Offshore Cable Market

Offshore Cable Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_708529 | Last Updated : September 15, 2025 |

Format : ![]()

![]()

![]()

![]()

Offshore Cable Market Size

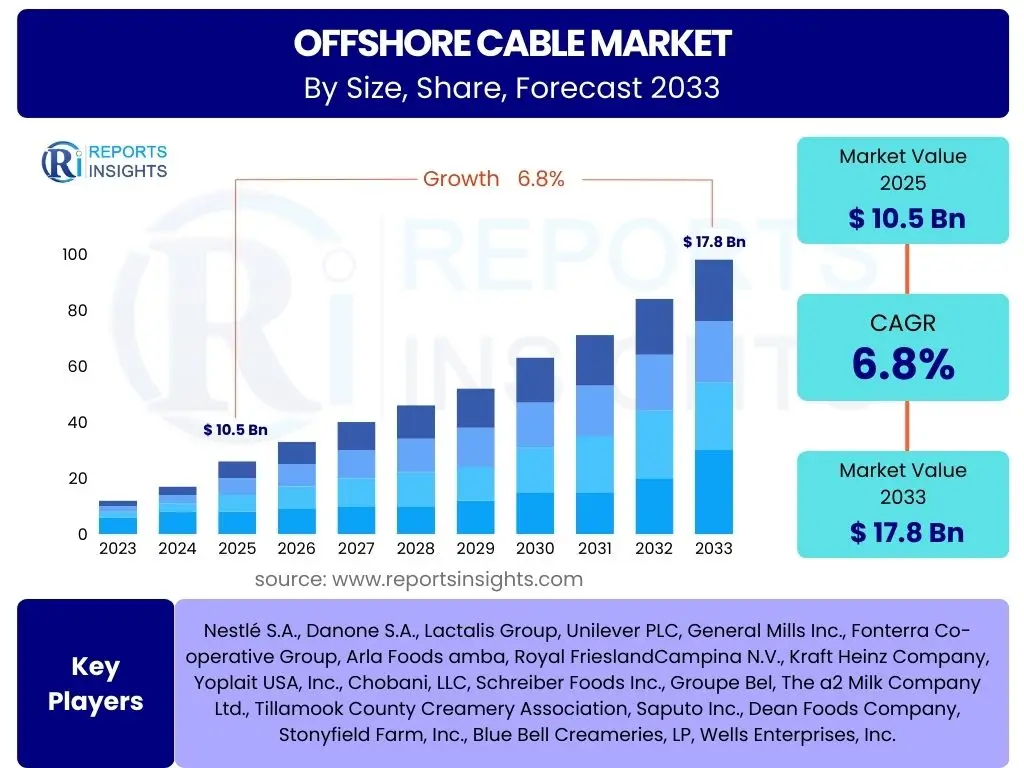

According to Reports Insights Consulting Pvt Ltd, The Offshore Cable Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2025 and 2033. The market is estimated at USD 10.5 billion in 2025 and is projected to reach USD 17.8 billion by the end of the forecast period in 2033.

Key Offshore Cable Market Trends & Insights

The offshore cable market is currently experiencing significant transformative trends driven by the global push towards renewable energy sources and the increasing complexity of subsea infrastructure. A prominent trend involves the growing investment in offshore wind farms, which necessitates extensive high-voltage direct current (HVDC) and high-voltage alternating current (HVAC) cables for power transmission back to shore. This demand is further amplified by the development of floating offshore wind technologies, which introduce new requirements for dynamic cables capable of withstanding constant movement and harsh marine environments. Additionally, there is a clear shift towards advanced materials and designs aimed at enhancing cable durability, reducing transmission losses, and extending operational lifespans, crucial for the economic viability of large-scale offshore projects.

Another critical insight is the increasing demand for interconnector projects between countries and regions, aiming to bolster grid stability and facilitate cross-border energy trading, particularly with excess renewable energy. This requires robust subsea cable systems capable of handling significant power loads over long distances. The integration of digitalization and smart monitoring systems into offshore cable infrastructure is also gaining traction, enabling predictive maintenance, real-time performance analytics, and improved operational efficiency. These technological advancements are not only improving the reliability of existing networks but also paving the way for more resilient and interconnected global energy systems, thereby significantly influencing market growth and technological development.

- Exponential growth in offshore wind farm development, driving demand for HVDC and HVAC cables.

- Increased investment in interconnector projects for cross-border energy exchange and grid stability.

- Technological advancements in cable materials and designs for enhanced durability and efficiency.

- Emergence of floating offshore wind technologies requiring specialized dynamic cable solutions.

- Integration of smart monitoring and digitalization for predictive maintenance and operational optimization.

- Focus on higher voltage and larger capacity cables to meet escalating power transmission needs.

- Growing emphasis on environmental sustainability and reducing the ecological footprint of cable installation.

AI Impact Analysis on Offshore Cable

User inquiries regarding Artificial Intelligence (AI) in the offshore cable sector frequently revolve around its potential to optimize operational efficiency, enhance predictive maintenance, and improve overall system reliability. Stakeholders are particularly interested in how AI can process vast amounts of data from subsea sensors to detect anomalies, forecast equipment failures, and schedule maintenance interventions proactively, thereby minimizing costly downtime and extending the operational life of critical infrastructure. There is also significant curiosity about AI's role in optimizing cable design, manufacturing processes, and installation methodologies, suggesting a desire for data-driven precision to reduce risks and improve project execution. Furthermore, questions often arise about AI's capacity to enhance grid management, especially with the intermittent nature of renewable energy sources, by optimizing power flow through subsea cables and ensuring grid stability.

Concerns often include the initial investment costs associated with AI integration, the availability of skilled personnel to manage and interpret AI-driven insights, and cybersecurity risks inherent in connecting advanced AI systems to vital energy infrastructure. Users also seek clarity on the regulatory frameworks and industry standards that will govern AI deployment in such a critical and high-stakes environment. Expectations are high for AI to revolutionize the entire lifecycle of offshore cables, from concept and design to installation, operation, and eventual decommissioning, by providing unprecedented levels of insight and control. The market anticipates that AI will not only lead to substantial cost savings and efficiency gains but also significantly improve safety and environmental compliance within the offshore energy sector.

- Enhanced predictive maintenance and fault detection through AI-driven analytics of sensor data.

- Optimization of cable design and manufacturing processes using AI for material efficiency and performance.

- Improved operational efficiency and reduced downtime by forecasting equipment failures with AI.

- AI-powered grid management for optimized power flow and enhanced stability from offshore wind farms.

- Automation of inspection tasks using AI-integrated autonomous underwater vehicles (AUVs).

- Risk mitigation during installation and repair through AI-informed decision-making.

- Development of AI models for environmental impact assessment and route optimization for cable laying.

Key Takeaways Offshore Cable Market Size & Forecast

The Offshore Cable market is poised for robust expansion, primarily fueled by the accelerating global transition to renewable energy, particularly offshore wind power. The projected Compound Annual Growth Rate (CAGR) of 6.8% signifies a sustained and healthy growth trajectory over the forecast period, reflecting significant ongoing and planned investments in offshore energy infrastructure. A key takeaway is that the market's growth from an estimated USD 10.5 billion in 2025 to USD 17.8 billion by 2033 indicates a substantial increase in demand for advanced subsea power transmission solutions. This growth is not merely volumetric but also qualitative, emphasizing a shift towards higher voltage, more durable, and technologically sophisticated cable systems capable of meeting the stringent requirements of deep-water and long-distance transmission.

Furthermore, the market's upward trend underscores the increasing importance of grid interconnectivity and energy security initiatives across various regions. The demand for subsea interconnectors, alongside power export cables for offshore wind, forms a dual engine for market expansion. The significant forecast valuation suggests that stakeholders across the value chain, from raw material suppliers to installation and maintenance service providers, will experience expanding opportunities. The market's resilience and growth despite economic fluctuations highlight the foundational role of offshore cables in global decarbonization efforts and the broader energy transition, making it a pivotal sector for long-term investment and technological innovation. This sustained growth trajectory reinforces the strategic importance of developing robust and efficient offshore cable infrastructure to support the future energy landscape.

- Significant market expansion expected, with a robust CAGR of 6.8% from 2025 to 2033.

- Market valuation projected to increase from USD 10.5 billion (2025) to USD 17.8 billion (2033), indicating strong investment.

- Growth primarily driven by global offshore wind energy development and increased demand for power interconnectors.

- Emphasis on advanced, higher voltage, and more durable cable technologies for enhanced performance.

- Market development reflects critical role of offshore cables in achieving global decarbonization targets and energy security.

- Expanding opportunities across the entire value chain, from manufacturing to installation and maintenance.

Offshore Cable Market Drivers Analysis

The offshore cable market is primarily driven by the ambitious global targets for renewable energy integration, particularly the massive build-out of offshore wind farms. Governments worldwide are committing substantial investments and implementing supportive policies to accelerate offshore wind development as a key component of their decarbonization strategies. This surge in offshore wind capacity directly translates into an escalating demand for high-capacity subsea power cables to transmit electricity from offshore generation sites to onshore grids. The increasing scale and distance of these projects necessitate advanced HVDC and HVAC cable systems capable of minimizing transmission losses and ensuring grid stability over long distances.

Additionally, the growing imperative for enhanced energy security and grid reliability is a significant driver. Interconnector projects, linking national and regional grids, are becoming more prevalent to enable power sharing, balance electricity supply and demand, and integrate diverse energy sources effectively. These projects rely heavily on robust offshore cable infrastructure. Furthermore, technological advancements in cable manufacturing, such as improved insulation materials, enhanced durability, and higher voltage capabilities, are making offshore cable installations more efficient and cost-effective, thereby encouraging further market expansion. The decreasing levelized cost of energy (LCOE) for offshore wind also contributes to its attractiveness, indirectly boosting demand for associated cable infrastructure.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Global Offshore Wind Farm Development | +2.5% | Europe (UK, Germany, Netherlands), Asia Pacific (China, Taiwan), North America (USA) | 2025-2033 (Long-term) |

| Increased Demand for Grid Interconnectors | +1.8% | Europe (North Sea, Baltic Sea), Asia Pacific (Japan, Korea), North America (East Coast) | 2026-2033 (Medium to Long-term) |

| Government Policies and Renewable Energy Targets | +1.5% | Global, particularly EU, UK, USA, China, India | 2025-2033 (Long-term) |

| Technological Advancements in Cable Manufacturing | +1.0% | Global (leading manufacturers) | 2025-2030 (Short to Medium-term) |

| Rising Energy Demand and Electrification | +0.8% | Developing Economies (Asia Pacific, Africa), Global | 2027-2033 (Medium to Long-term) |

Offshore Cable Market Restraints Analysis

Despite the strong growth drivers, the offshore cable market faces several significant restraints that can impede its expansion. One of the primary challenges is the extremely high capital expenditure required for manufacturing, installation, and maintenance of offshore cable systems. The specialized vessels, advanced equipment, and skilled labor needed for subsea operations contribute significantly to project costs, making large-scale offshore cable projects inherently expensive. These high costs can deter investment, especially in regions with less established renewable energy policies or in periods of economic uncertainty. Furthermore, the lengthy lead times associated with cable manufacturing and specialized vessel availability can cause project delays and increase overall costs, impacting market growth.

Another critical restraint is the complex and stringent regulatory and environmental permitting processes. Obtaining approvals for cable routes, managing potential impacts on marine ecosystems, and navigating international waters involves a labyrinth of regulations that can prolong project timelines and escalate administrative burdens. Environmental concerns, such as potential disruption to marine life during installation and the long-term impact of electromagnetic fields, also lead to increased scrutiny and compliance costs. Additionally, geopolitical risks and territorial disputes in certain maritime regions can introduce uncertainty and hinder the development of interconnector projects, further constraining market potential. The lack of standardized international regulations for certain aspects of offshore cable deployment also presents a challenge for cross-border projects.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Capital Expenditure for Projects | -1.2% | Global, particularly emerging markets | 2025-2033 (Long-term) |

| Complex Regulatory & Permitting Processes | -1.0% | Europe, North America, highly regulated marine areas | 2025-2033 (Long-term) |

| Environmental Concerns and Impact Mitigation | -0.8% | Global, especially sensitive marine ecosystems | 2025-2033 (Long-term) |

| Limited Availability of Specialized Installation Vessels | -0.7% | Global | 2025-2029 (Short to Medium-term) |

| Geopolitical Risks and Territorial Disputes | -0.5% | Asia Pacific (South China Sea), Arctic regions | 2025-2033 (Long-term) |

Offshore Cable Market Opportunities Analysis

The offshore cable market presents significant growth opportunities driven by emerging technologies and expanding geographical horizons. One major opportunity lies in the burgeoning market for floating offshore wind farms. As wind turbines move into deeper waters, dynamic cables capable of handling continuous movement and severe ocean conditions become essential. This niche requires specialized engineering, materials, and manufacturing processes, offering a high-value segment for innovation and market entry. Furthermore, the development of multi-purpose offshore energy hubs, integrating various renewable energy sources with storage solutions and grid connections, creates demand for complex and robust subsea grid infrastructure, opening avenues for advanced cable solutions and system integration services.

Another substantial opportunity is the untapped potential in emerging markets, particularly in Asia Pacific, Latin America, and parts of Africa, where energy demand is rapidly increasing and offshore renewable resources are abundant. These regions are beginning to invest heavily in offshore wind and grid interconnectivity, creating new frontiers for market expansion beyond established European and North American markets. Additionally, the increasing focus on the decarbonization of oil and gas platforms through electrification from offshore renewable sources or shore-to-platform power supply represents a growing market segment for specialized offshore cables. Advances in power electronics, enabling more efficient HVDC transmission over longer distances, also present opportunities for developing next-generation cable systems that can unlock even more remote offshore energy resources.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development of Floating Offshore Wind Farms | +1.5% | Europe (Norway, UK), Asia Pacific (Japan, Korea), North America (USA West Coast) | 2027-2033 (Medium to Long-term) |

| Emergence of Multi-Purpose Energy Hubs | +1.2% | North Sea region, Baltic Sea, Asia Pacific | 2028-2033 (Long-term) |

| Expansion into Emerging Offshore Wind Markets | +1.0% | Asia Pacific (Vietnam, India), Latin America (Brazil), Africa (South Africa) | 2026-2033 (Medium to Long-term) |

| Electrification of Offshore Oil & Gas Platforms | +0.8% | North Sea, Gulf of Mexico, Brazil | 2025-2031 (Short to Medium-term) |

| Advancements in HVDC Technology for Long-Distance Transmission | +0.7% | Global | 2025-2033 (Long-term) |

Offshore Cable Market Challenges Impact Analysis

The offshore cable market faces several complex challenges that can significantly impact project execution and market growth. One critical challenge is the harsh and unpredictable marine environment. Subsea cables are exposed to extreme weather conditions, strong currents, seismic activity, and marine life, which can lead to damage during installation or operation. Repairing damaged subsea cables is an incredibly complex, time-consuming, and expensive endeavor, often requiring specialized vessels and equipment, leading to significant power outages and financial losses. The increasing depth and distance of offshore projects further exacerbate these environmental and operational complexities, pushing the boundaries of current cable technology and installation methods.

Another substantial challenge is the skilled labor shortage. The highly specialized nature of offshore cable manufacturing, installation, maintenance, and project management requires a niche set of engineering and technical skills. There is a global deficit of experienced personnel in areas such as subsea cable engineering, marine operations, and HVDC system integration, which can lead to project delays, increased labor costs, and compromised quality. Furthermore, the supply chain for critical raw materials, such as copper and specialized insulation polymers, can be vulnerable to disruptions, leading to price volatility and manufacturing delays. Ensuring the long-term reliability and integrity of cables in dynamic offshore environments, particularly for floating wind applications, also poses an ongoing engineering challenge requiring continuous research and development efforts.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Harsh Marine Environment & Cable Damage Risks | -1.1% | Global, particularly storm-prone regions | 2025-2033 (Long-term) |

| Skilled Labor Shortage & Workforce Development | -0.9% | Global, particularly Europe and North America | 2025-2033 (Long-term) |

| Supply Chain Volatility for Key Raw Materials | -0.7% | Global (dependencies on specific producers) | 2025-2029 (Short to Medium-term) |

| Logistical Complexities of Installation & Maintenance | -0.6% | Global, especially remote project sites | 2025-2033 (Long-term) |

| Technological Barriers for Ultra-Deepwater & Dynamic Cables | -0.5% | Global, especially new floating wind regions | 2026-2033 (Medium to Long-term) |

Offshore Cable Market - Updated Report Scope

This report provides a detailed and extensive analysis of the global Offshore Cable Market, encompassing historical data, current market dynamics, and future projections. It aims to offer comprehensive insights into market size, growth drivers, restraints, opportunities, and challenges affecting the industry from 2019 through 2033. The scope includes an in-depth segmentation analysis by type, voltage, application, and end-use, alongside a thorough regional and country-level examination. The report also highlights the competitive landscape, profiling key market players and assessing their strategic initiatives, while integrating the impact of emerging technologies like AI. This analysis is designed to equip stakeholders with actionable intelligence for strategic decision-making and market positioning.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 10.5 billion |

| Market Forecast in 2033 | USD 17.8 billion |

| Growth Rate | 6.8% |

| Number of Pages | 247 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Global Cable Solutions Inc., Subsea Power Systems Corp., Marine Cable Networks Ltd., Oceanic Wire & Transmission, Deepwater Energy Cables, NexGen Offshore Link, AquaConductor Technologies, Sentinel Submarine Cables, Horizon Power Solutions, Pioneer Marine Cable, Titan Subsea Systems, Vantage Offshore Grid, Zenith Cable Innovations, Blue Current Networks, SeaLink Infrastructure |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The offshore cable market is meticulously segmented to provide a granular understanding of its diverse components and drivers. These segments allow for a detailed examination of demand patterns, technological preferences, and regional variations in market adoption. The primary segmentation categories include cable type, voltage level, specific application areas, and overarching end-use industries, each reflecting distinct operational requirements and market dynamics. This comprehensive breakdown facilitates precise market forecasting and strategic planning for manufacturers, service providers, and energy developers looking to navigate the complexities of the subsea infrastructure landscape.

- By Type:

- Submarine Power Cable (HVDC, HVAC): These cables are crucial for transmitting electricity over long distances, primarily from offshore wind farms to onshore grids (HVAC for shorter distances, HVDC for longer and higher capacity).

- Submarine Communication Cable (Fiber Optic, Coaxial): Essential for telecommunications, data transfer, and specialized applications such as seismic monitoring and smart grid communication.

- By Voltage:

- Less than 66 kV: Typically used for inter-array connections within offshore wind farms or shorter-distance power transmission.

- 66 kV to 220 kV: Common for larger offshore wind farm export cables and regional grid interconnectors.

- Above 220 kV: Predominantly used for long-distance, high-capacity HVDC transmission for major inter-continental interconnectors and very large offshore wind projects.

- By Application:

- Offshore Wind Power Export: Cables that carry generated electricity from offshore substations to onshore grids.

- Inter-array Connections (Offshore Wind): Cables linking individual wind turbines to the offshore substation within a wind farm.

- Oil & Gas Subsea Tie-backs: Cables providing power or communication to subsea oil and gas production facilities.

- Inter-country/Regional Grid Interconnectors: High-capacity cables connecting power grids of different nations or regions to enhance energy security and trade.

- Island Grid Connections: Cables connecting island communities to mainland grids for stable power supply or vice versa.

- By End-Use:

- Renewable Energy: Encompasses all aspects of offshore wind, wave, and tidal energy generation and transmission.

- Oil & Gas: Includes power and communication cables for offshore drilling rigs, production platforms, and subsea infrastructure.

- Telecommunications: Covers fiber optic and coaxial cables for internet, data, and voice communication across continents.

- Defense: Specialized cables for military surveillance, sonar systems, and secure communication networks.

Regional Highlights

- Europe: Dominates the offshore cable market, primarily driven by extensive offshore wind farm development in the North Sea and Baltic Sea, aggressive decarbonization targets, and numerous interconnector projects aimed at creating a unified European energy grid. Countries like the UK, Germany, Denmark, and the Netherlands are leading in project deployment and technological innovation.

- Asia Pacific (APAC): Emerging as the fastest-growing region due to significant investments in offshore wind by China, Taiwan, Vietnam, Japan, and South Korea, coupled with rapidly increasing energy demand and ambitious renewable energy targets. The region is witnessing a surge in new project announcements and infrastructure development.

- North America: Showing substantial growth potential, particularly along the East Coast of the United States, with increasing support for offshore wind energy projects. New state-level mandates and federal initiatives are accelerating the development of the necessary transmission infrastructure. Canada also contributes to regional growth with its offshore energy projects.

- Latin America: An emerging market with developing offshore wind potential, particularly off the coasts of Brazil and Colombia. Initial projects and feasibility studies indicate future growth in demand for subsea cables for power export and regional grid improvements.

- Middle East & Africa (MEA): While currently a smaller market, it presents long-term opportunities driven by a focus on diversifying energy sources beyond fossil fuels and developing regional power grids. Offshore wind and inter-regional power connections are areas of nascent interest and investment.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Offshore Cable Market.- Global Cable Solutions Inc.

- Subsea Power Systems Corp.

- Marine Cable Networks Ltd.

- Oceanic Wire & Transmission

- Deepwater Energy Cables

- NexGen Offshore Link

- AquaConductor Technologies

- Sentinel Submarine Cables

- Horizon Power Solutions

- Pioneer Marine Cable

- Titan Subsea Systems

- Vantage Offshore Grid

- Zenith Cable Innovations

- Blue Current Networks

- SeaLink Infrastructure

Frequently Asked Questions

What is the projected growth rate for the Offshore Cable Market?

The Offshore Cable Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2025 and 2033, reaching an estimated USD 17.8 billion by the end of the forecast period.

What are the main drivers of the Offshore Cable Market?

Key drivers include the global expansion of offshore wind farms, increasing demand for inter-country grid interconnectors, supportive government policies for renewable energy, and continuous technological advancements in cable manufacturing.

How does AI impact the Offshore Cable Market?

AI significantly impacts the market by enabling enhanced predictive maintenance, optimizing cable design and operational efficiency, improving fault detection, and assisting in smarter grid management for offshore energy projects.

What are the primary challenges facing the Offshore Cable Market?

Major challenges include the high capital expenditure for projects, complex regulatory and environmental permitting processes, the harsh marine environment leading to damage risks, and a shortage of skilled labor for specialized operations.

Which regions are leading the growth in the Offshore Cable Market?

Europe currently dominates the market due to extensive offshore wind development, while the Asia Pacific region is emerging as the fastest-growing market with significant investments in new projects and renewable energy initiatives.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted