Next Generation OSS and BSS Market

Next Generation OSS and BSS Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_703685 | Last Updated : August 05, 2025 |

Format : ![]()

![]()

![]()

![]()

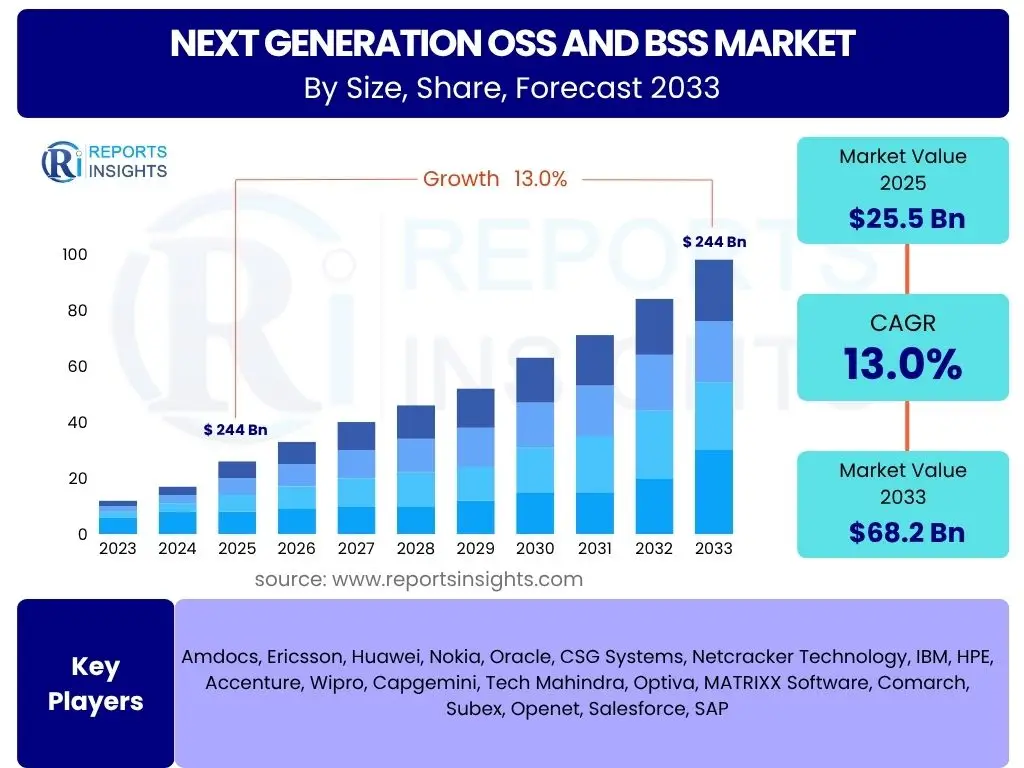

Next Generation OSS and BSS Market Size

According to Reports Insights Consulting Pvt Ltd, The Next Generation OSS and BSS Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 13.0% between 2025 and 2033. The market is estimated at USD 25.5 Billion in 2025 and is projected to reach USD 68.2 Billion by the end of the forecast period in 2033.

Key Next Generation OSS and BSS Market Trends & Insights

User inquiries frequently highlight the rapid evolution of telecommunications and the imperative for operators to modernize their operational and business support systems. A dominant theme in these queries revolves around the shift from monolithic, siloed legacy systems to more agile, cloud-native, and AI-driven architectures. There is a strong emphasis on understanding how these new systems facilitate the efficient management and monetization of advanced services, particularly those enabled by 5G, IoT, and edge computing.

Furthermore, significant interest is observed in the integration of Artificial Intelligence and Machine Learning (AI/ML) capabilities within OSS and BSS frameworks. Users seek information on how AI can automate complex network operations, enhance customer experience through personalized services, and enable predictive analytics for network health and revenue assurance. The demand for open, API-driven platforms that foster ecosystem collaboration and accelerate service innovation is also a recurring question, reflecting a broader industry move towards increased flexibility and interoperability.

Another prevalent concern among market stakeholders is the journey towards a truly customer-centric operational model. This involves transforming traditional service fulfillment and assurance processes to deliver seamless, on-demand experiences. The trends reflect a strategic pivot towards agile deployment models, microservices architectures, and a unified view of customer and network data to drive operational efficiency and create new revenue streams.

- Shift to Cloud-Native Architectures: Migration from on-premise legacy systems to highly scalable, flexible cloud-based OSS/BSS solutions.

- Increased AI and Machine Learning Adoption: Embedding AI/ML for network automation, predictive analytics, fraud detection, and customer experience enhancement.

- 5G Monetization and Service Orchestration: Development of systems capable of managing and monetizing complex 5G services, including network slicing and edge computing.

- API-First and Open Standards: Emphasis on open APIs and standards for seamless integration across diverse systems and third-party applications.

- Customer Experience Transformation: Focusing on unified customer views, personalized services, and proactive issue resolution through advanced analytics.

- Automation of Operations: Extensive use of automation across network operations, service fulfillment, and assurance processes to reduce manual intervention.

- Digital Twin Technology: Adoption of digital twins for real-time network modeling, simulation, and optimization.

AI Impact Analysis on Next Generation OSS and BSS

Common user questions regarding AI's impact on Next Generation OSS and BSS primarily focus on its transformative potential across various operational and business functions. Users frequently inquire about how AI can enhance automation, particularly in complex network management and service orchestration. There is significant interest in AI's role in predictive maintenance, proactive fault detection, and optimizing network performance to ensure high service availability and quality of experience for end-users.

Another key theme in user queries revolves around AI's contribution to improving customer experience and revenue management. This includes questions on how AI can personalize service offerings, optimize pricing strategies, detect revenue leakages, and enhance fraud prevention mechanisms. The expectation is that AI will move OSS and BSS from reactive problem-solving to proactive, intelligent operations, leading to reduced operational costs and improved profitability for communication service providers (CSPs).

Furthermore, users are keen to understand AI's capability in processing vast amounts of network and customer data to derive actionable insights. This encompasses applications such as intelligent resource allocation, dynamic network configuration, and automated service assurance. The overarching consensus is that AI is not merely an add-on but a fundamental enabler for the next generation of OSS and BSS, critical for navigating the complexities of 5G, IoT, and an increasingly digitalized service landscape.

- Enhanced Automation: AI drives autonomous network operations, reducing manual intervention and operational costs.

- Predictive Analytics: Enables proactive identification of potential network issues and customer churn, facilitating preventative measures.

- Optimized Network Performance: AI algorithms dynamically optimize network resources, ensuring superior quality of service and experience.

- Personalized Customer Experiences: Utilizes AI to analyze customer behavior for tailored service offerings and proactive support.

- Revenue Assurance and Fraud Detection: AI algorithms detect anomalies and potential revenue leakages, improving financial performance.

- Streamlined Service Fulfillment: Automates and optimizes the provisioning and activation of services, speeding up delivery.

- Intelligent Fault Management: AI quickly identifies root causes of network faults, leading to faster resolution times.

Key Takeaways Next Generation OSS and BSS Market Size & Forecast

Common user questions about the Next Generation OSS and BSS market size and forecast consistently point towards a strong interest in growth drivers, investment opportunities, and strategic implications for market participants. There is a clear emphasis on understanding which technologies and solutions within the OSS/BSS domain are poised for significant expansion, particularly in the context of 5G deployments, IoT proliferation, and the ongoing digital transformation initiatives of communication service providers (CSPs).

Users frequently seek insights into how the evolving telecommunications landscape, characterized by increasing network complexity and the demand for agile service delivery, directly translates into market expansion for Next Generation OSS and BSS. This includes queries about the impact of cloud adoption, AI integration, and the transition to open, programmable networks on market valuation and future growth trajectories. The insights desired often relate to identifying high-growth segments and regions that present the most lucrative opportunities for vendors and service providers.

The core takeaway from these inquiries is that the market for Next Generation OSS and BSS is not just growing; it is undergoing a fundamental transformation driven by technological advancements and operational necessities. The forecast underscores a critical need for CSPs to invest in modernizing their back-office systems to remain competitive, innovate new services, and efficiently manage increasingly complex digital ecosystems. This growth is a direct reflection of the imperative for agility, automation, and enhanced customer experience in the digital era.

- Significant Market Expansion: The market is projected for substantial growth, driven by digital transformation and network modernization.

- Investment in Cloud and AI is Crucial: Cloud-native architectures and AI/ML integration are key to future success and market share.

- 5G and IoT are Primary Growth Catalysts: The widespread rollout of 5G networks and the proliferation of IoT devices fuel demand for advanced OSS/BSS.

- Customer Experience as a Differentiator: Systems enabling superior customer journey management will command a premium.

- Agility and Automation are Imperatives: CSPs prioritize solutions that offer greater operational agility and extensive automation.

- Opportunities in Service Monetization: Next-gen BSS capabilities are vital for monetizing complex 5G services like network slicing.

Next Generation OSS and BSS Market Drivers Analysis

The Next Generation OSS and BSS market is propelled by a confluence of technological advancements and strategic imperatives within the telecommunications sector. A primary driver is the global rollout and increasing adoption of 5G networks, which demand more agile, automated, and intelligent operational and business support systems to manage their unprecedented complexity, massive connectivity, and diverse service requirements. Legacy OSS/BSS systems are inherently unsuited to handle the dynamic nature of 5G, necessitating investments in next-generation solutions.

Another significant driver is the widespread digital transformation initiatives undertaken by communication service providers (CSPs). These initiatives aim to enhance operational efficiency, reduce costs, and improve customer experience through automation, data analytics, and cloud migration. Next-gen OSS/BSS platforms are foundational to these transformations, enabling CSPs to streamline processes, automate service provisioning, and leverage data for informed decision-making across their entire value chain.

Furthermore, the escalating demand for superior customer experiences and personalized services is compelling CSPs to adopt more sophisticated OSS/BSS solutions. These systems enable a unified view of the customer, predictive analytics for churn prevention, and proactive service assurance, directly contributing to customer satisfaction and loyalty. The proliferation of IoT devices and services, requiring robust management and billing capabilities, also significantly contributes to the market's expansion.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Global 5G Network Rollouts | +2.5% | North America, Asia Pacific, Europe | Short to Mid-term (2025-2030) |

| Digital Transformation Initiatives by CSPs | +2.0% | Global | Mid-term (2025-2031) |

| Increasing Demand for Enhanced Customer Experience | +1.8% | Global | Short to Mid-term (2025-2030) |

| Proliferation of IoT Devices and Services | +1.5% | Asia Pacific, North America, Europe | Mid to Long-term (2027-2033) |

| Growing Complexity of Network Infrastructures | +1.2% | Global | Short to Mid-term (2025-2030) |

Next Generation OSS and BSS Market Restraints Analysis

Despite the strong growth drivers, the Next Generation OSS and BSS market faces several significant restraints that could impede its full potential. A primary challenge is the substantial initial investment required for the implementation and migration from legacy systems. Many communication service providers (CSPs) operate with tight budgets and face the daunting task of replacing or integrating decades-old, deeply embedded systems, which can involve considerable capital expenditure and operational disruption.

Another significant restraint is the complexity associated with integrating new, cloud-native, and AI-driven OSS/BSS solutions with existing legacy infrastructure. This often involves intricate data migration, interoperability issues, and ensuring seamless continuity of service during the transition. The absence of standardized interfaces and the bespoke nature of many legacy systems further complicate this integration, leading to prolonged deployment cycles and increased costs.

Furthermore, the scarcity of skilled personnel with expertise in emerging technologies such as cloud computing, AI/ML, and specific next-generation OSS/BSS platforms poses a considerable challenge. CSPs often struggle to find and retain talent capable of deploying, managing, and optimizing these sophisticated systems. This talent gap can delay adoption, increase reliance on external consultants, and ultimately slow down market growth. Concerns regarding data security and regulatory compliance in a highly interconnected environment also act as noteworthy restraints.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Initial Investment and Migration Costs | -1.8% | Global, particularly Tier 2/3 CSPs | Short to Mid-term (2025-2030) |

| Complexity of Integrating with Legacy Systems | -1.5% | Global | Short to Mid-term (2025-2030) |

| Shortage of Skilled Workforce | -1.0% | Global, developed economies | Mid-term (2025-2031) |

| Data Security and Privacy Concerns | -0.8% | Europe (GDPR), North America | Ongoing (2025-2033) |

| Regulatory and Compliance Challenges | -0.7% | Europe, Asia Pacific | Ongoing (2025-2033) |

Next Generation OSS and BSS Market Opportunities Analysis

The Next Generation OSS and BSS market presents significant opportunities for innovation and expansion, driven by the evolving needs of the telecommunications industry. One key opportunity lies in the burgeoning domain of network slicing and edge computing, enabled by 5G. Next-gen OSS/BSS solutions are crucial for the efficient orchestration, management, and monetization of these advanced services, allowing CSPs to create new revenue streams by offering customized network capabilities to enterprises and vertical industries.

Furthermore, the increasing adoption of AI and Machine Learning (ML) within OSS/BSS platforms opens avenues for highly automated and intelligent operations. This includes opportunities in predictive network maintenance, intelligent fault remediation, proactive customer support, and advanced fraud detection. By leveraging AI/ML, vendors can offer solutions that drastically reduce operational expenditures for CSPs while improving service quality and customer satisfaction, presenting a strong value proposition in a competitive market.

The growing emphasis on open APIs and partnerships within the telecom ecosystem also provides substantial opportunities. Collaborative frameworks and open-source initiatives allow for greater interoperability and foster a vibrant ecosystem of third-party developers and service providers. This enables CSPs to rapidly innovate and deploy new services, integrating best-of-breed solutions rather than relying on single-vendor, monolithic systems, thereby accelerating market growth and creating specialized niche opportunities for vendors.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Monetization of 5G Network Slicing and Edge Services | +2.2% | Global, focused on enterprises | Mid to Long-term (2027-2033) |

| Expansion of AI/ML-driven Automation in Operations | +1.9% | Global | Short to Mid-term (2025-2030) |

| Development of Open and API-driven Platforms | +1.7% | Global | Short to Mid-term (2025-2030) |

| Focus on Convergent Charging and Billing Solutions | +1.4% | Global | Mid-term (2026-2032) |

| Emergence of Digital Ecosystem Management Platforms | +1.0% | Global | Long-term (2028-2033) |

Next Generation OSS and BSS Market Challenges Impact Analysis

The Next Generation OSS and BSS market faces inherent challenges that can significantly influence its adoption rates and deployment success. A prominent challenge is the complexity of integrating these advanced systems with a multitude of diverse, often proprietary, legacy systems that communication service providers (CSPs) currently operate. This interoperability hurdle frequently leads to protracted deployment timelines, budget overruns, and potential disruptions to existing services, deterring rapid modernization efforts.

Another critical challenge is the rapid pace of technological evolution within the telecommunications sector. As new network technologies like 5G advanced, 6G research, and evolving IoT standards emerge, OSS/BSS solutions must continuously adapt. This requires significant ongoing investment in research and development from vendors and a continuous learning curve for CSPs, making long-term planning and technology lock-in a concern. The need for flexible, future-proof architectures is paramount, yet difficult to achieve.

Furthermore, cybersecurity threats pose a substantial challenge to the integrity and reliability of Next Generation OSS and BSS. As these systems become more interconnected and cloud-based, they present larger attack surfaces for malicious actors. Ensuring robust data security, protecting sensitive customer information, and maintaining network resilience against sophisticated cyberattacks are paramount. Addressing these security concerns requires continuous investment in advanced security protocols, compliance frameworks, and highly skilled security personnel, adding to the operational burden.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Complex Integration with Legacy Systems | -1.7% | Global | Short to Mid-term (2025-2030) |

| Rapid Technological Evolution and Obsolescence | -1.4% | Global | Ongoing (2025-2033) |

| Cybersecurity Threats and Data Breaches | -1.2% | Global | Ongoing (2025-2033) |

| Change Management within Organizations | -0.9% | Global | Short to Mid-term (2025-2030) |

| Regulatory Scrutiny and Compliance Costs | -0.6% | Europe, North America, Asia Pacific | Ongoing (2025-2033) |

Next Generation OSS and BSS Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the Next Generation OSS and BSS market, offering detailed insights into market dynamics, segmentation, regional trends, and competitive landscape. It covers the period from 2019 to 2033, with 2024 as the base year and a forecast extending to 2033. The report is designed to assist stakeholders in understanding the market's current state, future growth potential, and key strategic imperatives, offering actionable intelligence for business planning and investment decisions.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 25.5 Billion |

| Market Forecast in 2033 | USD 68.2 Billion |

| Growth Rate | 13.0% |

| Number of Pages | 250 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Amdocs, Ericsson, Huawei, Nokia, Oracle, CSG Systems, Netcracker Technology, IBM, HPE, Accenture, Wipro, Capgemini, Tech Mahindra, Optiva, MATRIXX Software, Comarch, Subex, Openet, Salesforce, SAP |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Next Generation OSS and BSS market is comprehensively segmented to provide a granular understanding of its diverse components and applications. This segmentation analysis dissects the market based on various factors, including the type of components offered (solutions and services), deployment models, operator tiers, and the specific end-user industries that leverage these advanced systems. Each segment represents a distinct facet of the market, driven by unique requirements and adoption patterns, collectively contributing to the market's overall growth trajectory.

Understanding these segments is crucial for market players to tailor their offerings, identify niche opportunities, and develop targeted strategies. For instance, the demand for cloud-based solutions is rapidly increasing across all operator types due to their scalability and flexibility, while specific industry verticals, such as BFSI and media, are increasingly seeking specialized OSS/BSS capabilities to manage their digital services and customer interactions. The detailed breakdown highlights where investments are being made and where future growth is anticipated across the value chain.

- By Component:

- Solutions: Encompassing critical functionalities such as Service Assurance, Revenue Management, Service Fulfillment, Network Management, Customer Management, Billing & Charging, and Analytics. These solutions form the core of operational and business support, enabling CSPs to manage their networks and customer interactions efficiently.

- Services: Including Consulting, Integration, and Managed Services, which are crucial for the successful planning, deployment, and ongoing operation of next-generation OSS/BSS environments. These services provide the expertise and support necessary for complex transformations.

- By Deployment:

- On-Premise: Traditional deployment where software and hardware are located at the customer's site. While still prevalent for sensitive data and legacy integration, its share is declining.

- Cloud: Includes public, private, and hybrid cloud models, offering scalability, flexibility, and reduced infrastructure costs. This segment is experiencing rapid growth due to its agility and support for modern architectures.

- By Operator Type:

- Tier 1: Large global and national operators with extensive infrastructure and subscriber bases, often leading early adoption of advanced OSS/BSS.

- Tier 2: Regional or national operators with moderate scale, often balancing innovation with cost-effectiveness.

- Tier 3 & MVNOs: Smaller operators and Mobile Virtual Network Operators, increasingly leveraging cloud-based and managed services due to limited resources.

- By End-User Industry:

- Telecom & IT: The primary consumers, including mobile and fixed-line operators, internet service providers, and data center operators.

- BFSI (Banking, Financial Services, and Insurance): Leveraging OSS/BSS concepts for managing digital services, customer engagement, and transaction processing.

- Media & Entertainment: Adopting solutions for content delivery, subscriber management, and streaming service monetization.

- Utilities: Implementing for smart grid management, IoT connectivity, and customer billing.

- Healthcare: Utilizing for remote patient monitoring, connected health devices, and data management.

- Others: Including transportation, manufacturing, and retail, as they adopt IoT and connected services.

Regional Highlights

The global Next Generation OSS and BSS market exhibits distinct regional dynamics, influenced by varying levels of digital infrastructure maturity, 5G deployment rates, regulatory landscapes, and investment capabilities of communication service providers (CSPs).

- North America: This region stands as a significant market, characterized by early and aggressive adoption of 5G technologies, high concentration of tier-1 CSPs, and a strong focus on innovation. The demand for advanced OSS and BSS solutions here is primarily driven by the need for network slicing monetization, edge computing integration, and enhancing customer experience through AI-driven automation. The presence of leading technology providers and a competitive market environment further propels investments in cloud-native and open-API based platforms.

- Europe: Europe represents a mature market with substantial investments in digital transformation initiatives. The region's focus on regulatory compliance, particularly GDPR, influences the design and implementation of OSS/BSS solutions with robust data privacy features. The rollout of 5G and the push towards network virtualization and service automation are key drivers. However, the diverse regulatory frameworks across countries and the presence of numerous legacy infrastructures can pose integration challenges.

- Asia Pacific (APAC): APAC is projected to be the fastest-growing market, largely due to rapid 5G rollouts in countries like China, South Korea, Japan, and India, coupled with a massive subscriber base and increasing smartphone penetration. The region is witnessing significant investments in network expansion and modernization, driving demand for scalable and efficient OSS/BSS to manage complex networks and new revenue streams from IoT and enterprise services. Government initiatives promoting digital economies also contribute significantly to market growth.

- Latin America: This region is experiencing a gradual but steady adoption of Next Generation OSS and BSS, driven by increasing internet penetration, mobile data consumption, and ongoing digitalization efforts. While facing challenges related to economic volatility and infrastructure development, there is a growing recognition among CSPs to modernize their systems to compete effectively and improve service delivery. Focus areas include basic automation, revenue management, and customer care improvements.

- Middle East and Africa (MEA): The MEA region is witnessing substantial growth, primarily fueled by significant infrastructure investments, particularly in the GCC countries, to deploy advanced 5G networks and smart city initiatives. There is a strong emphasis on leveraging next-generation OSS/BSS to support new digital services, manage rapidly expanding subscriber bases, and enhance operational efficiency. However, varying economic conditions and political stability across the region can influence the pace of adoption.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Next Generation OSS and BSS Market.- Amdocs

- Ericsson

- Huawei

- Nokia

- Oracle

- CSG Systems

- Netcracker Technology

- IBM

- HPE

- Accenture

- Wipro

- Capgemini

- Tech Mahindra

- Optiva

- MATRIXX Software

- Comarch

- Subex

- Openet

- Salesforce

- SAP

Frequently Asked Questions

Analyze common user questions about the Next Generation OSS and BSS market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is Next Generation OSS and BSS?

Next Generation Operations Support Systems (OSS) and Business Support Systems (BSS) are modern, often cloud-native, AI-driven software platforms that enable communication service providers (CSPs) to manage their networks and business operations efficiently. They facilitate automation, real-time analytics, and agile service delivery for advanced services like 5G, IoT, and digital transformation.

Why is Next Generation OSS and BSS important for telcos?

Next Generation OSS and BSS are crucial for telcos to manage the complexity of modern networks (e.g., 5G, SDN/NFV), automate operations, enhance customer experience, and rapidly launch and monetize new digital services. They enable agility, reduce operational costs, and provide the insights needed for competitive differentiation in a rapidly evolving market.

How does AI transform OSS and BSS?

AI transforms OSS and BSS by enabling advanced automation, predictive analytics for network issues and customer churn, intelligent service orchestration, and enhanced fraud detection. It allows CSPs to move from reactive to proactive operations, optimize resource allocation, and deliver more personalized and efficient customer experiences.

What are the main challenges in adopting Next Gen OSS and BSS?

Key challenges include high initial investment costs, complex integration with existing legacy systems, a shortage of skilled personnel with expertise in new technologies, ongoing cybersecurity concerns, and the rapid pace of technological evolution requiring continuous adaptation and updates.

What are the key market segments within Next Generation OSS and BSS?

The market segments primarily by components (solutions like service assurance, revenue management, network management, and services like consulting, integration), deployment models (on-premise vs. cloud), operator types (Tier 1, 2, 3 & MVNOs), and various end-user industries beyond telecom such as BFSI, Media & Entertainment, and Utilities.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted