ODM Smartphone Market

ODM Smartphone Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_709543 | Last Updated : December 10, 2025 |

Format : ![]()

![]()

![]()

![]()

ODM Smartphone Market Size

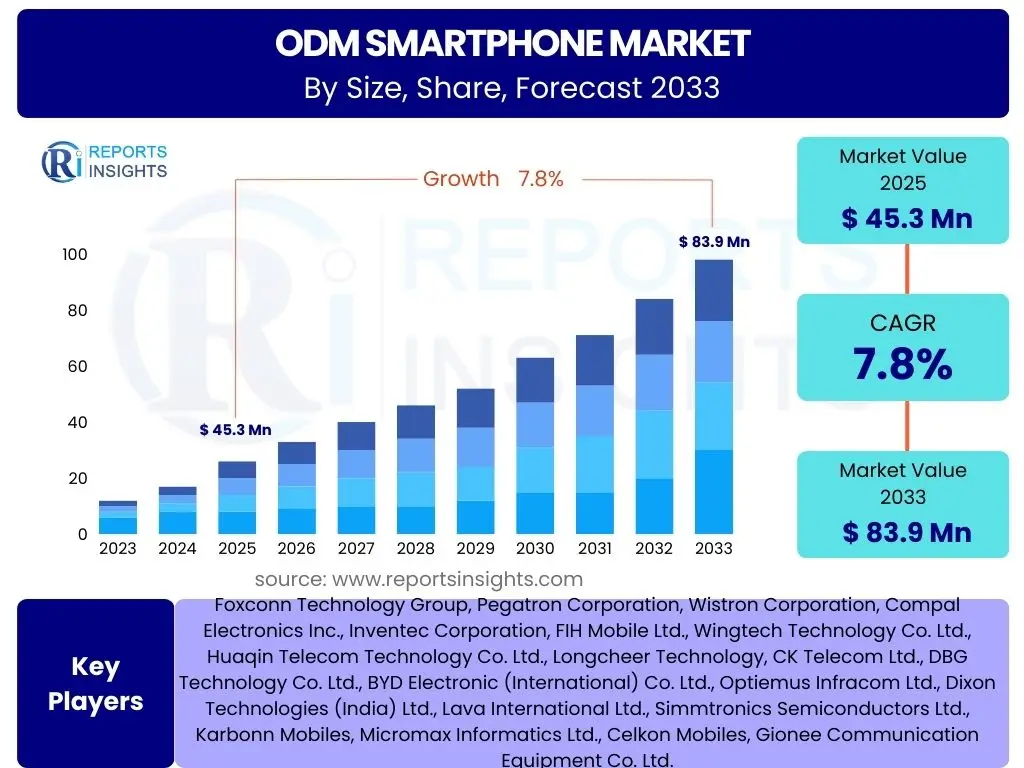

According to Reports Insights Consulting Pvt Ltd, The ODM Smartphone Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 7.8% between 2025 and 2033. The market is estimated at USD 45.3 Billion in 2025 and is projected to reach USD 83.9 Billion by the end of the forecast period in 2033. This substantial growth is primarily driven by the increasing global demand for cost-efficient and technologically advanced smartphones, particularly from emerging economies and brand owners seeking to optimize their production costs and time-to-market. The ODM model allows for significant flexibility and scalability, enabling a wider range of companies to participate in the competitive smartphone landscape.

The upward trajectory of the ODM smartphone market underscores a strategic shift in the electronics manufacturing industry, where brand differentiation increasingly relies on design, marketing, and software, rather than extensive in-house hardware production. This trend allows brands, both established and new, to focus on their core competencies while outsourcing the complex manufacturing and supply chain management to specialized Original Design Manufacturers. Furthermore, the rapid evolution of smartphone technology, including advancements in camera capabilities, processing power, and connectivity standards like 5G, continually fuels innovation cycles that ODMs are uniquely positioned to deliver efficiently.

Key ODM Smartphone Market Trends & Insights

User inquiries frequently highlight evolving consumer preferences, technological advancements, and supply chain dynamics as critical trends shaping the ODM smartphone market. A significant focus is on how ODMs are adapting to demands for more sustainable practices, integrating cutting-edge features like AI and advanced connectivity, and navigating geopolitical influences on global manufacturing. The market is also keenly observing the rise of niche segments and the increasing diversification of ODM service offerings beyond basic manufacturing to include design, R&D, and after-sales support.

- 5G Integration and Advanced Connectivity: The pervasive rollout of 5G networks globally is driving demand for 5G-enabled smartphones, pushing ODMs to rapidly incorporate advanced modem technologies and antenna designs into their offerings.

- AI and Machine Learning Capabilities: Integration of AI for enhanced camera features, battery optimization, personal assistants, and overall user experience is becoming a standard expectation, with ODMs playing a crucial role in hardware-software co-development.

- Cost-Efficiency and Supply Chain Diversification: Brands are increasingly leveraging ODMs to achieve lower manufacturing costs and to diversify their supply chains, reducing reliance on single regions and mitigating geopolitical risks.

- Sustainability and Ethical Manufacturing: Growing consumer and regulatory pressure for eco-friendly production, use of recycled materials, and reduced carbon footprints is prompting ODMs to adopt more sustainable practices.

- Foldable and Innovative Form Factors: The emergence of foldable display technology and other novel smartphone designs presents new opportunities and challenges for ODMs in terms of engineering and manufacturing complexities.

- Increased R&D Investment by ODMs: ODMs are investing more in their own research and development to offer proprietary designs and technologies, thereby providing more value to their brand partners and securing a competitive edge.

AI Impact Analysis on ODM Smartphone

Common user questions regarding AI's impact on ODM smartphones often revolve around its application in performance, user experience, and the manufacturing process itself. Users are keen to understand how AI is enhancing camera quality, optimizing battery life, and enabling smarter device interactions, while also considering the implications for data privacy and security. Furthermore, there is significant interest in how AI technologies are being leveraged within the ODM operational framework, from design and prototyping to quality control and supply chain prediction, aiming for greater efficiency and reduced time-to-market.

The integration of artificial intelligence is not merely a feature addition but a fundamental shift in how smartphones are designed, produced, and utilized. For ODMs, this means not only accommodating AI chipsets and neural processing units (NPUs) in their designs but also developing the necessary software and algorithms that allow these components to function optimally. This dual focus on hardware and software enablement for AI functionalities is crucial for delivering a competitive product. Additionally, AI-driven automation in manufacturing lines and predictive analytics for demand forecasting are transforming ODM operational efficiencies, allowing for faster response times and improved resource allocation in a dynamic market.

- Enhanced Photography and Videography: AI algorithms improve image processing, scene recognition, low-light performance, and computational photography features, becoming a standard offering from ODMs.

- Optimized Performance and Battery Life: AI-driven resource management intelligently allocates processing power and optimizes background tasks, leading to better overall performance and extended battery longevity.

- Advanced User Interface and Experience: AI enables personalized recommendations, more intuitive voice assistants, gesture recognition, and adaptive displays, making smartphones more responsive to individual user habits.

- Manufacturing Process Automation and Efficiency: AI and machine learning are applied in ODM factories for quality control, predictive maintenance of machinery, and optimization of assembly lines, leading to reduced defects and increased output.

- Supply Chain Optimization: AI algorithms analyze vast datasets to predict demand fluctuations, optimize logistics, and identify potential supply chain disruptions, allowing ODMs to maintain efficient inventory and production schedules.

- Edge AI for Data Privacy: Increasing emphasis on processing sensitive data directly on the device using edge AI capabilities, reducing reliance on cloud processing and enhancing user data privacy and security.

Key Takeaways ODM Smartphone Market Size & Forecast

User queries frequently highlight the strategic importance of ODMs in the global smartphone ecosystem, emphasizing their role in democratizing access to advanced mobile technology and enabling a diverse range of brands. The key takeaways from the market size and forecast analysis center on the sustained growth driven by emerging markets, the strategic value of outsourcing for brand agility, and the continuous innovation fostered by ODM capabilities. Stakeholders are particularly interested in understanding how ODMs contribute to cost efficiencies, faster product cycles, and the scaling of new technologies, ensuring competitive pricing and broad availability.

The forecast suggests that the ODM model will continue to be a cornerstone for smartphone brands, allowing them to navigate complex supply chains and rapidly evolving technological landscapes without prohibitive capital investments in manufacturing. This flexibility positions ODMs as critical partners for both established brands looking to streamline operations and new entrants aiming to quickly establish a market presence. The market's robust growth projection underscores a fundamental shift where expertise in design, manufacturing, and supply chain management, centralized within ODMs, becomes a powerful enabler for the broader smartphone industry, facilitating innovation and affordability on a global scale.

- Robust Growth Trajectory: The ODM smartphone market is projected for significant expansion, indicating continued reliance on external manufacturing expertise by brand owners.

- Cost-Efficiency as a Primary Driver: ODMs enable brands to achieve substantial cost savings in production, R&D, and supply chain management, making advanced smartphones more accessible.

- Acceleration of Time-to-Market: The integrated design and manufacturing capabilities of ODMs significantly shorten product development cycles, allowing brands to respond quickly to market trends.

- Enabler for Emerging Brands: The ODM model lowers entry barriers for new smartphone brands, facilitating competition and innovation across the industry.

- Technological Integration Hub: ODMs are crucial for integrating cutting-edge technologies like 5G, AI, and advanced display technologies into mass-market devices efficiently.

- Strategic Partner in Global Supply Chains: ODMs play a vital role in navigating global supply chain complexities, offering resilience and diversified manufacturing options to brand partners.

ODM Smartphone Market Drivers Analysis

The ODM smartphone market is propelled by a confluence of factors, primarily centered around the economic benefits and operational efficiencies they offer to brand owners. The relentless pursuit of cost-effective manufacturing solutions, coupled with the desire for rapid product development cycles, positions ODMs as indispensable partners. Furthermore, the burgeoning smartphone demand in emerging economies, where price sensitivity is high, creates a robust environment for ODM-produced devices that can meet both quality and affordability criteria. This strategic outsourcing model enables brands to focus on core competencies like marketing and software development, delegating complex hardware manufacturing to specialized experts.

Beyond cost and speed, the increasing complexity of smartphone technology also acts as a significant driver. Integrating advanced features such as 5G connectivity, sophisticated camera systems, and AI processors requires specialized engineering expertise and substantial R&D investment, which many brand owners prefer to outsource rather than develop internally. ODMs, with their dedicated R&D teams and manufacturing infrastructures, are well-equipped to handle these complexities, offering ready-to-market solutions that are both innovative and scalable. The global competition in the smartphone sector further intensifies the need for brands to leverage ODM capabilities to maintain a competitive edge and expand market reach efficiently.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Smartphone Penetration in Emerging Markets | +1.5% | Asia Pacific, Latin America, Africa | Long-term (2025-2033) |

| Demand for Cost-Efficient Manufacturing and R&D | +1.2% | Global | Continuous |

| Rapid Technological Advancements (e.g., 5G, AI) | +1.0% | Global | Mid-to-Long term |

| Shortened Product Life Cycles and Time-to-Market Pressure | +0.8% | North America, Europe, Asia Pacific | Short-to-Mid term |

| Brand Focus on Core Competencies (Marketing, Software) | +0.7% | Global | Continuous |

ODM Smartphone Market Restraints Analysis

Despite the robust growth, the ODM smartphone market faces several significant restraints that could temper its expansion. Intense competition among ODMs, coupled with the bargaining power of major brand clients, often leads to compressed profit margins. This pressure can limit investment in advanced R&D and manufacturing upgrades, potentially hindering innovation. Furthermore, geopolitical tensions and trade disputes pose a constant threat, causing supply chain disruptions, increasing raw material costs, and creating uncertainties in global market access for components and finished products. These external factors can significantly impact the stability and predictability of ODM operations.

Another critical restraint is the evolving regulatory landscape, particularly concerning environmental standards, labor practices, and intellectual property rights. Compliance with diverse international regulations adds complexity and cost to ODM operations, especially for those operating across multiple regions. The risk of intellectual property infringement, while often managed through stringent agreements, remains a concern for brand owners, necessitating careful selection and oversight of ODM partners. Additionally, a slowdown in global economic growth or a significant decrease in consumer spending power could directly reduce smartphone demand, thereby impacting ODM production volumes and revenues. The increasing maturity of developed smartphone markets, leading to extended upgrade cycles, also presents a challenge to sustained high growth rates.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Intense Competition and Price Pressure on ODMs | -0.9% | Global | Continuous |

| Geopolitical Tensions and Supply Chain Vulnerabilities | -0.7% | Asia Pacific, North America, Europe | Mid-term |

| Global Economic Slowdown and Reduced Consumer Spending | -0.6% | Global | Short-term |

| Intellectual Property (IP) Infringement Concerns | -0.4% | Global | Long-term |

| Extended Smartphone Upgrade Cycles in Developed Markets | -0.3% | North America, Europe, parts of Asia | Mid-to-Long term |

ODM Smartphone Market Opportunities Analysis

The ODM smartphone market is ripe with opportunities, particularly driven by technological advancements and unmet consumer demands. The burgeoning interest in niche markets, such as ruggedized phones for industrial use, specialized devices for specific enterprise applications, or sustainable smartphones, offers ODMs avenues for diversification and value creation. As brand owners increasingly seek partners capable of integrating advanced technologies like augmented reality (AR) features, sophisticated biometric security, or even satellite connectivity, ODMs with strong R&D capabilities can capture significant market share. The continuous evolution of smartphone form factors, including foldables and rollables, also presents a fertile ground for ODMs to showcase their engineering prowess and design flexibility.

Furthermore, the expansion of the IoT ecosystem and the growing demand for seamlessly connected devices provide new integration opportunities for ODM smartphones within a broader digital landscape. ODMs can leverage their expertise to develop smartphones that act as central hubs for smart homes, wearable devices, and connected vehicles, creating enhanced user experiences. The increasing focus on ethical sourcing and sustainable manufacturing practices by global consumers and regulators also presents an opportunity for ODMs to differentiate themselves by adopting green technologies and transparent supply chains. By proactively addressing these demands, ODMs can attract environmentally conscious brands and consumers, positioning themselves as leaders in responsible manufacturing. The opportunity to serve diverse regional markets with tailored devices, recognizing unique cultural and economic preferences, further enhances the growth potential.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growth in Niche and Specialized Smartphone Markets | +1.3% | Global | Mid-to-Long term |

| Integration of Advanced Technologies (AR, Satellite Connectivity) | +1.0% | North America, Europe, Asia Pacific | Long-term |

| Expansion into IoT and Connected Device Ecosystems | +0.9% | Global | Long-term |

| Increased Demand for Sustainable and Ethical Manufacturing | +0.7% | Europe, North America, parts of Asia | Mid-to-Long term |

| Customization and Regional Market Tailoring | +0.6% | Asia Pacific, Latin America, Africa | Continuous |

ODM Smartphone Market Challenges Impact Analysis

The ODM smartphone market is subject to significant challenges, with rapid technological obsolescence being a primary concern. The constant pressure to integrate the latest chipsets, camera modules, and display technologies means ODMs must continually invest heavily in R&D and retool their manufacturing lines, leading to substantial capital expenditure and a high risk of inventory devaluation. Managing these rapid cycles while maintaining cost-efficiency is a delicate balancing act. Furthermore, the inherent risk of intellectual property disputes, particularly concerning design patents and core technologies, poses a legal and financial threat, demanding robust legal frameworks and careful supplier management.

Another critical challenge stems from the volatility of global component supply chains. Shortages of critical components, such as semiconductors, displays, or memory chips, can halt production, cause delays, and significantly increase costs, directly impacting ODM profitability and their ability to meet client demands. The fierce competition among ODMs, coupled with the strong negotiating power of major clients, results in intense pricing pressures, often compressing profit margins to thin levels. Moreover, attracting and retaining skilled engineering and manufacturing talent capable of handling complex production processes and sophisticated designs remains an ongoing challenge, particularly in regions experiencing labor shortages or high turnover. Maintaining consistent product quality across vast production volumes while adapting to diverse client specifications adds another layer of complexity for ODMs.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Rapid Technological Obsolescence and R&D Investment | -1.0% | Global | Continuous |

| Volatility in Global Component Supply Chains and Costs | -0.8% | Asia Pacific, Global | Short-to-Mid term |

| Intense Pricing Pressure and Thin Profit Margins | -0.7% | Global | Continuous |

| Intellectual Property Protection and Infringement Risks | -0.5% | Global | Long-term |

| Attracting and Retaining Skilled Labor and Talent | -0.4% | Asia Pacific, Europe | Long-term |

ODM Smartphone Market - Updated Report Scope

This market research report provides a comprehensive analysis of the Original Design Manufacturer (ODM) Smartphone Market, detailing its size, growth trends, and future projections across various segments and key regions. The scope encompasses an in-depth examination of market drivers, restraints, opportunities, and challenges that shape the competitive landscape. Through rigorous data collection and expert analysis, the report aims to offer strategic insights into technological advancements, competitive dynamics, and the evolving role of ODMs in the global smartphone industry, providing stakeholders with actionable intelligence for informed decision-making.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 45.3 Billion |

| Market Forecast in 2033 | USD 83.9 Billion |

| Growth Rate | 7.8% |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Foxconn Technology Group, Pegatron Corporation, Wistron Corporation, Compal Electronics Inc., Inventec Corporation, FIH Mobile Ltd., Wingtech Technology Co. Ltd., Huaqin Telecom Technology Co. Ltd., Longcheer Technology, CK Telecom Ltd., DBG Technology Co. Ltd., BYD Electronic (International) Co. Ltd., Optiemus Infracom Ltd., Dixon Technologies (India) Ltd., Lava International Ltd., Simmtronics Semiconductors Ltd., Karbonn Mobiles, Micromax Informatics Ltd., Celkon Mobiles, Gionee Communication Equipment Co. Ltd. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The ODM smartphone market is comprehensively segmented to provide granular insights into its diverse components, reflecting various product types, technological integrations, operating systems, distribution channels, and end-user applications. This segmentation analysis helps stakeholders understand the specific dynamics and growth drivers within each sub-market, enabling targeted strategic planning and investment. The detailed breakdown allows for a clearer picture of market maturity, consumer preferences, and technological adoption rates across different categories, identifying both saturated and nascent areas for expansion.

Understanding these segments is crucial for ODMs to tailor their offerings effectively and for brand owners to select the most suitable manufacturing partners. For instance, the demand for high-end versus low-end devices varies significantly across regions, influencing production volumes and feature sets. Similarly, the prevalence of 5G technology is still geographically concentrated, dictating the focus of technological development. The analysis also differentiates between consumer and enterprise applications, recognizing their distinct requirements for security, ruggedness, and software integration, thereby offering a multifaceted view of the ODM smartphone ecosystem.

- By Type: This segment classifies smartphones based on their pricing and feature sets, including high-end, mid-range, and low-end devices, reflecting diverse consumer purchasing power and market strategies.

- By Operating System: Primarily dominated by Android, this segment also includes other operating systems, highlighting the platforms ODMs specialize in developing for.

- By Technology: Categorization by network technology, such as 5G, 4G, and older generations (3G & 2G), demonstrates the market's progression and regional technological readiness.

- By Distribution Channel: This segment outlines how ODM-produced smartphones reach end-users, including through direct partnerships with Original Equipment Manufacturers (OEMs), brand owners, telecommunication companies, and various retail channels.

- By End-user: Differentiation between consumer and enterprise users helps identify specific feature requirements, volume demands, and vertical market opportunities for ODM services.

Regional Highlights

- Asia Pacific (APAC): Dominates the ODM smartphone market due to a large manufacturing base, high smartphone penetration in emerging economies like India and Southeast Asia, and robust demand for affordable, feature-rich devices. China remains a global hub for ODM operations and supply chain infrastructure.

- North America: Characterized by demand for high-end and technologically advanced smartphones, with ODMs often partnering with established brands to integrate cutting-edge features and manage complex supply chains for premium devices. Focus on 5G, AI, and secure enterprise solutions.

- Europe: Exhibits a strong emphasis on sustainability, ethical manufacturing, and privacy features, influencing ODM production practices and material sourcing. Demand is balanced between mid-range and high-end devices, with a growing interest in devices from niche brands.

- Latin America: A rapidly growing market for ODM smartphones, driven by increasing internet penetration, urbanization, and a strong preference for value-for-money devices. ODMs cater to local market demands for specific features and pricing strategies.

- Middle East and Africa (MEA): Emerging as a significant growth region, with increasing smartphone adoption rates, particularly in affordable and entry-level segments. ODMs are crucial in providing accessible technology to a rapidly expanding consumer base across diverse markets.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the ODM Smartphone Market.- Foxconn Technology Group

- Pegatron Corporation

- Wistron Corporation

- Compal Electronics Inc.

- Inventec Corporation

- FIH Mobile Ltd.

- Wingtech Technology Co. Ltd.

- Huaqin Telecom Technology Co. Ltd.

- Longcheer Technology

- CK Telecom Ltd.

- DBG Technology Co. Ltd.

- BYD Electronic (International) Co. Ltd.

- Optiemus Infracom Ltd.

- Dixon Technologies (India) Ltd.

- Lava International Ltd.

- Simmtronics Semiconductors Ltd.

- Karbonn Mobiles

- Micromax Informatics Ltd.

- Celkon Mobiles

- Gionee Communication Equipment Co. Ltd.

Frequently Asked Questions

What is the current market size and projected growth rate of the ODM Smartphone Market?

The ODM Smartphone Market is estimated at USD 45.3 Billion in 2025 and is projected to reach USD 83.9 Billion by 2033, demonstrating a Compound Annual Growth Rate (CAGR) of 7.8% during the forecast period.

What are the primary drivers for the growth of the ODM Smartphone Market?

Key drivers include increasing smartphone penetration in emerging markets, demand for cost-efficient manufacturing, rapid technological advancements like 5G and AI, and brand owners focusing on core competencies by outsourcing production.

How does AI impact the ODM Smartphone Market?

AI significantly impacts the ODM smartphone market by enhancing photography, optimizing performance and battery life, improving user interfaces, and increasing efficiency in manufacturing processes and supply chain management.

Which regions are key contributors to the ODM Smartphone Market?

Asia Pacific is the leading region due to extensive manufacturing capabilities and high demand, followed by North America and Europe, which drive innovation and demand for advanced features. Latin America and MEA are emerging as significant growth areas.

What challenges does the ODM Smartphone Market face?

Challenges include rapid technological obsolescence, volatility in global component supply chains, intense pricing pressure, intellectual property protection concerns, and the need to attract and retain skilled labor.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted