |

| Number of Pages | 255 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Eaton, Siemens, Schneider Electric, ABB, Emerson Electric, Littelfuse Inc., Phoenix Contact, TE Connectivity, Leviton Manufacturing, Hakel, Citel, Mersen, Weidmüller Interface, Hubbell Incorporated, Raycap, DEHN SE, MCG Surge Protection, Belkin International, Tripp Lite (Eaton acquired), Cirprotec |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Surge Protection Device (SPD) market is extensively segmented to provide granular insights into its diverse components and applications. This segmentation allows for a detailed understanding of how different product types, technologies, and end-use industries contribute to the overall market landscape. The primary segmentation categories encompass device type, discharge current capacity, voltage levels, underlying technology, application areas, and the specific end-use industries.

Understanding these segments is crucial for manufacturers to tailor their product offerings, for distributors to optimize their supply chains, and for end-users to select the most appropriate protection solutions. For instance, the demand for Type 1 SPDs is often driven by direct lightning strike protection requirements, while Type 2 and Type 3 SPDs cater to finer protection levels within facilities. Similarly, the proliferation of data centers drives demand for high-capacity, reliable SPDs, whereas residential applications might prioritize cost-effective, easily installable solutions.

- By Type: Type 1 SPD, Type 2 SPD, Type 3 SPD, Type 4 SPD

- By Discharge Current: Below 10 kA, 10 kA - 20 kA, 20 kA - 40 kA, Above 40 kA

- By Voltage: Low Voltage, Medium Voltage

- By Technology: Metal Oxide Varistor (MOV), Silicon Avalanche Diode (SAD), Gas Discharge Tube (GDT), Others (Hybrid)

- By Application: Residential, Commercial, Industrial, Data Centers, Telecommunication, Renewable Energy, Others (Healthcare, Transportation)

- By End-Use Industry: Manufacturing, IT & Telecommunications, Energy & Utilities, Commercial & Retail, Residential, Healthcare, Transportation, Others

Regional Highlights

- North America: A mature market characterized by stringent safety regulations, a high degree of industrial automation, and substantial investment in data centers and smart grid infrastructure. The region exhibits a strong demand for advanced and high-performance SPDs, driven by the need to protect sensitive electronics and maintain grid stability.

- Europe: Dominated by robust electrical safety standards (e.g., IEC standards) and a strong emphasis on renewable energy integration. Countries like Germany, France, and the UK are key contributors, driven by smart city initiatives, industrial automation, and a significant installed base of both commercial and residential buildings requiring modern surge protection.

- Asia Pacific (APAC): The fastest-growing market due to rapid industrialization, urbanization, and a booming manufacturing sector, particularly in China and India. Massive investments in infrastructure development, telecommunications, and renewable energy projects (solar, wind) are fueling unprecedented demand for SPDs across all applications.

- Latin America: An emerging market with increasing industrial and commercial development. Growing investments in energy infrastructure and telecommunications, coupled with expanding residential sectors, are driving the adoption of SPDs, though awareness and regulatory enforcement are still evolving.

- Middle East and Africa (MEA): Experiencing significant growth driven by large-scale construction projects, oil & gas industry investments, smart city developments (e.g., UAE, Saudi Arabia), and expanding power generation capabilities. The region's exposure to frequent lightning strikes further underscores the critical need for effective surge protection.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Surge Protection Device Market.- Eaton

- Siemens

- Schneider Electric

- ABB

- Emerson Electric

- Littelfuse Inc.

- Phoenix Contact

- TE Connectivity

- Leviton Manufacturing

- Hakel

- Citel

- Mersen

- Weidmüller Interface

- Hubbell Incorporated

- Raycap

- DEHN SE

- MCG Surge Protection

- Belkin International

- Tripp Lite (Eaton acquired)

- Cirprotec

Frequently Asked Questions

Analyze common user questions about the Surge Protection Device market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is a Surge Protection Device (SPD)?

A Surge Protection Device (SPD) is an electrical component designed to protect electrical equipment from voltage spikes or transient overvoltages. It diverts excess current to the ground, preventing it from reaching sensitive electronic devices and causing damage.

Why are Surge Protection Devices important?

SPDs are crucial for safeguarding valuable electronic equipment, preventing data loss, and ensuring operational continuity. They protect against damage from lightning strikes, utility switching, and internal electrical load changes, thereby extending equipment lifespan and reducing maintenance costs.

How does an SPD work?

An SPD works by acting as a short circuit to ground when a transient overvoltage exceeds a specific threshold. It diverts the surge current away from the protected equipment, and once the voltage returns to normal levels, the SPD resets to its high-impedance state, allowing normal current flow.

What are the main types of SPDs?

SPDs are typically classified into Type 1, Type 2, and Type 3. Type 1 SPDs protect against direct lightning strikes and are installed at the main service entrance. Type 2 SPDs protect against indirect lightning and switching surges, installed at sub-distribution boards. Type 3 SPDs offer localized protection for sensitive equipment, often at the point of use.

What factors are driving the growth of the SPD market?

Key drivers include the global increase in sensitive electronic equipment, the expansion of smart grid and renewable energy infrastructure, the proliferation of data centers and IoT devices, and increasingly stringent electrical safety regulations worldwide.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted