Metal Clad Plate Market

Metal Clad Plate Market Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_707009 | Last Updated : September 08, 2025 |

Format : ![]()

![]()

![]()

![]()

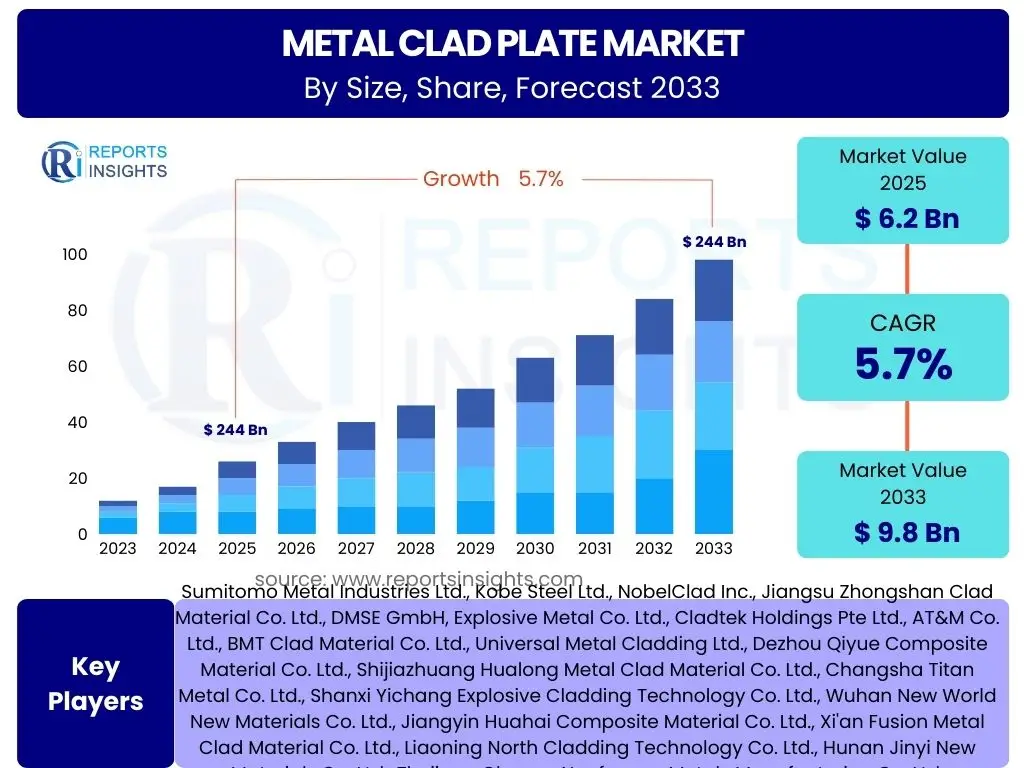

Metal Clad Plate Market Size

According to Reports Insights Consulting Pvt Ltd, The Metal Clad Plate Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.7% between 2025 and 2033. The market is estimated at USD 6.2 Billion in 2025 and is projected to reach USD 9.8 Billion by the end of the forecast period in 2033.

Key Metal Clad Plate Market Trends & Insights

The Metal Clad Plate market is currently shaped by several significant trends, primarily driven by increasing demand from heavy industries requiring advanced material solutions. Users frequently inquire about the latest technological advancements in cladding processes and the expanding range of applications beyond traditional sectors. There is a growing emphasis on high-performance materials capable of withstanding extreme operating conditions, such as high temperatures, pressures, and corrosive environments, which is propelling innovation in the market. Furthermore, sustainability considerations and the pursuit of cost-effective manufacturing methods are emerging as crucial factors influencing market dynamics.

Industry stakeholders are keenly observing the shift towards more sophisticated cladding techniques that offer superior metallurgical bonds and enhanced material properties. The adoption of automation and digitalization in manufacturing processes is also a key trend, aimed at improving efficiency and product consistency. Additionally, the customization of clad plates to meet specific project requirements, particularly in niche and high-value applications, is gaining traction. These trends collectively underscore a market moving towards greater specialization, efficiency, and material performance.

- Growing demand for corrosion-resistant and high-temperature-resistant materials across various industries.

- Advancements in cladding technologies, including explosive bonding, roll bonding, and diffusion bonding, leading to improved product quality and wider application range.

- Increasing adoption of clad plates in emerging sectors such as renewable energy, hydrogen production, and advanced defense systems.

- Focus on lightweighting and enhanced mechanical properties to optimize structural integrity and performance in critical applications.

- Rising investment in research and development for novel material combinations and surface treatments to expand application versatility.

AI Impact Analysis on Metal Clad Plate

The integration of Artificial Intelligence (AI) and machine learning (ML) is beginning to revolutionize various aspects of the Metal Clad Plate industry, addressing common user questions related to process optimization, quality assurance, and material innovation. AI algorithms are increasingly employed to analyze vast datasets from manufacturing processes, enabling predictive modeling for material behavior, optimizing process parameters, and reducing defects. This leads to more efficient production cycles and enhanced product reliability, which are critical concerns for manufacturers and end-users alike.

Beyond manufacturing, AI holds significant potential in the design and engineering phases of metal clad plates. Generative design tools powered by AI can explore numerous material combinations and structural configurations to identify optimal solutions for specific applications, significantly reducing development time and costs. Furthermore, AI-driven inspection systems can provide real-time quality control, ensuring that clad plates meet stringent industry standards with higher precision than traditional manual methods. The strategic adoption of AI is therefore viewed as a key enabler for competitive advantage and sustained growth in the metal clad plate market.

- Enhanced material design and selection through AI-driven simulations and predictive analytics for optimal clad combinations.

- Optimization of manufacturing processes, including explosive bonding and roll bonding, leading to reduced waste and increased yield.

- Improved quality control and defect detection using AI-powered visual inspection systems and non-destructive testing.

- Predictive maintenance for manufacturing equipment, minimizing downtime and extending machinery lifespan.

- Supply chain optimization and demand forecasting, leading to more efficient resource allocation and inventory management.

Key Takeaways Metal Clad Plate Market Size & Forecast

The Metal Clad Plate market is poised for robust growth, driven by escalating industrial demands for specialized materials that offer superior performance in harsh environments. A key takeaway from the market size and forecast is the consistent expansion of application areas, particularly within the energy, chemical processing, and shipbuilding sectors, where the unique properties of clad plates provide significant advantages over monolithic materials. The market's upward trajectory reflects a global emphasis on infrastructure development and industrial modernization, necessitating durable and efficient material solutions.

Furthermore, the forecast indicates a significant shift towards technological innovation and customization as primary growth enablers. Stakeholders should note the increasing investment in research and development aimed at improving cladding techniques and expanding the range of compatible materials. The market’s resilience to economic fluctuations is also a crucial insight, as the demand for high-performance materials often persists due to their critical role in ensuring operational safety and efficiency across essential industries. This sustained demand underpins the optimistic growth projections for the coming years.

- The market is projected for significant growth, driven by increasing industrial application in demanding environments.

- Technological advancements in cladding processes are crucial for enhancing product performance and expanding market reach.

- Strong demand from the oil & gas, chemical, power generation, and shipbuilding industries continues to be a primary growth driver.

- The market exhibits resilience due to the essential role of clad plates in critical infrastructure and industrial operations.

- Emphasis on customization and specialized solutions for high-value applications will contribute substantially to market expansion.

Metal Clad Plate Market Drivers Analysis

The global Metal Clad Plate market is significantly propelled by the increasing demand for high-performance materials capable of withstanding severe operational conditions. Industries such as oil and gas, chemical processing, power generation, and marine consistently require materials that offer superior corrosion resistance, high strength-to-weight ratio, and excellent thermal conductivity. Metal clad plates address these critical needs by combining the properties of two or more distinct metals, thereby extending the lifespan of equipment and reducing maintenance costs in harsh environments. This inherent advantage drives their adoption across various critical applications, underpinning market expansion.

Furthermore, the rapid pace of industrialization and infrastructure development, particularly in emerging economies, contributes substantially to market growth. As new chemical plants, power stations, and offshore structures are constructed, the demand for reliable and durable materials intensifies. The unique ability of metal clad plates to provide a cost-effective alternative to solid alloy plates, without compromising on performance, makes them an attractive solution for large-scale projects. This economic viability, coupled with stringent safety and environmental regulations demanding robust material integrity, further catalyzes the market’s upward trajectory.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing demand from Oil & Gas and Chemical Processing Industries | +1.5% | North America, Middle East & Africa, Asia Pacific | Short to Mid-term (2025-2029) |

| Increasing Investment in Power Generation (Nuclear, Thermal, Renewables) | +1.2% | Asia Pacific, Europe, North America | Mid to Long-term (2027-2033) |

| Need for Corrosion and Wear Resistance in Harsh Environments | +1.0% | Global | Long-term (2025-2033) |

| Expansion of Shipbuilding and Marine Applications | +0.8% | Asia Pacific, Europe | Mid-term (2026-2031) |

| Technological Advancements in Cladding Methods | +0.7% | Global | Long-term (2025-2033) |

Metal Clad Plate Market Restraints Analysis

Despite the robust growth prospects, the Metal Clad Plate market faces certain restraints that could impede its expansion. One significant challenge is the relatively high manufacturing cost associated with producing clad plates compared to solid base metals. The complex processes involved, such as explosive bonding, roll bonding, or diffusion bonding, require specialized equipment, skilled labor, and stringent quality control, which collectively add to the overall production expenses. This cost factor can sometimes deter potential end-users, particularly those operating on tight budgets or in less critical applications where the benefits of clad plates may not outweigh the initial investment.

Furthermore, the availability of alternative materials and processes poses a competitive threat to the widespread adoption of metal clad plates. While clad plates offer unique advantages, certain applications might opt for solid corrosion-resistant alloys, coatings, or liners as more conventional or perceived simpler solutions. Market awareness about the long-term benefits and cost-effectiveness of clad plates also remains a restraint in some regions, necessitating greater educational efforts from manufacturers. These factors, alongside potential supply chain disruptions for specific base or cladding materials, contribute to the challenges faced by the market.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Manufacturing Cost and Complex Production Processes | -0.9% | Global | Long-term (2025-2033) |

| Availability of Alternative Materials and Technologies (e.g., solid alloys, coatings) | -0.7% | Global | Mid to Long-term (2026-2033) |

| Economic Volatility and Fluctuations in Raw Material Prices | -0.6% | Global, particularly emerging markets | Short to Mid-term (2025-2029) |

| Limited Standardization and Certification in Niche Applications | -0.4% | Specific Niche Markets | Long-term (2025-2033) |

| Lack of Awareness and Technical Expertise in Certain Regions | -0.3% | Emerging Economies | Long-term (2025-2033) |

Metal Clad Plate Market Opportunities Analysis

The Metal Clad Plate market is presented with substantial opportunities for expansion, primarily driven by the burgeoning demand from industries transitioning to cleaner energy sources and sustainable practices. The global push for renewable energy projects, including offshore wind farms, geothermal plants, and hydrogen production facilities, creates a significant need for materials that can withstand corrosive environments and offer long-term durability. Metal clad plates, with their superior corrosion resistance and structural integrity, are ideally suited for components within these emerging energy infrastructures, offering a lucrative avenue for market growth and innovation.

Furthermore, the increasing focus on resource efficiency and asset life extension across industrial sectors provides a compelling opportunity for metal clad plate manufacturers. Companies are actively seeking ways to reduce downtime, minimize maintenance, and improve the operational lifespan of their equipment. By offering customized clad solutions that address specific operational challenges, manufacturers can tap into a broader customer base looking for high-value, long-lasting material solutions. The expansion into new applications, such as advanced aerospace and defense components or specialized high-pressure vessels, also represents a key area for market development and technological diversification.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Expansion in Renewable Energy and Green Hydrogen Production Sectors | +1.3% | Europe, Asia Pacific, North America | Mid to Long-term (2027-2033) |

| Growth in Aerospace and Defense Applications requiring Lightweight and Strong Materials | +1.0% | North America, Europe | Long-term (2025-2033) |

| R&D in Novel Cladding Materials and Advanced Manufacturing Techniques | +0.9% | Global | Long-term (2025-2033) |

| Increased Demand for Customization and Application-Specific Solutions | +0.8% | Global | Mid-term (2026-2031) |

| Infrastructure Development in Developing Economies | +0.7% | Asia Pacific, Latin America, Middle East & Africa | Mid to Long-term (2027-2033) |

Metal Clad Plate Market Challenges Impact Analysis

The Metal Clad Plate market faces several challenges that require strategic navigation for sustained growth. A significant hurdle is maintaining stringent quality control throughout the complex manufacturing processes, which involve bonding dissimilar metals. Any imperfections in the bond integrity or material properties can lead to catastrophic failures in critical applications, underscoring the need for advanced inspection techniques and highly skilled operators. Achieving consistent quality across various cladding methods and material combinations demands substantial investment in technology and expertise, posing a continuous challenge for manufacturers.

Another prominent challenge relates to the inherent complexity of the supply chain for specialized base and cladding materials. The sourcing of high-grade raw materials, often from limited suppliers, can be susceptible to geopolitical factors, trade policies, and global economic fluctuations, leading to price volatility and potential supply disruptions. Furthermore, the market is characterized by intense competition among a relatively small number of highly specialized manufacturers, necessitating continuous innovation and differentiation. Navigating these complexities while adhering to evolving environmental regulations and safety standards presents an ongoing test for market participants.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Maintaining Stringent Quality Control and Ensuring Bond Integrity | -0.8% | Global | Long-term (2025-2033) |

| Volatility in Raw Material Prices and Supply Chain Disruptions | -0.7% | Global | Short to Mid-term (2025-2029) |

| Intense Competition and Need for Product Differentiation | -0.6% | Global | Long-term (2025-2033) |

| Stringent Regulatory Compliance and Environmental Standards | -0.5% | Europe, North America | Long-term (2025-2033) |

| Requirement for Highly Skilled Labor and Technical Expertise | -0.4% | Global | Long-term (2025-2033) |

Metal Clad Plate Market - Updated Report Scope

This comprehensive report delves into the Metal Clad Plate market, providing an in-depth analysis of its current landscape, historical performance, and future growth trajectories. The scope encompasses detailed market sizing, segmentation by type, material, application, and end-use industry, along with a thorough regional assessment. It offers strategic insights into market trends, drivers, restraints, opportunities, and challenges, highlighting the impact of technological advancements and key market dynamics. The report also profiles leading industry players, offering a holistic view of the competitive environment and providing valuable strategic recommendations for stakeholders.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 6.2 Billion |

| Market Forecast in 2033 | USD 9.8 Billion |

| Growth Rate | 5.7% |

| Number of Pages | 247 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Sumitomo Metal Industries Ltd., Kobe Steel Ltd., NobelClad Inc., Jiangsu Zhongshan Clad Material Co. Ltd., DMSE GmbH, Explosive Metal Co. Ltd., Cladtek Holdings Pte Ltd., AT&M Co. Ltd., BMT Clad Material Co. Ltd., Universal Metal Cladding Ltd., Dezhou Qiyue Composite Material Co. Ltd., Shijiazhuang Hualong Metal Clad Material Co. Ltd., Changsha Titan Metal Co. Ltd., Shanxi Yichang Explosive Cladding Technology Co. Ltd., Wuhan New World New Materials Co. Ltd., Jiangyin Huahai Composite Material Co. Ltd., Xi'an Fusion Metal Clad Material Co. Ltd., Liaoning North Cladding Technology Co. Ltd., Hunan Jinyi New Materials Co. Ltd., Zhejiang Chunan Nonferrous Metals Manufacturing Co. Ltd. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Metal Clad Plate market is comprehensively segmented to provide a granular understanding of its diverse applications and material compositions. This segmentation is crucial for identifying specific market niches, understanding demand patterns across various industries, and recognizing the technological preferences driving adoption. The categorization by type reflects the primary manufacturing methods, each offering distinct advantages in terms of bond strength, material compatibility, and production scale. Similarly, segmenting by material highlights the range of base and cladding metals used, reflecting the specific performance requirements of different end-use industries.

Further segmentation by application and end-use industry delineates how metal clad plates are utilized across a spectrum of critical sectors, from energy production and chemical processing to marine and aerospace. This detailed breakdown allows for a precise analysis of demand drivers, regional preferences, and competitive landscapes within each sub-segment. Such comprehensive segmentation is vital for stakeholders to formulate targeted strategies, identify emerging opportunities, and adapt to evolving market needs, ultimately facilitating informed decision-making across the value chain.

- By Type: Explosive Cladding, Roll Bonding, Diffusion Bonding, Weld Overlay, Others

- By Material: Stainless Steel Clad, Titanium Clad, Nickel Alloy Clad, Copper Clad, Aluminum Clad, Zirconium Clad, Other Specialty Metal Clad

- By Application: Heat Exchangers, Pressure Vessels, Pipelines, Tanks and Storage Vessels, Shipbuilding Components, Structural Components, Chemical Equipment, Desalination Plants, Power Plant Components, Other Industrial Applications

- By End-Use Industry: Oil & Gas, Chemical & Petrochemical, Power Generation, Shipbuilding & Marine, Metallurgy & Mining, Desalination, Automotive, Aerospace & Defense, Construction, Others

- By Region: North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA)

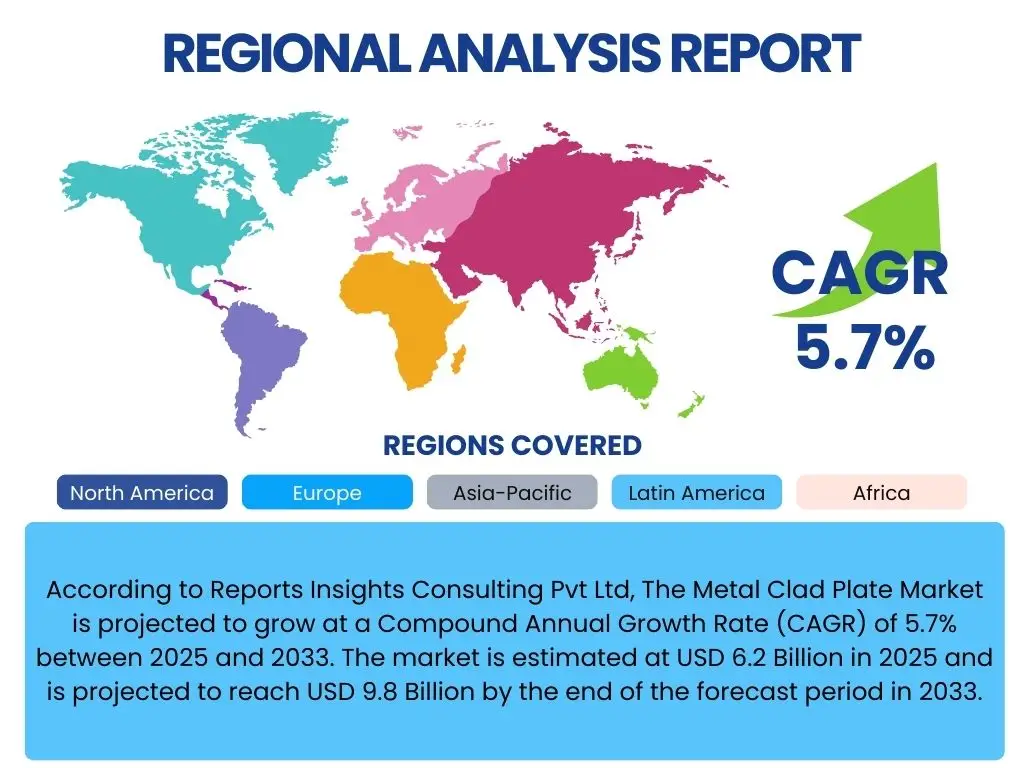

Regional Highlights

- Asia Pacific: This region is anticipated to be a dominant force in the Metal Clad Plate market, driven by rapid industrialization, extensive infrastructure development projects, and significant investments in the chemical, petrochemical, and power generation sectors, particularly in countries like China, India, and South Korea.

- North America: The market in North America is characterized by robust demand from the oil and gas industry, ongoing modernization of chemical processing facilities, and increasing adoption in the aerospace and defense sectors, with the United States being a key contributor.

- Europe: Europe represents a mature but growing market, propelled by advanced manufacturing capabilities, stringent environmental regulations necessitating high-performance materials, and substantial investments in renewable energy infrastructure, including offshore wind and hydrogen technologies.

- Middle East & Africa (MEA): The MEA region exhibits strong growth potential, primarily due to large-scale oil and gas projects, significant investments in desalination plants to address water scarcity, and infrastructure expansion initiatives across various countries.

- Latin America: This region is experiencing steady growth, fueled by investments in the metallurgy and mining sectors, expanding oil and gas exploration activities, and the need for durable materials in chemical processing industries.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Metal Clad Plate Market.- Sumitomo Metal Industries Ltd.

- Kobe Steel Ltd.

- NobelClad Inc.

- Jiangsu Zhongshan Clad Material Co. Ltd.

- DMSE GmbH

- Explosive Metal Co. Ltd.

- Cladtek Holdings Pte Ltd.

- AT&M Co. Ltd.

- BMT Clad Material Co. Ltd.

- Universal Metal Cladding Ltd.

- Dezhou Qiyue Composite Material Co. Ltd.

- Shijiazhuang Hualong Metal Clad Material Co. Ltd.

- Changsha Titan Metal Co. Ltd.

- Shanxi Yichang Explosive Cladding Technology Co. Ltd.

- Wuhan New World New Materials Co. Ltd.

- Jiangyin Huahai Composite Material Co. Ltd.

- Xi'an Fusion Metal Clad Material Co. Ltd.

- Liaoning North Cladding Technology Co. Ltd.

- Hunan Jinyi New Materials Co. Ltd.

- Zhejiang Chunan Nonferrous Metals Manufacturing Co. Ltd.

Frequently Asked Questions

What is a metal clad plate?

A metal clad plate is a composite material consisting of two or more distinct metals or alloys permanently bonded together to combine their unique properties. This bonding creates a material that leverages the strength and cost-effectiveness of a base metal with the corrosion resistance or specialized properties of a cladding metal, offering superior performance in demanding applications.

What are the primary applications of metal clad plates?

Metal clad plates are primarily used in industries requiring materials with high resistance to corrosion, wear, and extreme temperatures. Key applications include heat exchangers, pressure vessels, pipelines, and storage tanks in oil and gas, chemical processing, power generation, and shipbuilding sectors, where durability and safety are paramount.

How do metal clad plates differ from solid plates?

Metal clad plates differ from solid plates by offering a combination of material properties that a single, monolithic metal cannot provide. They are more cost-effective than solid specialty alloys for large structures while delivering equivalent or superior performance in specific corrosive or high-temperature environments. This composite nature allows for optimized material usage and enhanced functionality.

What manufacturing processes are used for metal clad plates?

The primary manufacturing processes for metal clad plates include explosive bonding, where a controlled explosion bonds the metals; roll bonding, which uses pressure and heat; and diffusion bonding, relying on atomic diffusion at high temperatures. Weld overlay is also utilized for surface cladding. Each method offers distinct advantages depending on the material combination and application requirements.

What factors are driving the growth of the metal clad plate market?

The growth of the metal clad plate market is primarily driven by increasing demand from industries facing harsh operating conditions, such as oil & gas, chemical, and power generation, for materials with superior corrosion and wear resistance. Technological advancements in cladding processes and a global focus on industrial infrastructure development also significantly contribute to market expansion.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted