Non Alcoholic Wine and Beer Market

Non Alcoholic Wine and Beer Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_705950 | Last Updated : August 17, 2025 |

Format : ![]()

![]()

![]()

![]()

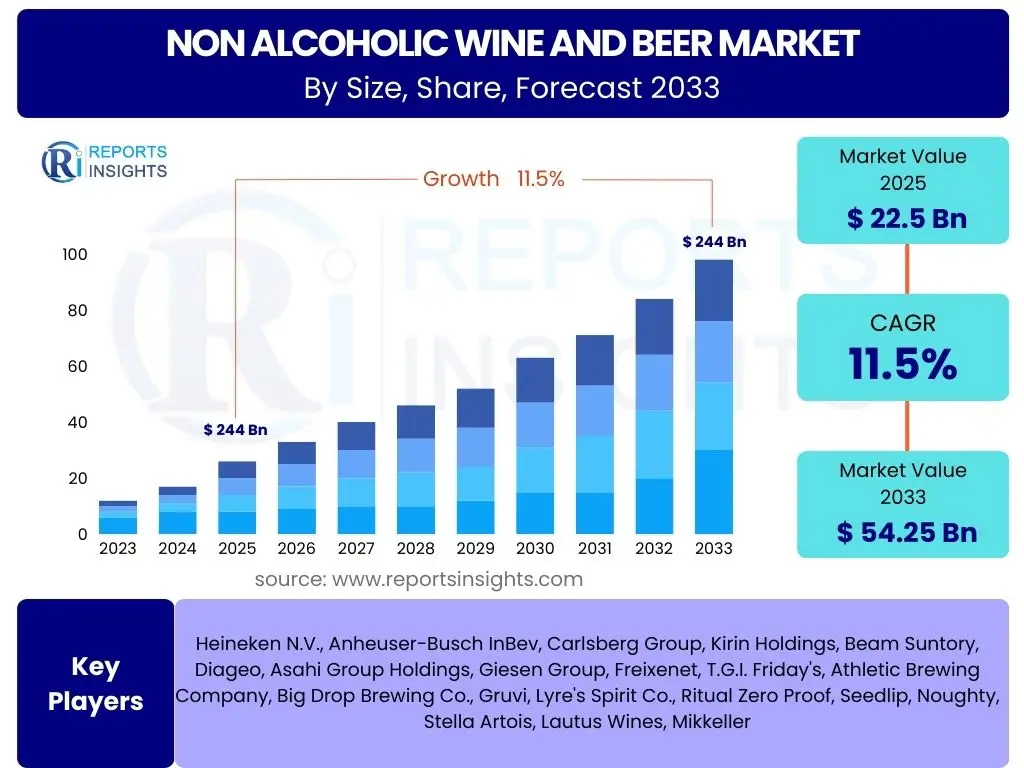

Non Alcoholic Wine and Beer Market Size

According to Reports Insights Consulting Pvt Ltd, The Non Alcoholic Wine and Beer Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 11.5% between 2025 and 2033. The market is estimated at USD 22.5 Billion in 2025 and is projected to reach USD 54.25 Billion by the end of the forecast period in 2033.

Key Non Alcoholic Wine and Beer Market Trends & Insights

The Non Alcoholic Wine and Beer market is experiencing dynamic shifts, driven by evolving consumer lifestyles and heightened health consciousness. Common user inquiries frequently revolve around what specific factors are fueling this growth and how product innovation is keeping pace with demand. Key trends indicate a significant pivot towards mindful consumption, where consumers seek alternatives that align with healthier habits without compromising on social experiences or taste.

Furthermore, consumers are increasingly interested in understanding the breadth of product offerings beyond traditional non-alcoholic options. There is a growing demand for premium non-alcoholic beverages that replicate the complex flavor profiles and sophisticated experiences associated with their alcoholic counterparts. This trend towards premiumization and diversification of choices reflects a mature market responding to nuanced consumer preferences for quality, variety, and an elevated drinking experience.

- Rising health and wellness consciousness among global consumers.

- Significant expansion of product variety and flavor profiles.

- Premiumization of non-alcoholic offerings, appealing to discerning consumers.

- Increased adoption of sustainable and ethical production practices.

- Growing presence across diverse distribution channels, including e-commerce.

AI Impact Analysis on Non Alcoholic Wine and Beer

The integration of Artificial Intelligence (AI) is set to profoundly impact the Non Alcoholic Wine and Beer market, addressing several common user concerns related to production efficiency, personalized consumption, and supply chain optimization. AI algorithms can analyze vast datasets to predict consumer preferences, identify emerging flavor trends, and optimize product formulations to mimic the sensory experience of alcoholic beverages more accurately. This precision in product development can lead to faster innovation cycles and a greater likelihood of market acceptance for new non-alcoholic offerings, directly responding to consumer desires for variety and quality.

Beyond product innovation, AI's influence extends to enhancing operational efficiencies and customer engagement. Through predictive analytics, AI can optimize supply chain logistics, reduce waste, and manage inventory levels more effectively, ensuring products are available where and when consumers demand them. Moreover, AI-powered marketing platforms can deliver highly personalized recommendations and advertisements, fostering stronger brand loyalty and driving sales by understanding individual consumer behavior. This targeted approach is crucial for capturing niche markets and expanding the overall reach of non-alcoholic brands, making the market more responsive and consumer-centric.

- Demand forecasting and inventory optimization for supply chain efficiency.

- Personalized marketing and product recommendations through data analytics.

- Accelerated new product development via AI-driven flavor profiling and formulation.

- Automated quality control and consistency in brewing/winemaking processes.

- Enhanced consumer engagement and feedback analysis for market responsiveness.

Key Takeaways Non Alcoholic Wine and Beer Market Size & Forecast

The Non Alcoholic Wine and Beer market demonstrates robust growth, largely fueled by a global shift towards healthier lifestyles and an increased awareness of wellness. Common user questions often focus on the longevity of this trend and the primary factors sustaining such a positive market outlook. The forecast suggests that this is not a transient trend but a fundamental change in consumer behavior, indicating significant long-term growth potential. The market’s resilience is underpinned by continuous product innovation and diversification, ensuring that consumer preferences for taste and experience are consistently met, thereby widening its appeal across various demographics.

Furthermore, the market’s projected expansion to over USD 54 billion by 2033 highlights the burgeoning opportunities for established players and new entrants alike. This significant growth trajectory is a key takeaway for investors and stakeholders, underscoring the increasing mainstream acceptance and desirability of non-alcoholic alternatives. The commitment of beverage manufacturers to invest in advanced de-alcoholization technologies and sophisticated marketing strategies further solidifies the positive forecast, positioning the non-alcoholic segment as a critical growth engine within the broader beverage industry.

- The market is poised for significant and sustained growth through 2033.

- Consumer health and wellness trends are the primary growth catalysts.

- Innovation in taste and product variety is crucial for market expansion.

- Strong potential for new market entrants and diversification for existing players.

- The shift towards mindful drinking is a global and enduring phenomenon.

Non Alcoholic Wine and Beer Market Drivers Analysis

The primary driver propelling the Non Alcoholic Wine and Beer market is the escalating global health and wellness trend. Consumers are increasingly prioritizing their well-being, seeking beverages that offer enjoyable experiences without the negative effects associated with alcohol consumption. This shift is evident in the growing demand for products with lower sugar content, natural ingredients, and functional benefits, pushing manufacturers to innovate and expand their non-alcoholic portfolios. The desire for a balanced lifestyle, coupled with rising awareness about alcohol-related health risks, significantly contributes to the market's robust expansion, particularly in developed regions where wellness trends are deeply embedded in consumer culture.

Another significant driver is the evolving social dynamics and changing consumer preferences. There is a growing acceptance and even preference for non-alcoholic options in social settings, removing the stigma previously associated with abstaining from alcohol. This cultural shift is supported by younger generations who are more health-conscious and less inclined towards heavy drinking, as well as by individuals seeking moderation or avoiding alcohol for personal, religious, or dietary reasons. The increased mainstream availability and improved quality of non-alcoholic wines and beers have made them viable and appealing alternatives, integrating seamlessly into various social occasions and lifestyles.

Lastly, technological advancements in de-alcoholization processes and flavor development play a crucial role in driving market growth. Innovations such as vacuum distillation, reverse osmosis, and spinning cone columns enable manufacturers to produce non-alcoholic beverages that retain the complex aromas, flavors, and mouthfeel of their alcoholic counterparts. This technological progress addresses historical barriers related to taste perception, enhancing consumer acceptance and satisfaction. Coupled with aggressive marketing campaigns and broader distribution, these improvements make non-alcoholic options more accessible and appealing to a wider consumer base globally.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Rising Health & Wellness Trends | +3.5% | North America, Europe, Oceania | Short-term to Long-term |

| Evolving Consumer Preferences & Social Acceptance | +2.8% | Global, particularly Developed Markets | Mid-term to Long-term |

| Technological Advancements in De-alcoholization | +2.2% | Global | Short-term to Mid-term |

| Increased Availability & Distribution Channels | +1.5% | Global, particularly Emerging Markets | Mid-term |

Non Alcoholic Wine and Beer Market Restraints Analysis

One of the primary restraints in the Non Alcoholic Wine and Beer market is the lingering perception of inferior taste and quality compared to their alcoholic counterparts. Despite significant advancements in de-alcoholization technologies, some consumers remain skeptical about the ability of non-alcoholic beverages to replicate the complex flavor profiles and mouthfeel of traditional wines and beers. This taste barrier can deter potential consumers who prioritize sensory experience, leading to slower adoption rates in certain segments of the market. Overcoming this ingrained perception requires continuous innovation, extensive consumer education, and effective marketing strategies to highlight the improved quality of modern non-alcoholic offerings.

Another significant restraint is the relatively higher price point of some premium non-alcoholic products, which can be a barrier for price-sensitive consumers. The specialized processes involved in removing alcohol while preserving flavor, coupled with smaller production volumes for some niche brands, can contribute to increased manufacturing costs. These costs are often passed on to the consumer, making non-alcoholic options less competitive in price against mass-produced alcoholic beverages or even other non-alcoholic soft drinks. For widespread market penetration, especially in emerging economies, achieving a more competitive pricing structure without compromising quality remains a key challenge for manufacturers.

Furthermore, limited consumer awareness and inconsistent distribution channels in certain regions pose a restraint to market expansion. While non-alcoholic beverages are gaining traction in developed markets, their presence in less mature markets or traditional retail environments can be sporadic. Consumers may not be fully aware of the variety and availability of non-alcoholic options, or they might struggle to find them in local stores or dining establishments. This lack of broad visibility and accessibility can hinder impulse purchases and limit the growth potential, underscoring the need for more pervasive marketing efforts and strategic partnerships to ensure wider market penetration and consumer education.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Perception of Inferior Taste/Quality | -1.2% | Global, especially Traditional Alcohol Markets | Ongoing |

| Relatively Higher Price Point | -0.8% | Emerging Markets, Price-Sensitive Demographics | Mid-term |

| Limited Consumer Awareness & Distribution Gaps | -0.5% | Certain Developing Regions, Rural Areas | Short-term to Mid-term |

Non Alcoholic Wine and Beer Market Opportunities Analysis

The premiumization trend within the non-alcoholic sector presents a significant opportunity for market growth. As consumers increasingly seek high-quality, sophisticated alternatives to alcoholic beverages, there is a growing demand for non-alcoholic wines and beers that offer artisanal craftsmanship, complex flavor profiles, and elevated branding. This allows manufacturers to command higher price points and cater to a discerning segment of the market willing to invest in a superior experience. Developing innovative products that mimic craft beers or fine wines, offering unique ingredient combinations, and emphasizing origin stories can capture this lucrative market segment, fostering brand loyalty and driving revenue growth beyond basic non-alcoholic offerings.

Another substantial opportunity lies in the untapped potential of emerging markets, particularly in Asia Pacific and parts of Latin America and Africa. While developed regions currently dominate the non-alcoholic beverage market, rising disposable incomes, urbanization, and increasing health consciousness in these developing economies are creating fertile ground for expansion. Cultural factors, such as religious observances or social norms that limit alcohol consumption, further enhance the appeal of non-alcoholic options in these regions. Strategic market entry, localized product development, and tailored distribution networks can unlock significant growth avenues, leveraging these demographic and cultural shifts to introduce and popularize non-alcoholic wines and beers.

The expansion into new consumption occasions and functional benefits also offers considerable opportunities. Beyond simply being alcohol-free, non-alcoholic beverages can be positioned to offer additional health benefits, such as isotonic properties for hydration, added vitamins, or natural adaptogens for relaxation. This broader appeal allows products to move beyond traditional drinking occasions, becoming suitable for post-workout recovery, daily wellness routines, or as sophisticated alternatives in professional settings. Innovating with functional ingredients and marketing these diversified benefits can create new demand streams and attract a wider array of consumers, differentiating products in a competitive market.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Premiumization and Craft Segment Expansion | +2.5% | North America, Europe, Australia | Short-term to Long-term |

| Penetration into Emerging Markets | +2.0% | Asia Pacific, Latin America, Middle East & Africa | Mid-term to Long-term |

| Development of Functional and Wellness-oriented Products | +1.8% | Global | Short-term to Mid-term |

Non Alcoholic Wine and Beer Market Challenges Impact Analysis

One of the persistent challenges for the Non Alcoholic Wine and Beer market is the technical difficulty in consistently replicating the authentic taste and mouthfeel of traditional alcoholic beverages. Removing alcohol without stripping away the nuanced flavors, aromas, and sensory characteristics that consumers expect from wine and beer requires sophisticated and often costly processes. Achieving this balance is crucial, as any significant deviation in taste can lead to consumer dissatisfaction and reluctance to repurchase. This challenge drives ongoing investment in research and development to refine de-alcoholization technologies and ingredient sourcing, impacting production costs and time-to-market for new innovations.

Another significant challenge involves navigating the complex and often fragmented regulatory landscape concerning labeling and marketing of non-alcoholic products. Different countries and regions have varying definitions for "non-alcoholic," "alcohol-free," or "de-alcoholized," and regulations regarding ingredient lists, health claims, and marketing restrictions can differ widely. This complexity necessitates careful compliance and can increase operational burdens for companies operating internationally, potentially delaying product launches or requiring significant adjustments for different markets. Standardizing labeling guidelines would greatly benefit global expansion, but until then, regulatory hurdles remain a considerable barrier.

The challenge of ensuring efficient and cost-effective supply chain management also impacts the market. As the demand for non-alcoholic beverages grows, maintaining product freshness and quality across extended supply chains becomes critical, especially for products that may have shorter shelf lives once opened or require specific storage conditions. Furthermore, sourcing specialized ingredients or adapting existing production lines for non-alcoholic variants can introduce complexities and increase operational costs. Efficiently scaling production and distribution while maintaining product integrity and profitability is a continuous challenge for manufacturers in this expanding market.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Taste Replication and Quality Consistency | -0.9% | Global | Ongoing |

| Regulatory Complexity and Labeling Standards | -0.7% | Global, particularly Cross-border Trade | Long-term |

| Supply Chain Management and Logistics | -0.4% | Global | Short-term to Mid-term |

Non Alcoholic Wine and Beer Market - Updated Report Scope

This market insights report provides a comprehensive analysis of the Non Alcoholic Wine and Beer market, covering historical data, current market dynamics, and future projections. It delves into the driving forces, restraining factors, emerging opportunities, and critical challenges shaping the industry. The scope encompasses detailed segmentation analysis, regional deep-dives, and profiles of key market participants, offering a holistic view for strategic decision-making.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 22.5 Billion |

| Market Forecast in 2033 | USD 54.25 Billion |

| Growth Rate | 11.5% |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Heineken N.V., Anheuser-Busch InBev, Carlsberg Group, Kirin Holdings, Beam Suntory, Diageo, Asahi Group Holdings, Giesen Group, Freixenet, T.G.I. Friday's, Athletic Brewing Company, Big Drop Brewing Co., Gruvi, Lyre's Spirit Co., Ritual Zero Proof, Seedlip, Noughty, Stella Artois, Lautus Wines, Mikkeller |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Non Alcoholic Wine and Beer market is comprehensively segmented to provide granular insights into its diverse components, facilitating targeted strategies for market participants. This detailed breakdown allows for an in-depth understanding of consumer preferences, distribution efficacy, and product development priorities across various categories. Analyzing these segments helps stakeholders identify high-growth areas and tailor their offerings to specific consumer needs and market demands, ensuring optimal resource allocation and competitive advantage within the evolving beverage landscape.

- By Product Type: Non Alcoholic Wine, Non Alcoholic Beer

- By Distribution Channel: Off-Trade (Supermarkets, Hypermarkets, Convenience Stores, Liquor Stores, Online Retail), On-Trade (Restaurants, Bars, Hotels, Cafes)

- By Alcohol Content: 0.0% ABV, Less than 0.5% ABV

- By Packaging Type: Bottles, Cans, Other (Kegs, Pouches)

- By Flavor Profile: Fruity, Hoppy, Malty, Crisp, Dry, Sweet

Regional Highlights

North America stands as a significant market for Non Alcoholic Wine and Beer, driven by a strong consumer focus on health and wellness, coupled with evolving social attitudes towards alcohol consumption. The region, particularly the United States and Canada, has witnessed a surge in demand for premium non-alcoholic alternatives, with a growing number of craft non-alcoholic breweries and distilleries emerging. Marketing efforts emphasize taste, variety, and the benefits of a balanced lifestyle, resonating well with a diverse consumer base. Retail availability has expanded significantly, including dedicated sections in supermarkets and online platforms, making these products more accessible to a broad demographic.

Europe represents a mature yet dynamic market, with countries like Germany, the UK, and Spain leading the adoption of non-alcoholic beers and wines. This region benefits from established brewing and winemaking traditions, allowing producers to leverage existing expertise in developing high-quality non-alcoholic options. The trend towards moderation and mindful drinking is well-ingrained in European culture, further propelling market growth. Regulatory frameworks are relatively clear, supporting innovation and widespread distribution. Consumers here often seek sophisticated flavor profiles and products that seamlessly fit into traditional social drinking occasions.

Asia Pacific is emerging as a high-growth region, characterized by increasing disposable incomes, changing dietary habits, and a growing middle-class population. While still nascent in some areas, markets such as Australia, Japan, and increasingly China are showing significant potential for non-alcoholic beverages. Cultural factors, including religious practices in some countries that discourage alcohol, also contribute to the appeal of non-alcoholic alternatives. The challenge in this region lies in adapting product portfolios to diverse local tastes and establishing robust distribution networks, offering substantial opportunities for future market expansion as consumer awareness and preference grow.

- North America: Strong emphasis on health, premiumization, and craft non-alcoholic offerings.

- Europe: High adoption driven by traditional beverage culture and growing moderation trends.

- Asia Pacific (APAC): Rapidly growing market with increasing health awareness and disposable incomes.

- Latin America: Emerging market with cultural shifts towards healthier alternatives and expanding retail presence.

- Middle East and Africa (MEA): Growth influenced by cultural and religious preferences for non-alcoholic options, albeit from a lower base.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Non Alcoholic Wine and Beer Market.- Heineken N.V.

- Anheuser-Busch InBev

- Carlsberg Group

- Kirin Holdings

- Beam Suntory

- Diageo

- Asahi Group Holdings

- Giesen Group

- Freixenet

- T.G.I. Friday's

- Athletic Brewing Company

- Big Drop Brewing Co.

- Gruvi

- Lyre's Spirit Co.

- Ritual Zero Proof

- Seedlip

- Noughty

- Stella Artois

- Lautus Wines

- Mikkeller

Frequently Asked Questions

What defines non-alcoholic wine and beer, and how is it made?

Non-alcoholic wine and beer are beverages that undergo traditional fermentation processes but then have their alcohol content significantly reduced or entirely removed. For beer, "non-alcoholic" typically means less than 0.5% alcohol by volume (ABV), while for wine, it generally means 0.0% or trace amounts. Common de-alcoholization methods include vacuum distillation, which evaporates alcohol at lower temperatures to preserve flavor, and reverse osmosis, which filters out alcohol molecules. Other techniques like spinning cone columns or arrested fermentation ensure the characteristic flavors and aromas of their alcoholic counterparts are retained, providing a true beverage experience without the intoxicating effects.

Is non-alcoholic wine and beer healthier than traditional alcoholic beverages?

Generally, non-alcoholic wine and beer are considered a healthier alternative to their alcoholic versions. They eliminate the health risks associated with alcohol consumption, such as liver damage, increased risk of certain cancers, and impaired cognitive function. Many non-alcoholic options also tend to have fewer calories and less sugar compared to their full-strength counterparts or even some sugary soft drinks. However, the exact health benefits can vary by product; consumers should still check nutritional labels for sugar content and calorie count to ensure they align with their dietary goals. The primary health advantage lies in the absence of alcohol.

What are the primary drivers of growth in the non-alcoholic beverage market?

The non-alcoholic beverage market's growth is primarily driven by a global surge in health and wellness consciousness, leading consumers to seek healthier lifestyle choices and moderate or abstain from alcohol. Evolving social norms and greater acceptance of non-alcoholic options in social settings also play a crucial role, allowing individuals to participate in drinking rituals without alcohol. Furthermore, significant advancements in de-alcoholization technology have drastically improved the taste and quality of non-alcoholic products, making them more appealing. Increased product diversification, including premium and craft options, along with expanded distribution channels, further contributes to market expansion.

What challenges do non-alcoholic wine and beer manufacturers face?

Manufacturers in the non-alcoholic wine and beer market face several key challenges. A major hurdle is consistently replicating the authentic taste, aroma, and mouthfeel of traditional alcoholic beverages after de-alcoholization, which requires advanced and often costly technological processes. Consumer perception regarding taste can still be a barrier, despite significant improvements in product quality. Additionally, navigating the complex and varied international regulations for labeling and marketing "non-alcoholic" products poses compliance challenges. Ensuring efficient supply chain management and competitive pricing while maintaining high quality also remains a constant effort for producers in this growing segment.

What is the market outlook for non-alcoholic wine and beer in the coming years?

The market outlook for non-alcoholic wine and beer is highly positive, with projections indicating robust and sustained growth over the next decade. Driven by persistent health trends, evolving consumer preferences for moderation, and continuous product innovation, the market is expected to experience significant expansion globally. The increasing availability of diverse and high-quality non-alcoholic options, including premium and craft varieties, will continue to attract new consumers and solidify the category's mainstream appeal. Both established beverage companies and agile startups are investing heavily in this sector, signaling strong confidence in its long-term potential as a vital component of the broader beverage industry.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted