Ophthalmology Device Market

Ophthalmology Device Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_710242 | Last Updated : January 02, 2026 |

Format : ![]()

![]()

![]()

![]()

Ophthalmology Device Market Size

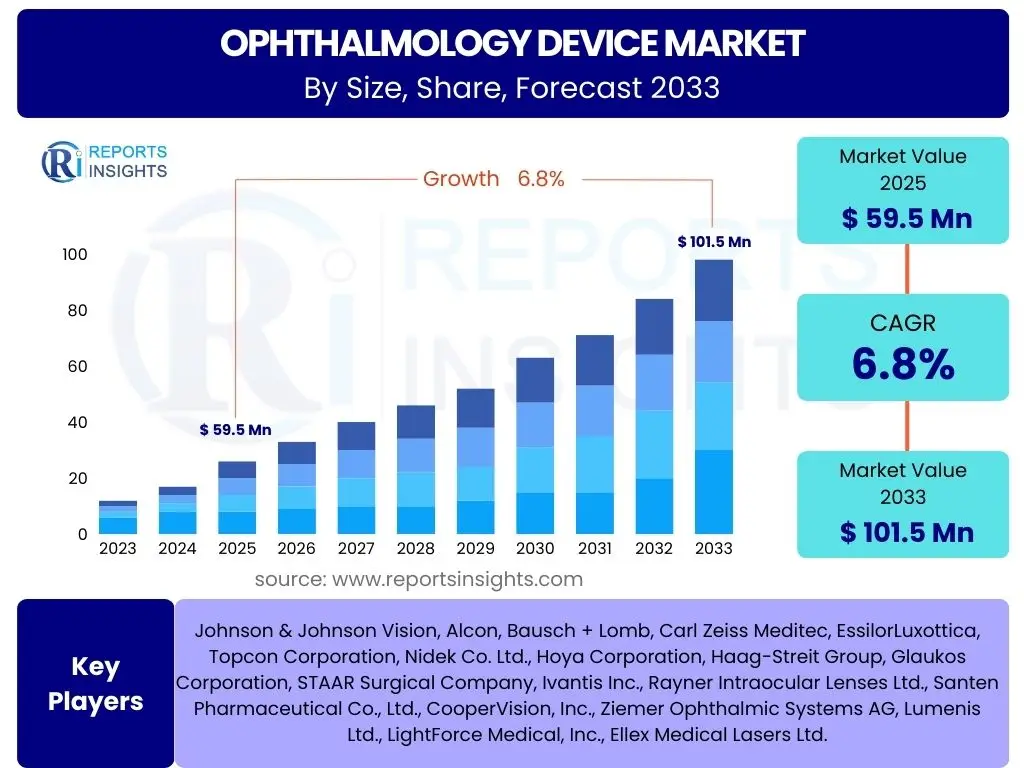

According to Reports Insights Consulting Pvt Ltd, The Ophthalmology Device Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2025 and 2033. The market is estimated at USD 59.5 billion in 2025 and is projected to reach USD 101.5 billion by the end of the forecast period in 2033.

Key Ophthalmology Device Market Trends & Insights

The ophthalmology device market is experiencing transformative growth, driven by a convergence of technological innovation, demographic shifts, and evolving patient demands. Key trends indicate a strong focus on enhancing diagnostic precision, improving surgical outcomes with minimally invasive techniques, and expanding access to eye care through digital platforms. Patients and practitioners are increasingly seeking solutions that offer greater accuracy, faster recovery times, and personalized treatment approaches, which is spurring significant research and development investments across the industry.

Furthermore, the integration of advanced technologies such as artificial intelligence and machine learning is not merely an incremental improvement but a foundational shift in how ophthalmic conditions are diagnosed and managed. This trend supports earlier detection of diseases like glaucoma and diabetic retinopathy, often before symptoms manifest significantly, allowing for more timely interventions. Manufacturers are also prioritizing user-friendly and portable devices to cater to a broader range of clinical settings, from large hospitals to remote clinics, thereby democratizing access to specialized eye care services.

The emphasis on preventive care and early intervention is also shaping market dynamics, with a growing demand for screening tools and monitoring devices. This proactive approach aims to reduce the burden of chronic eye diseases, improving long-term patient outcomes and quality of life. The market's trajectory reflects a concerted effort to leverage sophisticated engineering and digital capabilities to address complex ophthalmological challenges effectively.

- Advanced diagnostic imaging for early disease detection.

- Minimally invasive surgical techniques leading to faster recovery.

- Integration of artificial intelligence and machine learning for enhanced analytics.

- Expansion of tele-ophthalmology for remote consultations and monitoring.

- Development of smart contact lenses and ocular wearables.

- Personalized treatment approaches based on genetic and clinical data.

AI Impact Analysis on Ophthalmology Device

The integration of artificial intelligence (AI) and machine learning (ML) is profoundly reshaping the ophthalmology device landscape, addressing common user questions about how technology can improve diagnostic accuracy, treatment efficacy, and operational efficiency. AI algorithms are becoming indispensable for analyzing vast datasets from imaging modalities like Optical Coherence Tomography (OCT) and fundus photography, enabling automated detection and classification of various eye conditions such as diabetic retinopathy, glaucoma, and age-related macular degeneration. This capability not only reduces human error but also provides clinicians with objective, data-driven insights, often leading to earlier and more precise diagnoses, thereby improving patient outcomes significantly.

User expectations for AI in ophthalmology revolve around its potential to streamline clinical workflows and personalize patient care. AI-powered systems can prioritize urgent cases, assist in surgical planning, and predict disease progression, allowing ophthalmologists to allocate their resources more effectively. While concerns about data privacy, algorithmic bias, and the ethical implications of autonomous decision-making exist, the overwhelming sentiment is one of optimism regarding AI's ability to augment human expertise and revolutionize ocular health management. The focus is on developing AI tools that are transparent, validated, and seamlessly integrated into existing clinical practices, enhancing rather than replacing the human element.

Furthermore, AI is expected to play a crucial role in the development of next-generation diagnostic and therapeutic devices. From smart sensors embedded in contact lenses that monitor intraocular pressure to AI-driven drug discovery platforms targeting ocular diseases, the scope of AI's influence is expanding rapidly. This technological convergence promises to unlock new avenues for treatment and prevention, fundamentally altering how eye care is delivered and experienced globally. The future of ophthalmology is inextricably linked with advancements in AI, promising more accessible, accurate, and personalized care.

- Enhanced diagnostic accuracy and early detection of diseases like diabetic retinopathy and glaucoma through automated image analysis.

- Personalized treatment recommendations based on individual patient data and predictive analytics.

- Optimized surgical planning and real-time guidance during complex ophthalmic procedures.

- Improved clinical workflow efficiency by automating routine tasks and prioritizing patient cases.

- Support for drug discovery and development for novel ocular therapies.

- Expansion of tele-ophthalmology capabilities with AI-assisted remote screening and monitoring.

Key Takeaways Ophthalmology Device Market Size & Forecast

The ophthalmology device market is poised for robust expansion, driven by a confluence of factors that address critical user questions regarding growth trajectories and influential market dynamics. A primary takeaway is the relentless progression in medical technology, particularly in diagnostic imaging and surgical instrumentation, which continually elevates the standard of care for ocular conditions. This technological push not only creates new market segments but also fuels demand for advanced, more effective solutions, ensuring sustained growth throughout the forecast period. The global increase in an aging population, coupled with the rising prevalence of chronic eye diseases, underpins the fundamental demand for ophthalmology devices, solidifying the market's long-term stability and growth prospects.

Another significant insight derived from market analysis is the increasing importance of emerging economies as growth engines. While developed regions continue to represent substantial market share due to established healthcare infrastructures and higher disposable incomes, countries in Asia Pacific and Latin America are expected to exhibit accelerated growth rates. This is attributable to improving healthcare access, increasing awareness of eye health, and expanding healthcare expenditures in these regions. Companies are strategically focusing on these markets, tailoring products and services to meet specific regional needs and regulatory frameworks.

The emphasis on preventive care and the shift towards less invasive procedures also stand out as critical market drivers. Patients and healthcare providers are actively seeking solutions that offer quicker recovery times, reduced discomfort, and lower risks. This demand is propelling innovation in areas such as minimally invasive glaucoma surgery (MIGS) devices and advanced intraocular lenses (IOLs), which are becoming standard options in cataract surgery. Understanding these core drivers is essential for stakeholders to capitalize on the market's significant potential and strategic opportunities over the coming years.

- Substantial market growth driven by technological advancements and an aging global population.

- Emerging economies, particularly in Asia Pacific, are key regions for future market expansion.

- Increased focus on preventive eye care and early disease detection.

- Growing adoption of minimally invasive surgical techniques across various ophthalmic procedures.

- Integration of digital health solutions and tele-ophthalmology for improved accessibility.

- Rising prevalence of chronic eye diseases, including cataracts, glaucoma, and diabetic retinopathy, fuels demand.

Ophthalmology Device Market Drivers Analysis

The ophthalmology device market is significantly propelled by several robust drivers, primarily the escalating global prevalence of chronic eye conditions. Diseases such as cataracts, glaucoma, diabetic retinopathy, and age-related macular degeneration are becoming more widespread, largely due to an aging global population and lifestyle changes associated with metabolic disorders. This demographic shift creates an inherent and sustained demand for diagnostic tools, surgical instruments, and vision correction devices. Healthcare systems worldwide are increasingly focused on managing these conditions effectively, stimulating investment in advanced ophthalmic technologies to improve patient outcomes and quality of life.

Technological advancements represent another critical driver, with continuous innovation pushing the boundaries of what is possible in eye care. Breakthroughs in imaging technologies, such as Optical Coherence Tomography (OCT) and advanced fundus cameras, enable earlier and more accurate diagnoses. Similarly, the evolution of surgical techniques, including femtosecond laser-assisted cataract surgery and minimally invasive glaucoma surgery (MIGS), offers improved precision, faster recovery times, and reduced complication rates. These innovations not only expand the treatment options available but also drive the replacement of older, less efficient devices, thereby maintaining market dynamism.

Furthermore, rising healthcare expenditure and increasing awareness of eye health, particularly in developing regions, are contributing significantly to market growth. As disposable incomes grow and access to healthcare improves, more individuals are seeking specialized eye care. Public health initiatives and educational campaigns are also playing a role in highlighting the importance of regular eye examinations and early intervention for various ocular diseases. This growing awareness translates into higher demand for diagnostic screenings, preventive measures, and corrective treatments, establishing a strong foundation for the ophthalmology device market's sustained expansion.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Prevalence of Eye Diseases (Cataracts, Glaucoma, DR, AMD) | +1.8% | Global, particularly Asia Pacific & Europe | Short to Long Term (2025-2033) |

| Aging Global Population | +1.5% | Global, particularly North America & Europe | Long Term (2025-2033) |

| Technological Advancements in Diagnostics & Surgery | +1.3% | Global, particularly Developed Markets | Short to Medium Term (2025-2029) |

| Rising Healthcare Expenditure & Awareness | +1.2% | Emerging Markets (Asia Pacific, Latin America) | Medium to Long Term (2027-2033) |

| Growing Demand for Minimally Invasive Procedures | +1.0% | Global, particularly North America & Europe | Short to Medium Term (2025-2029) |

| Expansion of Digital Health & Tele-ophthalmology | +0.8% | Global, particularly Rural & Remote Areas | Short Term (2025-2027) |

Ophthalmology Device Market Restraints Analysis

Despite robust growth drivers, the ophthalmology device market faces significant restraints that can impede its full potential. One prominent challenge is the high cost associated with advanced ophthalmic devices, particularly sophisticated diagnostic equipment and surgical lasers. These substantial capital investments can be prohibitive for smaller clinics, hospitals in developing regions, or even larger institutions operating under tight budget constraints. The high initial purchase price, coupled with ongoing maintenance and service costs, limits widespread adoption, especially in price-sensitive markets, thus restricting market penetration and overall growth.

Another critical restraint is the increasingly stringent regulatory landscape governing medical devices across various regions. Obtaining necessary approvals from bodies like the FDA in the United States, EMA in Europe, or PMDA in Japan, involves lengthy, complex, and costly processes. These regulations require extensive clinical trials, detailed documentation, and adherence to rigorous manufacturing standards, which can delay product launches and increase development costs significantly. This regulatory burden not only strains resources for manufacturers but also slows down the pace of innovation reaching the market, potentially hindering advancements that could otherwise benefit patients.

Furthermore, the scarcity of skilled ophthalmologists and trained technicians, particularly in underserved and rural areas globally, poses a substantial barrier to market expansion. Even with the availability of cutting-edge devices, their effective utilization depends on a skilled workforce capable of operating and interpreting them. This talent gap means that advanced technologies may remain underutilized or inaccessible in many regions, directly impacting the demand for and deployment of sophisticated ophthalmology devices. Addressing this shortage requires long-term investments in medical education and training programs, which currently present a significant bottleneck for market growth.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Cost of Advanced Ophthalmic Devices | -1.5% | Global, particularly Emerging Markets | Medium to Long Term (2026-2033) |

| Stringent Regulatory Approval Processes | -1.2% | Global, particularly Developed Markets | Long Term (2025-2033) |

| Lack of Skilled Ophthalmologists & Technicians | -1.0% | Global, particularly Rural & Underserved Regions | Long Term (2025-2033) |

| Limited Reimbursement Policies in Certain Regions | -0.8% | Europe, parts of Asia Pacific, Latin America | Medium Term (2027-2031) |

| Product Recalls & Safety Concerns | -0.5% | Global | Short Term (2025-2026) |

Ophthalmology Device Market Opportunities Analysis

The ophthalmology device market is ripe with opportunities that promise to accelerate its growth trajectory and redefine eye care delivery. A significant opportunity lies in the burgeoning economies of Asia Pacific, Latin America, and the Middle East & Africa. These regions are characterized by large populations, improving healthcare infrastructure, and increasing disposable incomes, which collectively fuel a growing demand for advanced ophthalmic devices. As access to healthcare expands and awareness of eye health increases, these markets present vast untapped potential for manufacturers to introduce innovative products and establish strong market footholds, thereby diversifying their revenue streams and driving global market expansion.

Another compelling opportunity emerges from the continued integration of artificial intelligence (AI) and machine learning (ML) into ophthalmic diagnostics and therapeutics. These technologies offer the potential for personalized medicine, where treatment plans are tailored to individual patient characteristics and disease profiles. AI can enhance the precision of surgical robotics, optimize drug delivery systems, and develop predictive models for disease progression, leading to more effective and patient-specific interventions. Companies that successfully leverage AI and ML to develop next-generation smart devices will gain a significant competitive advantage and unlock new avenues for market growth and improved patient outcomes.

Furthermore, the expansion of tele-ophthalmology and remote monitoring solutions presents a substantial opportunity, particularly in light of global health trends emphasizing digital health. These platforms can bridge geographical barriers, making specialized eye care accessible to remote and underserved populations. Remote diagnostic screening, virtual consultations, and at-home monitoring devices reduce the need for in-person visits, enhancing convenience for patients and efficiency for healthcare providers. Investments in developing secure, reliable, and user-friendly tele-ophthalmology platforms will allow companies to tap into a broader patient base and contribute to universal eye health, creating a scalable and impactful market segment.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Emerging Markets Expansion (Asia Pacific, Latin America) | +1.7% | Asia Pacific, Latin America, Middle East & Africa | Medium to Long Term (2026-2033) |

| Integration of AI/ML for Personalized Medicine | +1.4% | Global, particularly Developed Markets | Short to Medium Term (2025-2029) |

| Expansion of Tele-ophthalmology & Remote Monitoring | +1.3% | Global, particularly Rural & Underserved Regions | Short Term (2025-2027) |

| Development of Advanced Ocular Drug Delivery Systems | +1.1% | Global | Medium Term (2027-2031) |

| Growing Demand for Refractive Error Correction Devices | +0.9% | Global Youth Population | Long Term (2025-2033) |

Ophthalmology Device Market Challenges Impact Analysis

The ophthalmology device market, despite its promising growth, is confronted by several significant challenges that necessitate strategic navigation from manufacturers and healthcare providers. One prominent challenge is the intense competition and market saturation, particularly in developed regions for established product categories. This competitive landscape puts pressure on pricing, necessitates continuous innovation, and requires substantial investments in research and development to maintain market share. Companies must differentiate their offerings through superior technology, clinical efficacy, and strong brand recognition to overcome the fierce rivalry and capture new market segments.

Another substantial challenge revolves around data privacy and cybersecurity concerns, especially with the increasing integration of digital health solutions and AI into ophthalmic devices. The collection, storage, and analysis of sensitive patient data raise critical questions about data security, compliance with regulations like GDPR and HIPAA, and the ethical use of AI algorithms. Any breach of data security or misuse of patient information can severely damage patient trust and lead to significant legal and financial repercussions for device manufacturers. Addressing these concerns requires robust cybersecurity frameworks, transparent data governance policies, and adherence to global privacy standards.

Furthermore, the rapid pace of technological obsolescence poses a continuous challenge. As new advancements emerge quickly, existing devices can become outdated, requiring frequent upgrades or replacements. This not only impacts the return on investment for healthcare facilities but also places a burden on manufacturers to consistently innovate and update their product portfolios. Managing this cycle of innovation and obsolescence requires strategic planning, efficient R&D pipelines, and effective lifecycle management to ensure products remain competitive and clinically relevant over time. Overcoming these challenges is crucial for sustained success in the dynamic ophthalmology device market.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Intense Competition and Market Saturation | -1.3% | Developed Markets (North America, Europe) | Long Term (2025-2033) |

| Data Privacy and Cybersecurity Concerns (AI/Digital Health) | -1.0% | Global | Medium to Long Term (2026-2033) |

| Rapid Technological Obsolescence | -0.9% | Global | Short to Medium Term (2025-2029) |

| Intellectual Property (IP) Disputes & Patent Wars | -0.7% | Global, particularly Developed Markets | Medium Term (2027-2031) |

| Economic Downturns Impacting Healthcare Budgets | -0.6% | Global | Short Term (2025-2026) |

Ophthalmology Device Market - Updated Report Scope

This comprehensive market insights report meticulously analyzes the global ophthalmology device market, providing an in-depth assessment of its current landscape, historical performance, and future growth projections from 2025 to 2033. It encompasses a detailed examination of market size, growth drivers, restraints, opportunities, and challenges, leveraging robust market intelligence. The report aims to offer strategic insights into various market segments, regional dynamics, and competitive activities, thereby serving as an invaluable resource for stakeholders seeking to understand and capitalize on the evolving opportunities within the ophthalmology device industry.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 59.5 Billion |

| Market Forecast in 2033 | USD 101.5 Billion |

| Growth Rate | 6.8% |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Johnson & Johnson Vision, Alcon, Bausch + Lomb, Carl Zeiss Meditec, EssilorLuxottica, Topcon Corporation, Nidek Co. Ltd., Hoya Corporation, Haag-Streit Group, Glaukos Corporation, STAAR Surgical Company, Ivantis Inc., Rayner Intraocular Lenses Ltd., Santen Pharmaceutical Co., Ltd., CooperVision, Inc., Ziemer Ophthalmic Systems AG, Lumenis Ltd., LightForce Medical, Inc., Ellex Medical Lasers Ltd. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The ophthalmology device market is broadly segmented by device type, application, and end user, each contributing uniquely to the overall market dynamics and growth patterns. The segmentation by device type categorizes products into diagnostic, surgical, and vision care devices, reflecting the comprehensive range of tools and technologies employed across the spectrum of eye health. Diagnostic devices focus on early detection and precise characterization of ocular conditions, while surgical devices enable corrective and therapeutic interventions. Vision care devices, encompassing spectacles and contact lenses, address refractive errors and support daily visual needs. This granular breakdown provides a clear understanding of where innovation is most concentrated and which product categories are experiencing the highest demand.

Further segmentation by application highlights the specific ocular conditions that these devices are designed to address, including major areas such as cataracts, glaucoma, refractive errors, diabetic retinopathy, and age-related macular degeneration (AMD). The prevalence of these conditions globally directly correlates with the demand for specific device types, allowing for targeted market analysis and strategic development. For instance, the high incidence of cataracts drives demand for intraocular lenses and phacoemulsification systems, while the rising burden of diabetic retinopathy spurs innovation in retinal imaging and laser treatment devices. Analyzing these applications reveals the disease burden and corresponding market opportunities.

The market is also segmented by end user, encompassing hospitals, ambulatory surgical centers (ASCs), specialty eye clinics, and optical retail stores. Each end-user segment has distinct requirements and purchasing behaviors, influencing product design, distribution channels, and service models. Hospitals and ASCs typically invest in high-end surgical and diagnostic equipment, while specialty eye clinics might focus on advanced diagnostic tools and comprehensive vision care. Optical retail stores, on the other hand, primarily cater to vision correction needs. Understanding these end-user preferences is crucial for manufacturers to tailor their marketing and sales strategies effectively and to develop products that meet the specific needs of diverse healthcare settings.

- By Device Type: Diagnostic Devices (Ophthalmoscopes, Tonometers, Fundus Cameras, OCT, Perimeters, Corneal Topographers, Slit Lamps, Biometers, Pachymeters, Retinal Scanners, Autorefractors), Surgical Devices (Phacoemulsification Systems, Vitrectomy Devices, Femtosecond Lasers, Excimer Lasers, Intraocular Lenses (Monofocal, Multifocal, Toric, Accommodative), Ophthalmic Microscopes, Surgical Micro-instruments, Glaucoma Drainage Devices, Refractive Lasers), Vision Care Devices (Contact Lenses (Soft, RGP, Hybrid), Spectacles, Ocular Prosthetics, Low Vision Aids).

- By Application: Cataract, Glaucoma, Refractive Error, Diabetic Retinopathy, Age-related Macular Degeneration (AMD), Dry Eye Syndrome, Other Ophthalmic Conditions.

- By End User: Hospitals, Ambulatory Surgical Centers (ASCs), Specialty Eye Clinics, Optical Retail Stores, Academic & Research Institutes.

Regional Highlights

- North America: Dominates the global market share, driven by advanced healthcare infrastructure, high healthcare expenditure, significant R&D activities, and the rapid adoption of new technologies. The presence of key market players and a high prevalence of chronic eye diseases further contribute to its leading position. The United States is a primary contributor to this regional dominance.

- Europe: Represents a substantial market, characterized by an aging population, robust governmental support for healthcare innovation, and high awareness of eye health. Countries such as Germany, the UK, and France are key contributors, with strong regulatory frameworks and a focus on advanced medical device adoption.

- Asia Pacific (APAC): Expected to exhibit the highest growth rate during the forecast period. This growth is fueled by a large and expanding patient pool, improving healthcare access, rising disposable incomes, and increasing awareness about eye health. Countries like China, India, and Japan are pivotal, offering immense opportunities for market expansion and new product introductions.

- Latin America: Shows promising growth potential due to increasing healthcare investments, improving economic conditions, and a growing demand for advanced eye care solutions. Brazil and Mexico are leading markets in the region.

- Middle East and Africa (MEA): A developing market with increasing healthcare infrastructure development and a growing prevalence of lifestyle-related eye diseases. While smaller in market share, the region presents emerging opportunities as healthcare systems evolve and access to modern ophthalmology devices expands.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Ophthalmology Device Market.- Johnson & Johnson Vision

- Alcon

- Bausch + Lomb

- Carl Zeiss Meditec

- EssilorLuxottica

- Topcon Corporation

- Nidek Co. Ltd.

- Hoya Corporation

- Haag-Streit Group

- Glaukos Corporation

- STAAR Surgical Company

- Ivantis Inc.

- Rayner Intraocular Lenses Ltd.

- Santen Pharmaceutical Co., Ltd.

- CooperVision, Inc.

- Ziemer Ophthalmic Systems AG

- Lumenis Ltd.

- LightForce Medical, Inc.

- Ellex Medical Lasers Ltd.

Frequently Asked Questions

What is the primary driver for the Ophthalmology Device Market's growth?

The primary driver is the increasing global prevalence of chronic eye diseases such as cataracts, glaucoma, diabetic retinopathy, and age-related macular degeneration, significantly accelerated by an aging population worldwide.

How is AI transforming ophthalmic care?

AI is transforming ophthalmic care by enhancing diagnostic accuracy through automated image analysis, enabling personalized treatment plans, optimizing surgical procedures with real-time guidance, and improving clinical workflow efficiency.

Which regions offer the greatest growth opportunities in the Ophthalmology Device Market?

The Asia Pacific region, particularly countries like China and India, offers the greatest growth opportunities due to its large population, improving healthcare infrastructure, and rising disposable incomes.

What are the main challenges facing ophthalmology device manufacturers?

Key challenges include the high cost of advanced devices, stringent regulatory approval processes, intense market competition, data privacy concerns with digital health integration, and the rapid pace of technological obsolescence.

What types of devices are included in the Ophthalmology Device Market?

The market includes Diagnostic Devices (e.g., OCT, fundus cameras), Surgical Devices (e.g., phacoemulsification systems, IOLs, lasers), and Vision Care Devices (e.g., contact lenses, spectacles).

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted