Diesel Locomotive Engine Market

Diesel Locomotive Engine Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_705558 | Last Updated : August 17, 2025 |

Format : ![]()

![]()

![]()

![]()

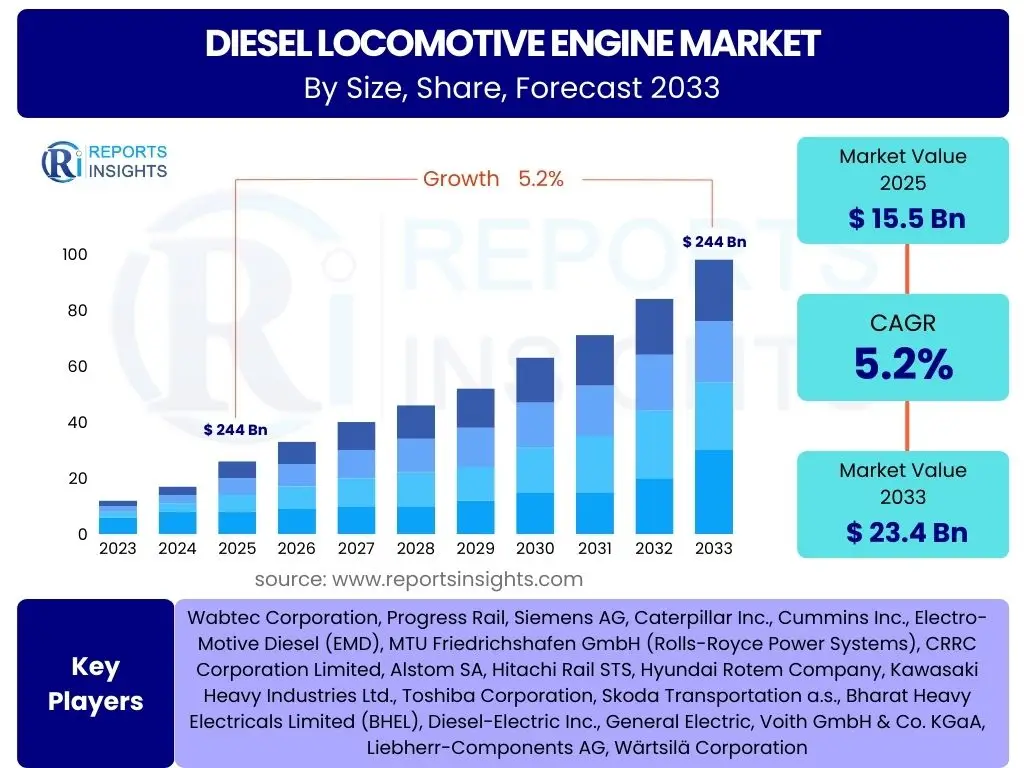

Diesel Locomotive Engine Market Size

According to Reports Insights Consulting Pvt Ltd, The Diesel Locomotive Engine Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.2% between 2025 and 2033. The market is estimated at USD 15.5 Billion in 2025 and is projected to reach USD 23.4 Billion by the end of the forecast period in 2033.

Key Diesel Locomotive Engine Market Trends & Insights

The diesel locomotive engine market is currently navigating a period of significant transformation, driven by a dual focus on operational efficiency and environmental sustainability. User inquiries frequently highlight the ongoing relevance of diesel technology despite the push for electrification, particularly in heavy freight and long-haul applications where its power density and range remain unparalleled. Key trends revolve around advancements in engine design, aiming to reduce emissions and improve fuel economy, while simultaneously leveraging digital technologies to enhance performance and reliability. The integration of smart systems for predictive maintenance and real-time diagnostics is becoming a standard expectation, signaling a shift towards more data-driven and proactive operational models within the rail industry.

Another prominent area of interest among users concerns the balance between regulatory pressures and economic viability. The global push for lower carbon footprints is compelling manufacturers to innovate, developing engines that comply with stringent emission standards (e.g., Tier 4 Final, Stage V). This includes exploring alternative fuels or hybridization concepts, which, while not fully replacing diesel, aim to reduce its environmental impact. Furthermore, the robust demand for freight transportation, especially in emerging economies, underscores the continued need for powerful and durable locomotive engines, ensuring a sustained market for diesel-based solutions.

The market is also witnessing an emphasis on modularity and upgradeability, allowing operators to extend the lifespan of their existing locomotive fleets through engine modernizations rather than full replacements. This approach not only provides a cost-effective solution but also facilitates the adoption of newer, more efficient engine technologies. Geopolitical factors and fluctuating raw material costs also play a role in shaping market dynamics, influencing investment decisions and supply chain strategies across the globe.

- Advanced Emission Control Systems: Development and adoption of technologies to meet stringent global emission standards, such as Tier 4 Final and Stage V.

- Fuel Efficiency Optimization: Focus on engine designs and operational strategies that reduce fuel consumption and operating costs.

- Digitalization and Connectivity: Integration of IoT, telematics, and data analytics for remote monitoring, diagnostics, and predictive maintenance.

- Hybridization and Dual-Fuel Concepts: Exploration and implementation of hybrid-electric or dual-fuel (e.g., LNG-diesel) engine solutions to enhance environmental performance.

- Lifecycle Extension through Modernization: Increasing trend of upgrading existing locomotive fleets with new, more efficient engines rather than full replacement.

- Robust Demand from Freight Sector: Sustained growth in global freight volumes driving the need for high-performance diesel locomotive engines.

- Emerging Market Infrastructure Development: Significant investments in railway infrastructure in developing economies, particularly in Asia Pacific and Africa.

AI Impact Analysis on Diesel Locomotive Engine

The integration of Artificial Intelligence (AI) into the diesel locomotive engine domain is a topic of increasing user inquiry, primarily focusing on its transformative potential across maintenance, operational efficiency, and safety. Users are keen to understand how AI can move beyond traditional reactive maintenance to predictive and prescriptive models, minimizing downtime and optimizing engine performance. AI algorithms can analyze vast datasets from engine sensors, identifying subtle patterns that indicate potential failures long before they occur, thereby enabling proactive interventions and significantly reducing unscheduled maintenance events. This capability is paramount for railway operators striving to maintain strict schedules and reduce operational costs, making AI a critical enabler for smart asset management.

Beyond maintenance, AI's influence extends to enhancing the operational efficiency of diesel locomotive engines. User questions often explore AI's role in optimizing fuel consumption, a significant operating expense for railway companies. AI-powered systems can analyze real-time variables such as terrain, load, speed, and track conditions to recommend optimal engine power settings and driving techniques, leading to substantial fuel savings. Furthermore, AI contributes to enhanced safety protocols by monitoring engine parameters for anomalies that might compromise operational integrity, providing early warnings to operators and maintenance teams. This proactive approach to safety not only protects equipment but, more importantly, ensures the well-being of personnel and the public.

The future impact of AI also encompasses the potential for more autonomous operations and sophisticated decision-making at the edge. While fully autonomous diesel locomotives are still nascent, AI is paving the way for advanced driver assistance systems that optimize train handling, reduce human error, and improve overall network fluidity. The continuous learning capabilities of AI systems mean that engine performance and operational strategies can be perpetually refined based on accumulating data, leading to a cycle of continuous improvement. This adaptability and intelligence are what users anticipate will drive the next wave of innovation in diesel locomotive engine technology.

- Predictive Maintenance: AI algorithms analyze sensor data to forecast equipment failures, enabling proactive repairs and reducing downtime.

- Optimized Fuel Consumption: AI systems recommend optimal engine settings and driving patterns based on real-time conditions, leading to significant fuel savings.

- Enhanced Operational Efficiency: AI facilitates real-time monitoring and adjustment of engine performance for optimal power output and reduced wear.

- Improved Safety: AI can detect anomalies in engine operation that may indicate a safety risk, providing early warnings to operators.

- Autonomous Operation Potential: Paving the way for advanced driver assistance systems and, eventually, more autonomous train control.

- Data-Driven Decision Making: Provides actionable insights from engine performance data, supporting strategic maintenance and operational planning.

Key Takeaways Diesel Locomotive Engine Market Size & Forecast

The Diesel Locomotive Engine market is poised for steady expansion through 2033, driven by the indispensable role of rail transport in global logistics and infrastructure development. User inquiries frequently highlight the market's resilience despite environmental pressures, emphasizing that the sheer power, range, and operational flexibility of diesel engines remain critical for heavy freight and challenging terrain where electrification is not yet feasible or cost-effective. The forecast indicates a sustained demand for new engines, alongside a robust market for modernization and upgrades of existing fleets, especially as operators seek to improve efficiency and comply with evolving emission standards. The growth trajectory is firmly linked to global economic activity, trade volumes, and ongoing investments in railway networks, particularly in rapidly developing regions.

A significant takeaway is the strategic shift by manufacturers towards developing more environmentally conscious diesel engines. This involves not only meeting stricter emission regulations but also exploring hybrid technologies and digital solutions that enhance fuel efficiency and reduce the overall carbon footprint. The market's growth is therefore not just about increasing unit sales but also about technological evolution and adapting to a greener operational paradigm. This dual focus on power and responsibility ensures the continued relevance of diesel locomotive engines in the broader transportation ecosystem.

Furthermore, the market exhibits a clear segmentation in terms of regional growth. While mature markets in North America and Europe will see demand driven primarily by fleet replacement and modernization, emerging economies in Asia Pacific, Latin America, and Africa are expected to fuel significant growth due to extensive railway infrastructure development and increased freight movement. This geographical diversity underscores varied market dynamics, where different regions prioritize either technological upgrades or fundamental infrastructure expansion, collectively contributing to the overall positive market outlook.

- Sustained Growth Trajectory: The market is projected for continuous growth, reflecting the enduring importance of diesel power in rail transport.

- Technological Evolution is Key: Manufacturers are prioritizing engines with lower emissions, higher fuel efficiency, and integrated digital capabilities.

- Modernization Drives Demand: Significant demand stems from the upgrading and retrofitting of existing locomotive fleets to meet contemporary standards.

- Freight Dominance: The market's robust growth is primarily propelled by the increasing volume of global freight transportation.

- Regional Disparities in Growth: Emerging economies are leading new infrastructure-driven demand, while mature markets focus on replacement and upgrades.

- Adaptability to Regulations: The industry is actively investing in R&D to ensure compliance with increasingly stringent environmental regulations.

Diesel Locomotive Engine Market Drivers Analysis

The growth of the diesel locomotive engine market is fundamentally propelled by the expanding global demand for efficient and reliable freight and passenger rail transportation. As economies worldwide grow, the volume of goods being transported across vast distances increases, placing higher demands on rail networks. Diesel locomotives, known for their high tractive effort and operational flexibility, remain the backbone of heavy-haul freight operations, especially in regions with extensive rail networks or challenging topographies where electrification is not viable. Furthermore, significant investments in railway infrastructure development, particularly in emerging markets, are creating new opportunities for locomotive manufacturers and, consequently, for diesel engine suppliers. These infrastructure projects often involve the construction of new rail lines, modernization of existing ones, and expansion of freight corridors, all requiring robust and powerful locomotive engines.

Another crucial driver is the ongoing need for fleet modernization and replacement. Many existing locomotive fleets globally are aging, necessitating upgrades to improve efficiency, reduce emissions, and enhance reliability. Railway operators are increasingly looking for engines that offer better fuel economy, lower maintenance costs, and advanced diagnostic capabilities, aligning with modern operational requirements. This replacement cycle, combined with the continuous push for higher operational efficiency and stricter environmental compliance, ensures a steady demand for technologically advanced diesel locomotive engines. The ability of modern diesel engines to incorporate advanced digital controls and achieve higher power output per unit of fuel also contributes significantly to their continued market relevance and adoption.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Global Growth in Freight & Passenger Rail Traffic | +0.8% | Global, particularly APAC & Africa | Short-Mid Term |

| Increasing Investments in Railway Infrastructure Development | +0.7% | APAC, Latin America, MEA | Mid-Long Term |

| Fleet Modernization & Replacement of Aging Locomotives | +0.6% | North America, Europe, China, India | Short-Mid Term |

| Demand for Fuel-Efficient & Low-Emission Engines | +0.5% | Global | Mid-Long Term |

| Advancements in Engine Technology (e.g., Digital Controls) | +0.4% | Global | Mid-Long Term |

Diesel Locomotive Engine Market Restraints Analysis

The diesel locomotive engine market faces significant restraints, primarily stemming from the global imperative for decarbonization and the increasingly stringent environmental regulations. Governments and regulatory bodies worldwide are implementing stricter emission standards (e.g., Euro 7, Tier 5) for internal combustion engines, compelling manufacturers to invest heavily in research and development for cleaner technologies. These regulations often necessitate complex and expensive after-treatment systems, such as selective catalytic reduction (SCR) and diesel particulate filters (DPF), which increase the overall cost and complexity of the engines. The constant pressure to reduce greenhouse gas emissions is also driving a shift towards alternative propulsion systems, including full electrification, hydrogen fuel cells, and battery-powered locomotives, which directly compete with diesel technology and threaten its long-term market share, particularly in developed regions with extensive electrified networks.

Another notable restraint is the high initial capital expenditure associated with purchasing and maintaining diesel locomotives, including their engines. While diesel offers operational flexibility, the upfront investment can be substantial, especially for advanced, compliant engines. Furthermore, the long operational lifespan of existing diesel locomotives means that replacement cycles are extended, slowing down the adoption of newer engine technologies. The volatility of diesel fuel prices also introduces an element of uncertainty for railway operators, impacting their operational budgets and influencing investment decisions towards potentially more stable energy sources. These economic and regulatory challenges combined pose a considerable hurdle to the uninhibited growth of the diesel locomotive engine market.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Stringent Environmental Regulations & Emission Standards | -0.7% | Europe, North America, China | Short-Long Term |

| Increasing Shift Towards Electrification & Alternative Fuels | -0.6% | Europe, North America | Mid-Long Term |

| High Initial Capital Costs & Long Operational Lifespan of Assets | -0.5% | Global | Short-Mid Term |

| Volatility in Diesel Fuel Prices | -0.4% | Global | Short Term |

| Competition from Other Modes of Transport (e.g., Road Freight) | -0.3% | Global | Short-Mid Term |

Diesel Locomotive Engine Market Opportunities Analysis

The diesel locomotive engine market presents significant opportunities for innovation and growth, particularly through the development and adoption of advanced engine technologies. The increasing focus on sustainability is creating avenues for hybrid-electric and dual-fuel (e.g., diesel-LNG or diesel-hydrogen) engine solutions that combine the power and range of diesel with reduced emissions. These hybrid systems allow operators to achieve greater fuel efficiency and environmental compliance without fully abandoning their existing diesel infrastructure. Furthermore, the global trend of railway network expansion, especially in emerging economies, represents a substantial opportunity for new engine sales. Countries in Asia Pacific, Latin America, and Africa are investing heavily in new freight corridors and passenger lines, necessitating a fresh supply of powerful and reliable locomotive engines tailored to local operational conditions.

Another major opportunity lies in the aftermarket services and modernization segment. With a large installed base of existing diesel locomotives, there is a strong demand for retrofitting older engines with modern components and control systems. This enables operators to extend the useful life of their assets while upgrading them to meet contemporary performance and emission standards. Such modernization programs are often more cost-effective than purchasing entirely new locomotives, making them an attractive option for railway companies facing budget constraints. The integration of advanced diagnostics, IoT, and AI into engine management systems also offers new revenue streams for engine manufacturers through data services and predictive maintenance contracts. These technological enhancements not only improve efficiency and reliability but also open doors for long-term service partnerships, securing future market presence.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development & Adoption of Hybrid and Dual-Fuel Engine Technologies | +0.9% | Global | Mid-Long Term |

| Expansion of Railway Networks in Emerging Economies | +0.8% | APAC, Latin America, Africa | Mid-Long Term |

| Increased Demand for Aftermarket Services & Modernization Programs | +0.7% | North America, Europe, Asia Pacific | Short-Mid Term |

| Integration of IoT, AI, & Advanced Diagnostics in Engines | +0.6% | Global | Mid-Long Term |

| Focus on Operational Efficiency & Reduced Maintenance Costs | +0.5% | Global | Short-Mid Term |

Diesel Locomotive Engine Market Challenges Impact Analysis

The diesel locomotive engine market faces significant challenges, primarily from the intensifying pressure to decarbonize the transportation sector. While diesel remains essential for heavy-haul and non-electrified routes, the long-term viability of internal combustion engines is under scrutiny due to climate change concerns and global net-zero targets. This creates uncertainty for manufacturers regarding long-term investment in diesel-specific R&D, as resources are increasingly diverted towards alternative propulsion technologies like hydrogen and battery-electric systems. Regulatory uncertainty, with varying emission standards across different regions and evolving timelines for their implementation, further complicates product development and market entry strategies for engine manufacturers.

Another substantial challenge is the high cost and complexity associated with meeting stringent emission regulations. Developing engines that comply with standards such as Tier 4 Final or Stage V often requires sophisticated exhaust after-treatment systems, advanced engine controls, and specialized components. These additions increase the manufacturing cost, complexity, and weight of the engines, potentially impacting their cost-effectiveness and ease of maintenance for operators. Furthermore, the supply chain for advanced engine components can be susceptible to disruptions, as demonstrated by recent global events, leading to production delays and increased costs. Addressing these intricate regulatory and manufacturing hurdles while remaining competitive requires continuous innovation and strategic adaptation from market players.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Long-Term Decarbonization Pressures & Uncertainty for Diesel | -0.6% | Global, particularly developed economies | Long Term |

| High Cost & Complexity of Meeting Stringent Emission Regulations | -0.5% | Global | Short-Mid Term |

| Supply Chain Disruptions & Volatility of Raw Material Prices | -0.4% | Global | Short-Mid Term |

| Technological Obsolescence & Competition from Disruptive Technologies | -0.3% | Global | Mid-Long Term |

| Shortage of Skilled Workforce for Advanced Engine Maintenance | -0.2% | Global | Mid-Long Term |

Diesel Locomotive Engine Market - Updated Report Scope

This comprehensive report provides an in-depth analysis of the global Diesel Locomotive Engine Market, offering critical insights into its current size, historical performance, and future growth projections. It meticulously examines the market landscape through various lenses, including key trends, technological advancements, regulatory impacts, and competitive dynamics. The report's scope covers a detailed segmentation analysis, identifying growth opportunities and challenges across different engine types, applications, and regional markets, ensuring a holistic understanding of the industry's trajectory. It further highlights the strategic initiatives of leading market players, offering a robust framework for stakeholders to make informed business decisions.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 15.5 Billion |

| Market Forecast in 2033 | USD 23.4 Billion |

| Growth Rate | 5.2% |

| Number of Pages | 250 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Wabtec Corporation, Progress Rail, Siemens AG, Caterpillar Inc., Cummins Inc., Electro-Motive Diesel (EMD), MTU Friedrichshafen GmbH (Rolls-Royce Power Systems), CRRC Corporation Limited, Alstom SA, Hitachi Rail STS, Hyundai Rotem Company, Kawasaki Heavy Industries Ltd., Toshiba Corporation, Skoda Transportation a.s., Bharat Heavy Electricals Limited (BHEL), Diesel-Electric Inc., General Electric, Voith GmbH & Co. KGaA, Liebherr-Components AG, Wärtsilä Corporation |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Diesel Locomotive Engine Market is meticulously segmented to provide a granular view of its diverse dynamics, allowing for a precise understanding of demand patterns and growth drivers across various categories. These segmentations are critical for stakeholders to identify niche opportunities, tailor product development, and refine market entry strategies. By categorizing engines based on horsepower, application, key components, and end-users, the report offers a multi-dimensional perspective on where growth is strongest and where technological advancements are most impactful. This detailed breakdown enables an in-depth assessment of market shifts, from the foundational engine block components to sophisticated exhaust after-treatment systems, and from heavy freight operations to specialized shunting activities.

- By Horsepower Range:

- Low Horsepower (Up to 2,000 HP)

- Medium Horsepower (2,001 - 4,000 HP)

- High Horsepower (Above 4,000 HP)

- By Application:

- Freight Locomotives

- Passenger Locomotives

- Shunting Locomotives

- By Component:

- Engine Block

- Crankshafts

- Cylinder Heads

- Fuel Injection Systems

- Turbochargers

- Exhaust After-treatment Systems (SCR, DPF)

- Pistons and Connecting Rods

- Valves and Valve Trains

- Engine Control Units (ECU)

- By End-User:

- Railway Operators (Class I, Regional, Short Line)

- Locomotive Manufacturers

- Leasing Companies

- Government & Defense

Regional Highlights

- North America: This region represents a mature market characterized by a significant installed base of diesel locomotives, particularly for heavy-haul freight operations. Growth in North America is primarily driven by fleet modernization programs, the replacement of aging engines with more fuel-efficient and lower-emission models, and the demand for digital integration in engine management. Regulatory pressures, especially the Tier 4 Final emission standards, have significantly shaped product development, leading to advancements in engine technology and exhaust after-treatment systems. The extensive rail network and robust freight volumes ensure a sustained, albeit moderate, demand for diesel locomotive engines, with a strong focus on enhancing operational efficiency and reducing total cost of ownership.

- Europe: Europe is at the forefront of railway electrification, posing a unique dynamic for the diesel locomotive engine market. While there's a strong push towards electric and alternative fuel solutions for new builds, diesel engines remain crucial for shunting, regional lines, and routes not yet electrified, as well as for certain heavy freight applications. The market here is largely driven by strict emission regulations (Stage V), necessitating advanced clean diesel technologies, and the need for flexible, high-performance engines for diverse operational scenarios. Opportunities exist in retrofitting existing fleets to comply with stricter environmental standards and in the development of hybrid-diesel solutions.

- Asia Pacific (APAC): APAC is projected to be the fastest-growing region in the diesel locomotive engine market, primarily due to massive investments in railway infrastructure development across countries like China, India, and Southeast Asian nations. The expansion of freight corridors, urban rail networks, and inter-city passenger lines fuels a strong demand for new locomotive engines. While some countries are exploring electrification, the sheer scale and rapid expansion of rail networks mean that diesel locomotives will continue to play a vital role for the foreseeable future, especially in non-electrified or challenging terrains. The market is also driven by the need for reliable, robust, and cost-effective engines to support burgeoning industrial and trade activities.

- Latin America: This region exhibits steady growth in the diesel locomotive engine market, largely influenced by the expansion of freight rail networks to support the burgeoning mining, agricultural, and industrial sectors. Countries like Brazil, Argentina, and Mexico are investing in upgrading and expanding their rail infrastructure to enhance logistics capabilities and reduce transportation costs. Demand is driven by the need for powerful engines capable of handling heavy loads over long distances and often challenging topographies. Modernization of existing fleets and the increasing focus on operational efficiency also contribute to market growth, with a growing interest in more fuel-efficient and reliable engine solutions.

- Middle East and Africa (MEA): The MEA region is emerging as a significant market for diesel locomotive engines, propelled by substantial investments in new railway projects aimed at improving connectivity, facilitating trade, and supporting economic diversification. Gulf Cooperation Council (GCC) countries are developing extensive rail networks, while various African nations are building new lines to connect industrial hubs, ports, and raw material extraction sites. Given the vast distances, extreme climates, and often limited electrification infrastructure, diesel locomotives are the preferred choice for their robustness and autonomy. This region offers considerable opportunities for new engine sales, driven by fundamental infrastructure development and the long-term vision for integrated transportation systems.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Diesel Locomotive Engine Market.- Wabtec Corporation

- Progress Rail

- Siemens AG

- Caterpillar Inc.

- Cummins Inc.

- Electro-Motive Diesel (EMD)

- MTU Friedrichshafen GmbH (Rolls-Royce Power Systems)

- CRRC Corporation Limited

- Alstom SA

- Hitachi Rail STS

- Hyundai Rotem Company

- Kawasaki Heavy Industries Ltd.

- Toshiba Corporation

- Skoda Transportation a.s.

- Bharat Heavy Electricals Limited (BHEL)

- Diesel-Electric Inc.

- General Electric

- Voith GmbH & Co. KGaA

- Liebherr-Components AG

- Wärtsilä Corporation

Frequently Asked Questions

What is the current outlook for the diesel locomotive engine market?

The diesel locomotive engine market is projected for steady growth, driven by sustained global demand for freight and passenger rail transport, particularly in emerging economies. While facing environmental pressures, the market thrives on technological advancements aimed at improving fuel efficiency, reducing emissions, and enabling smarter, more connected operations.

How are environmental regulations impacting the market?

Environmental regulations, such as Tier 4 Final and Stage V emission standards, are significantly impacting the market by compelling manufacturers to develop cleaner and more efficient diesel engines. This has led to the adoption of advanced exhaust after-treatment systems and is fostering innovation in hybrid and dual-fuel engine technologies.

What role does technology play in modern diesel locomotive engines?

Technology plays a crucial role, with advancements focused on digitalization, IoT, and AI integration. These technologies enable predictive maintenance, optimize fuel consumption through real-time data analysis, enhance operational efficiency, and contribute to improved safety and a lower total cost of ownership for railway operators.

Which regions are showing significant growth in this market?

The Asia Pacific region, particularly countries like China and India, is showing significant growth due to extensive investments in new railway infrastructure and rising freight volumes. Latin America and the Middle East & Africa are also emerging as key growth regions driven by rail network expansion projects.

What are the main challenges faced by diesel locomotive engine manufacturers?

Key challenges include navigating stringent and evolving environmental regulations, managing the high costs and complexity associated with meeting these standards, addressing the long-term decarbonization trend, and mitigating risks from supply chain disruptions and fluctuating raw material prices.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted