Structural Heart Device Market

Structural Heart Device Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_705907 | Last Updated : August 17, 2025 |

Format : ![]()

![]()

![]()

![]()

Structural Heart Device Market Size

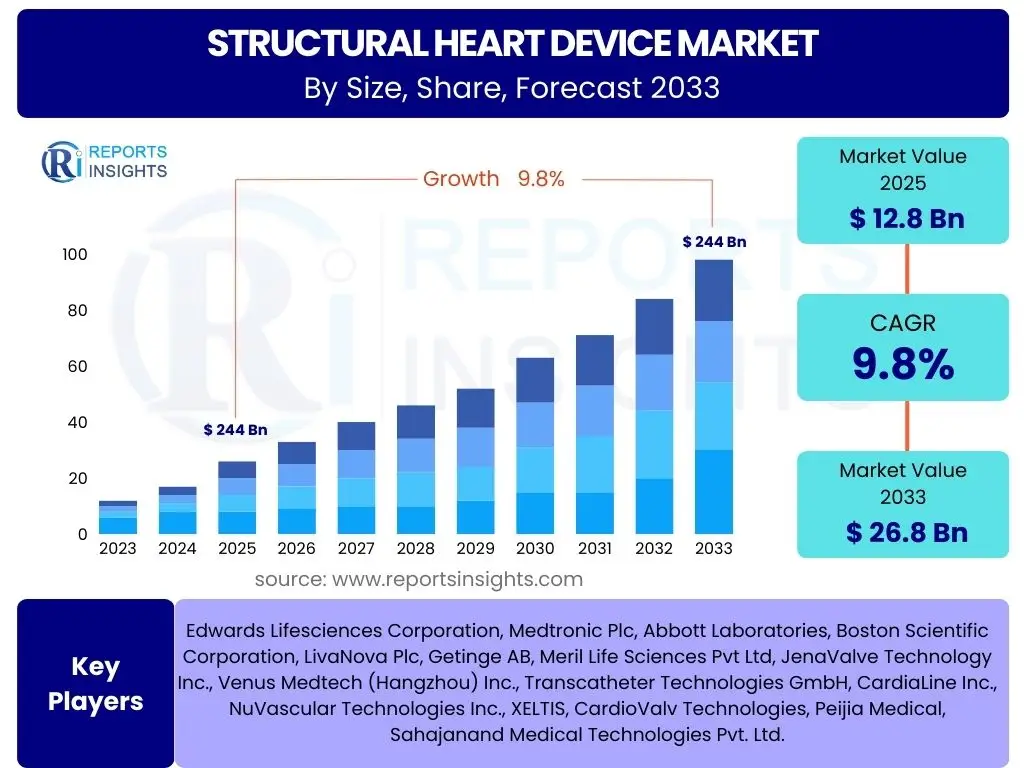

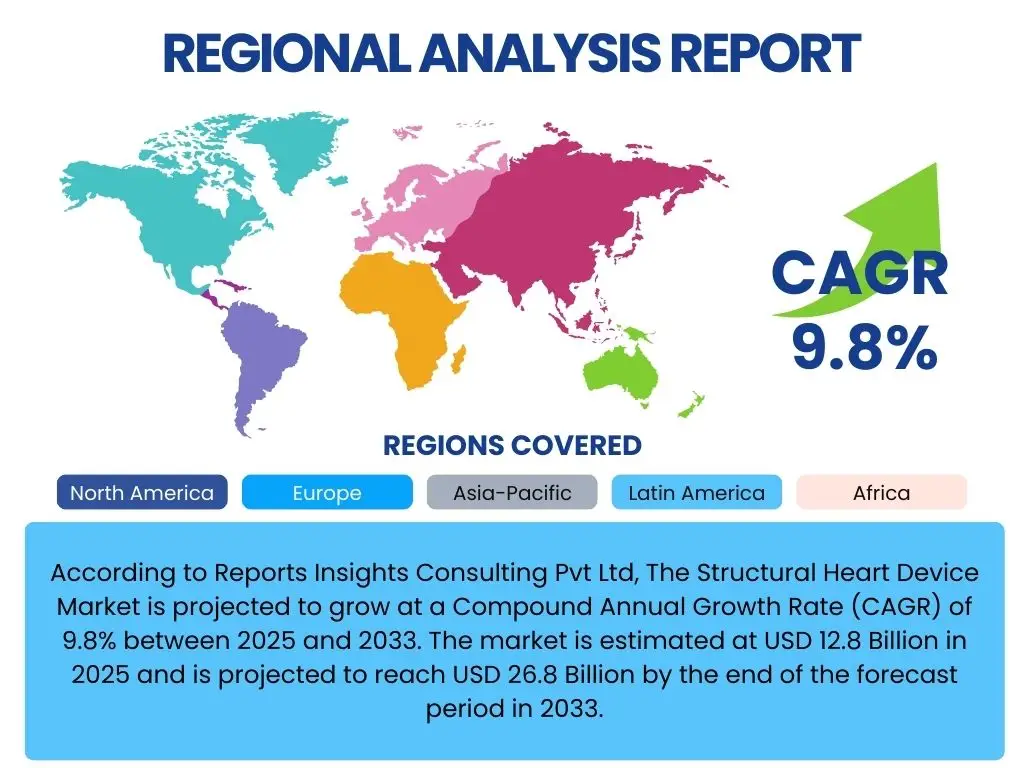

According to Reports Insights Consulting Pvt Ltd, The Structural Heart Device Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 9.8% between 2025 and 2033. The market is estimated at USD 12.8 Billion in 2025 and is projected to reach USD 26.8 Billion by the end of the forecast period in 2033.

Key Structural Heart Device Market Trends & Insights

The structural heart device market is currently experiencing significant transformative trends driven by advancements in medical technology, an aging global population, and a rising incidence of cardiovascular diseases. A key theme emerging from industry analysis is the strong shift towards minimally invasive procedures, which offer numerous benefits over traditional open-heart surgeries, including reduced recovery times, lower complication rates, and enhanced patient comfort. This procedural evolution is not merely a preference but a strategic direction for device manufacturers, who are continually innovating to develop more sophisticated and easier-to-deploy transcatheter solutions. Concurrently, the increasing focus on early diagnosis and intervention, coupled with a deeper understanding of complex cardiac anatomies, is propelling the demand for more precise and adaptable device designs. The market also observes a growing emphasis on personalized medicine, where devices are tailored to individual patient needs, leading to improved clinical outcomes and greater overall treatment efficacy.

Furthermore, the integration of advanced imaging modalities and artificial intelligence is enhancing procedural accuracy and expanding the pool of eligible patients for transcatheter interventions. As healthcare systems globally strive for cost-effectiveness and improved patient pathways, the structural heart device market is responding with innovations that enable procedures to be performed in a wider range of settings, potentially moving beyond large academic centers. There is also a notable trend towards developing next-generation devices that address specific, previously underserved patient populations or conditions, such as challenging mitral or tricuspid valve pathologies. The convergence of these trends suggests a dynamic market poised for sustained growth, characterized by continuous innovation aimed at expanding treatment options and improving patient quality of life.

- Shift towards minimally invasive transcatheter procedures.

- Rising adoption of advanced imaging techniques for procedure guidance.

- Increasing prevalence of structural heart diseases globally.

- Development of next-generation valve repair and replacement devices.

- Growing focus on personalized treatment approaches and device customization.

AI Impact Analysis on Structural Heart Device

Artificial intelligence is progressively transforming the structural heart device landscape, with its impact spanning diagnostics, surgical planning, and post-procedural care. Users frequently inquire about AI's role in improving diagnostic accuracy, optimizing device selection, and enhancing procedural precision. AI-powered algorithms are enabling more accurate and rapid analysis of medical images, such as echocardiograms and CT scans, facilitating earlier detection of structural heart defects and precise anatomical mapping crucial for interventional procedures. This capability reduces human error and provides comprehensive data for clinicians, leading to more informed treatment decisions. Furthermore, AI is being explored for predictive modeling, identifying patients at higher risk for complications or those who would benefit most from specific device interventions, thereby personalizing treatment pathways.

In the realm of procedural execution, AI is contributing to advancements in robotic-assisted surgery and real-time guidance systems, making complex transcatheter procedures safer and more efficient. It assists in precise device positioning and deployment by analyzing vast datasets of patient anatomies and past procedural outcomes. Beyond the operating room, AI is instrumental in post-operative monitoring, leveraging wearable devices and continuous data streams to detect potential complications early and optimize patient recovery protocols. While the integration of AI presents significant opportunities for enhanced precision, improved patient outcomes, and reduced healthcare costs, it also introduces considerations around data privacy, regulatory frameworks, and the need for rigorous validation to ensure clinical efficacy and safety. The ongoing development of robust AI solutions is poised to significantly augment the capabilities of structural heart devices, making interventions more accessible and effective.

- Enhanced diagnostic accuracy through AI-powered image analysis.

- Optimized surgical planning and device selection via predictive algorithms.

- Real-time procedural guidance improving precision and safety.

- Personalized patient risk stratification and treatment pathway optimization.

- Automation of data analysis for post-operative monitoring and long-term follow-up.

Key Takeaways Structural Heart Device Market Size & Forecast

The structural heart device market is poised for robust expansion over the forecast period, driven by an escalating global burden of structural heart diseases and significant advancements in transcatheter technologies. A critical takeaway is the increasing shift from traditional surgical interventions to less invasive transcatheter procedures, which are fundamentally reshaping treatment paradigms. This procedural evolution not only enhances patient outcomes and reduces recovery times but also expands the addressable patient population, including those previously deemed high-risk for open-heart surgery. Furthermore, the market's growth is inherently linked to demographic trends, specifically the aging global population, as structural heart conditions predominantly affect older individuals. Continuous research and development by key market players are leading to the introduction of novel devices and expanded indications, further fueling market momentum.

Another significant insight is the heightened investment in clinical trials and regulatory approvals, underscoring the commitment of manufacturers to expand market access for innovative solutions across diverse geographies. The Asia Pacific region, in particular, emerges as a high-growth area, propelled by improving healthcare infrastructure, rising awareness, and a large patient pool. Despite the promising outlook, the market will need to navigate challenges such as the high cost of devices and procedures, complex reimbursement policies, and the need for specialized training for healthcare professionals. Overall, the market trajectory indicates a future where structural heart interventions become more precise, accessible, and personalized, significantly improving the quality of life for millions affected by these conditions.

- Significant market growth driven by technological advancements and rising disease prevalence.

- Dominance and rapid adoption of minimally invasive transcatheter procedures.

- Aging global population remains a primary demographic driver.

- Increasing research and development efforts are expanding device portfolios and indications.

- Asia Pacific anticipated as a key growth region due to unmet needs and improving healthcare access.

Structural Heart Device Market Drivers Analysis

The structural heart device market is propelled by a confluence of powerful drivers, primarily the escalating global prevalence of structural heart diseases such as aortic stenosis, mitral regurgitation, and congenital heart defects. These conditions are increasingly diagnosed due to improved awareness, diagnostic technologies, and an aging population, which is inherently more susceptible to degenerative heart valve disorders. The demographic shift towards an older global population directly correlates with a higher incidence of these diseases, thereby creating a sustained demand for effective treatment solutions. Furthermore, advancements in medical technology, particularly in minimally invasive transcatheter procedures, have revolutionized treatment options, making interventions accessible to a wider patient demographic, including those considered high-risk for traditional open-heart surgery. These innovations offer substantial benefits such as reduced recovery times, lower hospital stays, and decreased patient morbidity, accelerating their adoption across healthcare systems globally.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Prevalence of Structural Heart Diseases | +2.5% | Global, particularly North America, Europe, Asia Pacific | Short to Long-term (2025-2033) |

| Aging Global Population | +2.0% | Global, especially Developed Nations (NA, Europe) | Long-term (2025-2033) |

| Technological Advancements in Minimally Invasive Procedures | +2.3% | Global, with rapid adoption in Developed Nations | Short to Mid-term (2025-2029) |

| Rising Awareness and Early Diagnosis | +1.5% | Emerging Markets (APAC, LATAM), Developed Nations | Mid to Long-term (2027-2033) |

Structural Heart Device Market Restraints Analysis

Despite significant growth potential, the structural heart device market faces several notable restraints that could temper its expansion. One primary concern is the high cost associated with structural heart procedures and the devices themselves. These advanced technologies, while clinically beneficial, often come with a substantial price tag, making them less accessible in developing regions or healthcare systems with limited budgets. This economic barrier can limit patient access and put pressure on reimbursement policies, delaying wider adoption. Furthermore, the stringent and complex regulatory approval processes for novel structural heart devices pose a significant hurdle. Gaining regulatory clearance in major markets like the U.S. (FDA) and Europe (CE Mark) requires extensive clinical trials, substantial investment, and considerable time, slowing down the market entry of innovative products. These rigorous approval pathways ensure patient safety and device efficacy but also create a challenging environment for manufacturers.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Cost of Devices and Procedures | -1.8% | Global, particularly developing and cost-sensitive markets | Short to Mid-term (2025-2029) |

| Stringent Regulatory Approval Processes | -1.5% | North America, Europe | Short to Mid-term (2025-2029) |

| Lack of Skilled Professionals and Infrastructure | -1.2% | Emerging Markets (APAC, LATAM, MEA) | Long-term (2027-2033) |

| Risk of Device-Related Complications | -0.8% | Global | Short to Mid-term (2025-2029) |

Structural Heart Device Market Opportunities Analysis

The structural heart device market presents significant opportunities for growth and innovation. A key opportunity lies in the substantial unmet needs within emerging economies, particularly in Asia Pacific and Latin America, where a large patient population, improving healthcare infrastructure, and increasing disposable incomes are creating fertile ground for market expansion. These regions are witnessing a rapid adoption of advanced medical technologies as awareness about structural heart diseases grows and access to specialized cardiac care improves. The expansion of indications for existing devices, such as the use of TAVR in younger, lower-risk patients, represents another crucial opportunity. Clinical trials demonstrating the safety and efficacy of transcatheter procedures for broader patient populations are paving the way for wider market penetration and increased procedure volumes.

Furthermore, the continuous development of novel and more refined devices, including those for mitral and tricuspid valve repair/replacement, offers considerable growth avenues. Companies are investing heavily in R&D to address complex valve pathologies that are currently underserved or require highly invasive surgical interventions. Strategic collaborations and partnerships between device manufacturers, academic institutions, and healthcare providers are also fostering innovation and accelerating market access. The growing focus on early intervention and preventive care within healthcare systems worldwide also contributes to expanding the pool of patients eligible for structural heart interventions. These combined factors highlight a robust opportunity landscape for the structural heart device market, driven by both geographical expansion and therapeutic innovation.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Untapped Markets in Emerging Economies | +1.7% | Asia Pacific, Latin America, Middle East & Africa | Mid to Long-term (2027-2033) |

| Expansion of Indication for Existing Devices | +1.5% | North America, Europe | Short to Mid-term (2025-2029) |

| Development of Novel Mitral and Tricuspid Valve Devices | +1.3% | Global | Mid to Long-term (2027-2033) |

| Increasing Focus on Early Diagnosis and Intervention | +1.0% | Global | Short to Long-term (2025-2033) |

Structural Heart Device Market Challenges Impact Analysis

The structural heart device market faces several intrinsic challenges that could influence its growth trajectory. One significant challenge is the ongoing complexity of reimbursement policies across different regions and healthcare systems. The high cost of structural heart devices and procedures necessitates robust and consistent reimbursement frameworks to ensure widespread adoption. Inconsistent or insufficient reimbursement can deter hospitals and patients from opting for these advanced therapies, particularly in value-based care environments. Furthermore, the competitive landscape is intense, with several established players and emerging innovators vying for market share. This intense competition drives innovation but also puts pressure on pricing and necessitates continuous differentiation and strong clinical evidence for new products. Product recalls, while rare, also pose a significant challenge, impacting patient trust, company reputation, and financial performance.

Another challenge stems from the requirement for highly specialized training and infrastructure. Performing complex transcatheter structural heart procedures demands significant expertise from interventional cardiologists, cardiac surgeons, and support staff, along with state-of-the-art cath labs and hybrid operating rooms. The limited availability of such specialized personnel and facilities, especially in developing regions, can constrain market penetration. Moreover, the long-term durability and efficacy data for some of the newer transcatheter devices are still evolving, leading to some caution among clinicians and payers regarding their widespread, long-term application. Addressing these challenges requires collaborative efforts from manufacturers, healthcare providers, and regulatory bodies to ensure broader access, sustained innovation, and patient confidence in structural heart interventions.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Complex and Evolving Reimbursement Policies | -1.6% | Global, particularly North America, Europe | Short to Mid-term (2025-2029) |

| Intense Competition and Pricing Pressures | -1.4% | Global | Short to Mid-term (2025-2029) |

| Need for Specialized Training and Infrastructure | -1.0% | Emerging Markets, specific regions within Developed Nations | Long-term (2027-2033) |

| Post-Market Surveillance and Product Recalls | -0.7% | Global | Short-term (2025-2027) |

Structural Heart Device Market - Updated Report Scope

This comprehensive report provides an in-depth analysis of the global structural heart device market, offering critical insights into its current landscape, future growth projections, and key influencing factors. It segments the market extensively by product, procedure, and end-use, delivering a granular view of market dynamics. The report incorporates historical data and robust forecasting methodologies to project market size, growth rates, and emerging opportunities and challenges through 2033. Furthermore, it includes a detailed regional analysis and profiles of leading market players, equipping stakeholders with actionable intelligence for strategic decision-making. The scope encompasses detailed examination of market drivers, restraints, opportunities, and challenges, along with an impact analysis of artificial intelligence on the industry. This report is designed to assist businesses, investors, and healthcare professionals in understanding the complex dynamics of the structural heart device market and identifying lucrative avenues for growth and investment.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 12.8 Billion |

| Market Forecast in 2033 | USD 26.8 Billion |

| Growth Rate | 9.8% |

| Number of Pages | 265 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Edwards Lifesciences Corporation, Medtronic Plc, Abbott Laboratories, Boston Scientific Corporation, LivaNova Plc, Getinge AB, Meril Life Sciences Pvt Ltd, JenaValve Technology Inc., Venus Medtech (Hangzhou) Inc., Transcatheter Technologies GmbH, CardiaLine Inc., NuVascular Technologies Inc., XELTIS, CardioValv Technologies, Peijia Medical, Sahajanand Medical Technologies Pvt. Ltd. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The structural heart device market is comprehensively segmented to provide a detailed understanding of its diverse components and dynamics. This segmentation facilitates a granular analysis of market trends, adoption rates, and growth opportunities across various product categories, procedural applications, and end-use environments. The product segment includes different types of heart valves and repair devices, reflecting the breadth of therapeutic options available for structural heart conditions. Within the product segment, transcatheter heart valves are anticipated to maintain significant dominance due to the increasing preference for minimally invasive procedures and the expanding indications for their use. The market is further analyzed based on the specific procedures performed, highlighting the growing adoption of transcatheter techniques over traditional surgical interventions. This procedural shift is a key driver for market growth, emphasizing the efficiency and reduced invasiveness of modern techniques. Each segment provides unique insights into demand patterns and technological advancements.

Moreover, the market is categorized by end-use facilities, which include hospitals, ambulatory surgical centers, and specialty clinics. Hospitals currently account for the largest share, primarily due to the complex nature of structural heart procedures requiring extensive infrastructure and specialized personnel. However, the emergence of ambulatory surgical centers and specialty clinics for less complex procedures represents a growing trend, offering more accessible and potentially cost-effective care. This multi-faceted segmentation allows for a precise evaluation of market performance, competitive landscape, and strategic planning, providing stakeholders with valuable insights into the most lucrative areas for investment and expansion within the global structural heart device market.

- By Product:

- Transcatheter Heart Valves (TAVR, TMVR, TPVR)

- Surgical Heart Valves (Mechanical Heart Valves, Biological Heart Valves)

- Annuloplasty Rings

- Occlusion Devices (ASD, VSD, PFO)

- Repair Devices (Surgical, Transcatheter)

- By Procedure:

- Transcatheter Aortic Valve Replacement (TAVR)

- Transcatheter Mitral Valve Repair/Replacement (TMVR/TMR)

- Transcatheter Pulmonary Valve Replacement (TPVR)

- Transcatheter Tricuspid Valve Repair/Replacement (TTVR/TTR)

- Surgical Valve Replacement

- Congenital Heart Defect Closure

- Left Atrial Appendage Closure (LAAC)

- By End-Use:

- Hospitals

- Ambulatory Surgical Centers

- Specialty Clinics

Regional Highlights

- North America: This region holds the largest share of the structural heart device market, primarily due to the high prevalence of structural heart diseases, advanced healthcare infrastructure, significant R&D investments by key players, and favorable reimbursement policies. The U.S. remains a dominant country, driven by early adoption of innovative technologies and a large geriatric population.

- Europe: Europe represents a mature market with a strong emphasis on clinical research and technological adoption. Countries like Germany, France, and the UK are key contributors, benefiting from an aging population, rising awareness, and increasing healthcare expenditure. The market is influenced by well-established regulatory pathways and a focus on cost-effectiveness.

- Asia Pacific (APAC): Expected to be the fastest-growing region during the forecast period. This growth is attributed to a large and expanding patient pool, improving healthcare infrastructure, increasing medical tourism, rising disposable incomes, and growing awareness regarding structural heart diseases. China, Japan, and India are emerging as significant markets due to their large populations and healthcare advancements.

- Latin America: The market in Latin America is characterized by increasing government initiatives to improve healthcare access, a growing prevalence of cardiovascular diseases, and developing medical infrastructure. Brazil and Mexico are leading the regional market, although challenges such as economic instability and healthcare disparities persist.

- Middle East and Africa (MEA): This region is projected to witness steady growth, driven by increasing healthcare investments, a rising incidence of cardiovascular diseases, and efforts to modernize healthcare facilities. Countries like Saudi Arabia, UAE, and South Africa are emerging as promising markets, though market penetration remains lower compared to developed regions.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Structural Heart Device Market.- Edwards Lifesciences Corporation

- Medtronic Plc

- Abbott Laboratories

- Boston Scientific Corporation

- LivaNova Plc

- Getinge AB

- Meril Life Sciences Pvt Ltd

- JenaValve Technology Inc.

- Venus Medtech (Hangzhou) Inc.

- Transcatheter Technologies GmbH

- CardiaLine Inc.

- NuVascular Technologies Inc.

- XELTIS

- CardioValv Technologies

- Peijia Medical

- Sahajanand Medical Technologies Pvt. Ltd.

Frequently Asked Questions

What is the projected growth rate for the Structural Heart Device Market?

The Structural Heart Device Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 9.8% between 2025 and 2033, driven by technological advancements and increasing disease prevalence.

Which factors are primarily driving the growth of the Structural Heart Device Market?

Key drivers include the rising global prevalence of structural heart diseases, an aging population, and significant advancements in minimally invasive transcatheter procedures that offer improved patient outcomes and reduced recovery times.

How is artificial intelligence impacting the Structural Heart Device industry?

AI is transforming the industry by enhancing diagnostic accuracy, optimizing surgical planning through precise image analysis, and providing real-time guidance during procedures, leading to more personalized and effective treatments.

What are the main challenges faced by the Structural Heart Device Market?

Major challenges include the high cost of devices and procedures, complex and evolving reimbursement policies, stringent regulatory approval processes, and the significant need for highly specialized training and advanced healthcare infrastructure.

Which geographical region is expected to lead the Structural Heart Device Market?

North America currently holds the largest market share due to advanced healthcare infrastructure and high disease prevalence, while the Asia Pacific region is anticipated to be the fastest-growing market during the forecast period.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted