Outpatient Oncology Infusion Market

Outpatient Oncology Infusion Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_703697 | Last Updated : August 05, 2025 |

Format : ![]()

![]()

![]()

![]()

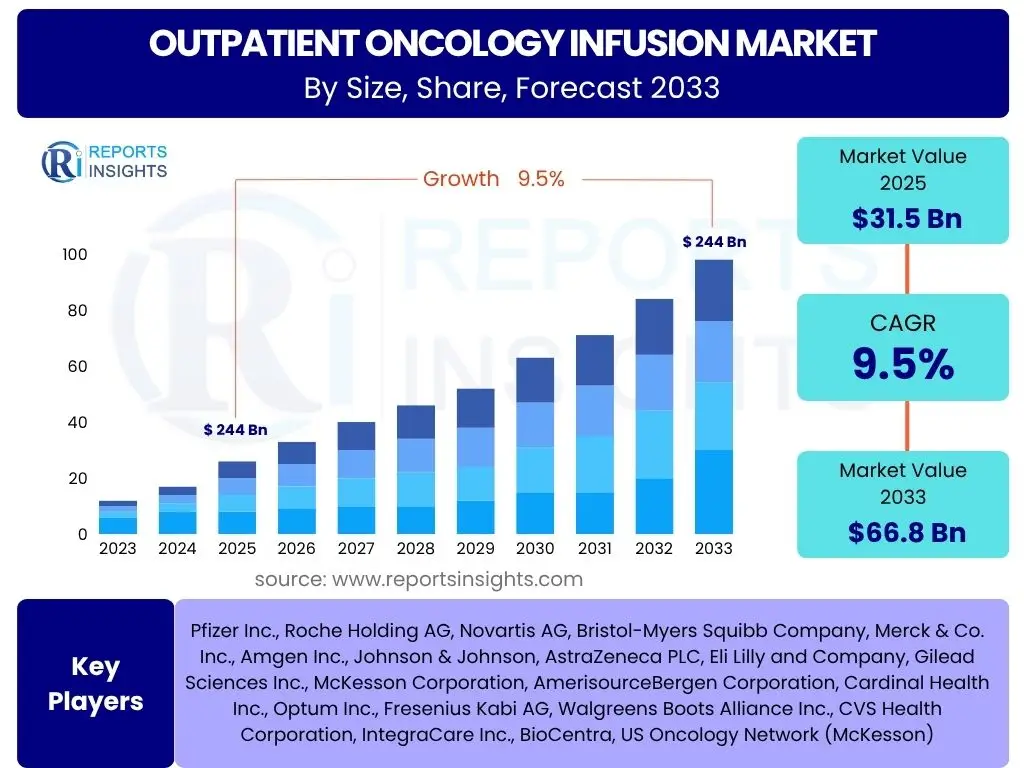

Outpatient Oncology Infusion Market Size

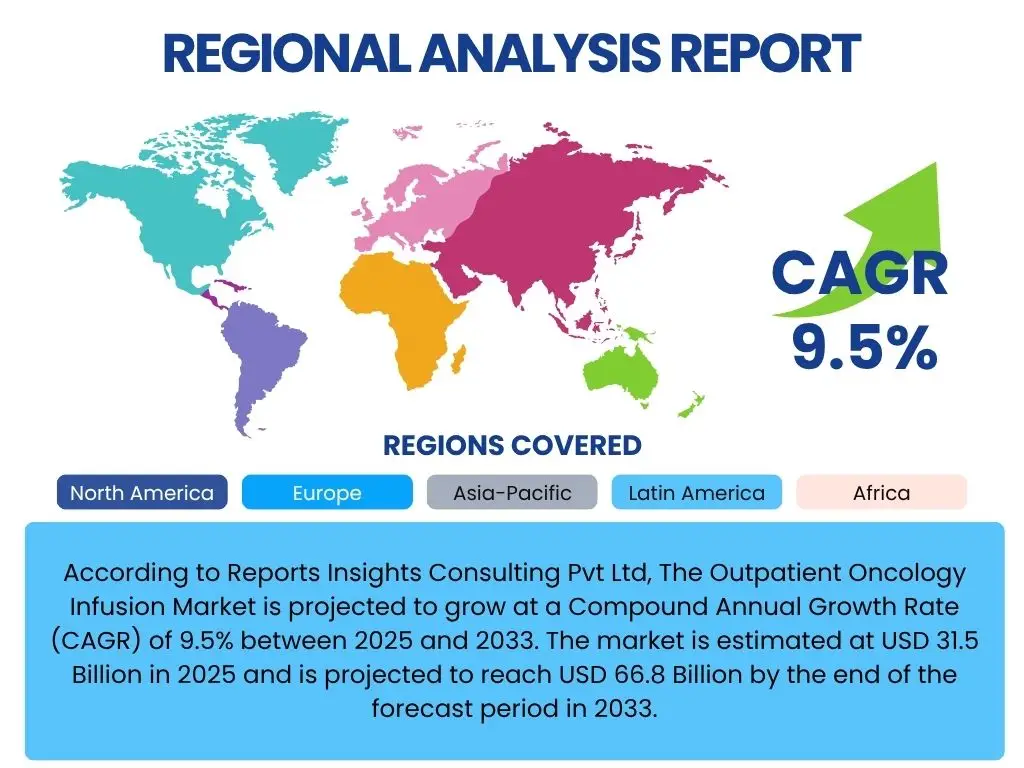

According to Reports Insights Consulting Pvt Ltd, The Outpatient Oncology Infusion Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 9.5% between 2025 and 2033. The market is estimated at USD 31.5 Billion in 2025 and is projected to reach USD 66.8 Billion by the end of the forecast period in 2033.

Key Outpatient Oncology Infusion Market Trends & Insights

The outpatient oncology infusion market is undergoing significant transformation, driven by evolving healthcare landscapes and patient preferences. A prominent trend observed is the continuous shift from inpatient to outpatient settings, primarily fueled by the cost-effectiveness and convenience offered by these facilities. Patients increasingly prefer receiving their infusion treatments in environments that are less clinical and more accessible, contributing to a higher quality of life during their treatment journey. This shift is further supported by advancements in drug formulations and delivery methods that enable safer and more efficient administration outside traditional hospital walls.

Another critical insight centers on the growing adoption of value-based care models, which emphasize outcomes and cost-efficiency. Outpatient infusion centers align well with these models by reducing overhead costs associated with inpatient stays while maintaining high standards of care. This focus on value is prompting healthcare providers to invest in specialized outpatient facilities, enhancing their infrastructure, and optimizing patient flow. Additionally, the integration of advanced technologies, such as digital health platforms and remote monitoring, is improving the efficiency of care delivery and patient management in these settings.

Furthermore, the market is seeing an expansion in the types of therapies administered in outpatient settings, extending beyond traditional chemotherapy to include complex immunotherapies and targeted therapies. This broadening scope necessitates specialized training for healthcare professionals and robust protocols to manage potential adverse events. The increasing prevalence of cancer globally and the development of new, effective therapeutic agents are continuously fueling the demand for accessible and high-quality outpatient infusion services, making this segment a crucial component of modern cancer care.

- Shift to Outpatient Settings: Growing preference for cost-effective and convenient care delivery outside hospitals.

- Advancements in Therapies: Expansion of complex immunotherapies and targeted therapies administered in outpatient settings.

- Value-Based Care Adoption: Emphasis on outcomes and cost-efficiency driving investment in specialized outpatient facilities.

- Technological Integration: Use of digital health and remote monitoring for enhanced efficiency and patient management.

- Focus on Patient Experience: Improved accessibility, comfort, and quality of life for patients undergoing treatment.

AI Impact Analysis on Outpatient Oncology Infusion

The integration of Artificial Intelligence (AI) in the outpatient oncology infusion sector holds immense potential to revolutionize operational efficiency, treatment personalization, and patient safety. Users frequently inquire about AI's role in optimizing scheduling, reducing wait times, and managing inventory in infusion centers, highlighting a strong desire for improved logistical performance. AI algorithms can analyze patient data, predict peak demand periods, and streamline resource allocation, directly addressing these operational challenges. This capability allows clinics to maximize their capacity, minimize patient inconvenience, and enhance the overall efficiency of the infusion process.

Beyond logistics, a significant area of user interest revolves around AI's capacity to personalize treatment regimens and monitor patient responses. AI-powered tools can analyze vast amounts of patient genomic, clinical, and lifestyle data to recommend the most effective and least toxic drug combinations, adjusting dosages in real-time based on predictive analytics of patient reactions. This personalization is crucial for maximizing therapeutic efficacy while minimizing adverse effects, leading to better patient outcomes and reduced healthcare costs associated with complications. The ability of AI to identify subtle patterns in patient data can also predict potential complications or non-responsiveness earlier, enabling timely intervention.

Furthermore, concerns and expectations often center on AI's contribution to enhanced safety and quality of care. Users anticipate AI systems could improve drug compounding accuracy, flag potential drug interactions, and provide real-time alerts for adverse events during infusions. AI-driven image analysis can assist in precise site selection for IV access, reducing discomfort and complications. While the adoption of AI brings forth questions regarding data security, regulatory frameworks, and the need for human oversight, the overarching sentiment is one of optimism regarding its transformative potential to elevate the standard of outpatient oncology care, making it safer, more efficient, and highly personalized.

- Operational Optimization: AI enhances scheduling, inventory management, and patient flow efficiency.

- Personalized Treatment: AI analyzes patient data for tailored drug regimens and predictive response monitoring.

- Enhanced Safety: AI improves drug compounding accuracy, flags interactions, and monitors adverse events.

- Predictive Analytics: AI forecasts demand and identifies at-risk patients for proactive intervention.

- Data-Driven Decision Making: AI supports clinicians with insights for improved therapeutic outcomes.

Key Takeaways Outpatient Oncology Infusion Market Size & Forecast

Analysis of common inquiries regarding the outpatient oncology infusion market size and forecast reveals a predominant focus on sustained growth, driven primarily by the escalating global incidence of cancer and the strategic shift towards more accessible and cost-effective care settings. Stakeholders are keen to understand the drivers behind this expansion, which notably include technological advancements enabling safer outpatient procedures, and the increasing patient preference for convenience and comfort offered by non-hospital environments. The market's projected robust CAGR signifies a significant opportunity for investment and innovation, particularly in developing new infrastructure and optimizing existing service delivery models.

Another crucial takeaway is the increasing sophistication of therapeutic options that are now amenable to outpatient administration. The market's growth is not merely volumetric but also qualitative, reflecting the evolving landscape of oncology treatments. This includes the wider application of immunotherapies, targeted therapies, and biologics, which often require careful monitoring but can be safely managed in a well-equipped outpatient setting. This expansion of treatable conditions in outpatient clinics reinforces their vital role in the cancer care continuum, reducing the burden on acute care hospitals and lowering overall healthcare expenditures.

The forecast also highlights the importance of regional disparities and the potential for growth in emerging economies. While North America and Europe currently dominate the market due to advanced healthcare infrastructure and higher cancer prevalence, Asia Pacific and Latin America are poised for accelerated growth, driven by improving healthcare access and rising awareness. These regions present significant untapped potential for expanding outpatient infusion services. Ultimately, the market trajectory indicates a future where outpatient oncology infusion centers become the primary hubs for cancer treatment, characterized by technological integration, patient-centric care, and economic efficiency, thereby reshaping the delivery of oncology services globally.

- Significant Market Growth: Robust CAGR driven by rising cancer incidence and shift to outpatient care.

- Therapeutic Advancements: Increased outpatient administration of advanced immunotherapies and targeted therapies.

- Cost-Efficiency & Convenience: Patient preference and healthcare economics favor outpatient settings.

- Regional Expansion: Strong growth potential in emerging markets, alongside established dominance in developed regions.

- Technological Integration: Automation, digital health, and AI are crucial for market evolution and efficiency.

Outpatient Oncology Infusion Market Drivers Analysis

The outpatient oncology infusion market is primarily driven by a confluence of factors that enhance accessibility, reduce costs, and improve patient experience. A key driver is the global increase in cancer incidence, which inherently expands the patient pool requiring infusion therapies. This demographic trend places pressure on healthcare systems to deliver efficient and accessible care. Coupled with this, advancements in oncology drug development have led to the creation of potent new therapies, including biologics and immunotherapies, which often require intravenous administration but are increasingly suitable for outpatient settings due to their improved safety profiles and reduced need for intensive monitoring.

Furthermore, the growing emphasis on value-based care models and cost containment strategies by payers and healthcare providers significantly boosts the shift to outpatient services. Outpatient infusion centers offer a more economical alternative to inpatient hospital stays for administering treatments, thereby reducing the overall burden on healthcare expenditures. This cost-effectiveness, combined with the convenience and comfort offered to patients—who often prefer receiving care in a less institutionalized environment closer to home—makes outpatient settings highly attractive. Policies supporting reimbursement for outpatient infusion services further incentivize this transition, creating a favorable environment for market expansion.

Technological innovations also play a pivotal role, from advanced infusion pumps that offer precision and safety, to digital health solutions for appointment scheduling, remote monitoring, and patient education. These technologies improve operational efficiency, enhance patient safety, and allow for better management of a larger patient volume. The increasing availability of highly skilled nursing staff specializing in oncology and infusion care further supports the growth of these specialized centers, ensuring high-quality treatment delivery outside traditional hospital settings.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Rising Cancer Incidence | +2.5% | Global | Long-term (2025-2033) |

| Advancements in Oncology Therapies | +2.0% | North America, Europe, Asia Pacific | Mid to Long-term (2025-2033) |

| Shift to Outpatient Care for Cost-Efficiency | +1.8% | Global, particularly Developed Markets | Mid-term (2025-2030) |

| Patient Preference for Convenience | +1.5% | Global | Long-term (2025-2033) |

| Supportive Reimbursement Policies | +1.2% | North America, Western Europe | Mid-term (2025-2030) |

| Technological Advancements in Infusion Devices | +1.0% | Global | Mid to Long-term (2025-2033) |

Outpatient Oncology Infusion Market Restraints Analysis

Despite the robust growth, the outpatient oncology infusion market faces several significant restraints that could impede its full potential. One primary challenge revolves around the complexity and stringency of regulatory and reimbursement policies. Variations in coverage across different payers and regions, coupled with the ever-changing landscape of drug pricing and administration codes, can create financial uncertainties for outpatient centers. This complexity often leads to administrative burdens, delaying patient access to care and limiting the expansion of services, particularly for smaller independent facilities that lack extensive legal and billing departments.

Another critical restraint is the ongoing shortage of specialized healthcare professionals, particularly oncology nurses and pharmacists, who are essential for safely administering and managing complex infusion therapies. The highly specialized nature of oncology treatment requires extensive training and experience, and the current supply often struggles to meet the growing demand. This shortage can lead to staffing challenges, increased operational costs due to competitive salaries, and in some cases, a compromise on the desired patient-to-staff ratios, potentially affecting the quality and safety of care delivered in outpatient settings.

Furthermore, the capital investment required to establish and maintain a state-of-the-art outpatient infusion center can be substantial. This includes costs for specialized equipment, sterile environments, advanced IT infrastructure, and compliance with stringent safety regulations. For new entrants or smaller providers, securing sufficient funding can be a major hurdle. Additionally, the risk of complications during infusions, while rare, necessitates robust emergency protocols and equipment, adding another layer of complexity and cost. Managing drug shortages and ensuring a consistent supply of expensive oncology medications also poses a logistical and financial challenge that can restrain market growth.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Complex Reimbursement Policies & Payer Coverage | -1.8% | North America, Europe | Mid to Long-term (2025-2033) |

| Shortage of Skilled Healthcare Professionals | -1.5% | Global | Long-term (2025-2033) |

| High Initial Capital Investment & Operating Costs | -1.2% | Global | Mid-term (2025-2030) |

| Drug Shortages and Supply Chain Volatility | -1.0% | Global | Short to Mid-term (2025-2028) |

| Risk of Infusion-Related Complications | -0.8% | Global | Ongoing |

| Regulatory Hurdles and Compliance Burden | -0.7% | Global | Ongoing |

Outpatient Oncology Infusion Market Opportunities Analysis

The outpatient oncology infusion market presents numerous opportunities for innovation and expansion, driven by evolving patient needs and technological advancements. A significant opportunity lies in the further integration of telehealth and remote monitoring solutions. As healthcare continues its digital transformation, leveraging virtual platforms can enhance patient engagement, facilitate pre- and post-infusion assessments, and enable timely intervention, particularly for patients in remote areas or those with mobility challenges. This not only improves patient convenience but also optimizes clinic efficiency by reducing unnecessary in-person visits and streamlining communication.

Another promising area is the expansion of home infusion services for suitable oncology patients. While currently limited for complex infusions, advancements in portable infusion pumps and improved training for home healthcare providers could unlock a substantial market segment. Administering certain therapies in the comfort of a patient's home can significantly reduce travel burden, infection risks, and associated costs, thereby improving overall quality of life during cancer treatment. This trend aligns with the broader push towards personalized and patient-centric care models, offering a highly customized treatment experience.

Furthermore, there is a considerable opportunity in developing specialized outpatient centers focusing on specific cancer types or highly specialized therapies, such as CAR T-cell therapy post-infusion monitoring. These niche centers can offer highly specialized expertise, advanced support services, and tailored environments that cater to the unique needs of these patient populations. Investing in infrastructure for these specialized services, along with expanding into emerging markets where cancer incidence is rising and healthcare infrastructure is developing, represents a long-term growth avenue. Strategic partnerships between pharmaceutical companies, technology providers, and healthcare systems can further accelerate the adoption of these innovative care delivery models.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Integration of Telehealth & Remote Monitoring | +2.2% | Global | Mid to Long-term (2025-2033) |

| Expansion of Home Infusion Services | +1.9% | North America, Europe | Long-term (2028-2033) |

| Development of Specialized Niche Infusion Centers | +1.7% | Developed Markets | Mid-term (2025-2030) |

| Geographic Expansion into Emerging Markets | +1.5% | Asia Pacific, Latin America, MEA | Long-term (2028-2033) |

| Adoption of AI & Predictive Analytics for Workflow | +1.3% | Global | Mid to Long-term (2025-2033) |

| Strategic Partnerships & Collaborations | +1.0% | Global | Ongoing |

Outpatient Oncology Infusion Market Challenges Impact Analysis

The outpatient oncology infusion market, while experiencing significant growth, is not without its inherent challenges that necessitate strategic navigation by market participants. A primary challenge involves maintaining consistent quality of care and patient safety standards across diverse outpatient settings. Unlike hospital environments with standardized protocols and readily available emergency support, outpatient centers must meticulously ensure robust safety measures, infection control, and staff training, especially when managing complex oncology treatments that carry risks of severe adverse reactions. This requires continuous investment in training, technology, and robust emergency preparedness, which can strain resources.

Another substantial challenge is managing the escalating costs of oncology drugs, which directly impacts the financial viability of outpatient infusion centers and the affordability of treatment for patients. While outpatient settings offer cost savings compared to inpatient care, the price of many novel cancer therapies remains exceptionally high, leading to significant financial burden for patients and health systems. Centers must constantly navigate complex drug procurement, inventory management, and reimbursement issues to remain sustainable, often contending with narrow profit margins on drug administration despite high drug costs.

Furthermore, operational complexities arising from increasing patient volumes, diverse treatment protocols, and the need for personalized care pose significant logistical challenges. Efficient patient scheduling, minimizing wait times, and optimizing resource utilization become critical to both patient satisfaction and clinic profitability. Cybersecurity threats to patient data and electronic health records also represent a growing concern, requiring substantial investment in secure IT infrastructure and data protection measures. Adapting to evolving regulatory landscapes, particularly concerning new drug approvals and value-based payment models, requires continuous monitoring and agile operational adjustments to ensure compliance and maintain competitive advantage.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Maintaining Quality & Safety Standards | -1.8% | Global | Ongoing |

| High Cost of Oncology Drugs & Affordability | -1.5% | Global | Long-term (2025-2033) |

| Operational Efficiency & Patient Flow Management | -1.2% | Global | Mid-term (2025-2030) |

| Data Security and Cybersecurity Risks | -1.0% | Global | Ongoing |

| Adaptation to Evolving Regulatory Environment | -0.9% | North America, Europe | Ongoing |

| Infrastructure Limitations in Developing Regions | -0.7% | Asia Pacific, Latin America, MEA | Long-term (2025-2033) |

Outpatient Oncology Infusion Market - Updated Report Scope

This report provides a comprehensive analysis of the global Outpatient Oncology Infusion Market, offering detailed insights into market dynamics, segmentation, and regional trends. It covers the historical period from 2019 to 2023, establishes a base year of 2024, and provides forecasts up to 2033, enabling stakeholders to understand past performance and project future growth trajectories. The study delves into key market drivers, restraints, opportunities, and challenges, along with a thorough impact analysis of these factors on the market's Compound Annual Growth Rate (CAGR). Additionally, the report includes a detailed profile of leading companies, regional highlights, and an extensive segmentation analysis to offer a holistic view of the market landscape.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 31.5 Billion |

| Market Forecast in 2033 | USD 66.8 Billion |

| Growth Rate | 9.5% |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Pfizer Inc., Roche Holding AG, Novartis AG, Bristol-Myers Squibb Company, Merck & Co. Inc., Amgen Inc., Johnson & Johnson, AstraZeneca PLC, Eli Lilly and Company, Gilead Sciences Inc., McKesson Corporation, AmerisourceBergen Corporation, Cardinal Health Inc., Optum Inc., Fresenius Kabi AG, Walgreens Boots Alliance Inc., CVS Health Corporation, IntegraCare Inc., BioCentra, US Oncology Network (McKesson) |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Outpatient Oncology Infusion Market is meticulously segmented to provide a granular view of its diverse components and understand the varied dynamics shaping its growth. This detailed segmentation allows for a comprehensive analysis of patient demographics, therapeutic preferences, and infrastructural variations, offering crucial insights for strategic planning and resource allocation. By breaking down the market into distinct categories, stakeholders can identify specific areas of high growth, emerging trends, and unmet needs, thereby tailoring their services and products to targeted segments.

The segmentation by type of therapy is critical as the oncology landscape evolves with the introduction of new treatments beyond traditional chemotherapy, such as immunotherapies and targeted therapies, each with unique administration requirements and patient profiles. Similarly, segmenting by cancer type helps understand the prevalence and treatment patterns for different malignancies in an outpatient setting. This allows providers to specialize and equip their centers appropriately for the most common or complex cancer types they serve. Furthermore, the segmentation by facility type reveals the shift in care settings, highlighting the growth of freestanding centers and the potential for home care.

Patient age group segmentation offers insights into the distinct needs of pediatric, adult, and geriatric populations, which often require different approaches to care, support services, and facility design. This multi-faceted segmentation provides a robust framework for assessing market opportunities and challenges, enabling a more precise understanding of the market's structure and the factors influencing its expansion across different dimensions.

- By Type of Therapy:

- Chemotherapy

- Immunotherapy

- Targeted Therapy

- Hormonal Therapy

- Others (e.g., Biologic Response Modifiers)

- By Cancer Type:

- Breast Cancer

- Lung Cancer

- Colorectal Cancer

- Prostate Cancer

- Lymphoma

- Leukemia

- Other Solid Tumors

- Hematologic Malignancies

- By Facility Type:

- Hospital-Associated Outpatient Clinics

- Freestanding Infusion Centers

- Physician Offices

- Home Care Settings

- By Patient Age Group:

- Pediatric

- Adult

- Geriatric

Regional Highlights

- North America: Dominates the outpatient oncology infusion market due to advanced healthcare infrastructure, high cancer incidence, favorable reimbursement policies, and a strong preference for outpatient care settings. The U.S. leads in adoption of novel therapies and technological integration.

- Europe: A mature market characterized by increasing adoption of outpatient services, driven by cost-containment efforts and an aging population. Western European countries like Germany, France, and the UK are key contributors, focusing on optimizing patient pathways and integrated care networks.

- Asia Pacific (APAC): Expected to exhibit the highest growth rate, fueled by rising cancer prevalence, improving healthcare access, growing medical tourism, and increasing investment in healthcare infrastructure, particularly in countries like China, India, and Japan.

- Latin America: Demonstrates significant growth potential, attributed to expanding healthcare expenditure, increasing awareness about early cancer detection, and the development of specialized outpatient facilities, though challenges exist in terms of widespread access and reimbursement.

- Middle East and Africa (MEA): Emerging as a nascent market with promising opportunities, driven by increasing healthcare investments, improving economic conditions, and rising demand for specialized oncology care. Collaboration and private sector involvement are key to unlocking its potential.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Outpatient Oncology Infusion Market.- Pfizer Inc.

- Roche Holding AG

- Novartis AG

- Bristol-Myers Squibb Company

- Merck & Co. Inc.

- Amgen Inc.

- Johnson & Johnson

- AstraZeneca PLC

- Eli Lilly and Company

- Gilead Sciences Inc.

- McKesson Corporation

- AmerisourceBergen Corporation

- Cardinal Health Inc.

- Optum Inc.

- Fresenius Kabi AG

- Walgreens Boots Alliance Inc.

- CVS Health Corporation

- IntegraCare Inc.

- BioCentra

- US Oncology Network (McKesson)

Frequently Asked Questions

Analyze common user questions about the Outpatient Oncology Infusion market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is the projected growth rate for the Outpatient Oncology Infusion Market?

The Outpatient Oncology Infusion Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 9.5% between 2025 and 2033, reflecting robust expansion driven by increasing cancer incidence and a shift towards outpatient care.

What are the primary drivers of growth in the Outpatient Oncology Infusion Market?

Key growth drivers include the rising global incidence of cancer, advancements in oncology therapies, the strategic shift towards cost-effective outpatient care, increasing patient preference for convenience, and supportive reimbursement policies.

How is Artificial Intelligence impacting outpatient oncology infusion services?

AI is significantly impacting the market by optimizing operational efficiency (e.g., scheduling, inventory), enabling personalized treatment plans, enhancing patient safety through predictive analytics and error reduction, and improving overall care quality.

Which regions are expected to show the most significant growth in this market?

While North America and Europe currently dominate, the Asia Pacific region is anticipated to exhibit the highest growth rate due to improving healthcare infrastructure, rising cancer prevalence, and increasing access to advanced treatments.

What are the main challenges facing the Outpatient Oncology Infusion Market?

Major challenges include complex and varying reimbursement policies, the ongoing shortage of specialized healthcare professionals, high initial capital investment costs, the high price of oncology drugs, and the need to maintain stringent quality and safety standards.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted