MOCVD for LED Market

MOCVD for LED Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_703283 | Last Updated : August 01, 2025 |

Format : ![]()

![]()

![]()

![]()

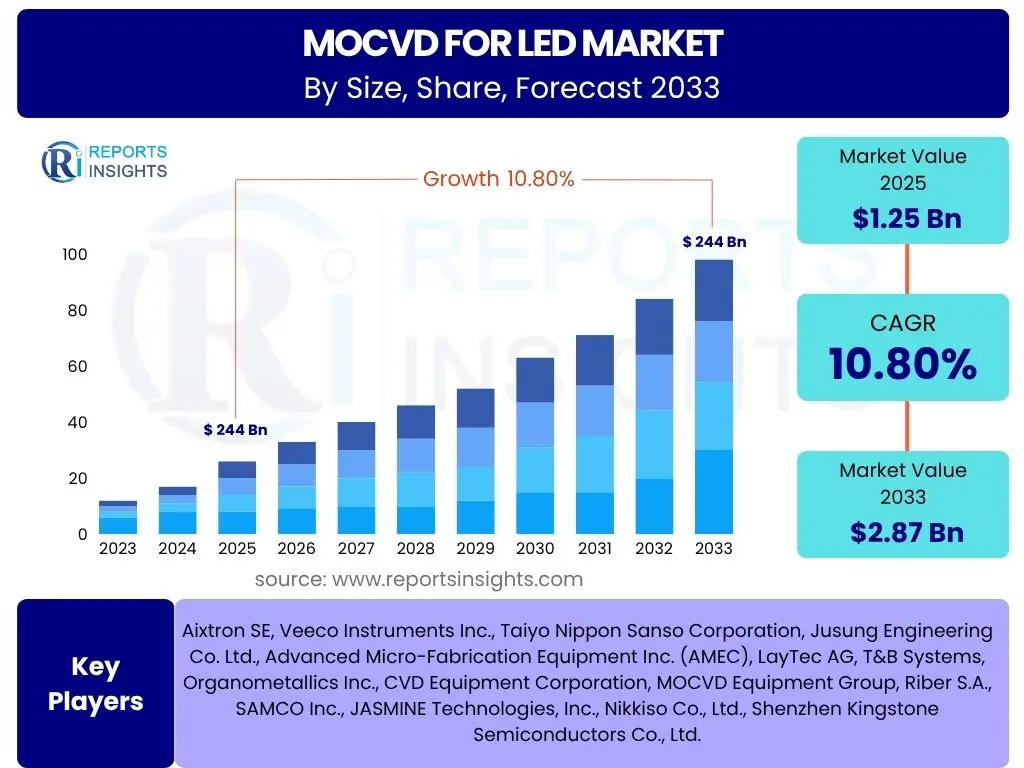

MOCVD for LED Market Size

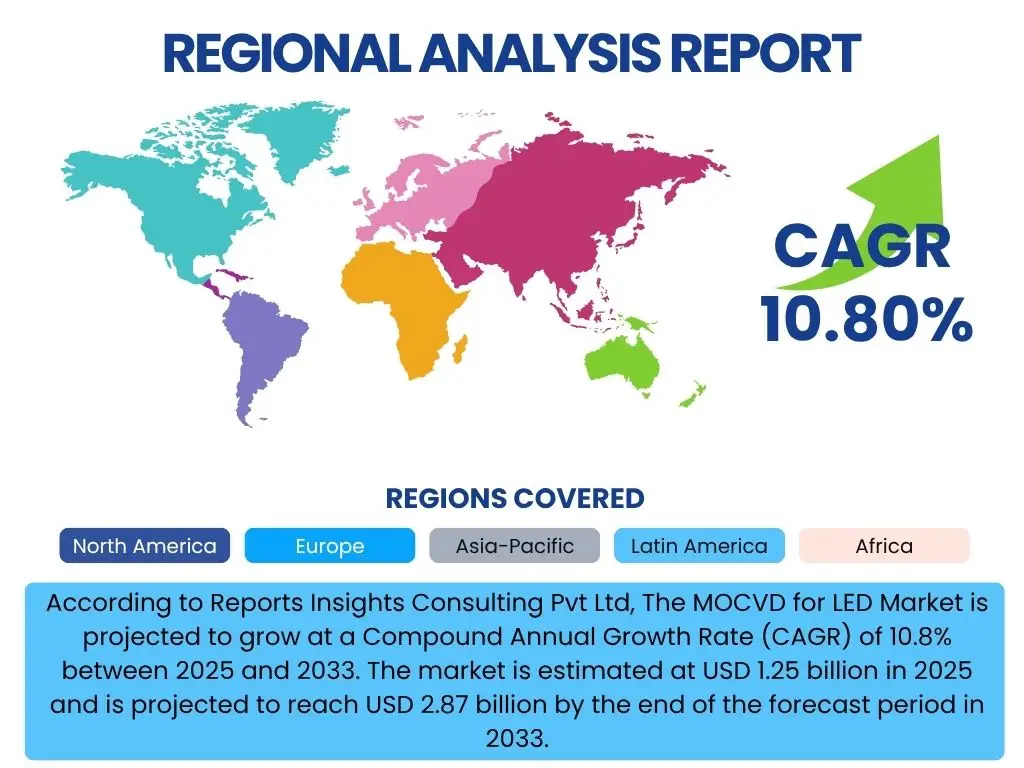

According to Reports Insights Consulting Pvt Ltd, The MOCVD for LED Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 10.8% between 2025 and 2033. The market is estimated at USD 1.25 billion in 2025 and is projected to reach USD 2.87 billion by the end of the forecast period in 2033.

Key MOCVD for LED Market Trends & Insights

The MOCVD for LED market is experiencing dynamic shifts driven by advancements in lighting technology and increasing demand for energy-efficient solutions. Key trends indicate a strong focus on higher efficiency, miniaturization, and the integration of MOCVD technology into novel applications beyond traditional illumination. Users are keenly interested in how these trends will shape the competitive landscape, influence material science, and impact manufacturing processes, specifically concerning the scalability and cost-effectiveness of advanced LED production. The market is also seeing a push towards more sustainable and environmentally friendly production methods, which MOCVD technology can support through optimized processes.

Furthermore, the growing adoption of compound semiconductors in various high-performance applications, such as micro-LED displays and advanced sensor technologies, is significantly influencing MOCVD equipment design and capabilities. This drives innovation in reactor design, precursor delivery systems, and in-situ monitoring tools. The pursuit of greater uniformity and reproducibility across larger wafer sizes remains a critical area of development, directly impacting the yield and cost structures for LED manufacturers. The market's future trajectory is deeply intertwined with these technological advancements and the broadening scope of LED applications.

- Shift towards GaN-on-Si substrates for cost reduction and larger wafer processing.

- Rising demand for Mini-LED and Micro-LED displays in consumer electronics and automotive.

- Development of UV-LEDs and IR-LEDs for sterilization, curing, and sensing applications.

- Integration of advanced automation and process control in MOCVD systems for higher yield.

- Increased focus on epitaxy of AlGaN and InGaN materials for advanced LED structures.

- Emphasis on energy-efficient and environmentally friendly MOCVD processes.

AI Impact Analysis on MOCVD for LED

User queries regarding AI's impact on MOCVD for LED consistently highlight expectations for improved efficiency, predictive capabilities, and enhanced process control. There is significant interest in how artificial intelligence and machine learning can optimize complex growth parameters, reduce material waste, and accelerate the development of new epitaxial structures. Users are exploring AI's potential in real-time data analysis to achieve higher yield rates and more consistent product quality, which are critical challenges in MOCVD. Concerns often revolve around the initial investment in AI integration, data security, and the need for specialized expertise to implement and manage AI-driven systems effectively within existing manufacturing infrastructures.

The application of AI in MOCVD extends beyond just process optimization to encompass predictive maintenance, enabling manufacturers to foresee equipment failures and schedule interventions proactively, thus minimizing costly downtime. Furthermore, AI algorithms can analyze vast datasets from previous growth runs to identify optimal conditions for new materials or structures, drastically reducing trial-and-error cycles in research and development. This capability can accelerate time-to-market for innovative LED products. The long-term vision involves fully autonomous MOCVD systems that self-adjust based on real-time feedback, representing a significant leap forward in manufacturing capability and precision for the LED industry.

- Optimized process parameter control through machine learning algorithms, enhancing yield and uniformity.

- Predictive maintenance of MOCVD equipment, reducing downtime and operational costs.

- Real-time in-situ monitoring with AI-driven analytics for immediate defect detection and correction.

- Accelerated material research and development by simulating growth conditions and predicting material properties.

- Automated quality control and wafer inspection, improving consistency and reducing manual intervention.

- Enhanced data analysis for root cause identification of process deviations and improved troubleshooting.

Key Takeaways MOCVD for LED Market Size & Forecast

User inquiries about key takeaways from the MOCVD for LED market size and forecast consistently point towards a robust growth trajectory, primarily fueled by the pervasive adoption of LED technology across diverse applications. The market's expansion is not merely incremental but driven by significant technological evolution within the LED sector, demanding more sophisticated and efficient MOCVD systems. The shift towards Mini-LED and Micro-LED displays is a pivotal force, creating substantial new demand for high-performance MOCVD equipment capable of precise and uniform epitaxy on larger substrates. This growth is anticipated to be globally distributed, with Asia Pacific remaining the dominant region due to its established manufacturing base.

Furthermore, the forecast underscores the critical importance of continuous innovation in MOCVD technology to meet future LED performance requirements, including higher power efficiency, longer lifespan, and broader spectral ranges (e.g., UV and IR LEDs). The market will also increasingly value MOCVD solutions that offer lower cost of ownership, higher throughput, and enhanced automation. Understanding these dynamics is crucial for stakeholders to strategize effectively, focusing on R&D, strategic partnerships, and market diversification to capitalize on emerging opportunities and mitigate potential challenges in this highly competitive landscape.

- The MOCVD for LED market is set for substantial growth, driven by expanding LED applications and technological advancements.

- Mini-LED and Micro-LED technologies are significant growth catalysts, demanding advanced MOCVD capabilities.

- Asia Pacific is projected to maintain its market leadership due to extensive LED manufacturing infrastructure.

- Continuous innovation in MOCVD system design for efficiency, throughput, and automation is crucial for market success.

- Increasing adoption of UV and IR LEDs will open new market segments for MOCVD technology.

- Strategic investments in R&D and supply chain optimization will be key competitive differentiators.

MOCVD for LED Market Drivers Analysis

The MOCVD for LED market is significantly propelled by the increasing global demand for energy-efficient lighting solutions and advanced display technologies. As environmental regulations become stricter and energy costs continue to rise, LEDs are increasingly favored over traditional lighting methods due to their superior efficiency, longer lifespan, and reduced environmental impact. This widespread adoption across residential, commercial, and industrial sectors directly stimulates the demand for MOCVD equipment, which is indispensable for the epitaxial growth of the semiconductor layers essential for LED production.

Moreover, the rapid evolution and widespread commercialization of Mini-LED and Micro-LED display technologies in consumer electronics, automotive infotainment, and augmented/virtual reality (AR/VR) devices are creating substantial new demand for MOCVD systems. These next-generation displays require incredibly precise and uniform epitaxial growth, pushing the boundaries of MOCVD technology and driving manufacturers to invest in more sophisticated and high-throughput reactors. The integration of LEDs into smart city infrastructure and innovative automotive lighting systems further contributes to this escalating demand, cementing MOCVD's critical role in the future of optoelectronics.

Furthermore, government initiatives and incentives promoting energy conservation and sustainable technologies globally are accelerating the transition to LED lighting. These policies often include subsidies for LED adoption or mandates for energy-efficient building standards, which indirectly boost the MOCVD market. The continuous push for miniaturization and higher performance in electronic devices also necessitates advanced semiconductor materials, for which MOCVD remains a cornerstone manufacturing process, ensuring sustained market growth.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Demand for Energy-Efficient LED Lighting | +2.5% | Global, particularly Asia Pacific, Europe | Long-term (2025-2033) |

| Growth of Mini-LED and Micro-LED Display Technologies | +2.0% | Global, particularly North America, APAC | Medium-term (2026-2030) |

| Government Initiatives and Regulations Promoting LED Adoption | +1.5% | Europe, Asia Pacific, North America | Medium-term (2025-2030) |

| Expansion of LED Applications in Automotive and Consumer Electronics | +1.8% | Global, particularly China, Germany, Japan | Long-term (2025-2033) |

| Technological Advancements in III-V Compound Semiconductors | +1.0% | Global, particularly US, Japan, South Korea | Long-term (2027-2033) |

MOCVD for LED Market Restraints Analysis

Despite the robust growth drivers, the MOCVD for LED market faces several significant restraints. One primary challenge is the high capital expenditure required for acquiring and installing MOCVD systems. These machines are technologically complex and represent a substantial investment for manufacturers, particularly smaller and medium-sized enterprises. The high upfront costs can deter new entrants and limit the expansion plans of existing players, especially in a market characterized by rapid technological obsolescence and the need for continuous upgrades.

Another key restraint is the inherent technological complexity associated with MOCVD processes. Achieving precise control over epitaxial layer thickness, composition, and uniformity requires highly skilled operators and extensive research and development. Any deviation in process parameters can lead to significant yield losses, impacting profitability. The sensitivity of the process to precursor purity and gas flow dynamics adds further layers of complexity, requiring stringent quality control and specialized maintenance. This complexity contributes to higher operational costs and can limit manufacturing flexibility.

Furthermore, the competitive landscape and emergence of alternative deposition techniques, though not yet directly comparable for all LED types, present a long-term restraint. While MOCVD remains the gold standard for high-performance LEDs, advancements in techniques like atomic layer deposition (ALD) or hybrid deposition methods could, in certain niche applications, offer competitive alternatives or complement existing processes. Trade disputes, geopolitical tensions, and supply chain vulnerabilities for critical precursors and components also pose ongoing risks, potentially leading to increased costs and production delays, thereby hindering market growth.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Capital Expenditure and Operating Costs of MOCVD Systems | -1.5% | Global, particularly emerging markets | Long-term (2025-2033) |

| Technological Complexity and Need for Skilled Workforce | -1.0% | Global | Long-term (2025-2033) |

| Supply Chain Vulnerabilities for Precursors and Components | -0.8% | Global, particularly Asia Pacific, Europe | Short-term (2025-2027) |

| Intense Competition and Pricing Pressures in the LED Market | -0.7% | Global, particularly China | Medium-term (2025-2030) |

MOCVD for LED Market Opportunities Analysis

The MOCVD for LED market is poised for significant growth stemming from several emerging opportunities. The most prominent opportunity lies in the expanding applications of UV-LEDs and IR-LEDs. UV-LEDs are increasingly utilized in sterilization, water purification, industrial curing, and medical applications, offering compact, mercury-free, and energy-efficient alternatives. Similarly, IR-LEDs are finding widespread use in advanced sensing, automotive night vision, security cameras, and gesture recognition, opening up entirely new market verticals that require precise epitaxial growth facilitated by MOCVD technology. This diversification beyond traditional visible light applications presents a substantial growth avenue for MOCVD equipment manufacturers.

Another significant opportunity is the continuous advancement in solid-state lighting (SSL) and the broader adoption of smart lighting solutions. As cities and industries move towards smart infrastructure, the demand for networked, dimmable, and color-tunable LEDs is surging. MOCVD technology is crucial for producing the high-quality, high-performance LEDs required for these sophisticated applications. Furthermore, the development of new compound semiconductor materials, such as GaN-on-Si and GaN-on-GaN for power electronics and high-frequency devices, leveraging MOCVD processes, presents cross-sector opportunities for MOCVD system providers.

The increasing focus on sustainable manufacturing practices and circular economy principles also creates opportunities for MOCVD system providers. Innovations that reduce precursor consumption, improve energy efficiency of the MOCVD process itself, and enable the use of recycled materials or less hazardous chemicals will be highly valued. Furthermore, the push for larger wafer sizes (e.g., 8-inch GaN-on-Si) and higher throughput MOCVD systems to drive down manufacturing costs for Mini/Micro-LEDs and general lighting continues to be a major opportunity for technology innovation and market penetration.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Emergence and Growth of UV-LED and IR-LED Markets | +1.8% | Global, particularly US, Europe, Japan | Long-term (2026-2033) |

| Development of Advanced Compound Semiconductor Materials (e.g., GaN-on-GaN) | +1.2% | Global, particularly US, Japan, South Korea | Long-term (2027-2033) |

| Increasing Adoption of Smart Lighting and IoT Integration | +1.5% | North America, Europe, Asia Pacific | Medium-term (2025-2030) |

| Transition to Larger Wafer Sizes (e.g., 8-inch GaN-on-Si) for Cost Reduction | +1.0% | Asia Pacific, North America | Medium-term (2026-2031) |

MOCVD for LED Market Challenges Impact Analysis

The MOCVD for LED market encounters several challenges that can impede its growth and operational efficiency. One significant challenge is achieving uniform and high-quality epitaxial growth across larger wafer sizes and for complex material stacks. As the industry moves towards 6-inch and 8-inch wafers for cost reduction, maintaining consistent film thickness, composition, and crystal quality across the entire wafer becomes increasingly difficult. Non-uniformity can lead to reduced yield and higher production costs, directly impacting profitability for LED manufacturers and presenting a persistent engineering challenge for MOCVD system designers.

Another critical challenge is the intense price competition within the broader LED market. While MOCVD equipment is essential, the downstream LED product market is highly commoditized, leading to continuous pressure on manufacturers to reduce production costs. This pressure cascades back to MOCVD system suppliers, demanding more cost-effective, higher-throughput, and more efficient equipment without compromising performance. Balancing these conflicting demands for lower cost and higher performance presents a constant challenge for MOCVD technology innovation and market penetration.

Furthermore, environmental regulations pertaining to the handling and disposal of hazardous precursors used in MOCVD, such as trimethylgallium (TMGa) and ammonia, pose operational and compliance challenges. Ensuring safe handling, effective waste management, and minimizing environmental impact adds to the operational complexity and cost. The rapid pace of technological change in the LED industry also means MOCVD equipment can quickly become outdated, necessitating significant ongoing investment in R&D and upgrades to remain competitive. Maintaining expertise and controlling the highly specialized supply chain for MOCVD components are additional complex hurdles.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Achieving High Uniformity and Yield on Larger Wafer Sizes | -1.0% | Global | Long-term (2025-2033) |

| Intense Price Competition and Margin Pressure in the LED Industry | -0.9% | Global, particularly Asia Pacific | Medium-term (2025-2030) |

| Strict Environmental Regulations and Safe Handling of Precursors | -0.7% | Europe, North America, Japan | Long-term (2025-2033) |

| Rapid Technological Obsolescence and Need for Continuous R&D | -0.6% | Global | Long-term (2025-2033) |

MOCVD for LED Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the MOCVD for LED market, covering historical data, current trends, and future projections. It segments the market by reactor type, application, material, and region, offering a holistic view of market dynamics. The report identifies key growth drivers, restraints, opportunities, and challenges, along with a detailed competitive landscape analysis profiling major industry players. It also includes insights into technological advancements, the impact of artificial intelligence, and a thorough regional analysis, aiding stakeholders in strategic decision-making and investment planning.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 1.25 billion |

| Market Forecast in 2033 | USD 2.87 billion |

| Growth Rate | 10.8% CAGR |

| Number of Pages | 245 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Aixtron SE, Veeco Instruments Inc., Taiyo Nippon Sanso Corporation, Jusung Engineering Co. Ltd., Advanced Micro-Fabrication Equipment Inc. (AMEC), LayTec AG, T&B Systems, Organometallics Inc., CVD Equipment Corporation, MOCVD Equipment Group, Riber S.A., SAMCO Inc., JASMINE Technologies, Inc., Nikkiso Co., Ltd., Shenzhen Kingstone Semiconductors Co., Ltd. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The MOCVD for LED market is meticulously segmented to provide a granular understanding of its diverse components and their respective contributions to overall market dynamics. This segmentation facilitates detailed analysis of growth opportunities and challenges across various product types, applications, and regional landscapes. Understanding these segments is crucial for stakeholders to identify lucrative niches, develop targeted strategies, and allocate resources effectively within the highly competitive MOCVD ecosystem.

The segmentation by reactor type, for instance, highlights the technological preferences and efficiencies associated with different MOCVD system designs. Application-based segmentation underscores the primary end-use sectors driving demand for LED components and, consequently, MOCVD equipment. Material segmentation is vital as it reflects the foundational semiconductor compounds driving LED performance improvements, while end-use industry segmentation provides a macro-level view of demand across various economic sectors. Each segment offers unique insights into market trends and investment potential.

- By Reactor Type: Horizontal Reactor, Vertical Reactor, Planetary Reactor, Showerhead Reactor.

- By Application: General Lighting, Automotive Lighting, Backlighting (LCD, Mini-LED), Specialty Lighting (UV-C, IR), Display (Micro-LED, OLED), Indicators & Signals.

- By Material: Gallium Nitride (GaN), Gallium Arsenide (GaAs), Indium Phosphide (InP), Aluminum Gallium Indium Phosphide (AlGaInP), Silicon Carbide (SiC).

- By End-Use Industry: Consumer Electronics, Automotive, General Illumination, Healthcare, Industrial, Aerospace & Defense.

Regional Highlights

- Asia Pacific (APAC): Dominates the MOCVD for LED market due to the presence of major LED manufacturing hubs, robust consumer electronics production, and government support for LED adoption in countries like China, South Korea, Japan, and Taiwan. The region is a key driver for Mini-LED and Micro-LED adoption.

- North America: Exhibits significant growth driven by advancements in advanced display technologies, research and development in compound semiconductors, and increasing adoption of specialty LEDs (UV, IR) in medical and industrial sectors, particularly in the United States.

- Europe: Characterized by strong emphasis on energy efficiency, smart lighting initiatives, and growing automotive sector demanding advanced LED solutions. Countries like Germany and the Netherlands are key contributors to MOCVD technology and application development.

- Latin America & Middle East & Africa (MEA): Emerging markets with nascent but growing LED manufacturing capabilities and increasing demand for energy-efficient lighting infrastructure. Investment in smart city projects in the MEA region is expected to drive future growth.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the MOCVD for LED Market.- Aixtron SE

- Veeco Instruments Inc.

- Taiyo Nippon Sanso Corporation

- Jusung Engineering Co. Ltd.

- Advanced Micro-Fabrication Equipment Inc. (AMEC)

- LayTec AG

- T&B Systems

- Organometallics Inc.

- CVD Equipment Corporation

- MOCVD Equipment Group

- Riber S.A.

- SAMCO Inc.

- JASMINE Technologies, Inc.

- Nikkiso Co., Ltd.

- Shenzhen Kingstone Semiconductors Co., Ltd.

- Opto-GaN, Inc.

- Meyer Burger Technology AG

- Fujifilm Corporation (Materials)

- Epistar Corporation (Utilizes MOCVD)

- Lumileds Holding B.V. (LED Manufacturer)

Frequently Asked Questions

What is MOCVD for LED?

MOCVD (Metal-Organic Chemical Vapor Deposition) for LED refers to a highly specialized epitaxy technique used to grow thin, crystalline layers of semiconductor materials, primarily gallium nitride (GaN) and its alloys, onto a substrate. This process is fundamental to manufacturing light-emitting diodes (LEDs) as it forms the active regions responsible for light emission.

What are the primary applications driving the MOCVD for LED market?

The MOCVD for LED market is primarily driven by the increasing demand for general illumination (e.g., residential, commercial lighting), advanced displays (especially Mini-LED and Micro-LED in TVs, smartphones, and automotive), and specialized applications such as UV-C LEDs for sterilization and IR-LEDs for sensing and automotive night vision systems.

How does AI impact MOCVD processes for LED manufacturing?

AI significantly impacts MOCVD processes by enabling real-time optimization of growth parameters, predictive maintenance for equipment, and automated quality control. It can analyze vast datasets to improve yield, enhance uniformity of epitaxial layers, accelerate material research, and reduce operational costs by minimizing downtime and waste.

What are the main challenges faced by the MOCVD for LED market?

Key challenges include the high capital investment required for MOCVD systems, the inherent technological complexity in achieving high uniformity and yield on larger wafer sizes, intense price competition within the LED industry, and strict environmental regulations concerning the handling of hazardous precursors.

Which regions are leading the MOCVD for LED market growth?

The Asia Pacific region, particularly countries like China, South Korea, Japan, and Taiwan, leads the MOCVD for LED market due to its extensive LED manufacturing infrastructure and high production volumes. North America and Europe also show significant growth driven by R&D, advanced applications, and government initiatives.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted