Medium speed Marine Diesel Engine Market

Medium speed Marine Diesel Engine Market Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_707575 | Last Updated : September 08, 2025 |

Format : ![]()

![]()

![]()

![]()

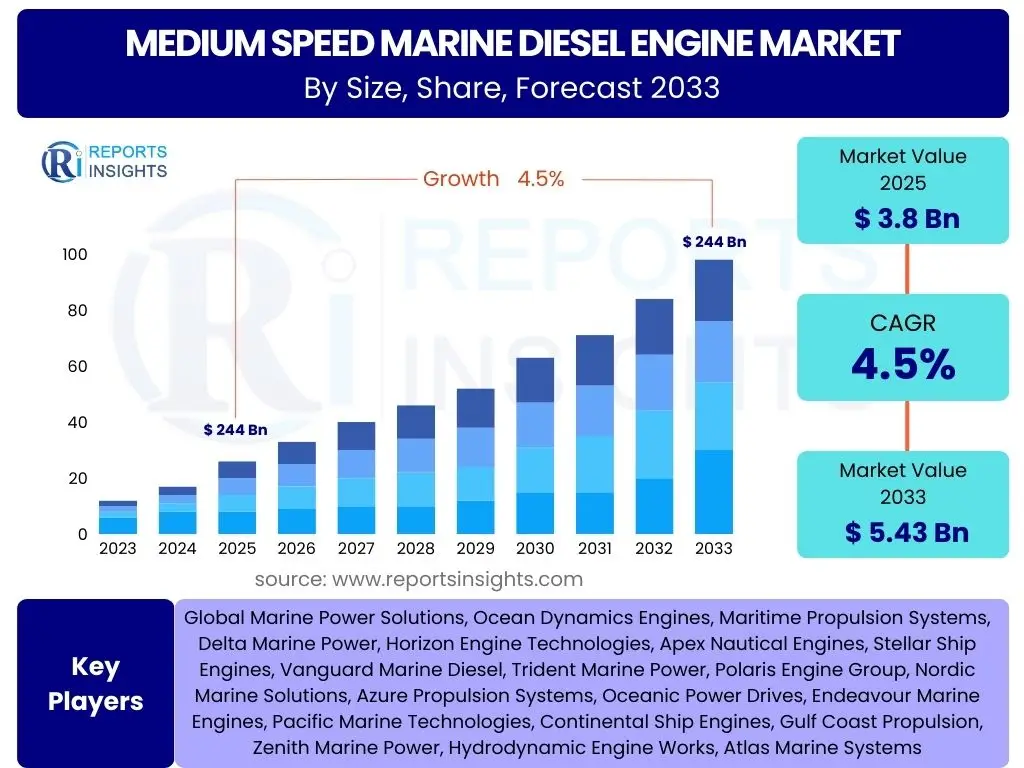

Medium speed Marine Diesel Engine Market Size

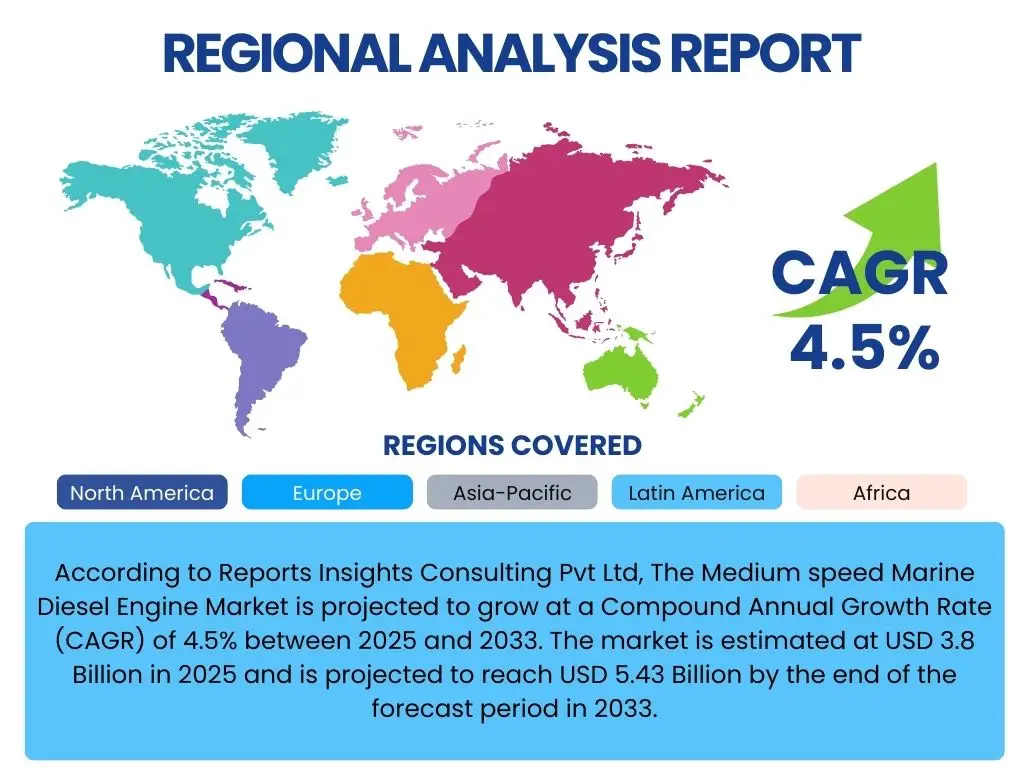

According to Reports Insights Consulting Pvt Ltd, The Medium speed Marine Diesel Engine Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 4.5% between 2025 and 2033. The market is estimated at USD 3.8 Billion in 2025 and is projected to reach USD 5.43 Billion by the end of the forecast period in 2033.

Key Medium speed Marine Diesel Engine Market Trends & Insights

User inquiries frequently center on the evolving technological landscape and sustainability pressures impacting the medium speed marine diesel engine sector. There is significant interest in how regulatory frameworks, particularly those related to emissions, are shaping engine design and fuel choices. Furthermore, the push towards digitalization and smart engine solutions is a recurring theme, highlighting the industry's shift towards optimized performance and predictive maintenance. These trends collectively underscore a transformative period for marine propulsion.

The market is witnessing a notable pivot towards multi-fuel and dual-fuel engine technologies, driven by stringent environmental regulations and the volatile nature of fossil fuel prices. Operators are increasingly investing in engines capable of running on traditional fuels alongside cleaner alternatives such as LNG, methanol, and potentially ammonia, to ensure compliance and operational flexibility. This trend is not merely about fuel diversification but also about enhancing engine efficiency and reducing the overall carbon footprint of maritime operations.

- Increased adoption of dual-fuel and multi-fuel engine technologies for emission compliance.

- Growing demand for engines compatible with alternative fuels like LNG, methanol, and potentially ammonia.

- Integration of advanced digital solutions for engine monitoring, diagnostics, and predictive maintenance.

- Focus on energy efficiency improvements and waste heat recovery systems.

- Modular design approaches for easier maintenance and upgrades.

- Development of hybrid propulsion systems combining diesel with electric or battery power.

AI Impact Analysis on Medium speed Marine Diesel Engine

Common user questions regarding AI's impact on medium speed marine diesel engines revolve around enhanced operational efficiency, predictive maintenance capabilities, and optimized fuel consumption. Users are keen to understand how artificial intelligence can transform traditional engine management practices, moving beyond reactive repairs to proactive interventions. There is also a strong interest in AI's role in autonomous vessel operations and its contribution to improving safety and reducing human error in complex maritime environments.

The application of AI in the medium speed marine diesel engine sector promises a paradigm shift in engine performance management. AI-powered analytics can process vast amounts of sensor data from engines, identifying subtle patterns indicative of impending failures or inefficiencies long before they become critical. This capability not only reduces costly downtime and extends engine lifespan but also optimizes fuel burn rates by dynamically adjusting engine parameters based on real-time operational conditions and environmental factors. Furthermore, AI contributes significantly to crew training and decision support systems, fostering a safer and more efficient maritime ecosystem.

- Predictive maintenance and fault detection through AI-driven analytics.

- Optimized fuel efficiency via real-time adaptive engine control systems.

- Enhanced operational decision-making support for vessel operators.

- Automated engine performance monitoring and anomaly detection.

- Improved safety and reduced human error in engine room operations.

Key Takeaways Medium speed Marine Diesel Engine Market Size & Forecast

User queries about market size and forecast often highlight a desire to understand the underlying drivers of growth and the long-term sustainability of traditional engine technologies amidst environmental pressures. Insights into the projected market expansion underscore the continued reliance on medium speed marine diesel engines for various vessel types, even as the industry transitions towards greener solutions. The forecast suggests resilience and adaptation, with innovation focused on fuel flexibility and operational efficiency being central to market evolution.

The market for medium speed marine diesel engines is poised for steady growth, reflecting continued new build orders in commercial shipping and ongoing demand for robust, reliable propulsion systems. While environmental regulations pose significant challenges, they also serve as catalysts for innovation, driving manufacturers to develop more efficient and environmentally compliant engine technologies. The substantial market valuation anticipated by 2033 indicates that these engines will remain a critical component of global maritime transport infrastructure, albeit with significant technological advancements. The emphasis on lifecycle cost reduction and enhanced operational uptime is also a key factor contributing to their enduring appeal.

- Steady market growth driven by global trade expansion and fleet renewal.

- Innovation in engine design is critical for regulatory compliance and competitive advantage.

- Dual-fuel technology is a primary enabler for future market expansion.

- Asia Pacific is expected to remain a dominant region for engine manufacturing and demand.

- Predictive maintenance and digitalization are becoming standard for operational efficiency.

Medium speed Marine Diesel Engine Market Drivers Analysis

The global medium speed marine diesel engine market is propelled by several robust factors, primarily the consistent growth in seaborne trade and the subsequent demand for new vessel constructions and fleet modernizations. As international commerce expands, the need for efficient and powerful propulsion systems to transport goods across oceans intensifies. This fundamental demand underpins the market's trajectory, ensuring a stable environment for engine manufacturers and service providers.

Furthermore, advancements in engine technology, particularly those enhancing fuel efficiency and reducing emissions, are significant drivers. Stricter environmental regulations from organizations like the IMO necessitate the development and adoption of engines capable of meeting EEDI and NOx emission standards, pushing innovation. The shift towards alternative fuels and dual-fuel engines also opens new market segments and opportunities for growth, positioning technological evolution as a critical market stimulant.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growth in Seaborne Trade & New Ship Building Orders | +1.2% | Global, particularly Asia Pacific (China, South Korea, Japan) | 2025-2033 |

| Stringent Environmental Regulations (IMO 2020, EEDI, EEXI) | +0.9% | Global, particularly Europe, North America, key shipping lanes | 2025-2030 |

| Technological Advancements in Fuel Efficiency & Dual-Fuel Engines | +1.0% | Global, especially technology-leading regions (Europe, Japan) | 2025-2033 |

| Increasing Demand for Cruise & Passenger Vessels | +0.7% | Europe, North America, Asia Pacific | 2026-2033 |

Medium speed Marine Diesel Engine Market Restraints Analysis

Despite positive growth drivers, the medium speed marine diesel engine market faces several restraints that could temper its expansion. One significant challenge is the volatility of fuel prices, particularly traditional marine fuels like HFO and MGO. Unpredictable fluctuations can impact operational costs for vessel operators, leading to deferrals in new engine investments or conversions, as companies weigh the economic viability of different propulsion solutions. This uncertainty often necessitates careful financial planning and risk assessment for both engine manufacturers and their clients.

Another major restraint is the escalating capital expenditure required for adopting new, more complex engine technologies, especially those supporting alternative fuels. While these technologies offer long-term environmental and operational benefits, their initial investment costs can be prohibitive for some smaller or medium-sized shipping companies. Furthermore, the global economic slowdowns or geopolitical uncertainties can impact trade volumes and shipbuilding activities, indirectly constraining the demand for marine engines. The nascent stage of alternative fuel infrastructure development also poses a hurdle, limiting the widespread adoption of next-generation engines.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Capital Expenditure for Advanced Engine Technologies | -0.8% | Global | 2025-2030 |

| Volatility in Crude Oil & Marine Fuel Prices | -0.6% | Global | 2025-2033 |

| Slow Development of Alternative Fuel Bunkering Infrastructure | -0.7% | Developing Regions, Specific Ports Globally | 2025-2030 |

| Economic Slowdown & Geopolitical Instabilities | -0.5% | Global, Impacted Regions Vary | Short-term to Mid-term (2025-2028) |

Medium speed Marine Diesel Engine Market Opportunities Analysis

Significant opportunities exist within the medium speed marine diesel engine market, primarily stemming from the accelerating global shift towards decarbonization and sustainable maritime practices. This presents a substantial opening for manufacturers specializing in engines compatible with emerging low-carbon fuels such as ammonia and hydrogen, beyond the current focus on LNG and methanol. Companies that invest early in the research, development, and commercialization of these future-proof engine solutions stand to gain a competitive edge and capture new market segments as regulations tighten and sustainability goals become paramount for shipping lines.

Another key opportunity lies in the burgeoning market for engine retrofits and conversions. As older vessels seek to comply with new emission standards without the significant investment of new builds, the demand for converting existing engines to dual-fuel capabilities or upgrading them with advanced emission reduction technologies is projected to surge. This segment offers a continuous revenue stream independent of new shipbuilding cycles. Furthermore, the integration of digital twin technology, IoT, and AI for enhanced operational efficiency and predictive maintenance offers lucrative avenues for service providers and technology innovators within the marine engine ecosystem.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development & Adoption of Ammonia/Hydrogen-Ready Engines | +1.1% | Global, particularly Europe, East Asia | 2028-2033 |

| Increased Demand for Engine Retrofits & Conversions for Emission Compliance | +0.9% | Global, especially established shipping fleets | 2025-2033 |

| Growth in Offshore Wind Farm Support Vessels | +0.8% | Europe, North Sea, East Asia (offshore wind development) | 2025-2033 |

| Leveraging Digitalization (IoT, AI) for Engine Optimization & Service | +0.7% | Global | 2025-2033 |

Medium speed Marine Diesel Engine Market Challenges Impact Analysis

The medium speed marine diesel engine market faces formidable challenges, primarily the significant uncertainty surrounding future fuel pathways and the necessary infrastructure development. While alternative fuels are gaining traction, the lack of a universally agreed-upon dominant green fuel and the massive investment required for global bunkering and supply chains create hesitation among shipowners and engine manufacturers. This indecision can slow down innovation and adoption, as stakeholders await clearer signals on long-term sustainable solutions, impacting investment cycles and market stability.

Another critical challenge is the intense competition from alternative propulsion technologies, including fully electric, hybrid, and potentially nuclear options for certain vessel types. Although medium speed diesel remains highly versatile and robust, the ongoing development of these alternative systems poses a long-term threat by potentially eroding its market share in specific segments. Furthermore, the complexity of integrating advanced emission reduction systems (e.g., SCR, scrubbers) and new fuel handling systems adds to engine design and manufacturing costs, which can ultimately be passed on to customers, affecting affordability and market competitiveness.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Uncertainty in Future Fuel Landscape & Infrastructure Development | -0.9% | Global | 2025-2035 |

| Competition from Alternative Propulsion Technologies | -0.7% | Global, specific vessel segments | 2027-2033 |

| High Research & Development Costs for Compliance & New Fuels | -0.6% | Global | 2025-2033 |

| Shortage of Skilled Labor for New Technologies & Maintenance | -0.5% | Global, particularly Europe, North America | 2025-2033 |

Medium speed Marine Diesel Engine Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the Medium speed Marine Diesel Engine Market, segmenting it by various critical parameters to offer a granular view of market dynamics. It covers historical data from 2019 to 2023, establishes 2024 as the base year, and projects market trends and values up to 2033. The report meticulously details market size, growth drivers, restraints, opportunities, and challenges, alongside a thorough regional analysis. It also includes profiles of key market players, competitive landscape insights, and an assessment of emerging technologies and regulatory impacts, offering a holistic perspective for stakeholders.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 3.8 Billion |

| Market Forecast in 2033 | USD 5.43 Billion |

| Growth Rate | 4.5% |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Global Marine Power Solutions, Ocean Dynamics Engines, Maritime Propulsion Systems, Delta Marine Power, Horizon Engine Technologies, Apex Nautical Engines, Stellar Ship Engines, Vanguard Marine Diesel, Trident Marine Power, Polaris Engine Group, Nordic Marine Solutions, Azure Propulsion Systems, Oceanic Power Drives, Endeavour Marine Engines, Pacific Marine Technologies, Continental Ship Engines, Gulf Coast Propulsion, Zenith Marine Power, Hydrodynamic Engine Works, Atlas Marine Systems |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The medium speed marine diesel engine market is comprehensively segmented to provide a detailed understanding of its diverse applications and technological nuances. This segmentation highlights the various end-use industries, vessel types, fuel preferences, and power output ranges that characterize the demand for these engines. By breaking down the market into these specific categories, the report offers stakeholders clear insights into the areas of highest growth potential and technological development, facilitating targeted business strategies and investment decisions. The differentiation by fuel type, in particular, underscores the industry's active transition towards cleaner energy solutions, driven by global environmental mandates.

- By Application: Commercial vessels, naval vessels, and onboard power generation represent the primary use cases. Commercial vessels further segmented into cargo ships (container, bulk carrier, tanker, general cargo), passenger vessels (cruise liners, ferries), fishing vessels, tugboats & workboats, and offshore support vessels.

- By Fuel Type: Includes traditional heavy fuel oil (HFO) and marine gas oil (MGO), alongside cleaner alternatives such as liquefied natural gas (LNG), methanol, biofuels, and other emerging fuels like hydrogen-ready and ammonia-ready solutions.

- By Power Output: Categorizes engines based on their power capacity, specifically 1,000 kW - 3,000 kW, 3,001 kW - 6,000 kW, and 6,001 kW - 10,000 kW, reflecting different vessel sizes and operational requirements.

- By End-Use Industry: Encompasses shipping & logistics, oil & gas, naval & defense, tourism & passenger transport, and fishing & aquaculture, identifying the sectors driving demand.

Regional Highlights

- Asia Pacific (APAC): Dominates the market due to its robust shipbuilding industry, particularly in China, South Korea, and Japan. The region also experiences significant growth in seaborne trade and investments in modernizing its commercial fleet, driving demand for medium speed marine diesel engines. Regulatory pressures for emission reduction are also stimulating the adoption of advanced engine technologies.

- Europe: A key region for technological innovation and early adoption of alternative fuels. European manufacturers are at the forefront of developing dual-fuel and multi-fuel engines. Strict environmental regulations and a strong maritime tradition contribute to a steady demand for high-efficiency and low-emission engines, especially for cruise liners, ferries, and specialized vessels.

- North America: Exhibits stable demand, primarily driven by fleet renewal, offshore support vessel operations, and increasing cruise tourism. The region is also investing in infrastructure for LNG bunkering, supporting the transition to cleaner fuel options for marine propulsion. Compliance with regional emission control areas (ECAs) influences engine selection and retrofit activities.

- Latin America: Expected to show gradual growth, fueled by increasing seaborne trade activities and investments in its port infrastructure. The demand here is largely for cargo vessels, fishing fleets, and offshore support vessels related to oil and gas exploration. Economic stability and governmental support for maritime industries will be crucial for sustained market expansion.

- Middle East & Africa (MEA): Growing due to expanding trade routes, investments in oil & gas exploration, and a developing maritime logistics sector. The demand for medium speed marine diesel engines is primarily from offshore support vessels, tankers, and general cargo ships. Infrastructure development for alternative fuels is still in early stages but presents future opportunities.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Medium speed Marine Diesel Engine Market.- Global Marine Power Solutions

- Ocean Dynamics Engines

- Maritime Propulsion Systems

- Delta Marine Power

- Horizon Engine Technologies

- Apex Nautical Engines

- Stellar Ship Engines

- Vanguard Marine Diesel

- Trident Marine Power

- Polaris Engine Group

- Nordic Marine Solutions

- Azure Propulsion Systems

- Oceanic Power Drives

- Endeavour Marine Engines

- Pacific Marine Technologies

- Continental Ship Engines

- Gulf Coast Propulsion

- Zenith Marine Power

- Hydrodynamic Engine Works

- Atlas Marine Systems

Frequently Asked Questions

What is the projected growth rate of the Medium speed Marine Diesel Engine Market?

The Medium speed Marine Diesel Engine Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 4.5% between 2025 and 2033, driven by increasing seaborne trade and technological advancements.

What are the key trends shaping the Medium speed Marine Diesel Engine Market?

Key trends include the increased adoption of dual-fuel and multi-fuel engine technologies, integration of digital solutions for engine monitoring, focus on energy efficiency, and the development of engines compatible with alternative fuels like LNG, methanol, and future ammonia/hydrogen fuels.

How will AI impact the Medium speed Marine Diesel Engine Market?

AI is expected to significantly enhance predictive maintenance capabilities, optimize fuel efficiency through real-time adaptive control, improve operational decision-making, and automate engine performance monitoring, leading to reduced downtime and increased reliability.

What are the main drivers for market growth?

The primary drivers are the consistent growth in global seaborne trade, the demand for new shipbuilding orders and fleet modernizations, and the stringent environmental regulations compelling the adoption of more efficient and compliant engine technologies, including dual-fuel systems.

Which regions are leading in the Medium speed Marine Diesel Engine Market?

Asia Pacific currently dominates the market due to its robust shipbuilding industry, while Europe leads in technological innovation and the early adoption of advanced, environmentally compliant engine solutions.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted