Mobile Logistic Robot Market

Mobile Logistic Robot Market Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_706968 | Last Updated : September 08, 2025 |

Format : ![]()

![]()

![]()

![]()

Mobile Logistic Robot Market Size

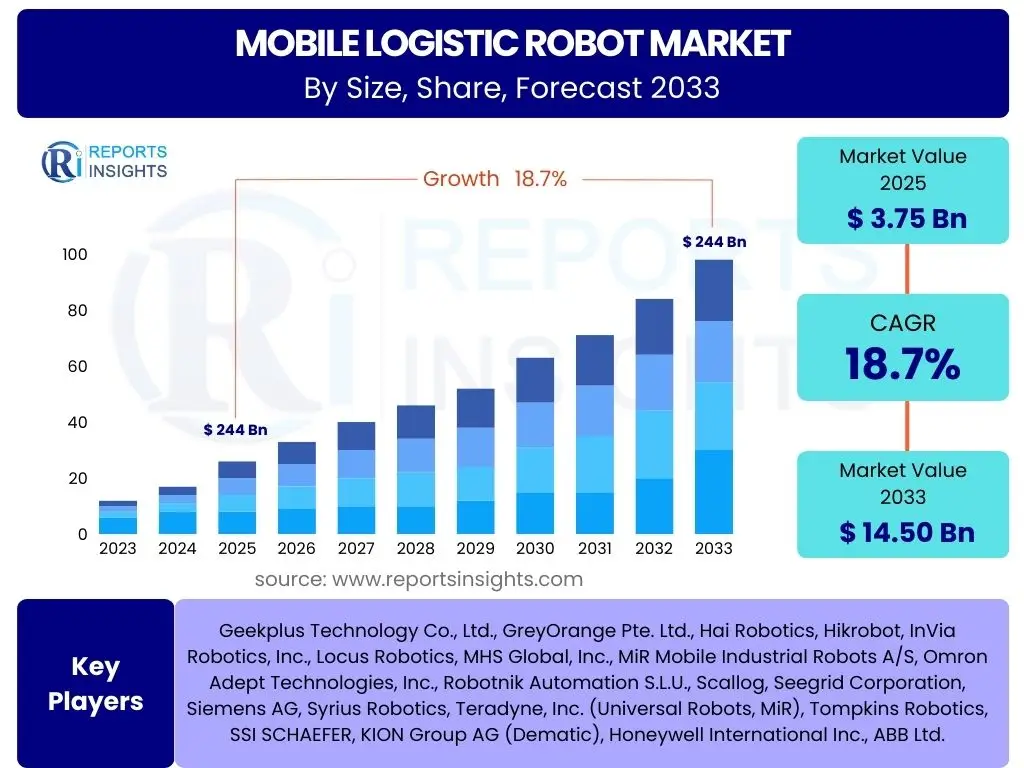

According to Reports Insights Consulting Pvt Ltd, The Mobile Logistic Robot Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 18.7% between 2025 and 2033. The market is estimated at USD 3.75 Billion in 2025 and is projected to reach USD 14.50 Billion by the end of the forecast period in 2033.

Key Mobile Logistic Robot Market Trends & Insights

The Mobile Logistic Robot market is currently experiencing transformative growth, primarily driven by the escalating demand for automation across various industries, particularly in e-commerce, warehousing, and manufacturing. A significant trend is the shift from traditional Automated Guided Vehicles (AGVs) to more sophisticated Autonomous Mobile Robots (AMRs), which offer greater flexibility, intelligence, and adaptability in dynamic environments. This evolution is enabling businesses to optimize their operational workflows, reduce labor costs, and enhance overall supply chain efficiency, directly addressing the challenges posed by labor shortages and increasing logistical complexities.

Furthermore, the market is characterized by a rapid integration of advanced technologies such as artificial intelligence, machine learning, and advanced sensor fusion, which empower robots with enhanced navigation, predictive capabilities, and collaborative functionalities. The focus is increasingly on solutions that can operate safely alongside human workers, facilitating seamless human-robot collaboration. Additionally, the development of Robot-as-a-Service (RaaS) models is gaining traction, lowering the upfront investment barrier for small and medium-sized enterprises and accelerating the adoption of these robotic solutions across diverse industry verticals, including retail, healthcare, and automotive.

- Transition from AGVs to AMRs for enhanced flexibility and autonomy.

- Increased adoption of cloud-based fleet management systems for optimized operations.

- Rising demand for collaborative mobile robots (cobots) in shared workspaces.

- Integration of advanced sensor technologies for improved navigation and safety.

- Development of modular and scalable robot designs to meet diverse application needs.

- Growing popularity of Robot-as-a-Service (RaaS) models.

- Emphasis on energy efficiency and sustainable robot operations.

- Proactive integration of predictive maintenance capabilities.

AI Impact Analysis on Mobile Logistic Robot

Artificial intelligence is profoundly reshaping the capabilities and applications of mobile logistic robots, moving them beyond mere programmed automation to intelligent, adaptive systems. Common user inquiries often revolve around how AI enables robots to handle complex, unstructured environments, make real-time decisions, and learn from their operational experiences. AI algorithms enhance navigation by allowing robots to dynamically map their surroundings, identify obstacles, and reroute paths instantaneously, significantly improving efficiency and safety in busy warehouses or factory floors. This real-time adaptability is crucial for optimal performance in unpredictable logistical scenarios.

Moreover, AI contributes significantly to predictive analytics within these systems, allowing robots to anticipate maintenance needs, optimize battery usage, and manage workload distribution more effectively, thus minimizing downtime and extending operational lifespans. Users also seek to understand AI's role in improving human-robot interaction, ensuring that robots can intelligently interpret human cues and collaborate seamlessly without requiring extensive programming. The integration of machine learning allows these robots to continuously refine their performance, learning from data patterns and adapting to new tasks or environmental changes, which is a major concern and expectation for businesses looking to future-proof their automation investments and maximize their return on investment.

- Enhanced autonomous navigation and path planning through AI-powered SLAM (Simultaneous Localization and Mapping).

- Intelligent decision-making capabilities for task prioritization and resource allocation.

- Predictive maintenance algorithms for proactive robot upkeep and reduced downtime.

- Optimized fleet management through AI-driven traffic control and task assignment.

- Improved object recognition and manipulation for diverse item handling.

- Adaptive learning from operational data to continually enhance performance and efficiency.

- Facilitation of more intuitive and safer human-robot collaboration.

Key Takeaways Mobile Logistic Robot Market Size & Forecast

Analysis of market inquiries reveals a strong interest in understanding the core growth drivers and strategic implications of the mobile logistic robot market's expansion. Users frequently ask about the primary factors fueling this rapid growth and what the long-term outlook suggests for investment and operational strategies. The market's robust forecast is underpinned by a confluence of critical factors, including the surging growth of the e-commerce sector, which necessitates highly efficient and scalable fulfillment operations, and the pervasive challenge of labor shortages in traditional logistics roles. This creates an urgent demand for automated solutions that can augment human capabilities and ensure operational continuity.

Furthermore, the continuous technological advancements in robotics, AI, and sensor technologies are not just incremental improvements but transformative leaps that enable robots to perform more complex, precise, and autonomous tasks than ever before. This technological maturation makes mobile logistic robots an increasingly viable and attractive investment for businesses seeking to reduce operational costs, enhance safety, and significantly boost throughput and accuracy in their supply chains. The market is poised for sustained expansion, offering substantial opportunities for both technology providers and end-users looking to gain a competitive edge through advanced automation.

- The market is experiencing substantial and sustained growth, driven by fundamental shifts in global logistics and manufacturing.

- E-commerce expansion and rising labor costs are primary catalysts for accelerated adoption of mobile logistic robots.

- Technological innovations, particularly in AI and navigation, are making robots more versatile and cost-effective.

- Significant investment opportunities exist for technology developers and integrators.

- Increased operational efficiency, safety, and cost reduction are key benefits driving widespread enterprise adoption.

- The market is set for long-term expansion, with increasing penetration across diverse industrial and commercial sectors.

- Strategic partnerships and mergers are becoming more common as companies seek to expand capabilities and market reach.

Mobile Logistic Robot Market Drivers Analysis

The global mobile logistic robot market is propelled by a confluence of powerful macroeconomic and technological forces. The exponential growth of the e-commerce industry, particularly post-pandemic, has created an unprecedented demand for rapid and efficient order fulfillment, which conventional manual processes struggle to meet. This necessitates the adoption of automation solutions like mobile logistic robots to manage vast inventory, optimize warehouse layouts, and accelerate delivery timelines. Simultaneously, a persistent global labor shortage in logistics and manufacturing sectors, coupled with rising labor costs, is pushing businesses to invest in robotics to maintain operational continuity and reduce overheads.

Furthermore, the broader embrace of Industry 4.0 principles and smart factory initiatives drives the integration of advanced automation and data-driven decision-making within industrial processes. Mobile logistic robots, with their ability to connect seamlessly within networked environments and contribute to real-time data collection, are foundational to achieving the efficiencies promised by these paradigms. The continuous innovation in robot capabilities, including enhanced payload capacities, improved navigation accuracy, and increased safety features, further bolsters their appeal, offering compelling solutions for businesses striving for greater productivity and resilience in their supply chains.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Exponential Growth of E-commerce | +2.2% | Global, especially Asia Pacific & North America | Short to Mid-term |

| Increasing Labor Shortages and Rising Wages | +1.9% | North America, Europe, Developed Asia | Short to Mid-term |

| Accelerated Adoption of Industry 4.0 and Smart Factories | +1.8% | Europe, North America, Japan, China | Mid to Long-term |

| Demand for Enhanced Operational Efficiency and Cost Reduction | +2.5% | Global, all industrial sectors | Short to Mid-term |

| Advancements in Robotics and AI Technology | +1.5% | Global, technology hubs | Ongoing, Long-term |

| Focus on Workplace Safety and Ergonomics | +1.0% | North America, Europe | Mid-term |

| Expansion of Automated Warehousing and Fulfillment Centers | +2.0% | Global, particularly urban areas | Short to Mid-term |

Mobile Logistic Robot Market Restraints Analysis

Despite the significant growth trajectory, the mobile logistic robot market faces several notable restraints that could temper its expansion. One of the primary barriers is the high initial capital investment required for purchasing and implementing these sophisticated robotic systems. This substantial upfront cost can be prohibitive for small and medium-sized enterprises (SMEs) or businesses with limited capital, despite the long-term operational savings. Furthermore, integrating mobile robots into existing legacy infrastructure often presents significant technical complexities, requiring substantial modifications to facilities, IT systems, and operational protocols, which can be both time-consuming and expensive.

Another significant restraint involves the technical complexities associated with their deployment and maintenance. These robots require specialized programming, software integration, and ongoing technical support, which can be challenging for organizations lacking in-house expertise. Safety concerns, particularly regarding human-robot interaction in dynamic environments, also pose a restraint, as robust safety protocols and regulations are still evolving. Additionally, the lack of widespread standardization in robot communication protocols and interoperability can hinder the seamless integration of diverse robotic fleets and limit their scalability across different vendors' solutions, contributing to higher total cost of ownership and slower adoption rates in certain sectors.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Initial Capital Investment | -0.8% | Emerging Economies, SMEs Globally | Short to Mid-term |

| Integration Complexities with Legacy Systems | -0.7% | Mature Industries, Traditional Manufacturers | Mid-term |

| Lack of Standardization and Interoperability Issues | -0.5% | Global, Multi-vendor Environments | Short to Mid-term |

| Technical Skill Gap for Deployment and Maintenance | -0.6% | Emerging Economies, Industries with low tech adoption | Mid-term |

| Concerns Regarding Cybersecurity Threats | -0.4% | Global, all sectors | Ongoing |

Mobile Logistic Robot Market Opportunities Analysis

The mobile logistic robot market is ripe with numerous opportunities for innovation and expansion. A significant avenue for growth lies in the increasing demand for customized robotic solutions tailored to niche applications within specific industries, such as healthcare for medical supply delivery, retail for in-store inventory management, and food & beverage for cold chain logistics. These specialized requirements often demand bespoke robot designs, unique navigation capabilities, or specific payload handling, opening up new market segments for agile manufacturers and solution providers who can offer highly adaptable platforms.

Furthermore, the Robot-as-a-Service (RaaS) model presents a transformative opportunity by democratizing access to advanced robotic solutions. By shifting from a capital expenditure to an operational expenditure model, RaaS reduces the financial barrier for adoption, making high-end mobile robots accessible to a broader range of businesses, including SMEs. This model not only expands the customer base but also ensures that robots are continuously updated and maintained by providers, guaranteeing optimal performance. The ongoing development of advanced sensor technologies, coupled with increasing computational power, also creates opportunities for robots to operate in more complex and dynamic environments, such as outdoor logistics or multi-floor operations, further broadening their applicability and market reach in the coming years.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Expansion into New Industry Verticals (e.g., Healthcare, Retail) | +1.8% | Global, particularly developed economies | Mid to Long-term |

| Growth of Robot-as-a-Service (RaaS) Models | +1.5% | Global, especially advantageous for SMEs | Short to Mid-term |

| Development of Advanced Sensor and Vision Technologies | +1.2% | Global, technology providers | Ongoing |

| Increased Automation in E-grocery and Food Delivery | +1.7% | Urban areas, North America, Europe, Asia Pacific | Short to Mid-term |

| Customization and Niche Application Development | +1.0% | Global, specific industry needs | Mid-term |

| Integration with Cloud Computing and IoT Platforms | +0.9% | Global, large enterprises | Long-term |

Mobile Logistic Robot Market Challenges Impact Analysis

The mobile logistic robot market encounters several significant challenges that necessitate strategic mitigation from manufacturers and integrators. One critical challenge is the seamless integration of new robotic systems with existing legacy infrastructure and diverse operational technologies within facilities. This often requires complex software customization, hardware modifications, and extensive testing, which can be time-consuming and expensive, delaying deployment and return on investment for end-users. Businesses face the hurdle of balancing the promise of automation with the practicalities of adapting their current setups.

Another pressing challenge is the evolving regulatory landscape and the establishment of universally accepted safety standards for mobile robots, especially as they increasingly operate in environments shared with humans. Ensuring robust cybersecurity measures to protect sensitive operational data and prevent malicious attacks on interconnected robotic fleets also remains a significant concern. Furthermore, public perception regarding job displacement and the need for workforce retraining poses a social challenge, requiring careful communication strategies and investment in upskilling programs to ensure a smooth transition and acceptance of automation technologies within the labor force, thus impacting adoption rates and societal integration.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Complex Integration with Existing Infrastructure | -0.9% | Global, large-scale industrial setups | Short to Mid-term |

| Evolving Regulatory Landscape and Safety Standards | -0.7% | Europe, North America, Highly Regulated Industries | Ongoing |

| Data Security and Cybersecurity Threats | -0.6% | Global, all sectors utilizing networked robots | Ongoing |

| Workforce Retraining and Job Displacement Concerns | -0.5% | Global, particularly manufacturing and logistics | Mid-term |

| High Energy Consumption and Battery Management | -0.4% | Global, intensive 24/7 operations | Short to Mid-term |

Mobile Logistic Robot Market - Updated Report Scope

This comprehensive report provides an in-depth analysis of the Mobile Logistic Robot Market, offering crucial insights into its current state, historical performance, and future growth trajectory. It meticulously covers market size estimations, growth forecasts, and a detailed breakdown of market dynamics, including key drivers, restraints, opportunities, and challenges. The report delivers a granular view through extensive segmentation analysis across various robot types, applications, payload capacities, navigation technologies, and end-use industries, providing stakeholders with a complete understanding of market nuances and competitive landscapes. It also highlights regional market performances and profiles key players, enabling strategic decision-making.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 3.75 Billion |

| Market Forecast in 2033 | USD 14.50 Billion |

| Growth Rate | 18.7% |

| Number of Pages | 265 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Geekplus Technology Co., Ltd., GreyOrange Pte. Ltd., Hai Robotics, Hikrobot, InVia Robotics, Inc., Locus Robotics, MHS Global, Inc., MiR Mobile Industrial Robots A/S, Omron Adept Technologies, Inc., Robotnik Automation S.L.U., Scallog, Seegrid Corporation, Siemens AG, Syrius Robotics, Teradyne, Inc. (Universal Robots, MiR), Tompkins Robotics, SSI SCHAEFER, KION Group AG (Dematic), Honeywell International Inc., ABB Ltd. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The mobile logistic robot market is extensively segmented to provide a granular understanding of its diverse components and applications, enabling a more precise analysis of market dynamics and growth opportunities. This segmentation helps identify specific market niches, understand varying technological preferences, and evaluate the demand patterns across different industry verticals. By dissecting the market based on robot type, navigation technology, payload capacity, application, end-use industry, and components, stakeholders can pinpoint high-growth areas, assess competitive landscapes within specific categories, and tailor their strategies to target particular market needs.

This detailed breakdown allows for a comprehensive assessment of how different technological advancements and operational requirements influence market adoption and revenue generation. For instance, the shift from AGVs to AMRs reflects a demand for greater flexibility and intelligence, while the varying payload capacities cater to diverse logistical needs, from light parcel handling to heavy pallet transport. Understanding these segments is crucial for manufacturers to innovate effectively, for investors to identify promising ventures, and for end-users to select the most appropriate robotic solutions for their specific operational challenges, ultimately driving efficient resource allocation and market expansion.

- By Type: Automated Guided Vehicles (AGVs), Autonomous Mobile Robots (AMRs)

- By Navigation Technology: SLAM (Simultaneous Localization and Mapping), Laser Guidance, Vision-based Navigation, Magnetic Tape/Wire Guidance, QR Code/Fiducial Markers

- By Payload Capacity: Up to 100 kg, 101 kg to 500 kg, Above 500 kg

- By Application: Transportation, Palletizing & Depalletizing, Picking & Placing, Assembly, Packaging, Towing

- By End-use Industry: Manufacturing (Automotive, Electronics, Food & Beverages, Pharmaceuticals, Heavy Industries), Logistics & Warehousing, Retail & E-commerce, Healthcare, Chemicals, Others (e.g., Agriculture, Construction)

- By Component: Hardware (Sensors, Actuators & Motors, Controllers, Batteries & Chargers, Chassis & Frame), Software (Navigation & Control Software, Fleet Management Software, AI & Machine Learning Software, Integration Software), Services (Installation & Deployment, Maintenance & Support, Consulting & Training, RaaS - Robot-as-a-Service)

Regional Highlights

Geographic analysis reveals distinct patterns in the adoption and growth of mobile logistic robots worldwide, influenced by varying levels of industrialization, labor costs, and technological infrastructure. North America stands out due to its early adoption of automation, driven by high labor costs and a mature e-commerce market that demands highly efficient fulfillment centers. The region also benefits from a robust ecosystem of robotics innovators and significant investment in R&D, positioning it as a key market for advanced mobile logistic solutions, particularly AMRs.

Europe closely follows, propelled by strong Industry 4.0 initiatives and a focus on smart manufacturing. Countries like Germany, the UK, and France are investing heavily in factory automation and warehouse modernization, spurred by government support for digital transformation and increasing competitiveness pressures. The region shows a strong preference for collaborative robot solutions that integrate seamlessly with existing human workflows, reflecting its emphasis on sustainable and human-centric automation.

Asia Pacific is projected to be the fastest-growing market, largely due to the rapid expansion of manufacturing hubs in China, India, Japan, and South Korea, coupled with an exploding e-commerce sector. Countries like China are not only major consumers but also leading producers of mobile logistic robots, benefiting from vast domestic demand, government incentives for automation, and significant technological advancements. The sheer volume of goods moved and the scale of warehousing operations in this region create immense opportunities for scalable robotic solutions, often at competitive price points.

Latin America and the Middle East & Africa (MEA) are emerging markets for mobile logistic robots, albeit at an earlier stage of adoption. Growth in these regions is primarily driven by increasing foreign direct investment in manufacturing and logistics infrastructure, coupled with a growing awareness of automation benefits. While facing challenges such as initial capital investment barriers and infrastructure limitations, these regions present long-term opportunities as their industrial sectors mature and global supply chains seek diversified, cost-effective operational hubs. The MEA region, in particular, is witnessing increased investment in port automation and new logistics parks, paving the way for future mobile robot deployment.

- North America: Early adopter of advanced automation; high labor costs and mature e-commerce drive demand; significant R&D investment.

- Europe: Strong focus on Industry 4.0 and smart factories; high adoption in automotive and manufacturing; emphasis on safety and collaboration.

- Asia Pacific (APAC): Fastest-growing market due to massive e-commerce expansion and manufacturing hubs (China, Japan, South Korea, India); significant domestic production and technological advancements.

- Latin America: Emerging market with increasing industrialization; growing demand for efficiency in manufacturing and logistics.

- Middle East & Africa (MEA): Nascent market, but increasing investment in infrastructure and logistics hubs (e.g., UAE, Saudi Arabia); long-term growth potential.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Mobile Logistic Robot Market.- Geekplus Technology Co., Ltd.

- GreyOrange Pte. Ltd.

- Hai Robotics

- Hikrobot

- InVia Robotics, Inc.

- Locus Robotics

- MHS Global, Inc.

- MiR Mobile Industrial Robots A/S

- Omron Adept Technologies, Inc.

- Robotnik Automation S.L.U.

- Scallog

- Seegrid Corporation

- Siemens AG

- Syrius Robotics

- Teradyne, Inc. (Universal Robots, MiR)

- Tompkins Robotics

- SSI SCHAEFER

- KION Group AG (Dematic)

- Honeywell International Inc.

- ABB Ltd.

Frequently Asked Questions

What is a mobile logistic robot?

A mobile logistic robot is an autonomous or semi-autonomous machine designed to transport goods, materials, or equipment within warehouses, factories, and other logistical environments. These robots can navigate independently using sensors, cameras, and mapping software, optimizing material flow, reducing human effort, and improving overall operational efficiency.

What are the primary applications of mobile logistic robots?

Mobile logistic robots are predominantly used for internal logistics tasks such as transporting raw materials, work-in-progress, and finished goods in manufacturing plants, moving inventory and parcels within fulfillment centers, and delivering medical supplies in healthcare facilities. They are also increasingly deployed in retail for inventory management and back-of-store operations.

How does Artificial Intelligence (AI) enhance mobile logistic robots?

AI significantly enhances mobile logistic robots by enabling advanced capabilities such as intelligent path planning, real-time obstacle avoidance, predictive maintenance, and optimized fleet management. AI algorithms allow robots to learn from their environment, adapt to dynamic conditions, and make autonomous decisions, leading to greater efficiency, safety, and operational reliability.

What are the key benefits of adopting mobile logistic robots?

The key benefits include significant improvements in operational efficiency, reduced labor costs, enhanced workplace safety by handling repetitive or hazardous tasks, increased throughput and accuracy in material handling, and improved scalability of operations. These robots also offer greater flexibility in adapting to changing production demands and warehouse layouts.

What are the future trends expected in the mobile logistic robot market?

Future trends include continued growth in the adoption of Autonomous Mobile Robots (AMRs) over traditional AGVs, further integration of AI and machine learning for enhanced autonomy, expansion of Robot-as-a-Service (RaaS) models, development of more collaborative robots (cobots) for human-robot interaction, and increased focus on sustainable and energy-efficient designs, alongside broader applications in new industry verticals.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted