Oil Country Tubular Good Market

Oil Country Tubular Good Market Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_707535 | Last Updated : September 08, 2025 |

Format : ![]()

![]()

![]()

![]()

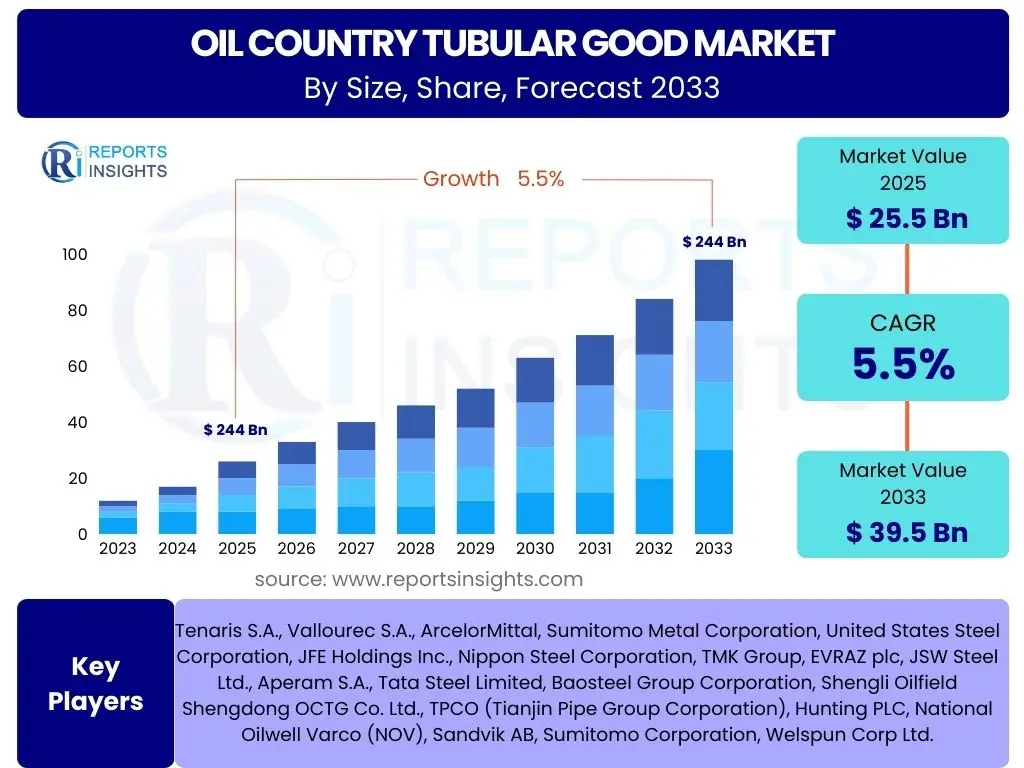

Oil Country Tubular Good Market Size

According to Reports Insights Consulting Pvt Ltd, The Oil Country Tubular Good Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.5% between 2025 and 2033. The market is estimated at USD 25.5 Billion in 2025 and is projected to reach USD 39.5 Billion by the end of the forecast period in 2033.

Key Oil Country Tubular Good Market Trends & Insights

User inquiries regarding the Oil Country Tubular Good (OCTG) market frequently highlight an interest in understanding the ongoing shifts and future directions of this critical industry component. Common questions revolve around the impact of global energy demand, technological advancements in drilling, the increasing focus on unconventional oil and gas resources, and the influence of environmental regulations. There is also significant curiosity about how geopolitical landscapes and supply chain resilience are shaping market dynamics. The prevailing themes indicate a market in transition, driven by both traditional energy needs and the evolving demands of a more sustainable energy future, emphasizing efficiency, durability, and cost-effectiveness in tubular goods.

The market is witnessing a notable trend towards higher-performance materials and specialized connections, particularly for challenging drilling environments such as deepwater and high-pressure, high-temperature (HPHT) wells. This demand is fueled by the exploration and production of complex reservoirs, where standard OCTG may not suffice. Furthermore, the integration of digital technologies, including advanced analytics and IoT sensors, is emerging as a key trend to optimize operational efficiency, predictive maintenance, and supply chain management within the OCTG sector. The industry is also adapting to the energy transition by exploring applications in geothermal drilling and carbon capture, utilization, and storage (CCUS) projects, positioning OCTG as a versatile component in future energy infrastructure.

- Growing demand for premium-grade and specialized OCTG for complex drilling environments.

- Increased adoption of digital solutions for operational efficiency and predictive maintenance.

- Emphasis on sustainability and reduced environmental impact in manufacturing processes.

- Diversification of OCTG applications into new energy sectors like geothermal and CCUS.

- Consolidation among market players to enhance technological capabilities and market reach.

- Shift towards more resilient and localized supply chains to mitigate geopolitical risks.

AI Impact Analysis on Oil Country Tubular Good

Common user questions regarding the impact of Artificial Intelligence (AI) on the Oil Country Tubular Good (OCTG) sector typically focus on its potential to revolutionize operational efficiency, enhance predictive capabilities, and introduce new levels of automation. Users are particularly interested in how AI can improve manufacturing processes, optimize material selection, and enable more precise quality control. Concerns often include the initial investment costs, data security, and the need for skilled personnel to implement and manage AI-driven systems. Expectations range from significant reductions in downtime and operational expenditures to advancements in product design and life cycle management.

The integration of AI in the OCTG market is poised to bring transformative changes across the value chain. In manufacturing, AI algorithms can optimize production schedules, monitor equipment health to prevent failures, and enhance quality inspection through computer vision, leading to higher product consistency and reduced waste. For exploration and production (E&P) activities, AI can analyze vast datasets from drilling operations to predict tool wear, optimize drilling parameters, and even recommend the ideal OCTG specifications for specific well conditions. This data-driven approach not only improves drilling efficiency but also extends the lifespan of tubular goods and enhances safety. Furthermore, AI-powered predictive analytics can optimize inventory management and logistics for OCTG suppliers, ensuring timely delivery and minimizing storage costs, thereby fostering a more responsive and efficient supply chain.

- Enhanced predictive maintenance for OCTG manufacturing equipment and downhole tools.

- Optimization of drilling parameters and well planning through AI-driven data analysis.

- Improved quality control and defect detection in tubular goods production via machine vision.

- Streamlined supply chain and inventory management using AI-powered forecasting.

- Development of smart OCTG with embedded sensors for real-time performance monitoring.

Key Takeaways Oil Country Tubular Good Market Size & Forecast

User queries regarding the key takeaways from the Oil Country Tubular Good (OCTG) market size and forecast frequently center on understanding the fundamental drivers of growth, the significant challenges anticipated, and the overall trajectory of the market. Users seek clarity on factors that will most profoundly influence market expansion, such as global energy demand trends, geopolitical stability, and technological advancements. There is also a strong interest in identifying the primary constraints that could hinder growth, including regulatory pressures and volatile commodity prices. The insights reveal a market expected to exhibit steady growth, underpinned by ongoing hydrocarbon exploration and production activities, while simultaneously navigating complex external influences.

The forecast for the OCTG market indicates sustained demand, primarily driven by the imperative to meet global energy consumption requirements, despite increasing investments in renewable energy. The market's resilience is tied to the continued reliance on fossil fuels in the global energy mix for the foreseeable future. Key growth segments are anticipated in unconventional resource development and offshore deepwater projects, which necessitate high-performance, specialized tubular goods. However, the market remains susceptible to fluctuations in crude oil prices, geopolitical tensions affecting supply routes, and evolving environmental policies that could impact drilling activities. The emphasis on efficiency, durability, and technological innovation in OCTG products will be crucial for market participants to thrive in this dynamic environment, offering significant opportunities for those who adapt to changing industry requirements and embrace advanced manufacturing techniques.

- The OCTG market is projected for steady growth, driven by global energy demand and unconventional resource development.

- Deepwater and high-pressure, high-temperature (HPHT) applications are key growth segments.

- Market growth is subject to crude oil price volatility and geopolitical stability.

- Technological advancements in materials and connections are critical for market competitiveness.

- Environmental regulations and the energy transition will increasingly influence market dynamics.

Oil Country Tubular Good Market Drivers Analysis

The Oil Country Tubular Good (OCTG) market is predominantly driven by the persistent global demand for energy, necessitating continuous exploration and production activities. As conventional oil and gas reserves deplete, the industry increasingly targets unconventional resources such such as shale gas and tight oil, as well as complex offshore and deepwater fields. These challenging environments require specialized, high-performance OCTG, thereby boosting demand for premium products. Furthermore, advancements in drilling technologies, including horizontal drilling and hydraulic fracturing, have unlocked vast reserves, directly translating to increased consumption of tubular goods.

Another significant driver is the aging energy infrastructure in various regions, which necessitates replacement and maintenance activities for existing wells. This creates a consistent demand for OCTG for workover operations and integrity management. Additionally, the strategic focus of major oil and gas companies on enhancing production efficiencies and extending the lifespan of wells contributes to the uptake of durable and technologically advanced tubular products. The global economic recovery and industrial growth also indirectly stimulate energy demand, further bolstering the need for oil and gas production and, consequently, OCTG.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Global Energy Demand | +1.2% | Global | 2025-2033 |

| Growth in Unconventional Oil & Gas Exploration | +1.0% | North America, South America, Asia Pacific | 2025-2033 |

| Advancements in Drilling Technologies | +0.8% | Global | 2025-2033 |

| Rising Demand for Deepwater & Offshore Drilling | +0.7% | Latin America, Africa, Europe | 2025-2033 |

| Aging Oil & Gas Infrastructure Replacement | +0.5% | North America, Europe, Middle East | 2025-2030 |

Oil Country Tubular Good Market Restraints Analysis

The Oil Country Tubular Good (OCTG) market faces significant restraints, primarily stemming from the inherent volatility of crude oil and natural gas prices. Fluctuations in these commodity prices directly impact E&P investments; a sustained period of low prices can lead to reduced drilling activities, subsequently dampening the demand for OCTG products. This price instability makes long-term investment and capacity planning challenging for manufacturers. Additionally, geopolitical tensions and instability in major oil-producing regions can disrupt supply chains, affect investment climates, and lead to sudden shifts in market dynamics, further restraining growth.

Environmental regulations and the global push towards renewable energy sources also pose a considerable restraint. Increasing pressure to reduce carbon emissions and stringent environmental policies can limit the scope of new drilling projects, particularly in environmentally sensitive areas. While OCTG is essential for current energy production, the long-term global energy transition away from fossil fuels represents a structural challenge. Oversupply of OCTG, often due to high production capacity coupled with fluctuating demand, can lead to intense price competition and reduced profit margins for manufacturers, acting as another significant restraint on market expansion.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Volatility in Crude Oil & Gas Prices | -1.5% | Global | 2025-2033 |

| Stringent Environmental Regulations | -0.8% | Europe, North America, Asia Pacific | 2025-2033 |

| Global Shift Towards Renewable Energy | -0.7% | Global | 2028-2033 |

| Geopolitical Instability in Key Regions | -0.6% | Middle East, Russia/Ukraine | 2025-2030 |

| Oversupply and Intense Price Competition | -0.4% | Asia Pacific, North America | 2025-2028 |

Oil Country Tubular Good Market Opportunities Analysis

Despite existing restraints, the Oil Country Tubular Good (OCTG) market is poised for various opportunities, primarily driven by the ongoing need for energy security and exploration of technically challenging reserves. The increasing focus on deepwater and ultra-deepwater drilling, particularly in regions like the Gulf of Mexico, Brazil, and West Africa, presents a substantial opportunity for manufacturers of high-strength, corrosion-resistant, and premium-connection OCTG. These complex projects demand superior product performance and reliability, offering higher profit margins for specialized suppliers. Similarly, the continued development of unconventional resources, such as shale oil and gas in North America and emerging shale plays globally, will sustain demand for specialized casing and tubing suitable for horizontal drilling and hydraulic fracturing operations.

Furthermore, the digitalization of the oil and gas industry opens new avenues for OCTG manufacturers. Opportunities exist in integrating smart technologies, such as embedded sensors and data analytics, into tubular goods for real-time monitoring of well integrity and performance. This not only enhances operational efficiency and safety but also enables predictive maintenance, extending the lifespan of OCTG in service. The growing interest in carbon capture, utilization, and storage (CCUS) projects, as well as geothermal energy exploration, also represents emerging niche markets for OCTG, requiring specific material properties and high integrity tubular solutions, thereby diversifying the market beyond traditional oil and gas extraction.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Expansion into Deepwater & Ultra-Deepwater Drilling | +1.1% | Latin America, Africa, North America | 2025-2033 |

| Development of Unconventional Resources Globally | +0.9% | North America, Asia Pacific, South America | 2025-2033 |

| Technological Advancements & Digitalization of OCTG | +0.8% | Global | 2026-2033 |

| Emerging Applications in Geothermal & CCUS Projects | +0.6% | Europe, North America, Asia Pacific | 2027-2033 |

| Increased Demand for Premium & Corrosion-Resistant Grades | +0.5% | Middle East, North America | 2025-2033 |

Oil Country Tubular Good Market Challenges Impact Analysis

The Oil Country Tubular Good (OCTG) market navigates several complex challenges that can impede its growth and operational efficiency. One primary challenge is the fluctuating price of raw materials, particularly steel, which directly impacts production costs and profit margins for OCTG manufacturers. Supply chain disruptions, exacerbated by geopolitical events, trade disputes, or global health crises, can lead to material shortages and increased lead times, making it difficult for companies to meet demand promptly and efficiently. Furthermore, maintaining stringent quality control and adhering to evolving industry standards and regulations, especially for premium and specialized tubular goods used in high-stress environments, adds to operational complexities and costs.

Another significant challenge is the intense competition within the OCTG market, characterized by a large number of global and regional players. This often leads to price wars and reduced profitability, especially for commodity-grade products. The industry also faces the challenge of attracting and retaining skilled labor, as specialized expertise is required for both the manufacturing and deployment of OCTG. Adapting to the long-term energy transition and the decreasing investment in fossil fuel exploration by some governments and financial institutions presents a strategic challenge, requiring OCTG manufacturers to diversify their offerings and explore new markets to sustain growth. This necessitates significant investment in research and development to innovate products for non-traditional energy applications.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Volatile Raw Material Prices (e.g., Steel) | -1.0% | Global | 2025-2033 |

| Supply Chain Disruptions & Logistics Issues | -0.9% | Global | 2025-2030 |

| Intense Market Competition & Price Pressure | -0.7% | Asia Pacific, North America | 2025-2033 |

| Stringent Quality & Safety Standards | -0.5% | Global | 2025-2033 |

| Skilled Labor Shortage & Workforce Training | -0.4% | North America, Europe | 2025-2030 |

Oil Country Tubular Good Market - Updated Report Scope

This comprehensive report provides an in-depth analysis of the Oil Country Tubular Good (OCTG) market, offering detailed insights into its current size, historical performance, and future growth projections. It covers a forecast period extending to 2033, examining key market drivers, restraints, opportunities, and challenges that shape the industry landscape. The scope includes a thorough segmentation analysis by product type, application, material, and grade, alongside regional dynamics and the competitive landscape of key players. The report aims to furnish stakeholders with actionable intelligence for strategic decision-making in this critical sector of the energy industry.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 25.5 Billion |

| Market Forecast in 2033 | USD 39.5 Billion |

| Growth Rate | 5.5% |

| Number of Pages | 250 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Tenaris S.A., Vallourec S.A., ArcelorMittal, Sumitomo Metal Corporation, United States Steel Corporation, JFE Holdings Inc., Nippon Steel Corporation, TMK Group, EVRAZ plc, JSW Steel Ltd., Aperam S.A., Tata Steel Limited, Baosteel Group Corporation, Shengli Oilfield Shengdong OCTG Co. Ltd., TPCO (Tianjin Pipe Group Corporation), Hunting PLC, National Oilwell Varco (NOV), Sandvik AB, Sumitomo Corporation, Welspun Corp Ltd. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Oil Country Tubular Good (OCTG) market is intricately segmented to provide a detailed understanding of its diverse components and their respective contributions to the overall market dynamics. This segmentation facilitates a granular analysis of product types, applications, materials, and grades, allowing stakeholders to identify specific growth areas and market niches. Each segment plays a crucial role in addressing the varied demands of the global oil and gas industry, from standard drilling operations to highly specialized and challenging extraction environments.

Understanding these segments is vital for manufacturers to tailor their product offerings, for operators to optimize their procurement strategies, and for investors to pinpoint lucrative opportunities. The distinctions across these segments often relate to the mechanical properties required for specific well conditions, the corrosive nature of the well environment, and the cost-effectiveness needed for different types of drilling projects. As the energy landscape evolves, the demand within these segments also shifts, favoring products that offer enhanced durability, efficiency, and environmental compliance.

- By Product Type:

- Casing: Used to line the borehole to provide structural integrity to the well and prevent collapse.

- Tubing: Used to transport crude oil or natural gas from the producing formation to the surface.

- Drill Pipe: Heavy, seamless tube that rotates the drill bit and circulates drilling fluid.

- Connectors: Specialized couplings for joining OCTG strings, often proprietary.

- Others: Including pup joints, crossovers, and various accessories.

- By Application:

- Onshore: Drilling and production activities conducted on land.

- Offshore: Drilling and production activities conducted in marine environments, including shallow water, deepwater, and ultra-deepwater.

- By Material:

- Carbon Steel: Standard and widely used for its cost-effectiveness and versatility.

- Alloy Steel: Offers improved strength and toughness, suitable for moderate conditions.

- Stainless Steel: Provides superior corrosion resistance, crucial for corrosive environments.

- Premium Steel: High-grade alloys offering enhanced strength, corrosion resistance, and performance for extreme conditions.

- By Grade:

- API Grade: Conforms to American Petroleum Institute standards, widely accepted globally.

- Premium Grade: Exceeds API standards, offering enhanced performance characteristics for challenging applications.

Regional Highlights

- North America: This region dominates the OCTG market, primarily driven by extensive shale oil and gas development, particularly in the United States and Canada. The demand for specialized tubular goods for horizontal drilling and hydraulic fracturing is consistently high. Investments in unconventional plays and mature fields requiring maintenance and workover operations continue to bolster market growth.

- Asia Pacific (APAC): Expected to witness significant growth due to increasing energy demand, new oil and gas discoveries, and growing investments in upstream activities, particularly in countries like China, India, and Australia. The region is also a major manufacturing hub for OCTG, contributing to both domestic supply and global exports.

- Middle East and Africa (MEA): A crucial region driven by substantial conventional oil and gas reserves and ongoing mega-projects. Countries like Saudi Arabia, UAE, Iran, and Qatar are continuously investing in E&P activities to maintain and increase production capacities. The demand here is often for standard and high-grade OCTG to handle large-scale, long-term operations.

- Europe: The market in Europe is mature, with stable demand from existing conventional fields and a growing emphasis on gas production from the North Sea. However, increasing environmental regulations and the strong push towards renewable energy sources are influencing the long-term outlook for new drilling projects, leading to a focus on maintenance and integrity management.

- Latin America: This region presents considerable growth opportunities, particularly due to deepwater projects in Brazil and Mexico, and onshore conventional and unconventional plays in Argentina. Investment levels are highly sensitive to crude oil prices and political stability, but the long-term potential for resource extraction remains strong.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Oil Country Tubular Good Market.- Tenaris S.A.

- Vallourec S.A.

- ArcelorMittal

- Sumitomo Metal Corporation

- United States Steel Corporation

- JFE Holdings Inc.

- Nippon Steel Corporation

- TMK Group

- EVRAZ plc

- JSW Steel Ltd.

- Aperam S.A.

- Tata Steel Limited

- Baosteel Group Corporation

- Shengli Oilfield Shengdong OCTG Co. Ltd.

- TPCO (Tianjin Pipe Group Corporation)

- Hunting PLC

- National Oilwell Varco (NOV)

- Sandvik AB

- Sumitomo Corporation

- Welspun Corp Ltd.

Frequently Asked Questions

What is the projected growth rate for the Oil Country Tubular Good Market?

The Oil Country Tubular Good (OCTG) Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.5% between 2025 and 2033, driven by ongoing global energy demand and advancements in drilling technologies.

Which regions are expected to drive the demand for OCTG?

North America is expected to remain a dominant region due to shale oil and gas development. Asia Pacific and the Middle East and Africa are also key drivers due to increasing energy consumption and significant upstream investments.

What are the primary factors driving the OCTG market?

Key drivers include increasing global energy demand, growth in unconventional oil and gas exploration, advancements in drilling technologies, and the rising need for deepwater and offshore drilling capabilities.

What challenges does the OCTG market face?

Major challenges include volatility in crude oil and gas prices, stringent environmental regulations, global shifts towards renewable energy, and intense market competition leading to price pressure.

How is AI impacting the Oil Country Tubular Good sector?

AI is transforming the OCTG sector through enhanced predictive maintenance, optimization of drilling operations, improved quality control in manufacturing, and streamlined supply chain management for greater efficiency and reliability.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted