Ophthalmic Viscoelastic Device Market

Ophthalmic Viscoelastic Device Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_702251 | Last Updated : July 31, 2025 |

Format : ![]()

![]()

![]()

![]()

Ophthalmic Viscoelastic Device Market Size

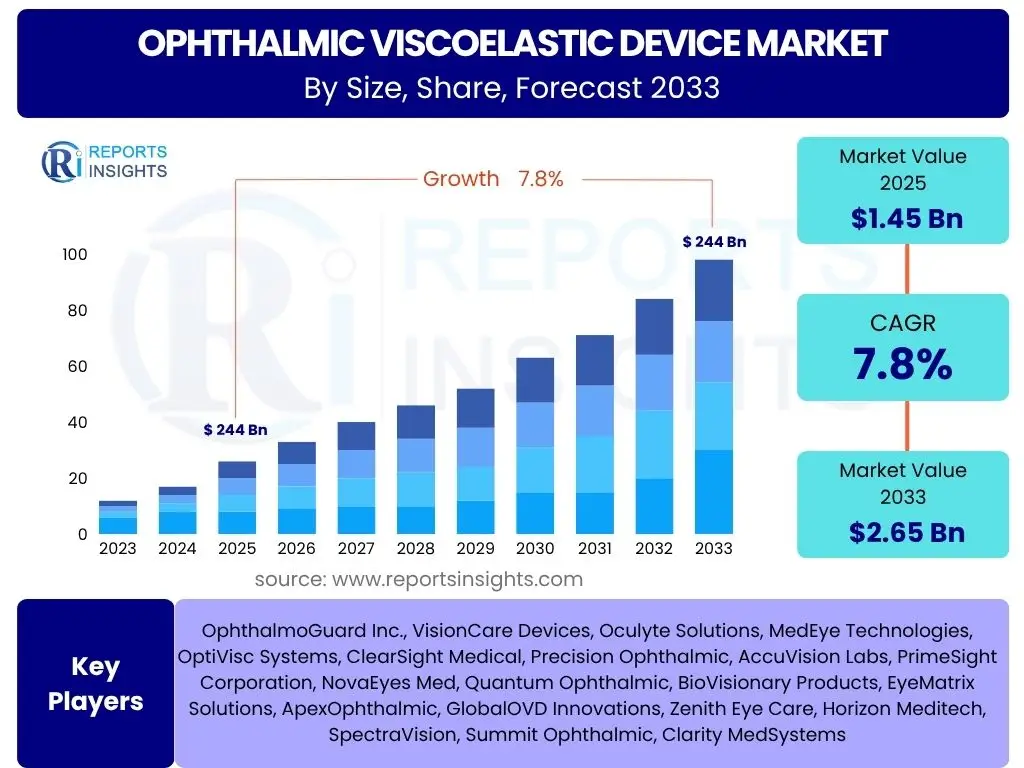

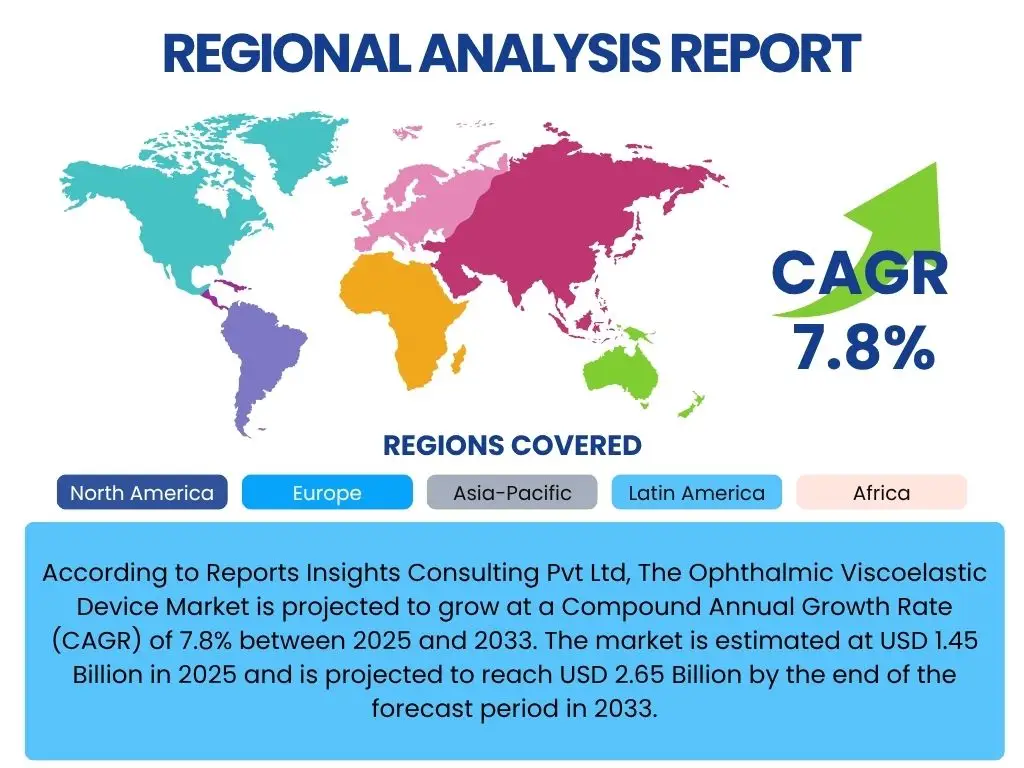

According to Reports Insights Consulting Pvt Ltd, The Ophthalmic Viscoelastic Device Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 7.8% between 2025 and 2033. The market is estimated at USD 1.45 Billion in 2025 and is projected to reach USD 2.65 Billion by the end of the forecast period in 2033.

Key Ophthalmic Viscoelastic Device Market Trends & Insights

The ophthalmic viscoelastic device (OVD) market is undergoing significant transformation driven by an aging global population and a rising incidence of chronic eye conditions. A prominent trend involves the increasing demand for advanced OVD formulations that offer enhanced surgical outcomes and patient safety. These next-generation OVDs are designed to provide superior chamber stability, improved endothelial cell protection, and easier removal, addressing critical needs in complex ophthalmic procedures.

Technological advancements in ophthalmic surgery, such as femtosecond laser-assisted cataract surgery and minimally invasive glaucoma surgery (MIGS), are also shaping the market landscape. These innovations necessitate OVDs that are compatible with new surgical techniques and instruments, driving research and development efforts toward more specialized and versatile products. Furthermore, there is a growing emphasis on cost-effectiveness and efficiency, pushing manufacturers to innovate without compromising on quality or performance, especially in price-sensitive markets.

The expansion of ambulatory surgical centers (ASCs) and private ophthalmic clinics represents another crucial trend. These facilities prioritize quick patient turnover and high-volume procedures, leading to a preference for OVDs that facilitate smooth surgical flow and reduce recovery times. Manufacturers are responding by offering pre-filled syringes and integrated delivery systems, streamlining the surgical process and enhancing convenience for healthcare providers.

- Growing adoption of premium intraocular lenses (IOLs) requiring precise surgical environments.

- Increasing prevalence of cataracts and other age-related eye disorders globally.

- Technological advancements in OVD formulations, including enhanced cohesiveness and dispersiveness.

- Rise in popularity of minimally invasive ophthalmic surgical procedures.

- Expansion of ambulatory surgical centers (ASCs) and private clinics.

AI Impact Analysis on Ophthalmic Viscoelastic Device

Artificial Intelligence (AI) is poised to revolutionize various aspects of ophthalmic surgery, indirectly influencing the Ophthalmic Viscoelastic Device (OVD) market by optimizing surgical planning, execution, and post-operative care. AI-powered diagnostic tools can provide more precise pre-operative assessments, enabling surgeons to select the most appropriate OVD type and quantity based on individual patient characteristics and complexity of the case. This data-driven approach leads to better surgical outcomes and potentially reduces OVD waste.

During surgical procedures, AI could assist in real-time monitoring of intraocular pressure and chamber dynamics, offering feedback that guides OVD injection and removal. Predictive analytics, fueled by AI, might forecast potential complications, allowing surgeons to adapt their OVD strategy proactively. While AI will not directly replace OVDs, its role in enhancing surgical precision and efficiency means that the demand will shift towards OVDs that offer predictable performance and compatibility with advanced, AI-guided surgical systems.

Furthermore, AI can streamline supply chain management and inventory optimization for OVDs, reducing operational costs for healthcare providers. In research and development, AI algorithms can accelerate the discovery of new OVD materials and formulations by simulating molecular interactions and predicting their rheological properties. This potential for innovation could lead to the development of OVDs with superior characteristics tailored for future ophthalmic interventions, reinforcing the market's growth trajectory.

- AI-assisted pre-operative planning optimizing OVD selection and quantity.

- Real-time AI monitoring of surgical parameters, enhancing OVD application precision.

- Predictive analytics for post-operative outcomes influencing OVD choice.

- Streamlined OVD supply chain management and inventory optimization via AI.

- Accelerated R&D for novel OVD formulations through AI-driven material discovery.

Key Takeaways Ophthalmic Viscoelastic Device Market Size & Forecast

The Ophthalmic Viscoelastic Device (OVD) market demonstrates robust growth potential, primarily propelled by the increasing global burden of ophthalmic diseases and the continuous advancements in surgical techniques. The substantial projected Compound Annual Growth Rate (CAGR) signifies a sustained demand for OVDs, driven by an aging population requiring cataract and other vision-correcting surgeries. This upward trend underscores the essential role OVDs play in ensuring surgical safety and efficacy, making them indispensable components of modern ophthalmic care.

A significant takeaway is the market's responsiveness to innovation, with new formulations and delivery systems constantly emerging to meet evolving surgical demands. Manufacturers are focusing on developing OVDs that offer a balance of cohesive and dispersive properties, enabling surgeons to achieve optimal chamber maintenance and tissue protection across a wider range of procedures. This adaptability ensures the market remains dynamic and competitive, with ongoing product enhancements contributing to its expansion.

Geographically, emerging economies present considerable opportunities for market growth due to improving healthcare infrastructure, increasing access to ophthalmic care, and rising awareness regarding eye health. While established markets in North America and Europe continue to hold significant shares, the focus is increasingly shifting towards Asia Pacific and Latin America, where a large patient pool and burgeoning medical tourism offer new avenues for market penetration and revenue generation for OVD manufacturers.

- Sustained growth driven by an aging population and rising ophthalmic disease prevalence.

- Strong market momentum due to continuous technological advancements in OVD formulations.

- Increasing surgical volumes, especially cataract surgeries, as a primary market driver.

- Emerging economies offering significant untapped growth potential.

- Focus on cost-effectiveness and procedural efficiency shaping product development.

Ophthalmic Viscoelastic Device Market Drivers Analysis

The Ophthalmic Viscoelastic Device (OVD) market is primarily driven by the escalating global prevalence of ophthalmic disorders, particularly cataracts, which necessitate surgical intervention. As the worldwide population ages, the incidence of age-related eye conditions naturally increases, creating a larger patient pool requiring ophthalmic surgeries where OVDs are crucial for maintaining space and protecting delicate eye tissues during procedures. This demographic shift provides a foundational growth impetus for the market.

Moreover, significant advancements in ophthalmic surgical techniques and instruments contribute substantially to market expansion. Procedures like femtosecond laser-assisted cataract surgery, minimally invasive glaucoma surgery (MIGS), and advanced vitreoretinal surgeries demand specialized OVDs that can integrate seamlessly with these sophisticated technologies. The continuous innovation in surgical approaches directly fuels the demand for high-performance and tailored OVD formulations, enhancing both safety and precision during complex operations.

Increased healthcare expenditure, particularly in developing regions, coupled with rising awareness about eye health and the availability of advanced treatment options, further propels market growth. Governments and private organizations are investing more in improving ophthalmic care infrastructure, leading to a greater number of surgical facilities and trained professionals capable of performing vision-restoring procedures. This improved accessibility to care translates directly into higher consumption of OVDs.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Aging Global Population and Increasing Ophthalmic Disease Prevalence | +2.1% | Global, particularly North America, Europe, Asia Pacific | 2025-2033 |

| Technological Advancements in Ophthalmic Surgical Procedures | +1.8% | Developed Markets (US, Germany, Japan), rapidly growing in China, India | 2025-2033 |

| Rising Healthcare Expenditure and Improving Healthcare Infrastructure | +1.5% | Emerging Economies (Brazil, India, China), parts of Middle East | 2025-2033 |

| Growing Awareness of Eye Health and Treatment Options | +1.2% | Global, with emphasis on underserved regions | 2025-2033 |

Ophthalmic Viscoelastic Device Market Restraints Analysis

Despite significant growth drivers, the Ophthalmic Viscoelastic Device (OVD) market faces certain restraints that could impede its expansion. One primary concern is the high cost associated with advanced OVDs, especially those with specialized formulations or integrated delivery systems. In many developing regions and even in some developed healthcare systems, budget constraints and reimbursement policies can limit the adoption of premium OVDs, prompting a preference for more economical, albeit less advanced, alternatives. This cost sensitivity can directly impact market penetration and revenue growth.

Another significant restraint is the stringent regulatory approval process required for new OVD products. Ophthalmic devices, due to their direct contact with sensitive ocular tissues, are subject to rigorous testing and clinical trials to ensure safety and efficacy. This lengthy and costly approval pathway can delay market entry for innovative products, discouraging investment in research and development, particularly for smaller manufacturers. Variations in regulatory requirements across different countries further complicate global market expansion.

The risk of post-operative complications, though rare, associated with OVD use, such as elevated intraocular pressure or inflammation, also acts as a restraint. While OVDs are generally safe, any perceived or actual risk can influence surgeon preference and patient acceptance. Furthermore, the availability of alternative surgical techniques or non-OVD solutions, even if less common, can present a competitive challenge, requiring OVD manufacturers to continuously demonstrate superior benefits and safety profiles.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Cost of Advanced OVDs and Budget Constraints | -0.8% | Global, particularly price-sensitive markets in Asia Pacific, Latin America | 2025-2033 |

| Stringent Regulatory Approval Processes | -0.6% | North America, Europe, Japan (regions with mature regulatory bodies) | 2025-2033 |

| Risk of Post-Operative Complications | -0.4% | Global, impacting patient and surgeon confidence | 2025-2033 |

| Availability of Alternative Surgical Techniques or Products | -0.3% | Developed Markets where diverse options exist | 2025-2033 |

Ophthalmic Viscoelastic Device Market Opportunities Analysis

The Ophthalmic Viscoelastic Device (OVD) market is ripe with opportunities, particularly in emerging economies where access to advanced ophthalmic care is expanding. Countries in Asia Pacific, Latin America, and the Middle East are experiencing rapid economic growth, improving healthcare infrastructure, and an increasing middle-class population with higher disposable incomes. This demographic shift creates a vast untapped market for ophthalmic surgeries and, consequently, for OVDs, offering manufacturers significant potential for market penetration and revenue generation through strategic investments and localized product offerings.

Another key opportunity lies in the continuous innovation and development of multi-functional OVDs. As surgical techniques become more sophisticated and individualized, there is a growing demand for OVDs that can perform multiple roles, such as providing space, protecting tissue, and assisting in IOL insertion, all within a single formulation. The development of OVDs with enhanced bio-compatibility, longer retention times, or easier removal properties could significantly differentiate products and capture a larger market share, catering to the evolving needs of surgeons.

Furthermore, the rising adoption of premium intraocular lenses (IOLs) and refractive surgeries presents a lucrative opportunity. These advanced procedures often require a more controlled and protective surgical environment, thus increasing the demand for high-quality, specialized OVDs. As patient expectations for superior visual outcomes grow, the preference for OVDs that can facilitate optimal surgical conditions for these high-value procedures will also increase, driving premium segment growth within the market.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Emerging Markets and Expanding Healthcare Access | +1.9% | Asia Pacific (China, India), Latin America (Brazil, Mexico), Middle East | 2025-2033 |

| Development of Multi-functional and Specialized OVDs | +1.7% | Global, driven by technological advancements | 2025-2033 |

| Rising Adoption of Premium IOLs and Refractive Surgeries | +1.4% | Developed Markets (US, Europe), affluent segments in emerging economies | 2025-2033 |

| Expansion of Ambulatory Surgical Centers (ASCs) | +1.0% | North America, Europe, Australia | 2025-2033 |

Ophthalmic Viscoelastic Device Market Challenges Impact Analysis

The Ophthalmic Viscoelastic Device (OVD) market faces several challenges that require strategic navigation for sustained growth. Intense competition among existing market players, coupled with the entry of new manufacturers, leads to significant pricing pressure. This competitive landscape forces companies to differentiate their products through innovation or cost-effectiveness, impacting profit margins, especially for generic or less specialized OVDs. The need to balance high-quality production with competitive pricing remains a critical challenge for market participants.

Supply chain disruptions, as evidenced by recent global events, pose a substantial challenge to the OVD market. Raw material sourcing, manufacturing, and distribution can be severely impacted by geopolitical tensions, natural disasters, or pandemics, leading to product shortages and increased operational costs. Ensuring a resilient and diversified supply chain is crucial for maintaining consistent product availability and meeting market demand, particularly for medical devices with specific material requirements.

Another challenge is managing the ongoing need for product innovation while adhering to stringent regulatory requirements and high R&D costs. Developing new OVD formulations that offer significant clinical advantages requires substantial investment and a long lead time for approval. Companies must continuously balance the imperative for innovation with the financial burden and regulatory hurdles, ensuring that new products offer a clear value proposition to justify the development efforts and obtain market acceptance.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Intense Market Competition and Pricing Pressure | -0.7% | Global, particularly in mature and generic segments | 2025-2033 |

| Supply Chain Disruptions and Raw Material Volatility | -0.5% | Global, with varying regional impacts | 2025-2033 |

| High R&D Costs and Complex Regulatory Compliance | -0.4% | Developed Markets (US, EU, Japan) | 2025-2033 |

| Educating Healthcare Professionals in Underserved Regions | -0.3% | Emerging Markets (Africa, parts of Asia) | 2025-2033 |

Ophthalmic Viscoelastic Device Market - Updated Report Scope

This comprehensive report provides an in-depth analysis of the global Ophthalmic Viscoelastic Device market, covering market size estimations, growth forecasts, and detailed segmentation. It examines key market trends, drivers, restraints, opportunities, and challenges influencing market dynamics from 2019 to 2033. The report also includes an assessment of the competitive landscape, profiling leading companies and highlighting regional market insights, offering a strategic overview for stakeholders.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 1.45 Billion |

| Market Forecast in 2033 | USD 2.65 Billion |

| Growth Rate | 7.8% |

| Number of Pages | 255 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | OphthalmoGuard Inc., VisionCare Devices, Oculyte Solutions, MedEye Technologies, OptiVisc Systems, ClearSight Medical, Precision Ophthalmic, AccuVision Labs, PrimeSight Corporation, NovaEyes Med, Quantum Ophthalmic, BioVisionary Products, EyeMatrix Solutions, ApexOphthalmic, GlobalOVD Innovations, Zenith Eye Care, Horizon Meditech, SpectraVision, Summit Ophthalmic, Clarity MedSystems |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Ophthalmic Viscoelastic Device (OVD) market is meticulously segmented to provide a granular understanding of its diverse components and drivers. These segmentations are critical for identifying key growth areas, understanding competitive dynamics, and tailoring strategic initiatives. The market is primarily bifurcated by product type, application, and end-user, each influencing overall market performance and adoption rates across different healthcare settings.

By product type, the market includes Cohesive OVDs, Dispersive OVDs, and Cohesive-Dispersive OVDs. Cohesive OVDs, characterized by their high molecular weight and pseudoplasticity, are preferred for space creation and easy removal, widely used in routine cataract surgeries. Dispersive OVDs, with lower molecular weight and higher retentivity, excel in coating and protecting intraocular tissues. The hybrid Cohesive-Dispersive OVDs offer a combination of these properties, providing versatility for various surgical complexities and surgeon preferences.

Applications span a wide range of ophthalmic surgeries, including cataract surgery, glaucoma surgery, vitreoretinal surgery, and corneal transplants, with cataract surgery being the dominant segment due to its high volume globally. End-users comprise hospitals, ophthalmic clinics, ambulatory surgical centers (ASCs), and academic & research institutes. Hospitals and ASCs represent the largest end-user segments, driven by the increasing number of ophthalmic procedures performed in these facilities, while ophthalmic clinics and research institutes contribute to specialized applications and product development.

- By Product Type:

- Cohesive OVDs

- Dispersive OVDs

- Cohesive-Dispersive OVDs

- By Application:

- Cataract Surgery

- Glaucoma Surgery

- Vitreoretinal Surgery

- Corneal Transplant

- Other Ophthalmic Surgeries

- By End User:

- Hospitals

- Ophthalmic Clinics

- Ambulatory Surgical Centers

- Academic & Research Institutes

Regional Highlights

- North America: This region dominates the Ophthalmic Viscoelastic Device market, attributed to its advanced healthcare infrastructure, high adoption rates of advanced surgical technologies, and a significant aging population prone to ophthalmic conditions. Favorable reimbursement policies and strong R&D activities also contribute to its leading position. The United States is a key contributor, with high surgical volumes and a strong presence of major market players.

- Europe: Europe holds a substantial share of the OVD market, driven by increasing awareness of eye health, rising prevalence of ophthalmic diseases, and well-established healthcare systems in countries like Germany, the UK, and France. Government initiatives supporting eye care and the continuous integration of innovative surgical techniques further bolster market growth.

- Asia Pacific (APAC): The APAC region is projected to be the fastest-growing market for OVDs, fueled by a large and rapidly aging population, improving healthcare access, and increasing disposable incomes. Countries like China and India are witnessing a surge in ophthalmic surgeries due to medical tourism and government investments in healthcare infrastructure, creating immense growth opportunities.

- Latin America: This region presents a growing market for OVDs, characterized by improving economic conditions, expanding healthcare infrastructure, and a rising awareness of ophthalmic health. Brazil and Mexico are leading markets, with increasing numbers of ophthalmic clinics and surgical procedures driving demand.

- Middle East and Africa (MEA): The MEA region is expected to show steady growth, primarily due to developing healthcare facilities, increasing foreign investments in the healthcare sector, and a rising prevalence of ophthalmic disorders. Saudi Arabia and UAE are at the forefront of adopting advanced medical technologies, including OVDs, reflecting a commitment to enhancing eye care services.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Ophthalmic Viscoelastic Device Market.- OphthalmoGuard Inc.

- VisionCare Devices

- Oculyte Solutions

- MedEye Technologies

- OptiVisc Systems

- ClearSight Medical

- Precision Ophthalmic

- AccuVision Labs

- PrimeSight Corporation

- NovaEyes Med

- Quantum Ophthalmic

- BioVisionary Products

- EyeMatrix Solutions

- ApexOphthalmic

- GlobalOVD Innovations

- Zenith Eye Care

- Horizon Meditech

- SpectraVision

- Summit Ophthalmic

- Clarity MedSystems

Frequently Asked Questions

What is an Ophthalmic Viscoelastic Device (OVD)?

An Ophthalmic Viscoelastic Device (OVD) is a clear, gel-like substance used in various eye surgeries, primarily to maintain space within the eye, protect delicate tissues from damage, and facilitate surgical maneuvers. OVDs help to create a stable anterior chamber, cushion the endothelium, and aid in the insertion of intraocular lenses (IOLs).

What are the primary types of OVDs used in eye surgery?

OVDs are primarily classified into three types: cohesive, dispersive, and cohesive-dispersive (or hybrid). Cohesive OVDs are highly viscous, designed for space maintenance and easy removal. Dispersive OVDs have lower viscosity, providing excellent tissue coating and protection. Cohesive-dispersive OVDs combine properties of both, offering versatility for complex procedures.

Which ophthalmic procedures commonly utilize OVDs?

OVDs are essential in a wide range of ophthalmic procedures. The most common application is in cataract surgery, including phacoemulsification and femtosecond laser-assisted cataract surgery. They are also widely used in glaucoma surgery, vitreoretinal surgery, corneal transplants, and other delicate intraocular interventions to ensure surgical safety and precision.

What factors are driving the growth of the Ophthalmic Viscoelastic Device market?

The key drivers include the global increase in age-related ophthalmic diseases, particularly cataracts; advancements in ophthalmic surgical techniques demanding specialized OVDs; rising healthcare expenditure and improving healthcare infrastructure in emerging economies; and growing awareness of eye health leading to more surgical interventions.

What challenges does the Ophthalmic Viscoelastic Device market face?

Major challenges for the OVD market include the high cost of advanced formulations, stringent regulatory approval processes that delay market entry, intense competition leading to pricing pressures, and potential supply chain disruptions affecting raw material sourcing and product availability. Managing these factors is crucial for sustained market growth.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted