Mobile Sensor Market

Mobile Sensor Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_702487 | Last Updated : July 31, 2025 |

Format : ![]()

![]()

![]()

![]()

Mobile Sensor Market Size

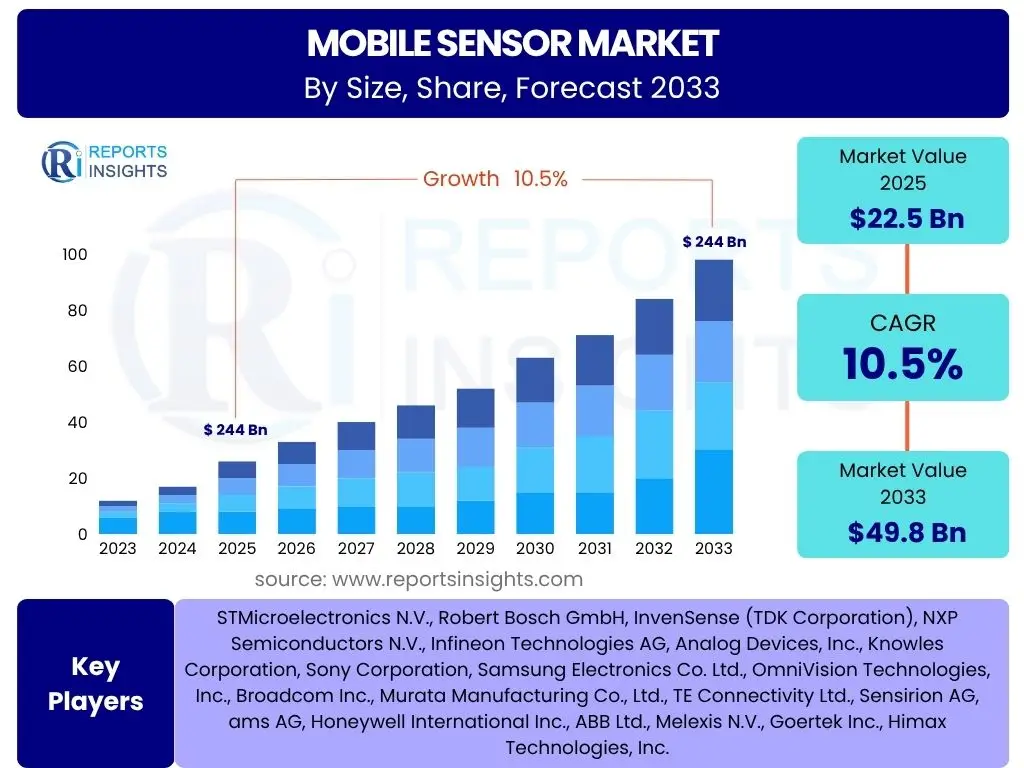

According to Reports Insights Consulting Pvt Ltd, The Mobile Sensor Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 10.5% between 2025 and 2033. The market is estimated at USD 22.5 Billion in 2025 and is projected to reach USD 49.8 Billion by the end of the forecast period in 2033.

Key Mobile Sensor Market Trends & Insights

The mobile sensor market is experiencing significant evolution driven by continuous innovation in smart devices and the expanding Internet of Things (IoT ecosystem. Key user questions often revolve around how miniaturization, increased integration capabilities, and advanced functionalities like AI integration are shaping the industry. Consumers and businesses alike are seeking to understand the progression of sensor technology beyond traditional accelerometers and gyroscopes to more sophisticated environmental, biometric, and health monitoring applications.

Another area of interest concerns the diversification of mobile sensor applications. While smartphones remain a dominant driver, the growth in wearables, smart home devices, automotive systems, and medical diagnostics powered by mobile sensor technology indicates a broad market expansion. Users are keen to know about the transition towards ultra-low power consumption, enhanced accuracy, and the capability of sensors to perform complex tasks at the edge, reducing reliance on cloud processing.

Furthermore, the convergence of multiple sensor types into single, compact modules, often referred to as sensor fusion, is a significant trend. This integration allows for more precise and reliable data collection, improving user experience in navigation, augmented reality (AR), and contextual awareness features. The continuous drive for smaller, more efficient, and multi-functional sensors is defining the trajectory of this dynamic market.

- Miniaturization and high-density integration of sensor arrays.

- Increased adoption of MEMS (Micro-Electro-Mechanical Systems) technology across diverse applications.

- Growing demand for environmental sensors (e.g., air quality, UV) in mobile devices.

- Advancements in biometric sensors for enhanced security and health monitoring.

- Proliferation of sensor fusion algorithms for improved data accuracy and contextual awareness.

- Expansion into new applications such as smart textiles, ingestible sensors, and industrial IoT.

- Development of ultra-low power sensors for extended battery life in portable devices.

AI Impact Analysis on Mobile Sensor

Artificial Intelligence (AI) is profoundly transforming the mobile sensor landscape, with common user inquiries focusing on how AI enhances sensor capabilities, processes data more efficiently, and enables new intelligent applications. The integration of AI, particularly machine learning algorithms, allows mobile sensors to move beyond simple data collection to performing complex analysis, pattern recognition, and predictive tasks directly on the device (edge AI). This reduces latency, conserves bandwidth, and enhances data privacy by minimizing the need for constant cloud connectivity.

AI's influence is evident in several aspects, including improved sensor accuracy through calibration and noise reduction, smart power management that optimizes sensor activity based on contextual needs, and the ability to interpret complex environmental and biometric data. For instance, AI algorithms can differentiate between subtle movements for precise gesture control, analyze voice patterns for advanced authentication, or interpret vital signs for early health anomaly detection. This transition from passive data capture to active, intelligent sensing is a major shift.

Moreover, AI is fostering the development of "smart sensors" that can learn and adapt over time, improving their performance and relevance to user behavior or environmental conditions. This includes AI-driven sensor fusion, where data from multiple sensors is intelligently combined to create a more comprehensive and accurate understanding of the surrounding environment or user state. The synergy between AI and mobile sensors is unlocking unprecedented levels of contextual awareness and personalized user experiences.

- Enhanced sensor data processing and interpretation through edge AI.

- Improved accuracy and noise reduction via AI-powered calibration algorithms.

- Intelligent power management for optimizing sensor activity and battery life.

- Enabling advanced contextual awareness and predictive capabilities in mobile devices.

- Facilitating complex sensor fusion for multi-modal data analysis.

- Development of adaptive and learning sensors that improve performance over time.

Key Takeaways Mobile Sensor Market Size & Forecast

The Mobile Sensor market is poised for robust growth, driven primarily by the relentless expansion of the smartphone ecosystem and the accelerating adoption of IoT devices across various sectors. User questions frequently highlight the significance of miniaturization and cost-effectiveness in enabling the widespread deployment of these sensors, recognizing them as critical factors for market penetration. The forecast indicates sustained demand, not just from traditional consumer electronics but increasingly from emerging applications that leverage advanced sensing capabilities for greater automation and intelligence.

A key takeaway from the market forecast is the substantial investment in research and development aimed at improving sensor performance, reducing power consumption, and expanding functional capabilities. This innovation cycle is expected to continually introduce new sensor types and improve existing ones, broadening their addressable market. The shift towards integrating multiple sensors into compact modules, often with embedded AI, underscores the industry's focus on delivering comprehensive and intelligent sensing solutions.

Furthermore, the market's trajectory is strongly influenced by the growth in health and fitness wearables, smart homes, and autonomous vehicles, all of which are becoming significant consumers of mobile sensor technology. These sectors demand highly reliable, accurate, and energy-efficient sensors, pushing manufacturers to innovate. The projected market value reflects a high degree of confidence in the continued technological advancements and the ever-growing utility of mobile sensors in shaping future digital experiences.

- Strong CAGR indicates significant expansion driven by diverse application areas.

- Technological advancements in miniaturization and power efficiency are key enablers.

- Growing demand from IoT, automotive, and healthcare sectors supplements smartphone market.

- Innovation in AI-integrated and multi-functional sensors will be critical for market leadership.

- Asia Pacific is expected to remain a dominant region due to manufacturing and consumer base.

Mobile Sensor Market Drivers Analysis

The proliferation of smartphones globally remains a foundational driver for the mobile sensor market, with each new generation of devices incorporating more sophisticated and numerous sensors for enhanced user experience, security, and functionality. Beyond smartphones, the explosive growth of the Internet of Things (IoT) devices, ranging from smart home appliances to industrial sensors, significantly amplifies demand for compact, efficient, and cost-effective mobile sensing solutions. The inherent need for these devices to perceive and interact with their environment directly translates into higher sensor integration.

Furthermore, advancements in automotive technology, particularly in autonomous and semi-autonomous vehicles, are creating a substantial new market for mobile sensors. These vehicles rely heavily on various sensor types—including accelerometers, gyroscopes, magnetometers, and environmental sensors—for navigation, safety systems, and vehicle control. Similarly, the burgeoning health and fitness wearable industry, coupled with the increasing trend of remote patient monitoring, necessitates the development and integration of highly accurate biometric and activity tracking sensors into compact, mobile form factors.

Lastly, the increasing adoption of augmented reality (AR) and virtual reality (VR) technologies across consumer and enterprise applications is driving innovation in motion tracking and spatial awareness sensors. These applications require high-precision, low-latency sensors to provide immersive and responsive user experiences, contributing directly to the demand for advanced mobile sensor capabilities.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Ubiquitous Smartphone Adoption and Evolution | +1.5% | Global, particularly Asia Pacific | Short-term (2025-2028) |

| Explosive Growth of IoT Devices and Ecosystem | +1.3% | North America, Europe, Asia Pacific | Medium-term (2026-2030) |

| Advancements in Automotive & Autonomous Driving | +1.1% | North America, Europe, Japan, China | Long-term (2029-2033) |

| Rising Demand for Wearables & Health Monitoring Devices | +0.9% | Global | Short to Medium-term (2025-2030) |

| Emergence of AR/VR Technologies | +0.7% | North America, Europe | Long-term (2029-2033) |

Mobile Sensor Market Restraints Analysis

Despite robust growth, the mobile sensor market faces several restraints, prominently including the high costs associated with research and development (R&D) and complex manufacturing processes, particularly for advanced MEMS sensors. Developing new sensor technologies that are smaller, more accurate, and consume less power requires significant upfront investment and specialized expertise, which can limit the entry of new players and slow down innovation in certain niche areas. This challenge is further compounded by the need for stringent quality control and reliability testing for components integrated into critical applications like automotive and medical devices.

Another significant restraint is the increasing market saturation in mature mobile device segments, especially smartphones, which could lead to slowing growth rates for certain types of ubiquitous sensors. As the market matures, the differentiation often shifts from basic sensor inclusion to advanced features, but the sheer volume growth might decelerate. Additionally, issues related to data privacy and security present a growing concern. Mobile sensors collect vast amounts of personal and environmental data, raising questions about how this data is stored, processed, and protected, which can impact consumer trust and lead to stricter regulations.

Furthermore, supply chain complexities, including the reliance on a limited number of specialized raw material suppliers and geopolitical factors affecting trade, can introduce volatility and increase production costs. The global nature of electronic component manufacturing means that disruptions in one region can have ripple effects across the entire supply chain, impacting sensor availability and pricing.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High R&D and Manufacturing Costs | -0.8% | Global | Medium-term (2026-2030) |

| Data Privacy and Security Concerns | -0.7% | Europe, North America | Ongoing |

| Supply Chain Volatility and Geopolitical Risks | -0.6% | Global | Short to Medium-term (2025-2028) |

| Market Saturation in Mature Mobile Segments | -0.5% | Developed Economies | Long-term (2029-2033) |

| Interoperability and Standardization Challenges | -0.4% | Global | Ongoing |

Mobile Sensor Market Opportunities Analysis

The mobile sensor market is rich with opportunities, particularly in the realm of emerging applications that leverage advanced sensing capabilities. The growing integration of sensors into industrial IoT (IIoT) for predictive maintenance, asset tracking, and operational efficiency presents a significant growth avenue. These applications require robust, reliable, and often ruggedized mobile sensors capable of operating in harsh environments, creating a demand for specialized products beyond consumer-grade offerings.

Another compelling opportunity lies in the continuous innovation within the healthcare sector, moving beyond simple fitness trackers to sophisticated medical-grade wearables and implantable devices. These applications demand higher accuracy, reliability, and regulatory compliance, offering premium market segments for sensor manufacturers. The focus on preventive healthcare and remote diagnostics is fueling the demand for advanced biometric, chemical, and optical sensors that can be integrated into mobile platforms.

Furthermore, the development of smart cities and smart infrastructure initiatives provides a long-term opportunity for environmental and structural monitoring sensors. These sensors can collect data on air quality, traffic flow, structural integrity, and noise levels, enabling more efficient urban management and improved public safety. The increasing convergence of mobile technology with these large-scale public initiatives creates a sustained demand for scalable and interconnected sensor networks.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Expansion into Industrial IoT (IIoT) | +1.2% | North America, Europe, Asia Pacific | Medium to Long-term (2027-2033) |

| Advancements in Medical & Healthcare Wearables | +1.0% | Global | Short to Medium-term (2025-2030) |

| Development of Smart Cities and Infrastructure | +0.9% | Asia Pacific, Europe, Middle East | Long-term (2029-2033) |

| Integration with Next-Gen Consumer Electronics (AR/VR, Smart Home) | +0.8% | North America, Asia Pacific | Medium-term (2026-2030) |

| Demand for Energy Harvesting and Ultra-Low Power Sensors | +0.7% | Global | Ongoing |

Mobile Sensor Market Challenges Impact Analysis

The mobile sensor market faces several operational and technological challenges that could impede its growth. One significant hurdle is achieving optimal power efficiency without compromising sensor performance, especially as mobile devices demand longer battery life and integration of more sensors. High power consumption can limit the types and number of sensors that can be effectively deployed in compact, portable devices, directly impacting user experience and device design. Manufacturers are constantly striving for breakthroughs in low-power sensor design and energy harvesting techniques.

Another challenge is ensuring interoperability and standardization across a diverse ecosystem of devices, platforms, and manufacturers. With numerous sensor types and communication protocols, achieving seamless integration and data exchange can be complex, hindering widespread adoption and creating fragmentation in the market. The lack of universal standards for sensor interfaces and data formats can increase development costs and time for device manufacturers.

Furthermore, the complexity of sensor fusion algorithms, which combine data from multiple sensors to provide more accurate and reliable insights, presents a significant technical challenge. Developing robust algorithms that can effectively process noisy, incomplete, or conflicting data from different sensor types requires advanced expertise in signal processing, machine learning, and domain-specific knowledge. Ensuring the security of sensor data, from collection to transmission and storage, is also a growing concern, as breaches can lead to privacy violations and compromised device integrity.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Achieving Ultra-Low Power Consumption | -0.5% | Global | Ongoing |

| Interoperability and Standardization Issues | -0.4% | Global | Ongoing |

| Complexity of Sensor Fusion Algorithms | -0.3% | Global | Ongoing |

| Ensuring Data Security and Privacy | -0.6% | Europe, North America | Ongoing |

| High Cost of Advanced Sensor Materials and Manufacturing | -0.4% | Global | Short to Medium-term (2025-2030) |

Mobile Sensor Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the global mobile sensor market, offering insights into its current size, historical growth, and future projections. The report delineates key market trends, analyzes the impact of artificial intelligence, identifies primary drivers, restraints, opportunities, and challenges affecting market expansion. It segments the market by sensor type, application, technology, and end-use, providing detailed regional breakdowns to assist stakeholders in strategic decision-making and understanding market dynamics.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 22.5 Billion |

| Market Forecast in 2033 | USD 49.8 Billion |

| Growth Rate | 10.5% |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | STMicroelectronics N.V., Robert Bosch GmbH, InvenSense (TDK Corporation), NXP Semiconductors N.V., Infineon Technologies AG, Analog Devices, Inc., Knowles Corporation, Sony Corporation, Samsung Electronics Co. Ltd., OmniVision Technologies, Inc., Broadcom Inc., Murata Manufacturing Co., Ltd., TE Connectivity Ltd., Sensirion AG, ams AG, Honeywell International Inc., ABB Ltd., Melexis N.V., Goertek Inc., Himax Technologies, Inc. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The mobile sensor market is comprehensively segmented to provide a granular understanding of its diverse components and evolving applications. This segmentation allows for precise analysis of market dynamics within specific product categories, technological advancements, and end-use industries, enabling stakeholders to identify high-growth areas and tailor their strategies effectively. The market is broadly categorized by sensor type, underlying technology, and various application and end-use sectors, reflecting the ubiquitous presence and functional specialization of mobile sensors.

- By Type:

- Image Sensors

- Accelerometers

- Gyroscopes

- Magnetometers

- Pressure Sensors

- Temperature Sensors

- Humidity Sensors

- Proximity Sensors

- Ambient Light Sensors

- Fingerprint Sensors

- Other Biometric Sensors

- Chemical Sensors

- Gas Sensors

- Acoustic Sensors

- By Technology:

- MEMS (Micro-Electro-Mechanical Systems)

- CMOS (Complementary Metal-Oxide-Semiconductor)

- NEMS (Nano-Electro-Mechanical Systems)

- Other Technologies

- By Application:

- Consumer Electronics

- Automotive

- Healthcare

- Industrial

- Robotics & Drones

- Smart Home & Building

- Environmental Monitoring

- Security & Surveillance

- Other Applications

- By End-Use Industry:

- Smartphones

- Tablets

- Wearables

- AR/VR Devices

- IoT Devices

- Automotive Infotainment & ADAS

- Medical Devices

- Industrial Automation

- Smart City Infrastructure

Regional Highlights

The global mobile sensor market exhibits distinct regional dynamics, influenced by technological adoption rates, manufacturing capabilities, and market maturity. Asia Pacific stands as the largest and fastest-growing region, primarily driven by the colossal consumer electronics manufacturing base in countries like China, South Korea, Japan, and Taiwan, coupled with the immense smartphone user base. This region is also a hub for IoT device production and innovation in smart city initiatives, fueling demand for a wide array of mobile sensors across various applications.

North America and Europe represent mature markets characterized by significant R&D investments, high adoption of advanced technologies like AI and AR/VR, and strong growth in niche segments such as automotive, healthcare, and industrial IoT. These regions emphasize high-value, high-precision sensors and sophisticated sensor fusion solutions. Government initiatives supporting smart infrastructure and connected vehicle technologies further contribute to market expansion in these areas.

Latin America, the Middle East, and Africa (MEA) are emerging markets for mobile sensors, experiencing growth primarily due to increasing smartphone penetration, expanding internet connectivity, and rising investments in smart cities and industrial digitalization projects. While starting from a smaller base, these regions offer significant future growth potential as digital transformation accelerates and disposable incomes rise, leading to greater adoption of smart devices and sensor-enabled solutions.

- Asia Pacific: Dominant market share and fastest growth attributed to vast consumer electronics manufacturing, high smartphone penetration, and rapid adoption of IoT and smart city technologies in countries such as China, India, Japan, and South Korea.

- North America: Strong market driven by early technology adoption, significant R&D investments, robust automotive and healthcare sectors, and a high concentration of key technology innovators and end-users.

- Europe: Characterized by stringent regulatory standards, advanced manufacturing capabilities, and increasing focus on industrial IoT, smart homes, and autonomous driving, particularly in Germany, France, and the UK.

- Latin America: Emerging market with increasing smartphone penetration, growing internet access, and rising investments in smart infrastructure and consumer electronics, especially in Brazil and Mexico.

- Middle East and Africa (MEA): Projected significant growth due to ongoing smart city developments, diversification of economies away from oil, and increasing consumer adoption of mobile and connected devices, particularly in UAE, Saudi Arabia, and South Africa.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Mobile Sensor Market.- STMicroelectronics N.V.

- Robert Bosch GmbH

- InvenSense (TDK Corporation)

- NXP Semiconductors N.V.

- Infineon Technologies AG

- Analog Devices, Inc.

- Knowles Corporation

- Sony Corporation

- Samsung Electronics Co. Ltd.

- OmniVision Technologies, Inc.

- Broadcom Inc.

- Murata Manufacturing Co., Ltd.

- TE Connectivity Ltd.

- Sensirion AG

- ams AG

- Honeywell International Inc.

- ABB Ltd.

- Melexis N.V.

- Goertek Inc.

- Himax Technologies, Inc.

Frequently Asked Questions

What are the primary types of mobile sensors?

Mobile sensors encompass a wide range, including accelerometers, gyroscopes, magnetometers, ambient light sensors, proximity sensors, pressure sensors, temperature and humidity sensors, image sensors, and various biometric sensors like fingerprint and heart rate monitors. These are typically based on MEMS or CMOS technologies.

How is Artificial Intelligence impacting mobile sensor technology?

AI significantly enhances mobile sensors by enabling advanced data processing at the edge, improving accuracy through intelligent calibration, optimizing power consumption, and facilitating complex sensor fusion. This allows for more sophisticated contextual awareness, predictive capabilities, and personalized user experiences directly on the device.

What are the key applications driving the mobile sensor market?

The mobile sensor market is primarily driven by applications in consumer electronics, especially smartphones, wearables, and AR/VR devices. Other significant drivers include automotive systems (ADAS, autonomous driving), healthcare (wearables, remote monitoring), industrial IoT, smart home devices, and environmental monitoring.

What are the main challenges faced by the mobile sensor market?

Key challenges include achieving ultra-low power consumption for extended battery life, ensuring interoperability and standardization across diverse devices, managing the complexity of sensor fusion algorithms, addressing data security and privacy concerns, and mitigating high R&D and manufacturing costs for advanced sensors.

Which regions are leading the growth in the mobile sensor market?

Asia Pacific is the leading region in terms of market size and growth, driven by its extensive consumer electronics manufacturing base and large user population. North America and Europe also hold significant market shares, characterized by high innovation and adoption rates in advanced applications like automotive and healthcare.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted