Nuclear Filter Market

Nuclear Filter Market Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_707758 | Last Updated : September 08, 2025 |

Format : ![]()

![]()

![]()

![]()

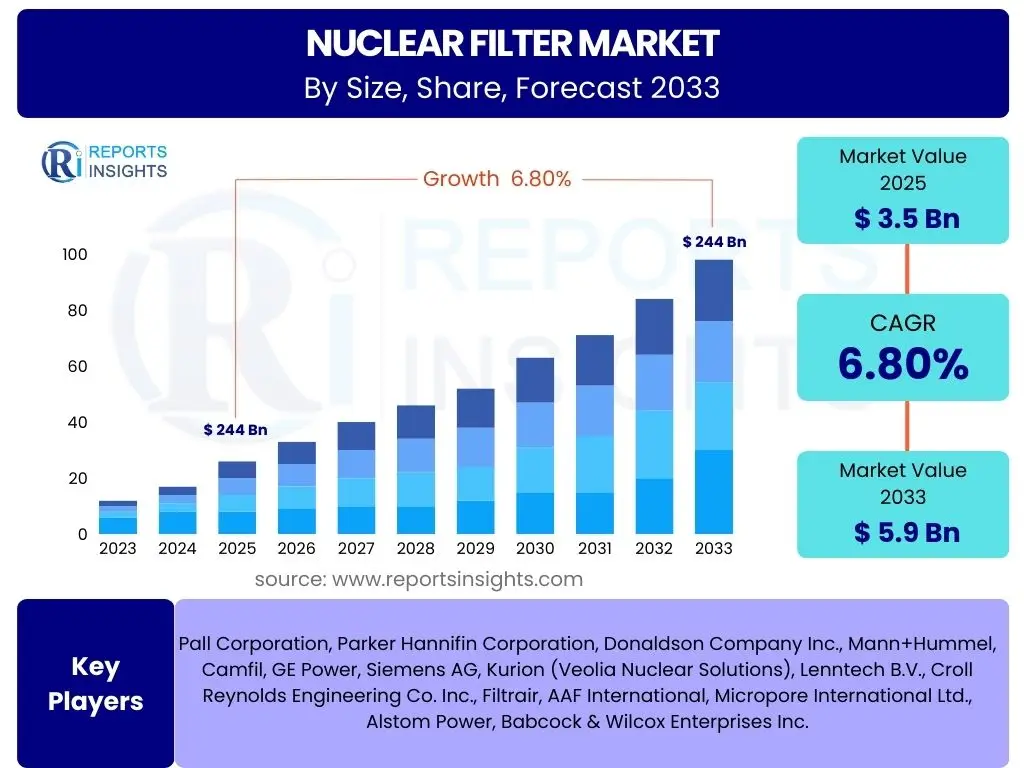

Nuclear Filter Market Size

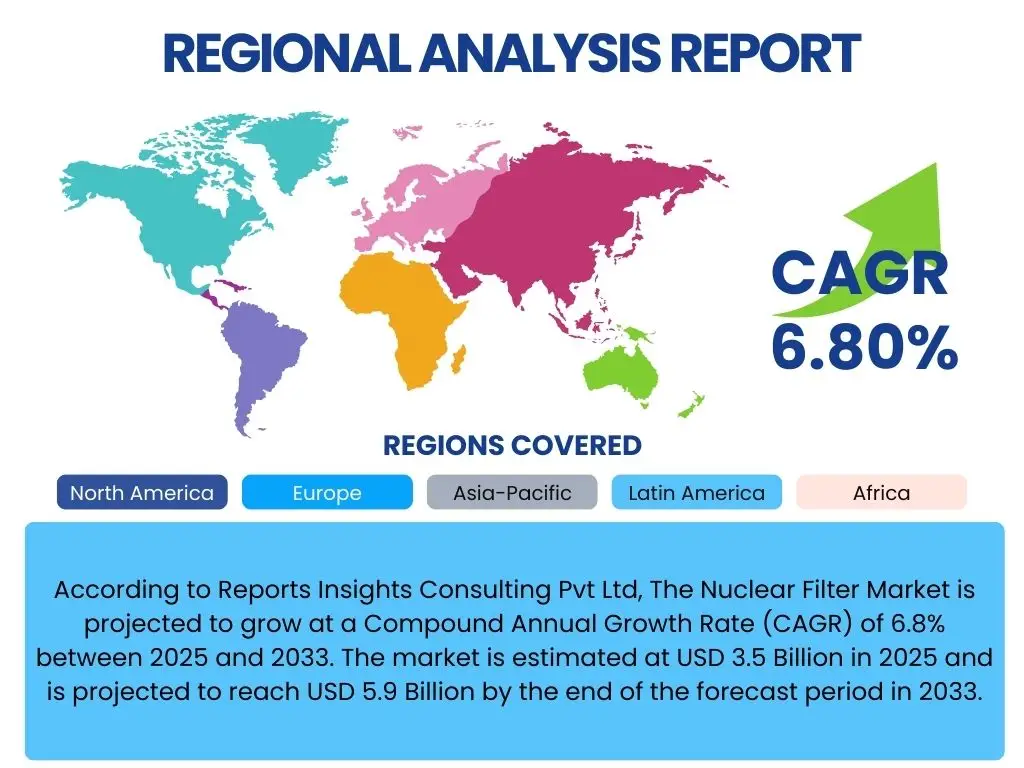

According to Reports Insights Consulting Pvt Ltd, The Nuclear Filter Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2025 and 2033. The market is estimated at USD 3.5 Billion in 2025 and is projected to reach USD 5.9 Billion by the end of the forecast period in 2033.

Key Nuclear Filter Market Trends & Insights

Current market trends in nuclear filtration are heavily influenced by the global energy transition, stringent safety regulations, and advancements in material science. There is a growing emphasis on high-efficiency particulate air (HEPA) filters and activated carbon filters due to their critical role in preventing radioactive material release and ensuring air quality within nuclear facilities. The push for cleaner energy sources worldwide is fostering renewed interest in nuclear power, which in turn necessitates robust filtration solutions for both operational safety and waste management.

Technological innovation is also a significant driver, with research and development focusing on longer-lasting filter media, smart filtration systems, and solutions for managing complex waste streams. The development and deployment of Small Modular Reactors (SMRs) are anticipated to introduce new design considerations for filtration, potentially driving demand for compact, highly efficient, and integrated filter systems. Furthermore, decommissioning activities for older nuclear power plants present a unique set of filtration challenges, requiring specialized solutions for decontamination and waste volume reduction.

- Increased adoption of advanced HEPA and activated carbon filter technologies.

- Growing demand driven by new nuclear power plant constructions and SMR deployment.

- Focus on extended filter lifespan and reduced maintenance requirements.

- Integration of smart monitoring and predictive maintenance for filtration systems.

- Development of specialized filters for nuclear waste processing and decommissioning.

- Emphasis on filtration solutions for tritium removal and radionuclide capture.

AI Impact Analysis on Nuclear Filter

The integration of Artificial Intelligence (AI) and machine learning (ML) is poised to significantly transform the nuclear filter market by enhancing operational efficiency, predictive maintenance, and overall safety. Users are increasingly seeking information on how AI can optimize filter performance, extend service life, and reduce manual intervention. AI-powered analytics can process vast amounts of sensor data from filtration systems to detect anomalies, predict potential failures before they occur, and schedule maintenance proactively, thereby minimizing downtime and operational costs in critical nuclear environments.

Beyond predictive maintenance, AI also holds promise in optimizing filter design and material selection. Generative design algorithms can explore countless design iterations for filters, identifying optimal configurations for fluid dynamics, particulate capture efficiency, and radiation resistance, which would be impossible for human engineers alone. Furthermore, AI can contribute to real-time monitoring of air and water quality within nuclear facilities, ensuring immediate detection of contaminants and enabling rapid response, which is crucial for safety and regulatory compliance. The demand for intelligent filtration solutions capable of self-diagnosis and adaptive operation is a key user expectation.

- Predictive maintenance for filtration systems, reducing unscheduled downtime.

- Optimized filter performance through real-time data analysis and adaptive control.

- Enhanced safety protocols by AI-driven anomaly detection in air and water quality.

- AI-assisted design and material selection for more efficient and durable filters.

- Automation of routine filter monitoring and diagnostic processes.

- Improved supply chain management and inventory optimization for filter consumables.

Key Takeaways Nuclear Filter Market Size & Forecast

The Nuclear Filter Market is set for consistent growth, primarily driven by the global imperative for clean energy and the inherent safety requirements of nuclear power generation. A key takeaway is the significant role of regulatory frameworks and public acceptance in shaping market dynamics, as stringent safety standards directly mandate the use of high-performance filtration technologies. The market's expansion is not only tied to new reactor builds but also to the ongoing maintenance, upgrades, and decommissioning activities of existing facilities, ensuring a diversified demand base across the entire nuclear lifecycle.

Another crucial insight is the accelerating pace of technological innovation, particularly in advanced materials and smart systems, which is enhancing filter efficiency, durability, and cost-effectiveness. The emergence of Small Modular Reactors (SMRs) represents a novel growth avenue, requiring bespoke filtration solutions that are compact yet highly effective. Furthermore, the market is characterized by a strong emphasis on sustainability and waste reduction, pushing manufacturers to develop filters with longer service lives and easier disposal methods, aligning with broader environmental goals.

- Steady market growth projected, reaching USD 5.9 Billion by 2033.

- Strong demand driven by new nuclear plant constructions and existing facility maintenance.

- Technological advancements in filter media and smart systems are pivotal for market evolution.

- Small Modular Reactors (SMRs) poised to open new market segments for specialized filters.

- Regulatory compliance and safety standards are fundamental growth drivers.

- Focus on reducing operational costs and improving filter lifecycle management.

Nuclear Filter Market Drivers Analysis

The global shift towards clean energy sources and the increasing demand for electricity are primary drivers propelling the nuclear filter market. Nuclear power, as a low-carbon energy source, is gaining renewed attention from governments worldwide seeking to reduce greenhouse gas emissions and enhance energy security. This resurgence in nuclear energy development, including the construction of new large-scale reactors and the proliferation of Small Modular Reactors (SMRs), directly translates into higher demand for specialized filtration systems essential for safe and efficient plant operation.

Furthermore, stringent regulatory frameworks and escalating safety concerns within the nuclear industry are significant drivers. Regulatory bodies consistently update and enforce stricter standards for radioactive emissions and worker safety, necessitating the deployment of advanced and highly efficient nuclear filters. Compliance with these evolving regulations compels nuclear operators to invest in cutting-edge filtration technologies to mitigate risks associated with airborne contaminants, radioactive particulates, and liquid waste streams, thereby ensuring environmental protection and public health. The aging nuclear infrastructure in many developed nations also requires ongoing maintenance, upgrades, and component replacements, including filters, to meet modern safety requirements and extend operational lifespans.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Global Demand for Clean Energy & Nuclear Revival | +2.1% | Asia Pacific (China, India), Europe, North America | 2025-2033 (Long-term) |

| Stringent Nuclear Safety Regulations & Standards | +1.8% | Global, particularly North America, Europe, Japan | 2025-2033 (Ongoing) |

| Aging Nuclear Infrastructure Modernization | +1.5% | North America (USA), Europe (France, UK), Japan | 2025-2030 (Mid-term) |

| Growth in Nuclear Waste Management & Decommissioning | +1.4% | Global, especially highly industrialized nations | 2025-2033 (Long-term) |

Nuclear Filter Market Restraints Analysis

Despite the positive growth trajectory, the nuclear filter market faces several significant restraints that could impede its expansion. One major hurdle is the substantial capital investment and high operational costs associated with nuclear power plant construction and maintenance. The lengthy and complex approval processes, coupled with the immense financial outlay required for a nuclear project, often deter new investments and can lead to project delays or cancellations. This directly impacts the demand for new filtration systems, particularly for large-scale projects.

Another critical restraint is the persistent public apprehension and negative perception surrounding nuclear energy, largely due to historical accidents and concerns about radioactive waste disposal. This public resistance can lead to political opposition, stricter regulatory hurdles, and difficulties in site selection for new nuclear facilities, thus slowing down market growth. Furthermore, the specialized nature of nuclear filtration requires highly specific materials and manufacturing processes, leading to a relatively limited number of suppliers and potential supply chain vulnerabilities. The disposal of spent nuclear filters, which can be radioactive, also presents an ongoing environmental and economic challenge, adding to the overall cost and complexity of nuclear operations.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Capital Costs & Long Project Timelines | -1.2% | Global, especially emerging markets | 2025-2033 (Long-term) |

| Public Perception & Opposition to Nuclear Power | -1.0% | Europe, North America, Japan | 2025-2033 (Ongoing) |

| Strict Regulatory Hurdles & Licensing Delays | -0.8% | Global, particularly Western countries | 2025-2030 (Mid-term) |

| Complex Nuclear Waste Disposal Challenges | -0.7% | Global, especially countries with existing nuclear fleets | 2025-2033 (Long-term) |

Nuclear Filter Market Opportunities Analysis

The development and increasing adoption of Small Modular Reactors (SMRs) represent a significant growth opportunity for the nuclear filter market. SMRs offer several advantages, including reduced upfront capital costs, shorter construction times, and enhanced safety features, making them an attractive option for expanding nuclear energy capacity. As SMR technology matures and gains wider acceptance, it will create substantial demand for compact, highly efficient, and integrated filtration systems tailored to their unique design and operational parameters, opening new market avenues for specialized filter manufacturers.

Technological advancements in filtration materials and smart monitoring systems also present lucrative opportunities. Innovations in nanofiber technology, advanced ceramics, and composite materials are leading to the development of filters with superior capture efficiency, extended lifespans, and improved resistance to harsh nuclear environments. Furthermore, the integration of IoT sensors, AI-powered analytics, and predictive maintenance capabilities into filtration systems allows for real-time performance monitoring, optimized filter replacement schedules, and reduced operational downtime. These advancements not only enhance safety and efficiency but also create opportunities for value-added services and smart filtration solutions, appealing to nuclear operators seeking to modernize their infrastructure and improve cost-effectiveness.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing Adoption of Small Modular Reactors (SMRs) | +1.9% | North America, Europe, Asia Pacific (Canada, US, UK, China) | 2027-2033 (Mid- to Long-term) |

| Technological Advancements in Filter Materials & Smart Systems | +1.6% | Global, especially R&D strong regions | 2025-2033 (Ongoing) |

| Increased Focus on Decommissioning & Waste Treatment | +1.3% | Europe, North America, Japan (countries with older fleets) | 2025-2033 (Long-term) |

| Expansion into Emerging Nuclear Programs | +1.0% | Middle East (UAE, Saudi Arabia), Southeast Asia, Africa | 2028-2033 (Long-term) |

Nuclear Filter Market Challenges Impact Analysis

The nuclear filter market faces significant challenges, primarily stemming from the inherent complexities and high-stakes nature of the nuclear industry. One major challenge is the stringent regulatory environment and the extremely long lead times for product development and approval. Nuclear-grade filters must undergo rigorous testing and certification processes to meet strict safety and performance standards, which can be time-consuming and costly. This lengthy approval cycle can delay market entry for innovative products and increase development expenses, impacting profitability and discouraging new entrants.

Another key challenge is the specialized skill set required for the design, manufacturing, installation, and maintenance of nuclear filtration systems. A shortage of skilled engineers, technicians, and specialized labor within the nuclear sector poses a significant barrier to market growth and operational efficiency. Furthermore, the geopolitical landscape and international relations can significantly impact nuclear energy projects. Political instability, trade disputes, or changes in energy policies can lead to project delays, cancellations, or shifts in national energy strategies, creating market uncertainty and affecting demand for nuclear filters. Supply chain vulnerabilities for highly specialized components and materials also present a challenge, particularly in a globalized yet often protected nuclear supply ecosystem.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Rigorous Regulatory Compliance & Certification | -0.9% | Global | 2025-2033 (Ongoing) |

| Skilled Labor Shortage in Nuclear Sector | -0.8% | North America, Europe | 2025-2030 (Mid-term) |

| Supply Chain Vulnerabilities & Material Sourcing | -0.7% | Global | 2025-2028 (Short-term to Mid-term) |

| Geopolitical Risks & Policy Instability | -0.6% | Global, country-specific | 2025-2033 (Variable) |

Nuclear Filter Market - Updated Report Scope

This report provides a comprehensive analysis of the Nuclear Filter Market, encompassing market size estimations, growth forecasts, and detailed segmentation. It examines key market trends, the impact of artificial intelligence, and a thorough analysis of drivers, restraints, opportunities, and challenges influencing market dynamics. The scope extends to regional insights and profiles of prominent market players, offering a holistic view of the industry landscape from 2019 to 2033.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 3.5 Billion |

| Market Forecast in 2033 | USD 5.9 Billion |

| Growth Rate | 6.8% CAGR |

| Number of Pages | 245 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Pall Corporation, Parker Hannifin Corporation, Donaldson Company Inc., Mann+Hummel, Camfil, GE Power, Siemens AG, Kurion (Veolia Nuclear Solutions), Lenntech B.V., Croll Reynolds Engineering Co. Inc., Filtrair, AAF International, Micropore International Ltd., Alstom Power, Babcock & Wilcox Enterprises Inc. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Nuclear Filter Market is extensively segmented based on filter type, material, and application, reflecting the diverse and specialized needs of the nuclear industry. Each segment plays a crucial role in ensuring safety, environmental protection, and operational efficiency within nuclear facilities. The market for nuclear filters is not monolithic; rather, it is characterized by specific technological requirements for handling various types of contaminants, from airborne radioactive particulates to liquid effluents and corrosive chemicals.

By understanding these distinct segments, stakeholders can better identify niche opportunities, tailor product development, and strategize market entry or expansion. The dominant segments, such as HEPA and activated carbon filters, are driven by their indispensable role in air purification and radionuclide capture. Meanwhile, the material segment highlights the importance of durability and resistance to harsh environments, critical for filter longevity and performance. Application-wise, nuclear power plants remain the largest consumers, but emerging areas like nuclear waste management and decommissioning are rapidly growing, demanding specialized and robust filtration solutions.

- By Type: HEPA Filters, Activated Carbon Filters, Liquid Filters, Cartridge Filters, Others

- By Material: Fiberglass, Polypropylene, Stainless Steel, Carbon Fiber, Others

- By Application: Nuclear Power Plants (Pressurized Water Reactors (PWR), Boiling Water Reactors (BWR), CANDU Reactors, VVER Reactors, Small Modular Reactors (SMRs)), Nuclear Waste Management Facilities, Research Reactors, Decommissioning Activities, Fuel Reprocessing Plants, Others

Regional Highlights

- North America: This region holds a significant share in the Nuclear Filter Market, driven by a large base of aging nuclear power plants requiring modernization and decommissioning, as well as new investments in SMR technology. The United States, in particular, has stringent regulatory standards and a robust research and development ecosystem that fosters innovation in nuclear filtration. Canada is also a key player due to its CANDU reactor fleet and active nuclear waste management programs.

- Europe: Europe represents a mature market with a considerable number of operational nuclear reactors and extensive decommissioning projects, particularly in countries like France, the UK, Germany, and Belgium. The region benefits from strong regulatory oversight and a collective push towards advanced nuclear technologies. Eastern European countries are also exploring new reactor builds, contributing to sustained demand for filters.

- Asia Pacific (APAC): The APAC region is projected to be the fastest-growing market for nuclear filters, primarily due to the rapid expansion of nuclear power programs in China, India, and South Korea. These countries are investing heavily in new reactor construction to meet escalating energy demands and combat climate change. Japan, despite its recent nuclear challenges, maintains a strong focus on nuclear safety and waste management, driving demand for advanced filtration solutions.

- Latin America: This region has a smaller but growing nuclear power footprint, with countries like Argentina, Brazil, and Mexico operating or planning nuclear facilities. The demand for nuclear filters here is expected to grow steadily, largely influenced by national energy policies and international collaborations aimed at expanding nuclear energy capacity.

- Middle East and Africa (MEA): The MEA region is emerging as a potential growth market, with countries like the UAE and Saudi Arabia investing in their first nuclear power plants to diversify energy sources. While currently a smaller market, the long-term outlook is positive as more nations in the region explore nuclear energy as a viable option, consequently driving demand for associated filtration technologies.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Nuclear Filter Market.- Pall Corporation

- Parker Hannifin Corporation

- Donaldson Company Inc.

- Mann+Hummel

- Camfil

- GE Power

- Siemens AG

- Kurion (Veolia Nuclear Solutions)

- Lenntech B.V.

- Croll Reynolds Engineering Co. Inc.

- Filtrair

- AAF International

- Micropore International Ltd.

- Alstom Power

- Babcock & Wilcox Enterprises Inc.

- Mitsubishi Heavy Industries, Ltd.

- SUEZ Water Technologies & Solutions

- U.S. Nuclear Corp.

- Eaton Corporation plc

- Pentair plc

Frequently Asked Questions

What is the projected growth rate of the Nuclear Filter Market?

The Nuclear Filter Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2025 and 2033, reaching an estimated USD 5.9 Billion by the end of the forecast period.

What are the primary drivers for the Nuclear Filter Market?

Key drivers include the global demand for clean energy and a resurgence in nuclear power initiatives, stringent nuclear safety regulations, ongoing modernization of aging nuclear infrastructure, and the increasing focus on nuclear waste management and decommissioning activities.

How is AI impacting the Nuclear Filter Market?

AI is transforming the market through predictive maintenance for filtration systems, optimized filter design, enhanced safety protocols via real-time anomaly detection, and automation of monitoring processes, leading to improved efficiency and reduced operational costs.

Which regions are key contributors to the Nuclear Filter Market?

North America and Europe currently hold significant market shares due to established nuclear fleets and ongoing maintenance. However, Asia Pacific, particularly China and India, is expected to be the fastest-growing region due to significant investments in new nuclear power plant construction.

What are the main types of filters used in nuclear applications?

The main types of filters include High-Efficiency Particulate Air (HEPA) filters for airborne contaminants, activated carbon filters for gaseous radionuclides, liquid filters for water treatment, and various cartridge filters designed for specific waste streams and applications.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted