Non dairy Yoghurt Market

Non dairy Yoghurt Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_700298 | Last Updated : July 23, 2025 |

Format : ![]()

![]()

![]()

![]()

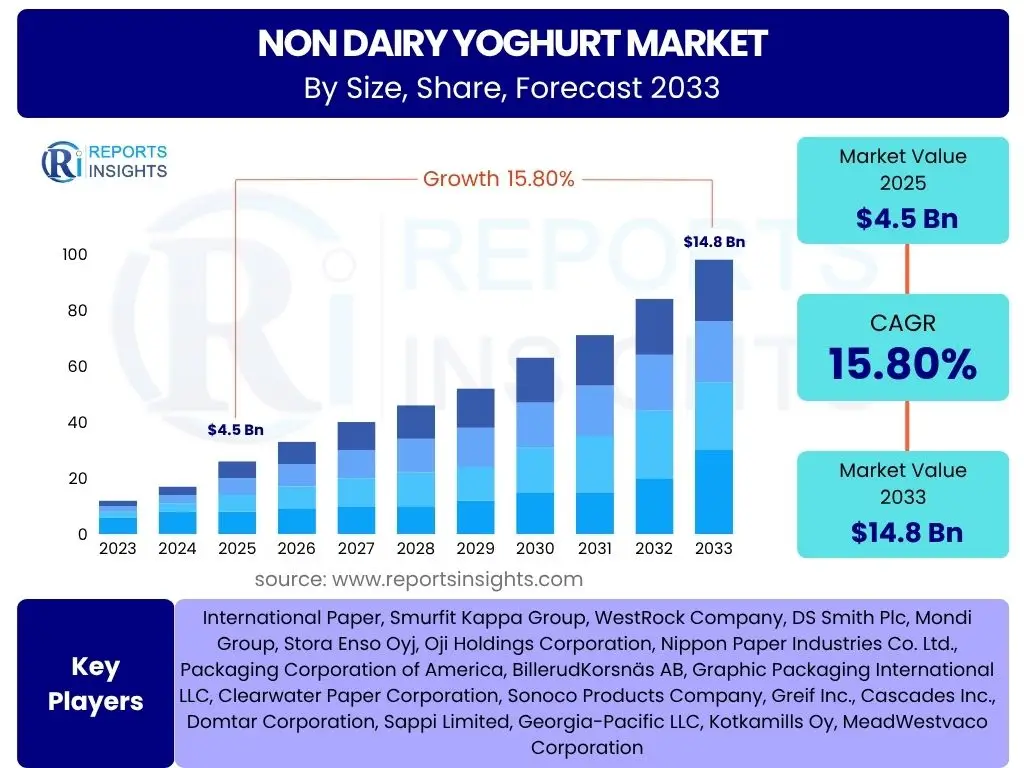

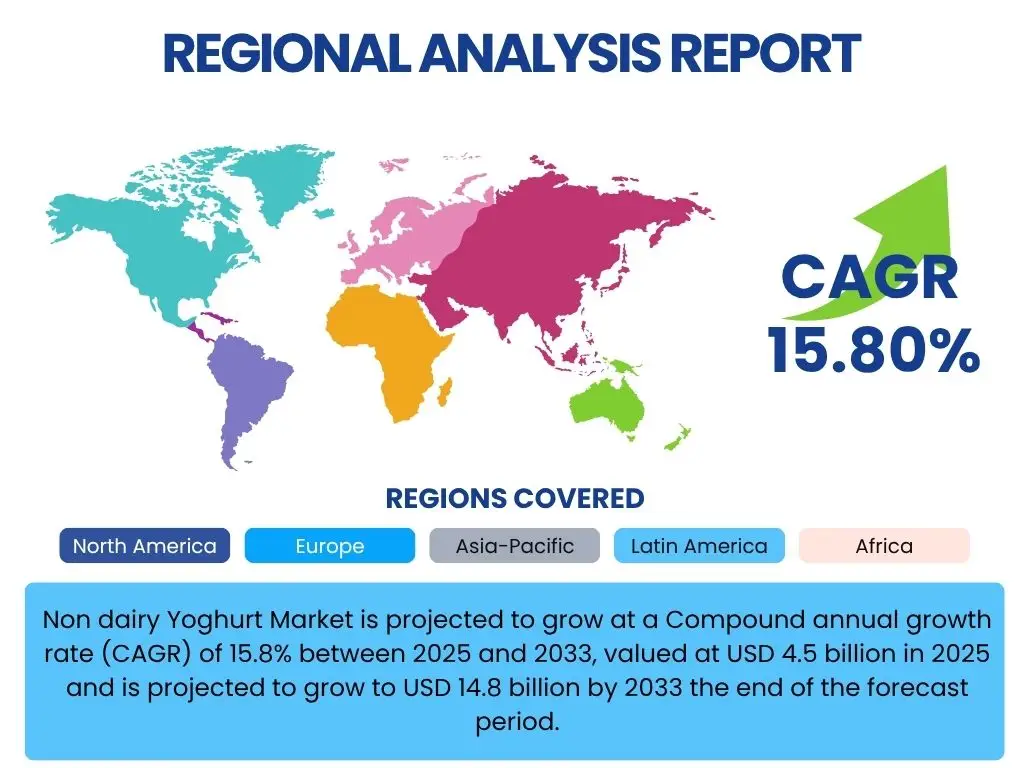

Non dairy Yoghurt Market is projected to grow at a Compound annual growth rate (CAGR) of 15.8% between 2025 and 2033, current valued at USD 4.5 billion in 2025 and is projected to grow to USD 14.8 billion by 2033 the end of the forecast period.

Key Non dairy Yoghurt Market Trends & Insights

The Non dairy Yoghurt Market is currently experiencing a dynamic phase driven by evolving consumer preferences and innovative product development. A significant shift towards plant-based diets, influenced by health, ethical, and environmental considerations, is reshaping the landscape. Manufacturers are actively responding to this demand by diversifying their product offerings, exploring novel ingredients, and enhancing sensory attributes to closely mimic traditional dairy options while offering distinct nutritional benefits. Furthermore, the market is seeing an emphasis on functional ingredients, addressing specific health concerns such as gut health and immune support, thereby expanding the appeal beyond core vegan consumers to a broader health-conscious demographic.- Increasing consumer adoption of plant-based diets and flexitarian lifestyles.

- Diverse ingredient innovation, including oat, almond, coconut, soy, and pea-based formulations.

- Growing demand for functional non-dairy yoghurts enriched with probiotics, prebiotics, and vitamins.

- Emphasis on sustainable and ethical sourcing of ingredients and eco-friendly packaging solutions.

- Expansion of flavor profiles and textures to enhance consumer experience and widen appeal.

- Rising prevalence of lactose intolerance and dairy allergies globally.

- Strategic partnerships and collaborations between established food companies and plant-based startups.

AI Impact Analysis on Non dairy Yoghurt

Artificial intelligence is poised to revolutionize various facets of the Non dairy Yoghurt Market, from ingredient sourcing and product formulation to supply chain management and consumer engagement. AI-driven predictive analytics can forecast consumer preferences with greater accuracy, enabling manufacturers to rapidly innovate and tailor products that resonate with emerging trends. In production, AI can optimize processes for efficiency, reduce waste, and ensure consistent quality, while also facilitating personalized nutrition recommendations based on individual dietary needs and health goals. This technological integration promises to enhance market responsiveness and drive sustainable growth.- AI-powered predictive analytics for consumer trend forecasting and demand planning.

- Optimization of supply chain and logistics for plant-based ingredients, reducing waste and costs.

- Automated quality control and sensory analysis in non-dairy yoghurt production.

- Personalized product recommendations and customized nutrition plans for consumers.

- Accelerated research and development for novel plant-based ingredients and fermentation techniques.

- Enhanced traceability and transparency throughout the non-dairy yoghurt production process.

- AI-driven marketing campaigns targeting specific consumer segments based on dietary habits.

Key Takeaways Non dairy Yoghurt Market Size & Forecast

- The market is projected to reach USD 14.8 billion by 2033, demonstrating robust growth from its USD 4.5 billion valuation in 2025.

- A significant compound annual growth rate (CAGR) of 15.8% is anticipated from 2025 to 2033, highlighting strong market momentum.

- Growth is predominantly fueled by increasing health consciousness, dietary shifts towards plant-based options, and rising incidence of lactose intolerance.

- North America and Europe currently represent the largest market shares, driven by early adoption and developed vegan food infrastructure.

- Asia Pacific is emerging as a high-growth region, propelled by changing dietary habits and rising disposable incomes.

- Product innovation, including diverse plant sources and functional benefits, is a key factor sustaining market expansion.

Non dairy Yoghurt Market Drivers Analysis

The growth of the Non dairy Yoghurt Market is primarily propelled by a confluence of evolving consumer preferences, health awareness, and ethical considerations. A significant driver is the increasing global adoption of vegan and flexitarian diets, which directly translates into higher demand for plant-based alternatives across all food categories, including yogurt. Furthermore, the rising awareness and diagnosis of lactose intolerance and dairy allergies have compelled consumers to seek out non-dairy options. Beyond dietary restrictions, a growing number of individuals are choosing non-dairy products due to perceived health benefits, such as lower cholesterol and saturated fat content, and environmental concerns regarding traditional dairy farming. Innovation in product formulation, leading to improved taste, texture, and nutritional profiles, also plays a critical role in expanding the market's appeal to a broader consumer base.| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing prevalence of lactose intolerance and dairy allergies, prompting consumers to seek alternative options that align with their dietary needs without compromising taste or texture. | +3.5% | Global, particularly in North America, Europe, and parts of Asia. | Short to Medium Term (2025-2029) |

| Increasing adoption of vegan, vegetarian, and flexitarian diets driven by ethical considerations, environmental concerns, and health benefits associated with plant-based living. | +4.0% | North America, Europe, increasingly in Asia Pacific. | Medium to Long Term (2026-2033) |

| Rising consumer health consciousness and demand for functional foods, leading to the popularity of non-dairy yoghurts enriched with probiotics, prebiotics, and essential vitamins for gut health and immunity. | +3.0% | Global, with strong traction in developed markets. | Short to Medium Term (2025-2030) |

| Significant product innovation and diversification by manufacturers, introducing a wider variety of plant-based sources (oat, almond, coconut, soy, pea), flavors, and textures, improving consumer acceptance. | +2.8% | Global, highly impactful in competitive markets. | Short to Medium Term (2025-2029) |

| Growing environmental concerns and consumer preference for sustainable food options, as non-dairy alternatives generally have a lower environmental footprint compared to traditional dairy products. | +2.5% | Developed markets, especially Europe and North America. | Medium to Long Term (2027-2033) |

Non dairy Yoghurt Market Restraints Analysis

Despite its robust growth, the Non dairy Yoghurt Market faces several restraints that could impede its full potential. A primary challenge is the higher production cost associated with some specialized plant-based ingredients and the processes required to achieve desired textures and flavors, which often translates to a higher retail price point compared to conventional dairy yogurts. This cost disparity can deter price-sensitive consumers. Furthermore, some non-dairy yoghurt varieties may struggle with achieving a taste and texture profile that precisely mimics traditional dairy, leading to consumer skepticism or dissatisfaction. Limited shelf life for certain formulations, particularly those with fewer preservatives, and potential allergic reactions to specific plant bases (e.g., nuts, soy) also pose challenges for market penetration and widespread acceptance.| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Higher retail prices of non-dairy yoghurts compared to traditional dairy variants, stemming from specialized ingredients, complex processing, and smaller production scales, impacting affordability for budget-conscious consumers. | -2.0% | Global, particularly in emerging markets and price-sensitive consumer segments. | Medium Term (2025-2031) |

| Taste and texture challenges, as some non-dairy yoghurt formulations may not fully replicate the sensory experience of dairy yogurt, potentially leading to consumer dissatisfaction or a preference for traditional options. | -1.5% | Global, especially in regions with strong dairy traditions. | Short to Medium Term (2025-2028) |

| Allergen concerns related to common plant bases like nuts (almond, cashew, coconut) and soy, limiting options for consumers with specific allergies and necessitating careful labeling and alternative base development. | -1.0% | Global, particularly in markets with high allergy prevalence. | Ongoing (2025-2033) |

| Perceived nutritional deficiencies or concerns about additives in some highly processed non-dairy yoghurts, despite many being fortified, leading to consumer skepticism about their overall health benefits. | -0.8% | Developed markets with high nutritional awareness. | Medium Term (2026-2032) |

Non dairy Yoghurt Market Opportunities Analysis

The Non dairy Yoghurt Market is rich with opportunities for innovation and expansion, driven by evolving consumer demands and technological advancements. A significant avenue lies in the continuous exploration and integration of novel plant-based ingredients beyond traditional almond and soy, such as faba bean, chickpea, or even potato, to offer diverse nutritional profiles and cater to different allergen sensitivities. Expanding into functional food categories, with fortification aimed at specific health benefits like immune support, cognitive health, or sports nutrition, presents a lucrative niche. Furthermore, geographical expansion into emerging markets, where plant-based diets are gaining traction, along with strategic collaborations and sustainable packaging innovations, will unlock new growth trajectories for the market.| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development of novel plant-based ingredients beyond traditional almond and soy, such as oat, pea, faba bean, chickpea, and potato, to diversify product offerings and cater to a wider range of tastes and allergies. | +2.2% | Global, highly relevant in competitive and innovative markets. | Short to Medium Term (2025-2030) |

| Expansion into functional non-dairy yoghurts tailored for specific health needs, including enhanced protein content for fitness enthusiasts, added adaptogens for stress relief, or fortified vitamins for specific dietary gaps. | +2.0% | North America, Europe, increasingly Asia Pacific. | Medium Term (2026-2032) |

| Penetration into untapped emerging markets, particularly in Asia Pacific, Latin America, and Africa, where awareness of plant-based products is rising and disposable incomes are increasing, presenting new consumer bases. | +1.8% | Asia Pacific, Latin America, Middle East & Africa. | Long Term (2028-2033) |

| Innovations in sustainable packaging solutions, including recyclable, compostable, or refillable options, aligning with consumer demand for environmentally friendly products and reducing ecological footprint. | +1.5% | Global, especially in regions with strong environmental regulations and consumer awareness. | Medium to Long Term (2027-2033) |

| Strategic collaborations and partnerships across the value chain, from ingredient suppliers to food service providers and retail channels, to enhance market reach, share expertise, and drive innovation collaboratively. | +1.0% | Global, particularly beneficial for market penetration and efficiency. | Short to Medium Term (2025-2029) |

Non dairy Yoghurt Market Challenges Impact Analysis

The Non dairy Yoghurt Market encounters several significant challenges that could hinder its growth trajectory and profitability. One major hurdle is the fluctuating availability and pricing of key plant-based raw materials, which can impact production costs and supply chain stability. Intense competition from both established dairy companies diversifying into plant-based lines and numerous new entrants in the non-dairy segment necessitates continuous innovation and differentiation. Additionally, achieving perfect taste and texture parity with traditional dairy yogurt remains a persistent challenge, influencing consumer acceptance, particularly among those transitioning from dairy. Stringent food safety and labeling regulations across different regions also add complexity and cost to product development and market entry.| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Volatility in the prices and supply of key plant-based raw materials, such as almonds, oats, and coconuts, due to climatic conditions, geopolitical factors, or agricultural yield fluctuations, impacting production costs and stability. | -1.8% | Global, with specific regional dependencies on raw material sources. | Short to Medium Term (2025-2029) |

| Intense competition within the plant-based food sector, with a proliferation of brands and products vying for consumer attention, leading to pricing pressures and saturation in mature markets. | -1.5% | North America, Europe, and other developed markets. | Ongoing (2025-2033) |

| Consumer skepticism or reluctance towards processed plant-based foods, with some consumers preferring whole, unprocessed ingredients, requiring transparent labeling and clear communication of nutritional benefits. | -1.2% | Developed markets with high consumer awareness about food processing. | Medium Term (2026-2031) |

| Maintaining consistency in taste, texture, and stability across different production batches and plant-based formulations, which can be technically challenging due to varying natural properties of raw ingredients. | -1.0% | Global, especially for manufacturers with diverse product lines. | Ongoing (2025-2033) |

| Complex regulatory landscape for novel food ingredients and labeling requirements for plant-based products, which can vary significantly by country, posing hurdles for international market expansion and compliance. | -0.7% | Global, particularly challenging for cross-border trade. | Ongoing (2025-2033) |

Non dairy Yoghurt Market - Updated Report Scope

This updated market research report on the Non dairy Yoghurt Market provides a comprehensive analysis of the industry's historical performance, current trends, and future projections. It delves into the market drivers, restraints, opportunities, and challenges shaping the landscape, offering critical insights for stakeholders. The report segments the market extensively by various parameters, including source, flavor, distribution channel, and end-user, across key global regions, providing a granular view of market dynamics and competitive intelligence.| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 4.5 billion |

| Market Forecast in 2033 | USD 14.8 billion |

| Growth Rate | 15.8% CAGR from 2025 to 2033 |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Miyoko's Kitchen, Silk, So Delicious Dairy Free, Kite Hill, Forager Project, Daiya Foods, Nancy's Probiotic Foods, Good Karma Foods, Chobani, Fage, Wallaby Organic, The WhiteWave Foods Company, Lactalis, Danone, General Mills, Hain Celestial Group, Califia Farms, Ripple Foods, Oatly, Blue Diamond Growers |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Non dairy Yoghurt Market is comprehensively segmented to provide a detailed understanding of its various facets, enabling stakeholders to identify key growth areas and targeted strategies. These segmentations delve into the diverse plant-based sources used, the array of flavors appealing to consumer palates, the channels through which products reach consumers, and the distinct end-user categories driving demand. Each segment is analyzed to highlight its unique market dynamics, growth potential, and contribution to the overall market landscape.- By Source:

The market is broadly categorized by the primary plant ingredient used in non-dairy yoghurt production, reflecting consumer preferences for specific taste profiles, nutritional benefits, and allergen considerations. This segmentation showcases the innovation within the industry to cater to diverse dietary needs and preferences, leading to a rich variety of product offerings.

- Almond: Popular for its creamy texture and mild taste, often fortified with calcium and vitamins.

- Soy: A traditional and widely available base, known for its protein content and versatility in fermentation.

- Coconut: Offers a rich, decadent texture and distinct tropical flavor, appealing to those seeking a indulgent option.

- Oat: Gaining significant traction due to its naturally creamy texture, neutral flavor, and allergen-friendly profile.

- Cashew: Provides a luxurious, smooth consistency and a rich taste, often used in premium non-dairy yoghurts.

- Pea: An emerging source valued for its high protein content, making it a favorite among health-conscious and fitness-oriented consumers.

- Other Plant-based Sources: Includes less common but growing bases like rice, hemp, flax, and faba bean, offering niche appeal and diversification for consumers with unique dietary requirements or preferences.

- By Flavor:

Flavor is a critical determinant of consumer acceptance and market penetration, with offerings ranging from foundational unflavored options to a wide array of fruit and dessert-inspired varieties. This segmentation highlights the industry's efforts to replicate beloved dairy yogurt flavors while also introducing innovative combinations unique to the plant-based category, catering to evolving taste preferences.

- Plain/Unsweetened: Appeals to consumers who prefer to add their own sweeteners or use yoghurt in savory applications, valued for its versatility and natural taste.

- Vanilla: A classic and universally appealing flavor, offering a comforting and familiar taste profile that works well on its own or as a base for smoothies.

- Strawberry: One of the most popular fruit flavors, offering a sweet and tangy profile widely embraced across all age groups.

- Blueberry: Provides a sweet and slightly tart profile, often associated with health benefits and popular in breakfast and snack categories.

- Mixed Berry: Combines various berries (e.g., raspberry, blackberry, strawberry) for a complex, rich fruit flavor, offering a blend of tartness and sweetness.

- Peach: Offers a sweet and aromatic flavor, reminiscent of fresh fruit, and is a perennial favorite in the yogurt market.

- Other Flavors: Encompasses a broad spectrum of innovative and seasonal offerings such as mango, cherry, lemon, chocolate, coffee, and unique spice blends, catering to adventurous palates and expanding market diversity.

- By Distribution Channel:

The availability of non-dairy yoghurts across diverse retail and commercial channels is crucial for market accessibility and penetration. This segmentation illustrates how products reach consumers, from traditional brick-and-mortar stores to the rapidly expanding e-commerce platforms, reflecting changing shopping habits and retail strategies employed by manufacturers.

- Supermarkets and Hypermarkets: Remain the dominant channel, offering wide product selections, competitive pricing, and convenience for bulk purchases. These large format stores serve as primary points of sale due to their extensive reach.

- Convenience Stores: Increasingly stocking non-dairy yoghurt, catering to impulse purchases and on-the-go consumption, driven by their widespread presence and extended operating hours.

- Online Retail: Experiencing exponential growth, offering unparalleled convenience, a wider product assortment often including niche brands, and direct-to-consumer delivery services, appealing to tech-savvy consumers.

- Specialty Stores: Includes health food stores and organic markets, which often stock premium, artisanal, or niche non-dairy yoghurt brands, appealing to dedicated health-conscious consumers.

- Other Retail Formats: Encompasses diverse outlets such as club stores, discount stores, and vending machines, expanding the market's reach and catering to varied consumer segments.

- By End-User:

Understanding the varied applications of non-dairy yoghurt across different consumer segments is vital for targeted product development and marketing. This segmentation distinguishes between household consumption, professional food service use, and industrial applications, highlighting the versatility of non-dairy yoghurt beyond direct consumption.

- Household/Residential: Represents the largest end-user segment, comprising individuals and families purchasing non-dairy yoghurt for direct consumption at home, as breakfast, snacks, or meal ingredients.

- Food Service: Includes restaurants, cafes, hotels, catering services, and institutional cafeterias that incorporate non-dairy yoghurt into their menus for various dishes, smoothies, desserts, or as a standalone option for diners seeking plant-based choices.

- Food & Beverage Industry: Involves the use of non-dairy yoghurt as an ingredient in the production of other food and beverage items, such as baked goods, dressings, dips, frozen desserts, and snack bars, demonstrating its versatility as a functional component.

Regional Highlights

The Non dairy Yoghurt Market exhibits distinct regional dynamics, reflecting varying consumer preferences, dietary trends, and regulatory landscapes. Each region contributes uniquely to the market's overall growth, with specific countries leading innovation or demand.- North America: This region stands as a dominant force in the Non dairy Yoghurt Market, driven by a high incidence of lactose intolerance, strong advocacy for plant-based diets, and a robust health and wellness trend. The United States, in particular, showcases significant market maturity with diverse product offerings and high consumer adoption rates. Extensive research and development, coupled with aggressive marketing by both established food giants and agile startups, further propels market expansion here. Canada also contributes significantly, mirroring similar consumer inclinations towards healthier and ethical food choices.

- Europe: Following closely, Europe represents another substantial market for non-dairy yoghurt, fueled by growing vegan and flexitarian populations, particularly in countries like the UK, Germany, and Sweden. Stringent environmental regulations and a strong consumer emphasis on sustainability further encourage the shift towards plant-based alternatives. Product innovation, especially in oat-based and coconut-based varieties, along with the increasing availability in mainstream retail channels, bolsters the market's upward trajectory across the continent.

- Asia Pacific (APAC): The APAC region is poised for remarkable growth, emerging as the fastest-growing market segment. This surge is attributed to rapidly rising disposable incomes, urbanization, and a gradual shift in traditional dietary patterns. Countries such as China, India, Japan, and Australia are witnessing increasing awareness of plant-based benefits and a growing demand for diverse food options. Local manufacturers are stepping up to cater to region-specific tastes, while global players are expanding their presence, making APAC a critical future growth hub.

- Latin America: This region is experiencing nascent but steady growth in the non-dairy yoghurt sector. Increasing health awareness, rising middle-class populations, and the influence of global dietary trends are slowly fostering a demand for plant-based alternatives. Brazil and Mexico are leading this charge, with evolving retail infrastructure and a gradual diversification of available products. The market here benefits from a younger demographic more open to experimenting with new food categories.

- Middle East and Africa (MEA): While a smaller market share currently, MEA is showing promising potential for future growth. Factors such as increasing urbanization, exposure to Western dietary trends, and a growing health-conscious consumer base are contributing to the gradual adoption of non-dairy options. Challenges like traditional dietary preferences and limited product availability persist, but increasing investment in plant-based food infrastructure and rising consumer awareness are expected to drive market expansion over the forecast period.

Top Key Players:

The market research report covers the analysis of key stake holders of the Non dairy Yoghurt Market. Some of the leading players profiled in the report include -:- Miyoko's Kitchen

- Silk

- So Delicious Dairy Free

- Kite Hill

- Forager Project

- Daiya Foods

- Nancy's Probiotic Foods

- Good Karma Foods

- Chobani

- Fage

- Wallaby Organic

- The WhiteWave Foods Company

- Lactalis

- Danone

- General Mills

- Hain Celestial Group

- Califia Farms

- Ripple Foods

- Oatly

- Blue Diamond Growers

Frequently Asked Questions:

What is non-dairy yoghurt?

Non-dairy yoghurt is a fermented food product designed to replicate traditional dairy yoghurt, but it is made from plant-based milk alternatives instead of animal milk. Common bases include almond milk, soy milk, coconut milk, oat milk, and pea milk. These plant-based milks are fermented with live active cultures, similar to dairy yoghurt, to achieve a characteristic tangy flavor and creamy texture. It is a popular choice for individuals with lactose intolerance, dairy allergies, vegans, or those seeking plant-based and environmentally conscious dietary options.What are the primary drivers of growth in the Non dairy Yoghurt Market?

The primary drivers of growth in the Non dairy Yoghurt Market include the escalating prevalence of lactose intolerance and dairy allergies globally, which compels consumers to seek alternative options. Furthermore, the rising adoption of plant-based diets, such as veganism and flexitarianism, driven by ethical, environmental, and health considerations, significantly boosts demand. Increased consumer health consciousness, leading to a demand for functional foods rich in probiotics and vitamins, along with continuous product innovation in terms of taste, texture, and variety of plant-based sources, also plays a crucial role in market expansion.Which regions are leading the Non dairy Yoghurt Market?

North America and Europe currently hold the largest market shares in the Non dairy Yoghurt Market. These regions are characterized by a strong consumer inclination towards healthy and sustainable food choices, well-established vegan communities, and widespread product availability in mainstream retail channels. The market in these regions benefits from early adoption of plant-based trends and significant investment in research and development for new non-dairy formulations. Asia Pacific is rapidly emerging as a high-growth region, driven by changing dietary habits and increasing disposable incomes.What are the key challenges facing the Non dairy Yoghurt Market?

The Non dairy Yoghurt Market faces several key challenges, including the higher retail prices of non-dairy variants compared to traditional dairy products, which can deter price-sensitive consumers. Maintaining taste and texture consistency across various plant-based formulations, and achieving a sensory profile comparable to dairy yogurt, remains a technical challenge. Additionally, the volatility in the prices and supply of plant-based raw materials, intense competition from new entrants and diversified dairy companies, and complex regulatory landscapes for labeling and novel ingredients pose significant hurdles to market expansion and profitability.What are the future opportunities in the Non dairy Yoghurt Market?

Significant opportunities in the Non dairy Yoghurt Market lie in the continuous innovation of novel plant-based ingredients beyond common sources like almond and soy, offering diverse nutritional profiles and catering to new taste preferences and allergen needs. There is also substantial potential in expanding into functional non-dairy yoghurts, fortified with specific health-promoting ingredients like adaptogens or specialized proteins. Furthermore, geographic expansion into untapped emerging markets, particularly in Asia Pacific and Latin America, along with advancements in sustainable packaging solutions and strategic collaborations across the value chain, present promising avenues for future growth.| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted