LED Phosphor Market

LED Phosphor Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_702888 | Last Updated : August 01, 2025 |

Format : ![]()

![]()

![]()

![]()

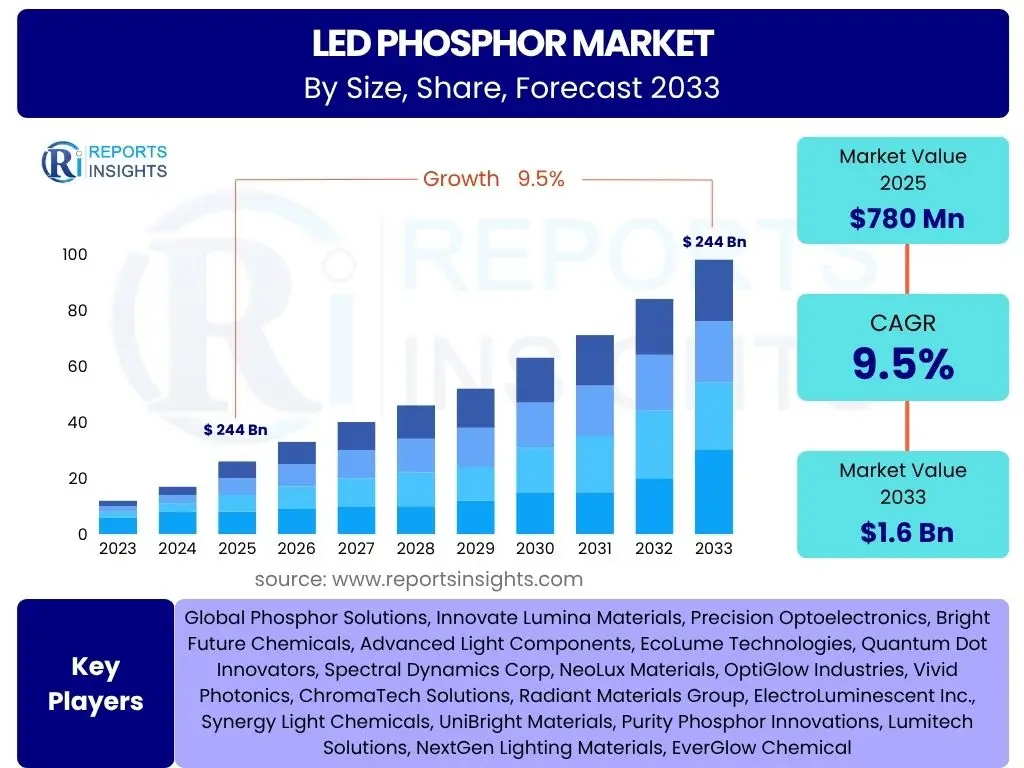

LED Phosphor Market Size

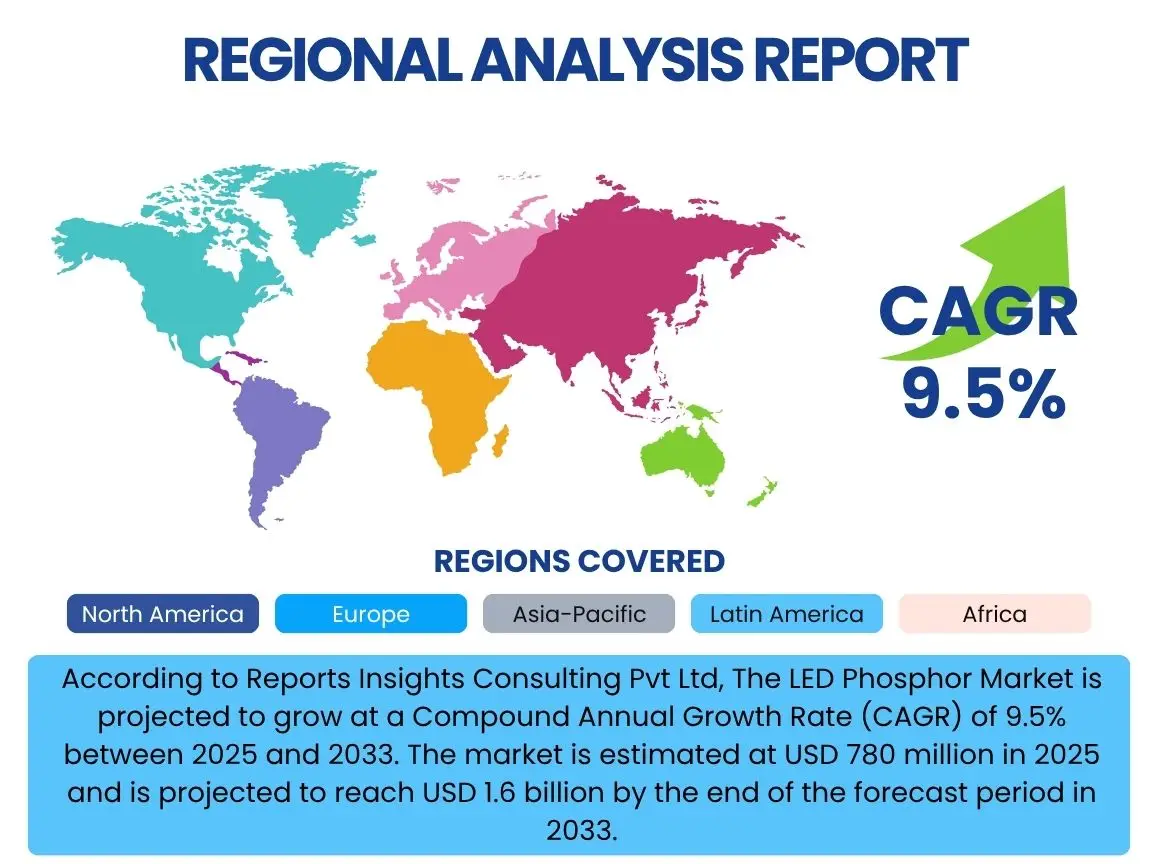

According to Reports Insights Consulting Pvt Ltd, The LED Phosphor Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 9.5% between 2025 and 2033. The market is estimated at USD 780 million in 2025 and is projected to reach USD 1.6 billion by the end of the forecast period in 2033.

Key LED Phosphor Market Trends & Insights

User queries regarding the LED phosphor market frequently center on technological evolution, material innovation, and application diversification. Common questions include how new phosphor materials are impacting LED performance, the role of quantum dots, and the shift towards tunable and smart lighting solutions. There is significant interest in understanding the ongoing evolution of phosphor formulations to meet stringent requirements for efficiency, color rendition, and stability across various emerging applications, beyond traditional general lighting.

The market is witnessing a profound shift towards high-performance and specialty phosphors that enable superior light quality and energy efficiency. Demand for customized spectral output for specific applications, such as horticultural lighting and medical devices, is driving innovation. Furthermore, the integration of advanced manufacturing techniques is enhancing the scalability and cost-effectiveness of these specialized materials, positioning them for broader adoption in next-generation illumination and display technologies.

- Shift towards Quantum Dot (QD) and Perovskite phosphors for wider color gamut and higher efficiency in displays.

- Increasing adoption of tunable white and full-spectrum phosphors for human-centric lighting and specialized applications.

- Development of high-temperature stability and reliability phosphors for automotive and industrial lighting.

- Growing focus on environmentally friendly and rare-earth-free phosphor materials to address supply chain concerns and sustainability goals.

- Miniaturization of LED devices driving demand for smaller, more efficient phosphor particles and advanced coating technologies.

AI Impact Analysis on LED Phosphor

Common user questions regarding AI's impact on the LED phosphor domain revolve around its potential to accelerate material discovery, optimize manufacturing processes, and predict performance characteristics. Users are keen to understand how artificial intelligence and machine learning algorithms can reduce research and development cycles, enhance quality control, and enable the design of novel phosphor compositions with unprecedented properties. Concerns often include data privacy, the cost of AI integration, and the need for specialized expertise.

AI's influence is transforming traditional material science approaches by leveraging vast datasets to identify patterns and correlations that human researchers might miss. This enables a more systematic and efficient exploration of the complex chemical space for new phosphors, optimizing synthesis parameters, and predicting luminescent properties. Furthermore, AI-driven simulations and predictive modeling can significantly cut down on experimental trials, leading to faster market introduction of advanced LED phosphor solutions and enhancing overall operational efficiency for manufacturers.

- AI-driven acceleration of new phosphor material discovery and optimization of synthesis parameters.

- Machine learning algorithms for predictive modeling of phosphor performance, stability, and color characteristics.

- Automation and quality control enhancement in phosphor manufacturing through AI-powered vision systems and data analytics.

- Optimization of supply chain and inventory management for raw materials used in phosphor production.

- AI-enabled customization of phosphor formulations for specific application requirements, leading to tailored lighting solutions.

Key Takeaways LED Phosphor Market Size & Forecast

User inquiries about key takeaways from the LED phosphor market size and forecast consistently highlight growth drivers, emerging opportunities, and strategic implications for stakeholders. There is a strong interest in understanding which application segments will experience the most substantial growth, the regional dynamics influencing market expansion, and the long-term viability of current material technologies. Users seek concise summaries of the market's trajectory and the critical factors that will shape its future development.

The market is poised for robust expansion, primarily fueled by the ubiquitous adoption of LED technology across diverse sectors and the continuous innovation in phosphor materials enhancing LED performance. While general lighting remains a significant segment, the disproportionate growth in niche applications like high-definition displays, automotive lighting, and specialized horticulture presents lucrative opportunities. Strategic focus on R&D for next-generation phosphors, sustainability in material sourcing, and efficient manufacturing processes will be paramount for competitive advantage and sustainable growth in this dynamic market.

- The LED Phosphor market is characterized by consistent high growth, driven by LED penetration in various industries.

- Significant growth segments include high-performance display backlighting (Mini/Micro-LED), automotive, and horticultural lighting, demanding specialized phosphors.

- Asia Pacific is projected to remain the dominant market due to robust manufacturing capabilities and high adoption rates of LED products.

- Technological advancements in Quantum Dots and other advanced phosphors are critical for future market expansion and competitive differentiation.

- Sustainability and material efficiency are becoming increasingly important factors influencing market trends and product development.

LED Phosphor Market Drivers Analysis

The LED Phosphor market is primarily propelled by the escalating global demand for energy-efficient and high-quality lighting solutions. The widespread adoption of LED technology across residential, commercial, and industrial sectors is creating a continuous need for advanced phosphor materials that enhance light output, color rendition, and overall LED performance. Furthermore, stringent energy efficiency regulations and increasing consumer awareness regarding sustainable lighting options are compelling manufacturers to integrate more advanced and efficient LED components, thereby directly boosting the demand for phosphors.

Beyond general illumination, the proliferation of sophisticated display technologies, including LCDs, OLEDs, and the emerging Mini-LED and Micro-LED displays, is a significant driver. These applications require phosphors that can deliver a wider color gamut, higher brightness, and improved contrast, leading to intensive research and development in quantum dot technology and other narrow-band emitting phosphors. The automotive sector's shift towards LED headlights and interior lighting, along with the burgeoning horticultural lighting market, also contribute substantially to the market's expansion by demanding specialized phosphor formulations tailored to specific spectral requirements.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing Demand for Energy-Efficient Lighting | +2.5% | Global, particularly Europe and North America | Short to Mid-term (2025-2029) |

| Advancements in Display Technologies (e.g., Mini-LED, Micro-LED) | +2.0% | Asia Pacific, North America | Mid-term (2027-2033) |

| Increasing Adoption of LEDs in Automotive Lighting | +1.5% | Europe, North America, China | Mid to Long-term (2026-2033) |

| Expansion of Horticultural and Specialty Lighting | +1.0% | North America, Europe, Israel | Mid to Long-term (2028-2033) |

| Technological Innovation in Phosphor Materials (e.g., Quantum Dots) | +2.5% | Global | Short to Long-term (2025-2033) |

LED Phosphor Market Restraints Analysis

Despite robust growth, the LED Phosphor market faces certain restraints that could impede its full potential. One significant challenge is the volatility in the prices of rare earth elements, which are crucial raw materials for many high-performance phosphors. Geopolitical tensions and supply chain disruptions can lead to unpredictable price fluctuations and availability issues, impacting manufacturing costs and profitability for phosphor producers. This reliance on a limited number of suppliers for critical materials introduces an element of risk to the market.

Another restraint stems from the continuous innovation within the LED industry itself, which sometimes introduces alternative light conversion technologies or optimizes chip designs that reduce the overall amount of phosphor required per LED unit. While this reflects efficiency gains, it can potentially constrain demand growth for phosphors in the long run. Furthermore, the high initial investment required for advanced phosphor research and development, coupled with intellectual property challenges and stringent performance requirements, can deter new entrants and limit the pace of diversified product development, especially for niche applications requiring bespoke phosphor formulations.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Volatility in Rare Earth Element Prices | -1.2% | Global, especially China (supply), Europe/North America (demand) | Short to Mid-term (2025-2030) |

| High Research & Development Costs | -0.8% | Global | Long-term (2025-2033) |

| Intense Competition and Price Pressure from Commoditization | -1.0% | Asia Pacific | Short to Mid-term (2025-2029) |

| Alternative Light Conversion Technologies | -0.5% | Global | Long-term (2030-2033) |

| Intellectual Property and Patent Litigation | -0.7% | North America, Europe, Japan | Mid-term (2027-2033) |

LED Phosphor Market Opportunities Analysis

The LED Phosphor market is ripe with opportunities driven by several evolving technological and application landscapes. The most prominent opportunity lies in the continued development and commercialization of next-generation phosphor materials, such as quantum dots and perovskites. These materials offer unprecedented control over spectral output, enabling superior color quality, higher luminous efficacy, and enhanced energy efficiency, which are crucial for high-end display technologies and specialized lighting applications. Investment in these areas promises significant returns as industries seek more advanced illumination solutions.

Furthermore, the expansion into niche and specialty lighting markets presents substantial avenues for growth. Horticultural lighting, medical lighting (e.g., phototherapy, surgical lamps), and sophisticated automotive lighting systems are increasingly relying on precisely engineered phosphor solutions to meet specific spectral requirements. The demand for tunable white light, human-centric lighting, and smart lighting systems also opens up new design possibilities for phosphors that can dynamically adjust color temperature and intensity. Lastly, the push for sustainable and circular economy practices creates opportunities for developing rare-earth-free phosphors and improving recycling processes for existing phosphor materials, aligning with global environmental objectives and reducing reliance on volatile raw material supplies.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development of Advanced Quantum Dot and Perovskite Phosphors | +2.8% | Global, particularly North America, Europe, Asia Pacific | Mid to Long-term (2026-2033) |

| Expansion into Horticultural and Medical Lighting | +1.7% | North America, Europe, Israel, Japan | Mid-term (2027-2032) |

| Growth of Tunable White and Human-Centric Lighting | +1.5% | Europe, North America, Japan | Mid to Long-term (2028-2033) |

| Development of Rare-Earth-Free and Sustainable Phosphors | +1.0% | Global | Long-term (2030-2033) |

| Integration with Smart Lighting Systems and IoT | +1.3% | Global Urban Centers | Mid-term (2026-2031) |

LED Phosphor Market Challenges Impact Analysis

The LED Phosphor market faces several significant challenges that necessitate strategic responses from industry players. One primary concern is the inherent performance degradation of phosphors over time, particularly under high operating temperatures and intense light flux within LED packages. This degradation can lead to color shift and reduced luminous efficacy, impacting the longevity and perceived quality of LED products. Addressing this requires continuous innovation in material stability and encapsulation technologies, which adds to research and development costs.

Another challenge is the complex manufacturing process involved in producing high-quality phosphors, requiring precise control over particle size, morphology, and chemical composition to achieve desired optical properties. Scaling up production while maintaining consistency and cost-effectiveness remains a hurdle, especially for novel materials. Furthermore, environmental regulations concerning certain heavy metals or rare-earth processing by-products pose compliance challenges and drive the need for greener synthesis methods. Intense market competition and the commoditization of standard phosphors also pressure profit margins, pushing manufacturers to differentiate through superior performance or cost efficiency.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Performance Degradation and Thermal Stability Issues | -1.5% | Global | Short to Mid-term (2025-2030) |

| High Manufacturing Complexity and Quality Control | -1.0% | Asia Pacific (production centers) | Short-term (2025-2028) |

| Supply Chain Disruptions and Raw Material Sourcing | -1.2% | Global | Short-term (2025-2027) |

| Environmental Regulations and Sustainability Compliance | -0.8% | Europe, North America, China | Mid to Long-term (2026-2033) |

| Market Saturation in General Lighting Segment | -0.7% | Global | Mid-term (2027-2031) |

LED Phosphor Market - Updated Report Scope

This comprehensive report delves into the intricate dynamics of the global LED Phosphor market, offering a detailed analysis of market size, trends, drivers, restraints, opportunities, and challenges across various segments and key regions. It provides an in-depth examination of the technological advancements shaping the industry, including the emergence of quantum dot and next-generation phosphor materials, and their impact on diverse applications from general lighting to advanced displays and specialty illumination. The report's scope extends to a strategic assessment of the competitive landscape, profiling leading players and offering actionable insights for stakeholders navigating this evolving market.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 780 million |

| Market Forecast in 2033 | USD 1.6 billion |

| Growth Rate | 9.5% |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Global Phosphor Solutions, Innovate Lumina Materials, Precision Optoelectronics, Bright Future Chemicals, Advanced Light Components, EcoLume Technologies, Quantum Dot Innovators, Spectral Dynamics Corp, NeoLux Materials, OptiGlow Industries, Vivid Photonics, ChromaTech Solutions, Radiant Materials Group, ElectroLuminescent Inc., Synergy Light Chemicals, UniBright Materials, Purity Phosphor Innovations, Lumitech Solutions, NextGen Lighting Materials, EverGlow Chemical |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The LED Phosphor market is meticulously segmented to provide a granular view of its diverse components, enabling a precise understanding of market dynamics across various dimensions. Segmentation by type differentiates between major phosphor compositions such as silicate, garnet, nitride, and the rapidly evolving quantum dot phosphors, each possessing distinct spectral properties and application suitability. This allows for a detailed analysis of how material science advancements are influencing market share and technological adoption.

Further segmentation by application highlights the varied end-uses for LED phosphors, ranging from ubiquitous general lighting to specialized fields like display backlighting, automotive illumination, and the burgeoning horticultural sector. Each application demands specific phosphor characteristics, driving tailored product development and market strategies. End-use industry segmentation provides insight into the major sectors consuming LED phosphors, including consumer electronics, automotive, and commercial sectors, offering a clear picture of market demand drivers from an industry-specific perspective. This multi-faceted segmentation ensures a comprehensive market overview, enabling stakeholders to identify high-growth areas and formulate targeted business strategies.

- By Type: Silicate Phosphor, Garnet Phosphor, Nitride Phosphor, Quantum Dot Phosphor, Halide Phosphor, Others

- By Application: General Lighting, Backlighting Units (BLUs) for Displays, Automotive Lighting, Horticultural Lighting, Medical Lighting, Specialty Lighting

- By End-Use Industry: Consumer Electronics, Automotive, Residential, Commercial, Industrial, Healthcare, Agriculture

Regional Highlights

- Asia Pacific (APAC): Dominates the global LED Phosphor market due to its robust manufacturing base for LEDs, displays, and consumer electronics, coupled with high demand from countries like China, Japan, and South Korea. Continuous investments in R&D and mass production capabilities further solidify its leading position.

- North America: A significant market driven by technological innovation, increasing adoption of smart lighting solutions, and strong demand from the automotive and specialty lighting sectors. The presence of key R&D centers and early adoption of advanced display technologies contribute to its growth.

- Europe: Characterized by stringent energy efficiency regulations and a strong emphasis on sustainable and human-centric lighting. Countries like Germany, the UK, and France are driving demand for high-quality, efficient, and specialized LED phosphors in both general illumination and automotive applications.

- Latin America: An emerging market with growing infrastructure development and increasing adoption of LED lighting solutions across residential and commercial sectors. While smaller than mature markets, it presents significant long-term growth potential.

- Middle East & Africa (MEA): Shows promising growth fueled by urbanization, government initiatives for energy conservation, and rising investments in smart city projects. The region is increasingly adopting LED technology for various applications, creating demand for associated phosphor materials.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the LED Phosphor Market.- Global Phosphor Solutions

- Innovate Lumina Materials

- Precision Optoelectronics

- Bright Future Chemicals

- Advanced Light Components

- EcoLume Technologies

- Quantum Dot Innovators

- Spectral Dynamics Corp

- NeoLux Materials

- OptiGlow Industries

- Vivid Photonics

- ChromaTech Solutions

- Radiant Materials Group

- ElectroLuminescent Inc.

- Synergy Light Chemicals

- UniBright Materials

- Purity Phosphor Innovations

- Lumitech Solutions

- NextGen Lighting Materials

- EverGlow Chemical

Frequently Asked Questions

What are LED phosphors primarily used for?

LED phosphors are primarily used to convert the blue or UV light emitted by an LED chip into a broader spectrum of visible light, enabling the creation of white light or specific colors for applications such as general illumination, display backlighting, automotive lighting, and horticultural lighting.

How do different types of phosphors impact LED performance?

Different phosphor types (e.g., YAG, silicate, nitride, quantum dots) impact LED performance by influencing factors like color rendition index (CRI), luminous efficacy, color temperature, and long-term stability. Each type offers distinct advantages for specific application requirements, balancing efficiency with color quality.

What is the role of Quantum Dots in the LED Phosphor market?

Quantum Dots are an advanced type of phosphor that offer superior color purity, narrow emission spectra, and high luminous efficacy, making them ideal for high-end displays (like QLED TVs) and specialized lighting applications where a wide color gamut and precise color control are essential.

What factors influence the lifespan and stability of LED phosphors?

The lifespan and stability of LED phosphors are primarily influenced by operating temperature, light intensity, moisture, and oxygen exposure. High temperatures and intense light can lead to thermal quenching and degradation, necessitating advanced encapsulation techniques and robust phosphor formulations.

What are the key growth drivers for the LED Phosphor market?

Key growth drivers include the increasing global demand for energy-efficient LED lighting, the rapid expansion of advanced display technologies (Mini-LED, Micro-LED), and the growing adoption of LED solutions in niche applications such as automotive, horticultural, and medical lighting.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted