Military Shipbuilding and Submarine Market

Military Shipbuilding and Submarine Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_703908 | Last Updated : August 05, 2025 |

Format : ![]()

![]()

![]()

![]()

Military Shipbuilding and Submarine Market Size

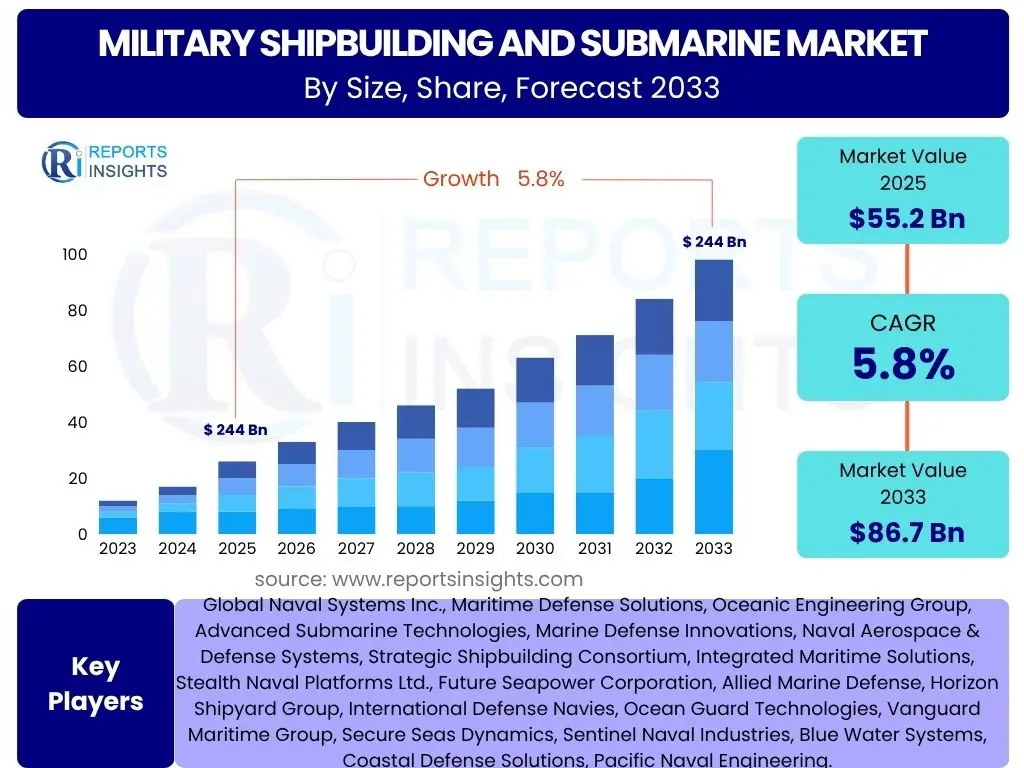

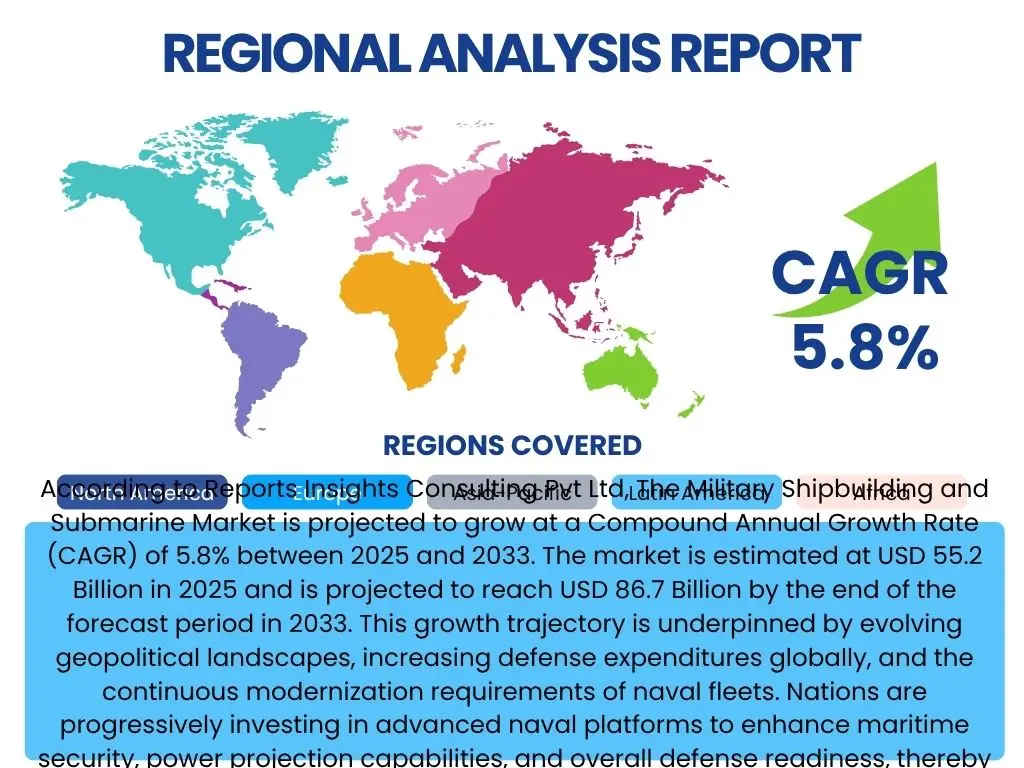

According to Reports Insights Consulting Pvt Ltd, The Military Shipbuilding and Submarine Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.8% between 2025 and 2033. The market is estimated at USD 55.2 Billion in 2025 and is projected to reach USD 86.7 Billion by the end of the forecast period in 2033. This growth trajectory is underpinned by evolving geopolitical landscapes, increasing defense expenditures globally, and the continuous modernization requirements of naval fleets. Nations are progressively investing in advanced naval platforms to enhance maritime security, power projection capabilities, and overall defense readiness, thereby driving market expansion.

The consistent demand for sophisticated naval vessels, including advanced submarines and surface combatants, is a primary catalyst for this market's robust growth. Countries are not only replacing aging fleets but also expanding their naval presence to protect economic interests, secure vital sea lanes, and respond to emergent threats. Technological advancements in shipbuilding, such as automation, stealth capabilities, and integrated combat systems, further contribute to the increased valuation and complexity of new builds, sustaining the market's upward trend through the forecast period.

Key Military Shipbuilding and Submarine Market Trends & Insights

Common user inquiries concerning military shipbuilding and submarine market trends frequently revolve around the adoption of new technologies, the impact of geopolitical shifts on procurement, and the increasing emphasis on autonomous systems. Users are keen to understand how stealth technology, advanced propulsion systems, and digital integration are reshaping naval capabilities, alongside the influence of regional conflicts and global power dynamics on naval fleet development. There is also a significant interest in the shift towards modular designs and multi-mission platforms, reflecting a demand for greater adaptability and cost-effectiveness in naval operations.

A notable trend is the escalating investment in advanced naval capabilities by emerging maritime powers, leading to a more diversified global demand landscape. This includes a focus on enhancing anti-submarine warfare (ASW) capabilities and developing platforms equipped with next-generation missile systems. The drive for greater operational endurance and reduced logistical footprints is also prompting research into more efficient propulsion systems and advanced onboard systems. Furthermore, the imperative for improved cybersecurity within integrated combat systems is becoming paramount, shaping design and development priorities.

- Increased focus on unmanned and autonomous underwater vehicles (UUVs).

- Integration of advanced stealth technologies for enhanced survivability.

- Development of hypersonic missile capabilities for naval platforms.

- Emphasis on modular design and multi-mission capabilities for flexibility.

- Adoption of digital shipbuilding techniques and smart ship concepts.

- Growing demand for nuclear-powered submarines and aircraft carriers.

- Enhancement of anti-submarine warfare (ASW) and anti-access/area denial (A2/AD) capabilities.

AI Impact Analysis on Military Shipbuilding and Submarine

User questions regarding Artificial Intelligence's impact on military shipbuilding and submarines often center on its potential to revolutionize operational efficiency, decision-making, and autonomous capabilities. Concerns frequently raised include the ethical implications of AI in warfare, the cybersecurity risks associated with integrated AI systems, and the significant investment required for development and deployment. Users seek to understand how AI will enhance situational awareness, predictive maintenance, and target recognition, while also questioning its reliability in critical combat scenarios and the necessary human oversight.

AI is poised to fundamentally transform the design, construction, and operation of military shipbuilding and submarines. In the design phase, AI-driven simulations can optimize hull forms for hydrodynamics and stealth, reduce material waste, and accelerate the prototyping process. Operationally, AI algorithms can analyze vast amounts of sensor data, providing enhanced situational awareness, threat assessment, and supporting faster, more informed decision-making for crew members. The integration of AI in combat management systems will enable advanced target tracking, autonomous navigation, and intelligent resource allocation, significantly improving mission effectiveness and reducing human workload.

Furthermore, AI will play a critical role in the maintenance and logistical aspects of naval assets. Predictive maintenance fueled by AI can analyze real-time performance data to anticipate equipment failures, enabling proactive repairs and minimizing downtime, thereby extending the operational lifespan of vessels. AI-powered supply chain management systems can optimize spare parts inventory and logistics, ensuring naval fleets remain mission-ready. While the benefits are substantial, addressing the ethical frameworks, ensuring robust cybersecurity, and establishing clear human-AI teaming protocols remain crucial for successful implementation.

- Enhanced situational awareness through AI-powered data fusion and analysis.

- Predictive maintenance optimization, reducing downtime and extending vessel lifespan.

- Autonomous navigation and intelligent decision-making support for crew.

- Improved combat management systems with AI for target recognition and threat assessment.

- Accelerated design and prototyping through AI-driven simulations and optimization.

- Cybersecurity challenges increasing with AI integration in sensitive systems.

- Ethical considerations surrounding autonomous weapon systems and human-machine teaming.

Key Takeaways Military Shipbuilding and Submarine Market Size & Forecast

Common user questions regarding key takeaways from the Military Shipbuilding and Submarine market size and forecast often focus on identifying the primary growth drivers, understanding the long-term investment outlook, and anticipating the impact of geopolitical factors. Users are interested in discerning which regions will demonstrate the most significant growth, the types of naval assets that will see the highest demand, and how emerging technologies will shape future market dynamics. They seek clear, concise summaries of market trajectory and the underlying factors influencing it.

The market is poised for consistent expansion, driven by a global emphasis on maritime security and strategic defense. Nations are committed to upgrading and expanding their naval capabilities, recognizing the critical role of sea power in modern geopolitical strategies. This sustained investment creates a stable demand environment, supporting long-term growth for naval shipbuilders and submarine manufacturers. The integration of advanced technologies, such as AI, stealth, and advanced propulsion, will be central to this evolution, commanding premium valuations for sophisticated platforms.

The forecast period anticipates robust growth across key segments, with particular emphasis on high-value assets like submarines and aircraft carriers, alongside increasing demand for versatile patrol vessels and support ships. Regional growth will be notably strong in the Asia Pacific due to escalating maritime disputes and defense modernization programs, while North America and Europe will continue to drive innovation and high-end technological advancements. The market is characterized by long procurement cycles and high barriers to entry, ensuring stability for established players but also fostering innovation in niche technology areas.

- Significant market growth projected, reaching USD 86.7 Billion by 2033.

- Global defense spending increases are a primary growth engine.

- Technological advancements, including AI and stealth, are central to market evolution.

- Asia Pacific anticipated as a key growth region due to naval modernization.

- Demand for submarines and aircraft carriers remains consistently high.

- Long-term market stability due to extended procurement cycles and high investment.

Military Shipbuilding and Submarine Market Drivers Analysis

The Military Shipbuilding and Submarine market is primarily driven by escalating geopolitical tensions and an increasing focus on maritime security. Nations globally are enhancing their naval capabilities to protect economic interests, secure vital sea lanes, and project power in an increasingly complex international environment. This has led to substantial increases in defense budgets, particularly for naval procurements, enabling the acquisition of advanced vessels and the modernization of existing fleets. The imperative to maintain a credible deterrence and respond effectively to emerging threats necessitates continuous investment in naval assets, thereby fueling market growth.

Technological advancements also play a crucial role as a market driver, pushing the boundaries of what is possible in naval warfare. Innovations in propulsion systems, stealth technology, integrated combat systems, and cybersecurity are continually introduced, leading to the development of more capable and resilient vessels. These technological leaps render older fleets obsolete, creating a perpetual demand for new builds. Furthermore, the rise of unconventional threats, such as piracy, terrorism, and illegal fishing, necessitates a diverse range of naval platforms, from large combatants to agile patrol vessels, contributing to the market's comprehensive expansion.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Geopolitical Tensions and Maritime Disputes | +1.5% | Asia Pacific, Middle East, Europe | Short to Medium-Term (2025-2030) |

| Global Naval Fleet Modernization Programs | +1.2% | North America, Europe, Asia Pacific | Medium to Long-Term (2025-2033) |

| Advancements in Naval Technology (Stealth, AI, Propulsion) | +1.0% | Global, particularly developed economies | Medium to Long-Term (2025-2033) |

| Rising Defense Budgets Worldwide | +0.8% | Global, with strong growth in emerging economies | Short to Medium-Term (2025-2030) |

| Protection of Economic Interests and Sea Lanes | +0.7% | Global, particularly coastal nations | Long-Term (2025-2033) |

Military Shipbuilding and Submarine Market Restraints Analysis

Despite the robust growth drivers, the Military Shipbuilding and Submarine market faces several significant restraints that can impede its expansion. One of the primary challenges is the incredibly high cost associated with the research, development, and procurement of naval vessels, especially sophisticated submarines and aircraft carriers. These projects often run into billions of dollars, placing immense financial strain on national budgets and potentially leading to project delays or cancellations, particularly in economies facing fiscal constraints. The long production cycles, sometimes spanning over a decade for complex platforms, also tie up significant capital and resources, making it difficult for nations to rapidly adapt to evolving threats or economic shifts.

Furthermore, stringent regulatory frameworks and complex international arms control treaties impose significant limitations on the export and transfer of military shipbuilding technologies. These regulations, often aimed at non-proliferation and regional stability, can restrict market access and limit the potential for sales to certain countries, thereby curbing global market opportunities. The political sensitivity surrounding defense contracts also means that decisions can be influenced by diplomatic relations, domestic politics, and human rights concerns, adding layers of complexity to market transactions. Public opposition to increased defense spending, particularly in democratic nations, can also lead to budget cuts or delays in major naval programs, further acting as a restraint on market growth.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Procurement and R&D Costs | -1.3% | Global, impacts all nations | Long-Term (2025-2033) |

| Stringent Regulations and Export Controls | -1.0% | Global, affects trade between nations | Long-Term (2025-2033) |

| Long Production Cycles and Delivery Times | -0.8% | Global, impacts defense planning | Medium to Long-Term (2025-2033) |

| Economic Downturns and Budgetary Constraints | -0.7% | Specific regions/countries experiencing recession | Short to Medium-Term (2025-2028) |

| Political Opposition to Defense Spending | -0.5% | Developed Western Democracies | Short to Medium-Term (2025-2028) |

Military Shipbuilding and Submarine Market Opportunities Analysis

Significant opportunities exist within the Military Shipbuilding and Submarine market, primarily driven by the increasing demand for advanced naval platforms from non-traditional buyers and the expanding scope of maritime security challenges. As more nations seek to establish or bolster their blue-water navies, there is a growing market for mid-range capabilities, including frigates, patrol vessels, and conventionally powered submarines, from countries previously reliant on older fleets or external security guarantees. This expansion of the customer base beyond traditional naval powers opens new avenues for manufacturers and suppliers, fostering market diversification.

The rapid evolution of naval technology also presents substantial opportunities for innovation and specialization. The ongoing integration of unmanned systems, cyber warfare capabilities, and advanced data analytics into naval platforms offers avenues for companies to develop cutting-edge solutions and capture new market niches. Furthermore, the emphasis on sustainability and environmental regulations within the maritime sector creates opportunities for developing greener propulsion systems and more energy-efficient vessel designs, aligning defense capabilities with global environmental responsibilities. Retrofit and upgrade programs for existing fleets also represent a continuous revenue stream, allowing nations to enhance current assets without incurring the full cost of new builds.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Emerging Market Demand from Non-Traditional Buyers | +1.3% | Southeast Asia, Africa, Latin America | Medium to Long-Term (2027-2033) |

| Development of Unmanned and Autonomous Naval Systems | +1.1% | Global, particularly North America, Europe, Asia Pacific | Long-Term (2028-2033) |

| Modernization and Retrofit Programs for Existing Fleets | +0.9% | Global, developed and developing nations | Short to Medium-Term (2025-2030) |

| Focus on Green Technologies and Sustainable Propulsion | +0.7% | Europe, North America, Japan | Long-Term (2028-2033) |

| Cybersecurity Integration for Naval Platforms | +0.6% | Global, with high demand from developed navies | Medium-Term (2025-2030) |

Military Shipbuilding and Submarine Market Challenges Impact Analysis

The Military Shipbuilding and Submarine market faces formidable challenges, notably the escalating complexity and technological sophistication required for modern naval vessels. The integration of advanced combat systems, stealth features, and robust cybersecurity necessitates specialized expertise, advanced manufacturing processes, and significant research and development investment. This increasing complexity drives up production costs and extends delivery timelines, making projects prone to budget overruns and schedule delays, which can deter potential buyers or strain national defense budgets. Maintaining a skilled workforce capable of designing, building, and maintaining these highly technical assets also presents a significant challenge.

Moreover, the geopolitical landscape, while a driver of demand, also presents inherent challenges. Shifting alliances, trade disputes, and economic sanctions can disrupt supply chains, impact component availability, and influence export agreements, creating instability in the market. The highly competitive nature of the global defense industry, coupled with the long-term nature of contracts, means that manufacturers must consistently innovate while navigating intense competition from established players and emerging competitors. Intellectual property protection and technology transfer issues also pose challenges, particularly when collaborating on international projects or licensing advanced systems, requiring careful negotiation and adherence to complex legal frameworks to safeguard national interests and technological advantages.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Complexity and Technological Integration | -1.2% | Global, impacts R&D and production | Long-Term (2025-2033) |

| Supply Chain Disruptions and Material Shortages | -1.0% | Global, specific impact on key manufacturing regions | Short to Medium-Term (2025-2028) |

| Skilled Labor Shortages and Workforce Development | -0.8% | Developed economies with aging workforce | Long-Term (2025-2033) |

| High Competition and Intellectual Property Concerns | -0.6% | Global, specific to major defense contractors | Medium to Long-Term (2025-2033) |

| Cyber Threats to Naval Systems and Infrastructure | -0.5% | Global, impacts all modern naval assets | Continuous |

Military Shipbuilding and Submarine Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the Military Shipbuilding and Submarine market, encompassing historical data, current market dynamics, and future projections. It delivers critical insights into market size, growth drivers, restraints, opportunities, and challenges across various segments and key geographical regions. The report leverages extensive primary and secondary research to offer a holistic view of the industry landscape, aiding stakeholders in strategic decision-making and understanding the evolving global naval defense environment.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 55.2 Billion |

| Market Forecast in 2033 | USD 86.7 Billion |

| Growth Rate | 5.8% |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Global Naval Systems Inc., Maritime Defense Solutions, Oceanic Engineering Group, Advanced Submarine Technologies, Marine Defense Innovations, Naval Aerospace & Defense Systems, Strategic Shipbuilding Consortium, Integrated Maritime Solutions, Stealth Naval Platforms Ltd., Future Seapower Corporation, Allied Marine Defense, Horizon Shipyard Group, International Defense Navies, Ocean Guard Technologies, Vanguard Maritime Group, Secure Seas Dynamics, Sentinel Naval Industries, Blue Water Systems, Coastal Defense Solutions, Pacific Naval Engineering. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Military Shipbuilding and Submarine market is meticulously segmented to provide a granular understanding of its diverse components and dynamics. This segmentation facilitates a deeper analysis of specific market niches, enabling stakeholders to identify key growth areas and tailor strategies effectively. The market is primarily segmented by type of vessel, including a comprehensive range from advanced submarines and aircraft carriers to specialized patrol and support vessels, each serving distinct operational requirements for naval forces globally. Further segmentation by technology, end-use, material, and propulsion system allows for a detailed examination of technological adoption rates, specific operational demands, material science advancements, and energy efficiency trends across the defense sector.

The 'By Technology' segment differentiates between conventional and nuclear-powered vessels, reflecting the strategic capabilities and operational ranges required by various navies. The 'By End-Use' segment highlights the varied applications, from core naval combat operations to coast guard duties and specialized missions. Furthermore, the 'By Material' and 'By Propulsion System' segments underscore the continuous innovation in shipbuilding materials and energy systems aimed at enhancing stealth, speed, endurance, and environmental compliance. This multi-layered segmentation ensures a comprehensive analytical framework for understanding the intricate supply and demand forces shaping the military shipbuilding and submarine industry.

- By Type:

- Submarines (Conventional, Nuclear)

- Aircraft Carriers

- Destroyers

- Frigates

- Corvettes

- Patrol Vessels

- Amphibious Ships

- Mine Countermeasure Vessels (MCMV)

- Support Vessels (Replenishment, Hospital Ships)

- By Technology:

- Conventional

- Nuclear-powered

- Hybrid-electric

- By End-Use:

- Naval Forces

- Coast Guard

- Special Operations Forces

- By Material:

- Steel

- Composites

- Special Alloys

- By Propulsion System:

- Diesel-Electric

- Nuclear Reactor

- Gas Turbine

- Integrated Electric Propulsion (IEP)

- Fuel Cell

Regional Highlights

- North America: This region, particularly the United States, represents a dominant force in the Military Shipbuilding and Submarine market due to substantial defense budgets, advanced technological capabilities, and a continuous focus on maintaining naval supremacy. Investments in next-generation aircraft carriers, nuclear-powered submarines, and cutting-edge surface combatants drive significant market value.

- Europe: European nations are heavily engaged in naval modernization programs, driven by regional security concerns and the need to replace aging Cold War-era fleets. Countries like the United Kingdom, France, Germany, and Italy are investing in advanced frigates, destroyers, and conventional submarines, often through multinational collaborations, emphasizing technological sophistication and interoperability.

- Asia Pacific (APAC): The APAC region is projected to exhibit the fastest growth, fueled by escalating maritime disputes, increasing geopolitical tensions, and ambitious naval expansion plans by countries such as China, India, Japan, and South Korea. These nations are heavily investing in both surface combatants and submarines to assert maritime claims and enhance regional power projection.

- Latin America: While smaller in market share compared to other regions, Latin American countries are focused on modernizing their patrol vessel fleets to combat illegal fishing, drug trafficking, and piracy, along with limited acquisition of corvettes and frigates for coastal defense and sovereignty protection.

- Middle East and Africa (MEA): This region is characterized by growing defense expenditures driven by geopolitical instabilities and the need for maritime security in strategic waterways. Investments are primarily directed towards patrol vessels, corvettes, and frigates for coastal defense and securing vital oil and gas infrastructure.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Military Shipbuilding and Submarine Market.- Global Naval Systems Inc.

- Maritime Defense Solutions

- Oceanic Engineering Group

- Advanced Submarine Technologies

- Marine Defense Innovations

- Naval Aerospace & Defense Systems

- Strategic Shipbuilding Consortium

- Integrated Maritime Solutions

- Stealth Naval Platforms Ltd.

- Future Seapower Corporation

- Allied Marine Defense

- Horizon Shipyard Group

- International Defense Navies

- Ocean Guard Technologies

- Vanguard Maritime Group

- Secure Seas Dynamics

- Sentinel Naval Industries

- Blue Water Systems

- Coastal Defense Solutions

- Pacific Naval Engineering

Frequently Asked Questions

Analyze common user questions about the Military Shipbuilding and Submarine market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is the current estimated size of the Military Shipbuilding and Submarine Market?

The Military Shipbuilding and Submarine Market is estimated at USD 55.2 Billion in 2025, reflecting global investments in naval defense and fleet modernization efforts.

What is the projected growth rate for the Military Shipbuilding and Submarine Market through 2033?

The market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.8% between 2025 and 2033, driven by increasing geopolitical tensions and technological advancements.

Which key trends are shaping the Military Shipbuilding and Submarine Market?

Key trends include the increased adoption of unmanned naval systems, integration of AI and stealth technologies, emphasis on modular designs, and a growing focus on sustainable propulsion systems for naval vessels.

How is AI impacting the Military Shipbuilding and Submarine sector?

AI is transforming the sector by enhancing situational awareness, optimizing predictive maintenance, enabling autonomous navigation, and improving combat management systems, leading to more efficient and capable naval operations.

Which regions are key contributors to the Military Shipbuilding and Submarine Market growth?

North America and Europe remain significant contributors, while the Asia Pacific region is expected to demonstrate the fastest growth due to extensive naval modernization and rising maritime security concerns.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted