Motor Vehicle Insurance Market

Motor Vehicle Insurance Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_702651 | Last Updated : July 31, 2025 |

Format : ![]()

![]()

![]()

![]()

Motor Vehicle Insurance Market Size

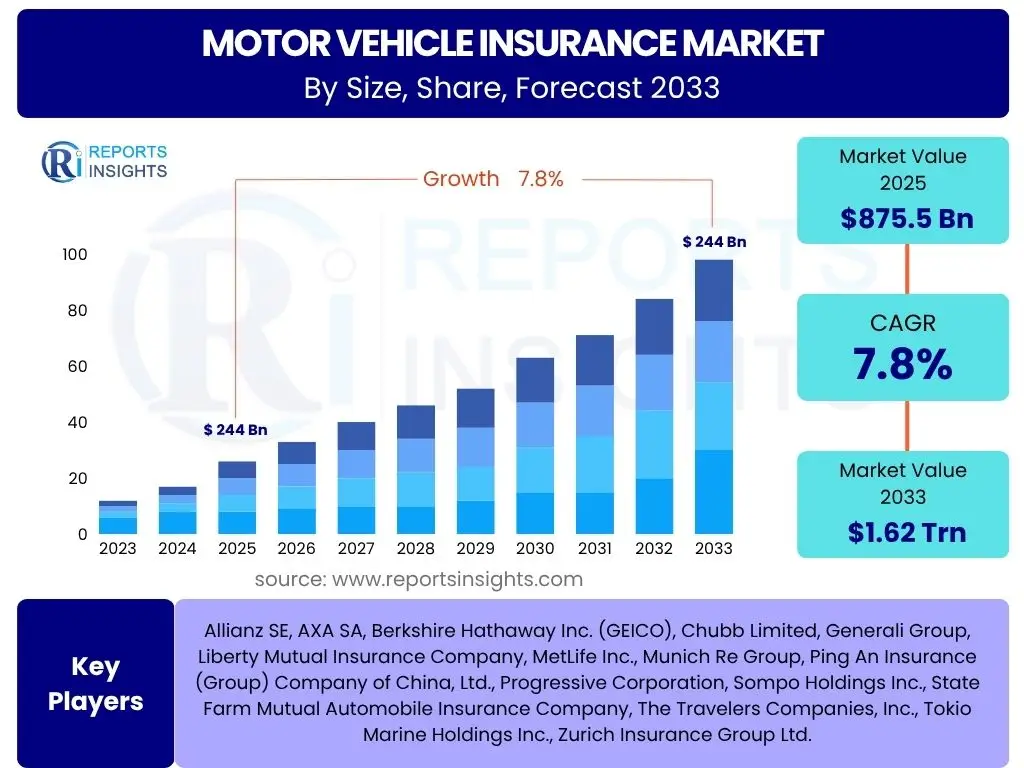

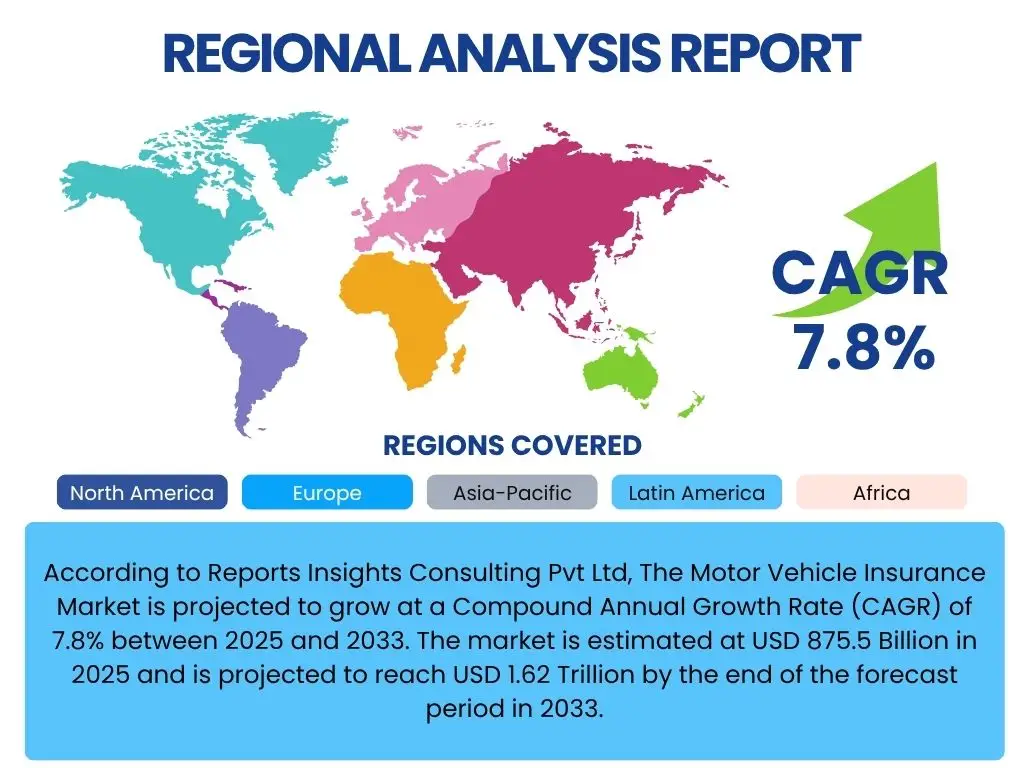

According to Reports Insights Consulting Pvt Ltd, The Motor Vehicle Insurance Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 7.8% between 2025 and 2033. The market is estimated at USD 875.5 Billion in 2025 and is projected to reach USD 1.62 Trillion by the end of the forecast period in 2033.

Key Motor Vehicle Insurance Market Trends & Insights

User inquiries frequently revolve around the transformative shifts occurring within the motor vehicle insurance sector, seeking to understand how technological advancements, evolving consumer behaviors, and environmental concerns are reshaping traditional models. Analysis reveals a strong focus on personalization, digitalization, and sustainability as core drivers of current market trends. Consumers are increasingly interested in policies that reflect their actual driving habits and vehicle usage, moving away from conventional blanket coverage.

The market is experiencing a significant pivot towards data-driven insurance solutions, enabled by telematics and artificial intelligence. This shift allows for more granular risk assessment, dynamic pricing, and proactive claims management. Furthermore, the rise of electric vehicles and autonomous driving technologies is prompting insurers to rethink policy structures, risk models, and liability frameworks. The emphasis is on creating more flexible, fair, and efficient insurance products that align with the future of mobility, while also addressing the environmental impact of the automotive industry and the demand for seamless digital experiences.

- Usage-Based Insurance (UBI) and Pay-As-You-Drive (PAYD) models gaining prominence.

- Increased adoption of telematics for personalized risk assessment and premium calculation.

- Digitalization of sales, claims processing, and customer service platforms.

- Emergence of embedded insurance solutions at the point of vehicle sale or financing.

- Growth of insurance offerings tailored for electric and autonomous vehicles.

- Focus on sustainability and green initiatives in insurance products.

- Personalization of policies based on individual driving behavior and lifestyle.

- Rise of micro-insurance and on-demand policies for shared mobility services.

AI Impact Analysis on Motor Vehicle Insurance

Common user questions regarding AI's impact on motor vehicle insurance frequently touch upon its role in risk assessment, fraud detection, claims processing, and customer service automation. Users are particularly interested in how AI can lead to more accurate pricing, faster claim settlements, and a more personalized insurance experience, while also expressing concerns about data privacy and algorithmic bias. The core theme is AI's potential to revolutionize efficiency and precision across the insurance value chain.

Artificial intelligence is profoundly transforming the motor vehicle insurance landscape by enabling unprecedented levels of data analysis and automation. AI algorithms can process vast amounts of data from telematics, accident reports, and external sources to generate highly accurate risk profiles, moving beyond traditional demographic factors. This capability facilitates more precise underwriting and dynamic pricing models. Moreover, AI-powered systems are significantly enhancing fraud detection capabilities by identifying suspicious patterns and anomalies in claims data, leading to reduced losses for insurers. In customer service, chatbots and virtual assistants provide instant support, while AI-driven claims processing accelerates damage assessment and settlement, ultimately improving the customer experience and operational efficiency for insurance providers.

- Enhanced risk assessment and underwriting through advanced data analytics.

- Automated and accelerated claims processing, reducing settlement times.

- Sophisticated fraud detection capabilities using pattern recognition.

- Personalized premium calculations based on individual driving behavior.

- Improved customer service via AI-powered chatbots and virtual assistants.

- Predictive analytics for accident prevention and proactive risk management.

- Development of new insurance products tailored for autonomous vehicles.

- Optimization of marketing and sales strategies through customer segmentation.

Key Takeaways Motor Vehicle Insurance Market Size & Forecast

User inquiries about key takeaways from the motor vehicle insurance market size and forecast consistently highlight curiosity about the market's long-term growth trajectory, the influence of digital transformation, and the evolving competitive landscape. There is a clear interest in understanding which factors will most significantly contribute to or impede market expansion. The insights reveal that sustained growth is anticipated, driven by a combination of increasing global vehicle ownership and the continuous innovation within insurance product offerings.

The market is poised for significant expansion, underpinned by the increasing global vehicle parc and the integration of advanced technologies like AI and telematics. These technologies are not only enhancing operational efficiencies for insurers but also enabling the development of more tailored and responsive insurance solutions that meet dynamic consumer demands. Digitalization across the insurance value chain, from policy issuance to claims settlement, is a critical enabler of this growth. While challenges such as economic volatility and stringent regulations persist, the overall outlook remains positive, with opportunities for differentiation through personalized products, superior customer experience, and strategic technological adoption.

- Projected robust growth indicating a healthy market expansion over the forecast period.

- Technological integration (AI, IoT, telematics) is a primary driver of market evolution.

- Shift towards customer-centric and personalized insurance offerings.

- Digital transformation is reshaping distribution channels and claims processes.

- Emerging economies present significant growth opportunities due to rising vehicle penetration.

- Focus on innovation for new risks, such as those associated with electric and autonomous vehicles.

- Competitive landscape is intensifying, pushing insurers towards efficiency and value creation.

Motor Vehicle Insurance Market Drivers Analysis

The motor vehicle insurance market is propelled by a confluence of macroeconomic, technological, and regulatory factors. A fundamental driver is the consistent global increase in vehicle sales and ownership, particularly in developing economies, which directly expands the base of insurable assets. Alongside this, rising disposable incomes in many regions enable more individuals to purchase vehicles and, consequently, seek insurance coverage, further fueling market expansion.

Technological advancements, such as telematics and advanced driver-assistance systems (ADAS), are creating new opportunities for risk assessment and personalized premium offerings, making insurance more appealing and accessible. Furthermore, the implementation of stringent regulatory mandates across various countries, making motor vehicle insurance compulsory, forms a critical foundational driver ensuring market stability and demand. This combination of growing vehicle parc, economic uplift, and evolving technological and regulatory landscapes collectively underpins the market's positive growth trajectory.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Global Vehicle Sales and Ownership | +2.1% | Asia Pacific, Latin America, Africa | Long-term (2025-2033) |

| Rising Disposable Incomes and Urbanization | +1.8% | Emerging Markets (India, China, Brazil) | Medium to Long-term |

| Mandatory Insurance Regulations | +1.5% | Globally pervasive, particularly Europe, Asia Pacific | Continuous |

| Technological Advancements (Telematics, ADAS) | +1.3% | North America, Europe, Developed Asia Pacific | Medium to Long-term |

| Growing Awareness of Insurance Benefits | +1.1% | Developing Economies | Long-term |

Motor Vehicle Insurance Market Restraints Analysis

Despite robust growth drivers, the motor vehicle insurance market faces several significant restraints that can temper its expansion. One of the primary challenges is the perceived high cost of insurance premiums, which can deter potential policyholders, especially in price-sensitive markets or during periods of economic downturn. Economic volatility and inflation can further exacerbate this issue, increasing operational costs for insurers and potentially leading to higher premiums for consumers.

Intense competition within the market, marked by a multitude of players vying for market share, often leads to pricing pressures that erode profit margins for insurers. Furthermore, the emergence of alternative transportation modes, such as shared mobility services, public transit improvements, and ride-hailing, could potentially reduce individual vehicle ownership rates in urban areas, thereby impacting the demand for traditional motor insurance policies. Navigating these restraints requires insurers to focus on value propositions, cost efficiencies, and innovative product development to maintain competitiveness and relevance.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Premium Costs and Affordability Concerns | -1.2% | Globally, particularly price-sensitive markets | Continuous |

| Economic Slowdowns and Inflationary Pressures | -0.9% | Global, varies by region | Short to Medium-term |

| Intense Market Competition and Price Wars | -0.8% | Mature Markets (North America, Europe) | Continuous |

| Rise of Shared Mobility and Public Transportation | -0.7% | Urban Centers globally | Medium to Long-term |

| Complex Regulatory Frameworks | -0.6% | Europe, highly regulated markets | Continuous |

Motor Vehicle Insurance Market Opportunities Analysis

The motor vehicle insurance market is rich with opportunities stemming from technological innovation, shifting consumer preferences, and unexplored market segments. The growing adoption of usage-based insurance (UBI) models, facilitated by telematics, represents a significant opportunity. UBI allows insurers to offer personalized premiums based on actual driving behavior, which can attract safer drivers, reduce claim frequencies, and enhance customer loyalty by providing a fairer pricing mechanism.

The rapid proliferation of electric vehicles (EVs) and the anticipated rise of autonomous vehicles (AVs) create entirely new segments for specialized insurance products. These vehicles have unique risk profiles and require tailored coverage, presenting a lucrative avenue for insurers willing to innovate. Furthermore, the potential for embedded insurance solutions, where coverage is seamlessly integrated at the point of vehicle purchase or financing, offers a streamlined distribution channel and enhanced customer convenience. Expanding into untapped emerging markets, leveraging digital channels, and harnessing big data analytics for hyper-personalization are additional key opportunities that can drive substantial market growth and competitive advantage for forward-thinking insurers.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Expansion of Usage-Based Insurance (UBI) Models | +1.9% | North America, Europe, Asia Pacific | Medium to Long-term |

| Growth in Electric Vehicle (EV) and Autonomous Vehicle (AV) Insurance | +1.7% | Globally, especially developed nations | Long-term |

| Development of Embedded Insurance Solutions | +1.5% | Global, particularly in automotive ecosystems | Medium-term |

| Penetration into Underserved Emerging Markets | +1.3% | Africa, Southeast Asia, Latin America | Long-term |

| Leveraging Big Data and AI for Hyper-personalization | +1.1% | Globally, for competitive differentiation | Medium to Long-term |

Motor Vehicle Insurance Market Challenges Impact Analysis

The motor vehicle insurance market faces a range of complex challenges that demand strategic responses from insurers. One significant hurdle is the increasing concern over data privacy and security, particularly as more personal driving data is collected through telematics devices and digital platforms. Ensuring robust cybersecurity measures and transparent data handling practices is crucial to maintaining consumer trust and complying with evolving data protection regulations like GDPR.

The rapid pace of technological advancements, while an opportunity, also poses a challenge for traditional insurers with legacy IT systems that may struggle to integrate new data streams and sophisticated analytical tools. This technological gap can hinder innovation and operational efficiency. Furthermore, the inherently competitive nature of the market, coupled with evolving consumer expectations for seamless digital experiences and instant gratification, presents ongoing challenges in terms of customer acquisition and retention. Insurers must continuously innovate, invest in modern infrastructure, and adapt their business models to effectively navigate these multifaceted challenges and remain competitive in a dynamic environment.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Data Privacy and Cybersecurity Concerns | -1.0% | Globally, especially highly regulated regions | Continuous |

| Integration of Legacy IT Systems with New Technologies | -0.9% | Mature markets with established insurers | Medium-term |

| Evolving Consumer Expectations for Digital Services | -0.8% | Globally, particularly younger demographics | Continuous |

| Climate Change Impact on Claims Frequency/Severity | -0.7% | Regions prone to extreme weather events | Long-term |

| Regulatory Divergence Across Jurisdictions | -0.6% | Europe, complex multinational operations | Continuous |

Motor Vehicle Insurance Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the Motor Vehicle Insurance Market, encompassing historical data, current trends, and future projections. The scope includes a detailed examination of market size and forecast, drivers, restraints, opportunities, and challenges influencing industry dynamics. It segments the market based on various criteria, offering granular insights into key product types, vehicle categories, distribution channels, and end-user demographics. Furthermore, the report provides a thorough regional analysis, highlighting growth prospects and competitive landscapes across major geographic areas. It also profiles key players, offering strategic insights into their market positions and recent developments.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 875.5 Billion |

| Market Forecast in 2033 | USD 1.62 Trillion |

| Growth Rate | 7.8% |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Allianz SE, AXA SA, Berkshire Hathaway Inc. (GEICO), Chubb Limited, Generali Group, Liberty Mutual Insurance Company, MetLife Inc., Munich Re Group, Ping An Insurance (Group) Company of China, Ltd., Progressive Corporation, Sompo Holdings Inc., State Farm Mutual Automobile Insurance Company, The Travelers Companies, Inc., Tokio Marine Holdings Inc., Zurich Insurance Group Ltd. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The motor vehicle insurance market is meticulously segmented to provide a granular understanding of its diverse components and drivers. This segmentation allows for targeted analysis of consumer needs, market dynamics, and competitive strategies across various dimensions of the insurance value chain. Understanding these segments is crucial for insurers to develop tailored products, optimize distribution channels, and refine their market penetration strategies.

The market is primarily broken down by coverage type, reflecting the different levels and kinds of protection sought by policyholders, from mandatory third-party liability to comprehensive packages. Vehicle type segmentation helps to differentiate risk profiles and premium structures based on vehicle characteristics and usage. Distribution channels highlight the evolving methods through which insurance products reach consumers, with a notable shift towards digital platforms. Finally, end-user segmentation distinguishes between individual consumers and commercial entities, each with distinct insurance requirements and purchasing behaviors, offering a holistic view of the market's structure.

- By Coverage Type: This segment includes different levels of protection.

- Third-Party Liability (TPL) Insurance: Covers damages to other vehicles or property, and injuries to third parties.

- Comprehensive Insurance: Offers protection against theft, fire, natural disasters, and damages to one's own vehicle.

- Collision Insurance: Covers damages to one's own vehicle resulting from a collision with another vehicle or object.

- Personal Accident Cover: Provides compensation for injuries or death to the driver or passengers in the insured vehicle.

- Other Coverages: Includes specialized add-ons like roadside assistance, legal expenses, or specific peril coverage.

- By Vehicle Type: Categorizes policies based on the type of vehicle being insured.

- Passenger Vehicles: Covers cars, SUVs, and other vehicles primarily used for personal transport.

- Commercial Vehicles: Includes policies for light, medium, and heavy commercial vehicles used for business purposes.

- Two-Wheelers: Specific insurance products designed for motorcycles and scooters.

- Other Vehicles: Encompasses insurance for recreational vehicles, agricultural vehicles, or specialized transport.

- By Distribution Channel: Describes the various avenues through which insurance products are sold.

- Insurance Agents/Brokers: Traditional intermediary channels providing personalized advice and sales.

- Direct (Online, Company Websites): Policy sales directly from the insurer via digital platforms.

- Bancassurance: Distribution of insurance products through banks' sales channels.

- Automobile Dealerships: Insurance offerings provided at the point of vehicle purchase.

- By End-User: Differentiates between individual and commercial policyholders.

- Individual/Personal: Policies for privately owned vehicles.

- Commercial/Fleet Owners: Insurance solutions for businesses operating multiple vehicles.

Regional Highlights

- North America: A mature and technologically advanced market characterized by high vehicle ownership rates and a strong emphasis on personalized insurance products. The region is a frontrunner in the adoption of telematics and usage-based insurance, driven by consumer demand for competitive pricing and data-driven insights. Regulatory environments are well-established, and the market shows a consistent trend towards digital transformation and innovation in claims processing.

- Europe: This region exhibits a diverse market landscape with varying regulatory frameworks across countries. Western European nations represent mature markets with high insurance penetration, while Central and Eastern Europe offer growth potential. The market is increasingly focused on sustainability, with a growing demand for insurance solutions for electric vehicles. Usage-based insurance is also gaining significant traction, particularly in countries like Italy and the UK, driven by favorable regulatory support and consumer acceptance.

- Asia Pacific (APAC): The APAC region is poised for significant growth, fueled by rapid urbanization, increasing disposable incomes, and a booming automotive industry, particularly in emerging economies like China, India, and Southeast Asia. This region is witnessing a surge in new vehicle sales, leading to a substantial expansion of the insurable base. Digital transformation is a key theme, with a strong preference for online distribution channels and mobile-first insurance solutions.

- Latin America: Characterized by developing markets with increasing vehicle penetration rates and a growing awareness of insurance benefits. Economic stability and infrastructure development in countries such as Brazil and Mexico are driving market expansion. While traditional distribution channels remain significant, there is a gradual shift towards digital platforms and a rising interest in more flexible and affordable insurance options tailored to specific local needs.

- Middle East and Africa (MEA): An emerging market with considerable untapped potential. Growth is driven by infrastructure projects, increasing vehicle ownership, and a young, digitally-savvy population. The region is witnessing a gradual adoption of technology-driven insurance solutions, although market penetration levels are generally lower compared to developed regions. Regulatory reforms aimed at enhancing market transparency and consumer protection are expected to further stimulate growth.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Motor Vehicle Insurance Market.- Allianz SE

- AXA SA

- Berkshire Hathaway Inc. (GEICO)

- Chubb Limited

- Generali Group

- Liberty Mutual Insurance Company

- MetLife Inc.

- Munich Re Group

- Ping An Insurance (Group) Company of China, Ltd.

- Progressive Corporation

- Sompo Holdings Inc.

- State Farm Mutual Automobile Insurance Company

- The Travelers Companies, Inc.

- Tokio Marine Holdings Inc.

- Zurich Insurance Group Ltd.

Frequently Asked Questions

Analyze common user questions about the Motor Vehicle Insurance market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is motor vehicle insurance?

Motor vehicle insurance, also known as auto insurance or car insurance, is a contract between a vehicle owner and an insurer. In exchange for premium payments, the insurer agrees to pay for specific losses, such as property damage, bodily injury, or liability arising from traffic collisions or other incidents involving the insured vehicle. It provides financial protection against physical damage or bodily injury resulting from traffic accidents and against liability that could arise from an accident.

Why is motor vehicle insurance important?

Motor vehicle insurance is crucial for several reasons. Firstly, it is legally mandated in most countries and regions to ensure financial responsibility in case of accidents. Secondly, it provides financial protection to policyholders against the potentially high costs of vehicle repairs, medical expenses, or legal liabilities arising from accidents. Without it, individuals could face significant financial burdens. It also offers peace of mind by covering risks like theft, vandalism, and natural disasters, depending on the policy type.

How is motor vehicle insurance premium calculated?

Motor vehicle insurance premiums are calculated based on various factors that assess the risk of a claim. These typically include the driver's age, driving record, claim history, and location. The type of vehicle (make, model, age, safety features), its primary usage (personal, commercial), and the chosen coverage types and deductibles also significantly influence the premium. Insurers use complex algorithms and historical data to determine individual risk profiles and set appropriate prices.

What factors affect motor vehicle insurance rates?

Several key factors impact motor vehicle insurance rates. These include the driver's age and experience, driving history (e.g., accidents, violations), and credit score (where permitted by law). The type, age, and safety rating of the vehicle, as well as its repair costs, also play a role. Furthermore, geographical location, the amount of coverage chosen, and the selected deductible significantly influence the final premium. Newer factors like telematics data for usage-based insurance are also increasingly affecting rates.

How will autonomous vehicles impact motor insurance?

Autonomous vehicles (AVs) are expected to profoundly impact motor insurance by shifting the focus of liability from human error to software, hardware, or manufacturers. As AV technology matures, accident frequency may decrease, potentially lowering premiums. However, the complexity of AVs might lead to higher repair costs. Insurers will need to adapt their risk assessment models, develop new policy types (e.g., product liability for manufacturers), and collaborate closely with automotive manufacturers to address the evolving liability landscape.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted