Mercury Removal Adsorbent Market

Mercury Removal Adsorbent Market Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_707657 | Last Updated : September 08, 2025 |

Format : ![]()

![]()

![]()

![]()

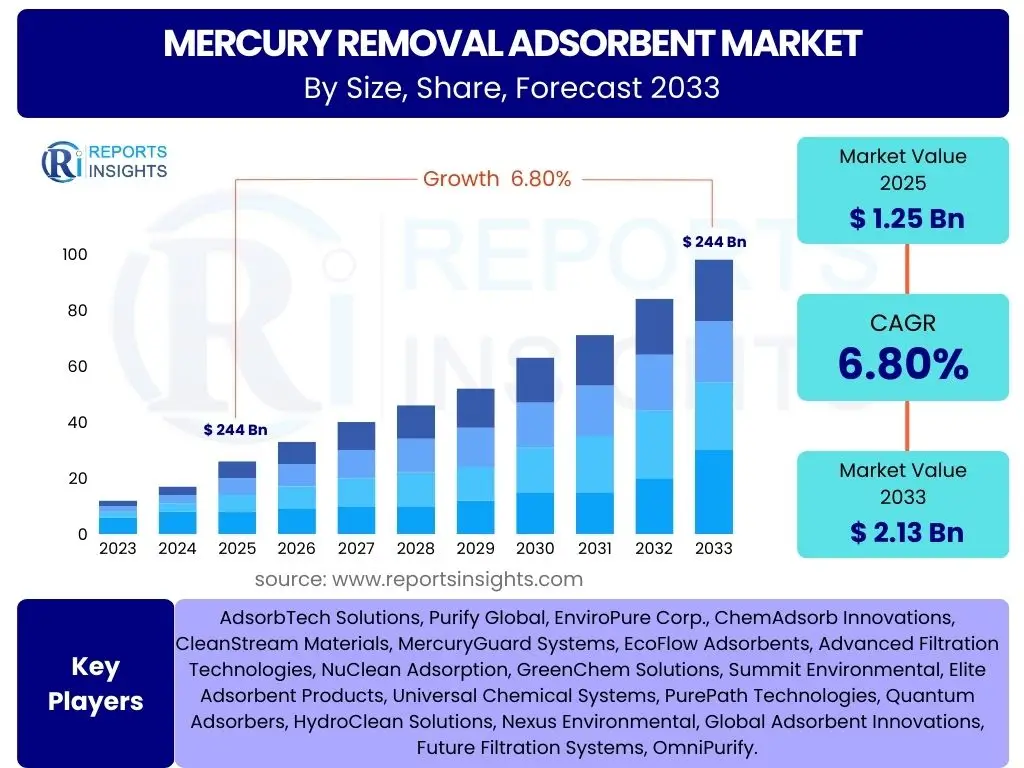

Mercury Removal Adsorbent Market Size

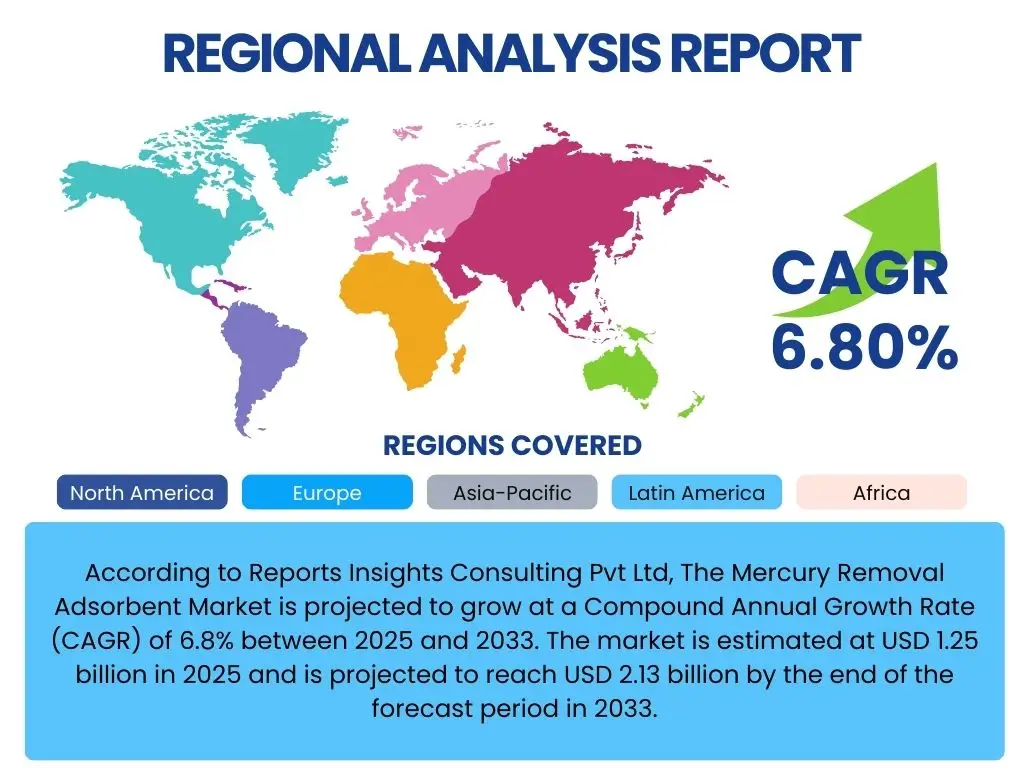

According to Reports Insights Consulting Pvt Ltd, The Mercury Removal Adsorbent Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2025 and 2033. The market is estimated at USD 1.25 billion in 2025 and is projected to reach USD 2.13 billion by the end of the forecast period in 2033.

Key Mercury Removal Adsorbent Market Trends & Insights

User queries frequently focus on the evolving landscape of mercury removal, particularly concerning new regulatory frameworks and the increasing demand for sustainable environmental solutions. Insights suggest a significant shift towards advanced, more efficient adsorbent materials that offer enhanced selectivity and longer service life. There is also a notable trend in industries seeking comprehensive solutions that integrate mercury removal into broader waste treatment processes, moving beyond standalone adsorption units. The market is increasingly influenced by the need for cost-effective and environmentally benign options, prompting research into novel materials and regeneration technologies.

A prominent trend is the adoption of nanotechnology and advanced materials, such as metal-organic frameworks (MOFs) and activated carbons modified with specific functional groups, to achieve superior mercury capture efficiency. This is driven by stringent environmental regulations and the desire for higher purity levels in industrial outputs. Furthermore, the market observes a growing emphasis on circular economy principles, leading to innovations in adsorbent regeneration and disposal methods, aimed at minimizing secondary waste generation and reducing operational expenditures for end-users. The globalization of environmental standards is also pushing companies in developing regions to invest in state-of-the-art mercury removal technologies.

- Development of highly selective and regenerative adsorbent materials.

- Increased integration of mercury removal solutions within broader industrial wastewater and gas treatment systems.

- Growing adoption of nanotechnology and advanced functionalized materials for enhanced adsorption.

- Focus on sustainable and eco-friendly adsorbent technologies, including biomass-derived and regenerated options.

- Expansion of regulatory frameworks globally, driving demand for compliant solutions.

- Digitalization and automation in monitoring and optimizing adsorption processes.

AI Impact Analysis on Mercury Removal Adsorbent

Common user questions regarding AI's influence on the mercury removal adsorbent market revolve around its potential to optimize process efficiency, predict adsorbent saturation, and enhance material discovery. Users are keenly interested in how AI can lead to smarter, more adaptive mercury removal systems that reduce operational costs and improve environmental compliance. The analysis reveals an expectation that AI will play a crucial role in data-driven decision-making for adsorbent selection and regeneration scheduling.

AI's impact is anticipated across several facets of the mercury removal adsorbent industry. It is expected to revolutionize the design and synthesis of novel adsorbent materials by predicting optimal structures and compositions, significantly accelerating R&D cycles. Furthermore, AI-powered predictive analytics can optimize the performance of existing adsorption systems by forecasting mercury breakthrough, managing adsorbent lifespan, and scheduling timely replacements or regeneration. This leads to reduced downtime, minimized chemical consumption, and improved overall operational efficiency. The integration of machine learning algorithms with sensor data can create real-time monitoring and control systems, ensuring consistent and effective mercury removal.

- Accelerated discovery and design of novel mercury adsorbent materials through predictive modeling.

- Optimization of adsorption processes via real-time monitoring and predictive analytics, enhancing efficiency and reducing operational costs.

- Improved adsorbent lifespan prediction and regeneration scheduling, minimizing downtime and waste.

- Enhanced quality control and performance verification for mercury removal systems.

- Development of autonomous or semi-autonomous mercury treatment plants with AI-driven control.

Key Takeaways Mercury Removal Adsorbent Market Size & Forecast

User inquiries about key takeaways from the market size and forecast consistently point towards understanding the most impactful factors driving growth and the regions poised for significant expansion. Insights suggest that regulatory stringency and industrial expansion in emerging economies are primary catalysts. The market is characterized by a strong emphasis on technological innovation aimed at improving efficiency and cost-effectiveness of mercury removal solutions.

The Mercury Removal Adsorbent Market is set for sustained growth, primarily propelled by increasingly stringent global environmental regulations, particularly those targeting mercury emissions from industrial sources. This regulatory pressure is compelling industries such as oil and gas, cement, power generation, and chemical manufacturing to invest in advanced mercury removal technologies. A significant takeaway is the ongoing shift towards advanced, high-performance adsorbents that offer greater efficiency, selectivity, and longevity compared to conventional materials. Furthermore, the forecast highlights the Asia Pacific region as a major growth engine, driven by rapid industrialization and growing environmental awareness in countries like China and India. The market also indicates a strong focus on sustainable solutions, including regenerative adsorbents and those derived from waste materials, contributing to both environmental benefits and cost efficiencies for end-users.

- Stringent global environmental regulations are the primary growth driver.

- Technological advancements in adsorbent materials are enhancing efficiency and market appeal.

- Asia Pacific is expected to exhibit the highest growth due to industrial expansion and environmental initiatives.

- Increasing adoption of sustainable and regenerative adsorbent solutions.

- Demand for mercury removal solutions is expanding across diverse industrial sectors.

Mercury Removal Adsorbent Market Drivers Analysis

The Mercury Removal Adsorbent Market is predominantly driven by the escalating global concern over mercury contamination and its severe health and environmental impacts. This concern has translated into the implementation and enforcement of stricter environmental regulations by governments worldwide, mandating the reduction of mercury emissions from various industrial sources. Compliance with these regulations necessitates the adoption of effective mercury removal technologies, thereby directly boosting the demand for specialized adsorbents. Industries such as oil and gas, power generation, cement, and chemical manufacturing are under increasing pressure to meet these new standards.

Beyond regulatory impetus, the rapid industrialization and urbanization in developing economies, particularly in the Asia Pacific region, are contributing significantly to market growth. The expansion of industrial activities in these regions, often accompanied by less mature environmental infrastructure, leads to higher levels of mercury emissions, creating an urgent need for effective abatement solutions. Furthermore, advancements in adsorbent technology, which offer higher efficiency, longer lifespan, and lower operational costs, are making these solutions more attractive and accessible to a wider range of industries, stimulating market adoption. The growing awareness among industries about corporate social responsibility and sustainable practices also plays a role in driving voluntary adoption of mercury removal systems.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Strict Environmental Regulations (e.g., Minamata Convention) | +2.1% | Global, particularly Europe, North America, and APAC | 2025-2033 (Long-term) |

| Increasing Industrialization and Energy Demand | +1.8% | Asia Pacific, Latin America, Middle East | 2025-2033 (Long-term) |

| Technological Advancements in Adsorbent Materials | +1.5% | Global | 2025-2030 (Mid-term) |

| Growing Awareness of Mercury's Health Impacts | +0.8% | Global | 2025-2033 (Long-term) |

Mercury Removal Adsorbent Market Restraints Analysis

Despite the robust growth drivers, the Mercury Removal Adsorbent Market faces several significant restraints that could impede its expansion. One primary concern is the high initial capital expenditure required for installing advanced mercury removal systems, particularly for small and medium-sized enterprises (SMEs). This cost barrier can deter adoption, especially in regions where environmental regulations are less stringently enforced or where economic conditions are challenging. Furthermore, the operational costs associated with adsorbent regeneration, disposal of spent adsorbents, and energy consumption for the treatment process can also be substantial, adding to the overall financial burden for end-users.

Another significant restraint is the limited awareness and technical expertise in certain regions regarding the necessity and benefits of mercury removal technologies. This often leads to a lack of investment in proper treatment systems, even when regulatory frameworks are in place. The availability of alternative, albeit less effective or less environmentally friendly, mercury abatement methods, such as traditional chemical precipitation or activated carbon injection, can also pose a competitive challenge to advanced adsorbents. Additionally, the variability in mercury concentrations and forms across different industrial streams often necessitates customized adsorbent solutions, which can increase complexity and cost, making a one-size-fits-all approach difficult and limiting widespread adoption in some niche applications.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Capital and Operational Costs | -1.5% | Global, particularly developing regions | 2025-2033 (Long-term) |

| Lack of Awareness and Technical Expertise | -0.9% | Latin America, parts of Asia Pacific, MEA | 2025-2030 (Mid-term) |

| Competition from Alternative Treatment Technologies | -0.7% | Global | 2025-2028 (Short-term) |

| Challenges in Spent Adsorbent Disposal and Regeneration | -0.5% | Global | 2025-2033 (Long-term) |

Mercury Removal Adsorbent Market Opportunities Analysis

The Mercury Removal Adsorbent Market presents significant opportunities stemming from the escalating global commitment to sustainable environmental practices and the drive towards cleaner industrial processes. The continuous refinement and enforcement of mercury emission standards worldwide are creating an expanding demand for advanced and efficient mercury abatement solutions across various industrial sectors. This regulatory push encourages industries to invest in new technologies, fostering an environment ripe for innovation and market penetration for novel adsorbent materials.

Furthermore, the growing emphasis on resource recovery and circular economy principles opens up new avenues for adsorbent manufacturers. Developing regenerative adsorbents that can be reused multiple times, thereby reducing waste and operational costs, represents a major opportunity. Similarly, the exploration of cost-effective and environmentally friendly raw materials, such as agricultural waste or industrial by-products, for adsorbent synthesis can lower production costs and enhance market competitiveness. The rising demand for ultra-pure water and gases in high-tech industries, such as semiconductor manufacturing and pharmaceuticals, also creates a niche for highly selective mercury adsorbents. The expansion into emerging markets, where industrial growth is rapid but environmental infrastructure is still developing, offers substantial untapped potential for market players. Collaborations between research institutions and industry leaders to develop next-generation adsorbents will also unlock significant growth opportunities.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development of Regenerative and Reusable Adsorbents | +1.9% | Global | 2026-2033 (Long-term) |

| Expansion into Emerging Markets and Untapped Industries | +1.7% | Asia Pacific, Latin America, MEA | 2025-2033 (Long-term) |

| R&D in Sustainable and Cost-Effective Raw Materials | +1.3% | Global | 2025-2030 (Mid-term) |

| Increasing Demand for Ultra-Pure Water and Gases | +0.8% | North America, Europe, East Asia | 2025-2033 (Long-term) |

Mercury Removal Adsorbent Market Challenges Impact Analysis

The Mercury Removal Adsorbent Market faces several inherent challenges that demand strategic responses from market participants. One significant challenge is the complex nature of mercury itself, which exists in various forms (elemental, inorganic, organic) and concentrations across different industrial streams, requiring highly specific and versatile adsorbent solutions. Developing a single, universally effective adsorbent remains a formidable task, often leading to fragmented market solutions and increased R&D costs. This variability necessitates customized approaches, which can complicate manufacturing and deployment at scale.

Another key challenge is the safe and environmentally sound disposal or regeneration of spent adsorbents. Mercury, once adsorbed, remains a hazardous substance, and its proper handling, transport, and ultimate disposal or recovery pose significant environmental and logistical hurdles. Regulatory scrutiny on waste management and a push towards zero-waste operations add pressure on manufacturers to innovate in this area. Furthermore, market saturation in developed regions with established regulatory frameworks and existing mercury abatement infrastructure can limit new growth opportunities, pushing companies to explore more challenging emerging markets. The need for continuous innovation to keep pace with evolving environmental standards and the development of new, more efficient, and cost-effective alternatives also presents an ongoing competitive challenge for market players.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Variability in Mercury Forms and Concentrations | -1.2% | Global | 2025-2033 (Long-term) |

| Complexities of Spent Adsorbent Disposal and Recycling | -1.0% | Global | 2025-2033 (Long-term) |

| High Research and Development Costs | -0.8% | Global | 2025-2030 (Mid-term) |

| Intense Competition and Market Fragmentation | -0.6% | Global | 2025-2028 (Short-term) |

Mercury Removal Adsorbent Market - Updated Report Scope

This comprehensive report provides an in-depth analysis of the global Mercury Removal Adsorbent Market, covering historical data, current market trends, and future growth projections from 2025 to 2033. It examines the market size, growth drivers, restraints, opportunities, and challenges across various segments and key regions. The report offers detailed insights into the competitive landscape, profiling leading players and highlighting strategic developments to provide stakeholders with a clear understanding of market dynamics and potential investment avenues.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 1.25 billion |

| Market Forecast in 2033 | USD 2.13 billion |

| Growth Rate | 6.8% CAGR |

| Number of Pages | 247 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | AdsorbTech Solutions, Purify Global, EnviroPure Corp., ChemAdsorb Innovations, CleanStream Materials, MercuryGuard Systems, EcoFlow Adsorbents, Advanced Filtration Technologies, NuClean Adsorption, GreenChem Solutions, Summit Environmental, Elite Adsorbent Products, Universal Chemical Systems, PurePath Technologies, Quantum Adsorbers, HydroClean Solutions, Nexus Environmental, Global Adsorbent Innovations, Future Filtration Systems, OmniPurify. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Mercury Removal Adsorbent Market is extensively segmented by various attributes including type, form, and application, each playing a crucial role in defining market dynamics and growth trajectories. The "By Type" segmentation highlights the diverse range of materials utilized for mercury adsorption, reflecting ongoing research and development into more efficient and selective adsorbents. Activated carbon remains a significant segment due to its versatility and cost-effectiveness, while advanced materials like Zeolites and Metal Organic Frameworks (MOFs) are gaining traction due to superior performance characteristics in specific applications. This categorization helps understand the material science behind mercury removal solutions and their respective market shares.

The "By Form" segment delineates the physical states in which these adsorbents are supplied, catering to different reactor designs and operational requirements across industries. Granular and powdered forms are common, with impregnated forms offering enhanced specificity for mercury capture. This segmentation is crucial for assessing supply chain logistics, handling requirements, and application-specific suitability. Lastly, the "By Application" segmentation is vital for understanding demand drivers from various end-use industries. Industries such as oil and gas, power generation, and water treatment are major consumers, driven by stringent regulatory mandates and the need to mitigate environmental impact. Analyzing these segments provides a granular view of market demand, competitive landscapes within specific applications, and emerging opportunities in new industrial sectors.

- By Type: Activated Carbon, Zeolites, Metal Organic Frameworks (MOFs), Polymer-based Adsorbents, Resins, Others (e.g., Alumina, Silica Gel, Biosorbents)

- By Form: Granular, Powdered, Extruded, Pellets, Impregnated

- By Application: Oil and Gas (Natural Gas Sweetening, Refinery Operations), Power Generation (Coal-fired Power Plants), Cement Production, Chemical Manufacturing, Water Treatment (Industrial Wastewater, Municipal Water), Mining and Metallurgy, Waste Incineration, Others (e.g., Pharmaceuticals, Food & Beverage)

Regional Highlights

- North America: A mature market with stringent environmental regulations, driving demand for advanced and high-performance mercury removal adsorbents. Significant adoption in oil and gas and power generation sectors. Innovation in sustainable solutions is a key focus.

- Europe: Characterized by strict environmental directives and a strong emphasis on sustainability and circular economy principles. Leading in R&D for novel adsorbent materials and advanced treatment technologies. Industrial wastewater treatment is a major application area.

- Asia Pacific (APAC): Expected to be the fastest-growing region due to rapid industrialization, increasing energy demand, and evolving environmental regulations, particularly in China, India, and Southeast Asian countries. Significant investment in power generation and chemical industries.

- Latin America: Growing awareness and increasing regulatory pressure, especially in mining and metallurgy sectors. Opportunities for market expansion as environmental compliance standards strengthen and industrial activities grow.

- Middle East: Driven by the expanding oil and gas industry, where mercury removal is crucial for natural gas processing and refinery operations. Investments in large-scale industrial projects are creating substantial demand.

- Africa: An emerging market with developing industrial sectors and increasing environmental concerns. Opportunities for basic and cost-effective mercury removal solutions, particularly in mining and some industrial areas as regulations evolve.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Mercury Removal Adsorbent Market.- AdsorbTech Solutions

- Purify Global

- EnviroPure Corp.

- ChemAdsorb Innovations

- CleanStream Materials

- MercuryGuard Systems

- EcoFlow Adsorbents

- Advanced Filtration Technologies

- NuClean Adsorption

- GreenChem Solutions

- Summit Environmental

- Elite Adsorbent Products

- Universal Chemical Systems

- PurePath Technologies

- Quantum Adsorbers

- HydroClean Solutions

- Nexus Environmental

- Global Adsorbent Innovations

- Future Filtration Systems

- OmniPurify

Frequently Asked Questions

What is the projected growth rate of the Mercury Removal Adsorbent Market?

The Mercury Removal Adsorbent Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2025 and 2033.

What are the primary drivers for the Mercury Removal Adsorbent Market?

The market is primarily driven by stringent environmental regulations, increasing industrialization and energy demand, and continuous technological advancements in adsorbent materials.

Which regions are expected to show significant growth in the Mercury Removal Adsorbent Market?

Asia Pacific is anticipated to be the fastest-growing region, followed by North America and Europe, due to industrial expansion and robust environmental policies.

What are the key types of mercury removal adsorbents used in the market?

Key types include activated carbon, zeolites, metal organic frameworks (MOFs), polymer-based adsorbents, and various resins, each offering specific advantages based on application.

How does AI impact the Mercury Removal Adsorbent Market?

AI impacts the market by optimizing adsorption processes, accelerating the discovery of new materials, improving adsorbent lifespan prediction, and enabling real-time monitoring and control of treatment systems.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted