Wind Turbine Rotor Blade Market

Wind Turbine Rotor Blade Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_678293 | Last Updated : July 21, 2025 |

Format : ![]()

![]()

![]()

![]()

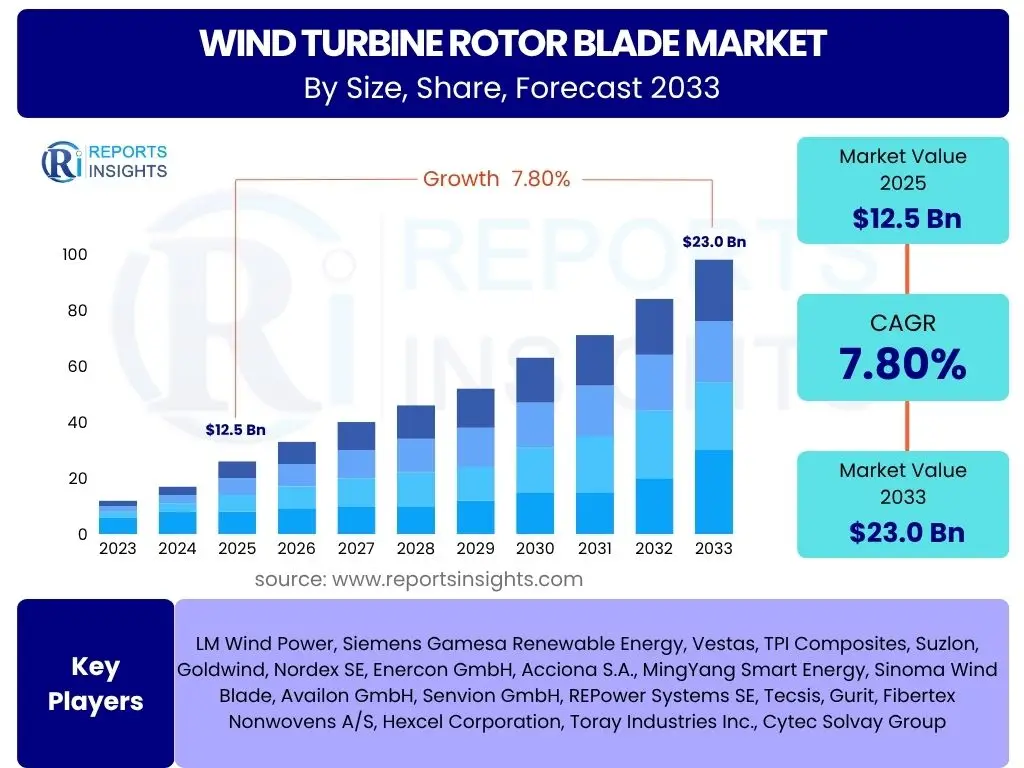

Wind Turbine Rotor Blade Market is projected to grow at a Compound annual growth rate (CAGR) of 7.5% between 2025 and 2033, reaching USD 15.2 billion in 2025 and is projected to grow by USD 27.2 billion by 2033 the end of the forecast period.

Key Wind Turbine Rotor Blade Market Trends & Insights

The wind turbine rotor blade market is experiencing dynamic shifts driven by advancements in material science, increasing demand for renewable energy, and evolving design philosophies. A prominent trend is the development of longer and more efficient blades, enabling turbines to capture more wind energy, especially in lower wind speed regions. This shift necessitates innovations in composite materials, manufacturing techniques, and logistics to handle these larger structures. Furthermore, the focus on sustainability extends to the entire lifecycle of blades, propelling research into recyclable resins and blade recycling technologies to address environmental concerns associated with end-of-life disposal.

Another significant trend is the rapid expansion of offshore wind power, which demands specialized blades capable of withstanding harsh marine environments and extreme weather conditions. These blades are often larger and require enhanced durability and corrosion resistance. Digitalization and predictive maintenance are also gaining traction, with sensors embedded in blades to monitor performance, detect anomalies, and optimize maintenance schedules, thereby maximizing operational efficiency and lifespan. Lastly, there's a growing emphasis on modular blade designs and segmented blades to overcome transportation challenges for increasingly large components, facilitating broader deployment in diverse geographical locations.

- Increased blade length for enhanced energy capture.

- Advanced composite materials and manufacturing processes.

- Growing focus on blade recyclability and sustainable materials.

- Expansion of offshore wind demanding specialized, robust blades.

- Integration of digital technologies for monitoring and predictive maintenance.

- Development of modular and segmented blade designs to ease transportation.

AI Impact Analysis on Wind Turbine Rotor Blade

Artificial Intelligence (AI) is set to revolutionize various aspects of the wind turbine rotor blade lifecycle, from design and manufacturing to operation and maintenance. In the design phase, AI-powered simulations can rapidly optimize aerodynamic profiles and structural integrity, significantly reducing development time and costs while improving blade efficiency. Generative design algorithms can explore thousands of permutations to identify optimal material combinations and geometries for specific site conditions, pushing the boundaries of what is conventionally achievable. This predictive capability allows manufacturers to create blades that are not only more efficient but also inherently more resilient and durable.

During operation, AI-driven analytics can process vast amounts of sensor data collected from installed blades to provide real-time performance monitoring and predictive failure analysis. This allows for proactive maintenance, minimizing downtime and extending the operational lifespan of the blades. AI can also optimize turbine pitch and yaw in response to changing wind conditions, further maximizing energy capture. Furthermore, AI contributes to quality control in manufacturing by identifying defects with high precision and automating inspection processes, ensuring consistent product quality and reducing waste. The integration of AI tools promises a leap forward in both the performance and cost-effectiveness of wind turbine rotor blades across their entire value chain.

- AI-driven optimization of aerodynamic design and structural integrity.

- Predictive maintenance and anomaly detection using real-time sensor data.

- Enhanced operational efficiency through AI-optimized turbine control.

- Automated quality control and defect detection in manufacturing.

- Accelerated research and development of new blade materials and designs.

Key Takeaways Wind Turbine Rotor Blade Market Size & Forecast

- Market value projected to reach USD 15.2 billion in 2025.

- Anticipated market expansion to USD 27.2 billion by 2033.

- Compound Annual Growth Rate (CAGR) estimated at 7.5% from 2025 to 2033.

- Significant growth propelled by global renewable energy initiatives.

- Technological advancements in blade design and materials are key growth catalysts.

- Offshore wind segment expected to contribute substantially to market size.

- Market expansion driven by increased demand for larger, more efficient turbines.

Wind Turbine Rotor Blade Market Drivers Impact Analysis

The wind turbine rotor blade market is significantly influenced by several powerful drivers, primarily the global imperative for renewable energy and supportive governmental policies. Increasing awareness of climate change and the need to reduce carbon emissions are driving substantial investments in wind power projects worldwide. This foundational shift towards sustainable energy sources directly translates into higher demand for wind turbines and, consequently, their essential components like rotor blades. Furthermore, continuous technological advancements in blade design and materials science are enhancing turbine efficiency and cost-effectiveness, making wind energy an increasingly attractive and competitive power generation option. These factors collectively create a robust growth environment for the market, fostering innovation and expansion.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Global Push for Renewable Energy Adoption | +2.5% | Global, especially Europe, North America, APAC | Long-term (2025-2033) |

| Favorable Government Policies and Incentives | +2.0% | China, USA, EU Member States, India | Medium to Long-term |

| Technological Advancements in Blade Design and Materials | +1.5% | Global, R&D centers in Europe, USA, China | Continuous, Medium to Long-term |

| Increasing Demand for Offshore Wind Power | +1.0% | Europe (North Sea), East Asia (China, Japan, South Korea), USA | Medium to Long-term |

| Rising Global Electricity Consumption | +0.5% | Emerging economies, Global | Long-term |

Wind Turbine Rotor Blade Market Restraints Impact Analysis

Despite robust growth prospects, the wind turbine rotor blade market faces certain restraints that could temper its expansion. One significant challenge is the high initial capital investment required for large-scale wind farm projects, including the cost of advanced rotor blades. This can be a barrier to entry for new players or slower adoption in developing regions with limited access to financing. Furthermore, the volatility in raw material prices, particularly for composite materials like carbon fiber and resin, can directly impact manufacturing costs and project viability, leading to unpredictable market conditions. Supply chain disruptions, often exacerbated by geopolitical events or global health crises, also pose a consistent threat by delaying production and delivery of essential components.

Another critical restraint is public opposition, sometimes referred to as 'Not In My Backyard' (NIMBY) syndrome, which can delay or halt wind farm developments due to concerns over visual impact, noise pollution, or effects on local wildlife. While continuous efforts are made to mitigate these concerns through improved design and siting, they remain a hurdle. Additionally, the inherent intermittency of wind as an energy source, requiring backup power solutions or advanced grid management, can impact the perceived reliability and thus the rate of adoption of wind power, indirectly affecting demand for rotor blades. Addressing these restraints effectively will be crucial for the sustained, accelerated growth of the market.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Initial Capital Investment for Wind Projects | -1.2% | Global, particularly emerging markets | Long-term |

| Volatile Raw Material Prices (e.g., resins, carbon fiber) | -1.0% | Global, supply chain dependent | Short to Medium-term |

| Logistical Challenges for Oversized Blade Transport | -0.8% | Regions with limited infrastructure, mountainous areas | Medium-term |

| Public Opposition and Permitting Delays | -0.7% | Dense population areas in Europe, North America | Project-specific, Long-term |

Wind Turbine Rotor Blade Market Opportunities Impact Analysis

The wind turbine rotor blade market is poised to capitalize on several significant opportunities that promise to accelerate its growth trajectory. The most prominent opportunity lies in the burgeoning offshore wind sector, which demands increasingly large and durable blades designed to withstand harsh marine environments. As nations invest heavily in expanding their offshore wind capacities, this segment will drive innovation in blade size, material strength, and corrosion resistance. Furthermore, the ongoing development of advanced composite materials, including thermoplastic composites and bio-based resins, offers opportunities for lighter, stronger, and more sustainable blades, addressing both performance and environmental concerns. These material breakthroughs can lead to more cost-effective manufacturing processes and extended blade lifespans.

Another substantial opportunity exists in the repowering of older wind farms. As turbines reach the end of their operational life or become less efficient compared to newer models, replacing existing blades with more advanced, longer, and aerodynamically superior designs can significantly boost energy output without requiring entirely new infrastructure. This presents a continuous aftermarket demand for high-performance blades. Lastly, the integration of wind power with emerging energy solutions, such as green hydrogen production or energy storage systems, broadens the applicability and economic viability of wind farms, indirectly creating more demand for their core components, including rotor blades. These forward-looking developments highlight multiple avenues for market expansion and value creation.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Rapid Growth of the Offshore Wind Energy Sector | +1.8% | Europe, East Asia, North America | Long-term |

| Advancements in Sustainable and Recyclable Materials | +1.5% | Global, R&D Hubs in Europe, USA | Medium to Long-term |

| Repowering and Modernization of Existing Wind Farms | +1.0% | Europe, North America, older wind markets | Medium-term |

| Expansion into Emerging Markets with Growing Energy Needs | +0.8% | India, Brazil, South Africa, Southeast Asia | Long-term |

| Integration with Green Hydrogen Production and Energy Storage | +0.6% | Global, policy-driven regions | Long-term |

Wind Turbine Rotor Blade Market Challenges Impact Analysis

The wind turbine rotor blade market, while promising, contends with several notable challenges that require strategic responses from manufacturers and stakeholders. A primary concern is the significant environmental impact associated with the disposal of end-of-life blades, which are typically made of thermoset composites that are difficult to recycle. This challenge is pushing the industry towards developing more sustainable, circular economy solutions, but it remains a complex hurdle. The increasing size of modern blades also presents considerable logistical and transportation challenges, as transporting these enormous components from manufacturing facilities to often remote wind farm sites requires specialized infrastructure and complex planning, impacting project timelines and costs.

Furthermore, maintaining the structural integrity and durability of blades in increasingly extreme weather conditions, particularly for offshore installations or regions prone to ice and lightning strikes, is a constant engineering challenge. Blade damage can lead to costly repairs and significant downtime, affecting the overall economics of wind power generation. Another key challenge involves the supply chain; securing consistent access to high-quality raw materials and specialized manufacturing equipment can be difficult, especially given global demand fluctuations and geopolitical tensions. Addressing these multifaceted challenges is essential for the sustained innovation and widespread adoption of wind turbine technology, ensuring the long-term viability and growth of the rotor blade market.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| End-of-Life Blade Recycling and Disposal | -1.5% | Global, particularly in mature wind markets | Long-term |

| Increasing Logistical Complexity of Oversized Components | -1.2% | Global, especially challenging terrains | Medium-term |

| Ensuring Durability in Extreme Weather Conditions | -1.0% | Offshore regions, cold climates, hurricane zones | Continuous |

| Maintaining Quality Control in Large-scale Production | -0.8% | Global, across manufacturing hubs | Continuous |

| Skilled Labor Shortage for Manufacturing and Installation | -0.7% | Global, specific technical roles | Medium to Long-term |

Wind Turbine Rotor Blade Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the Wind Turbine Rotor Blade Market, covering historical data, current market dynamics, and future projections. It offers strategic insights into market size, growth drivers, restraints, opportunities, and challenges affecting the industry. The report segments the market by product type, application, end-use industry, and region, offering a granular view of market performance across various dimensions. Key player analysis and competitive landscape assessment are included to provide a holistic understanding for business professionals seeking to make informed decisions in this rapidly evolving sector.

| Report Attributes | Report Details |

|---|---|

| Report Name | Wind Turbine Rotor Blade Market |

| Market Size in 2025 | USD 15.2 billion |

| Market Forecast in 2033 | USD 27.2 billion |

| Growth Rate | CAGR of 2025 to 2033 7.5% |

| Number of Pages | 250 |

| Key Companies Covered | China National Materials, Gamesa, General Electric, Siemens, Sinoi GMBH, Suzlon Energy, Vestas Wind Systems, Acciona, Enercon GMBH, Nordex, Powerblades GMBH, SGL Rotec GMBH |

| Segments Covered | By Type, By Application, By End-Use Industry, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Customization Scope | Avail customised purchase options to meet your exact research needs. Request For Customization |

Segmentation Analysis

: Market Product Type Segmentation:-- Glass Fiber

- Carbon Fiber

- Onshore Wind Turbines

- Offshore Wind Turbines

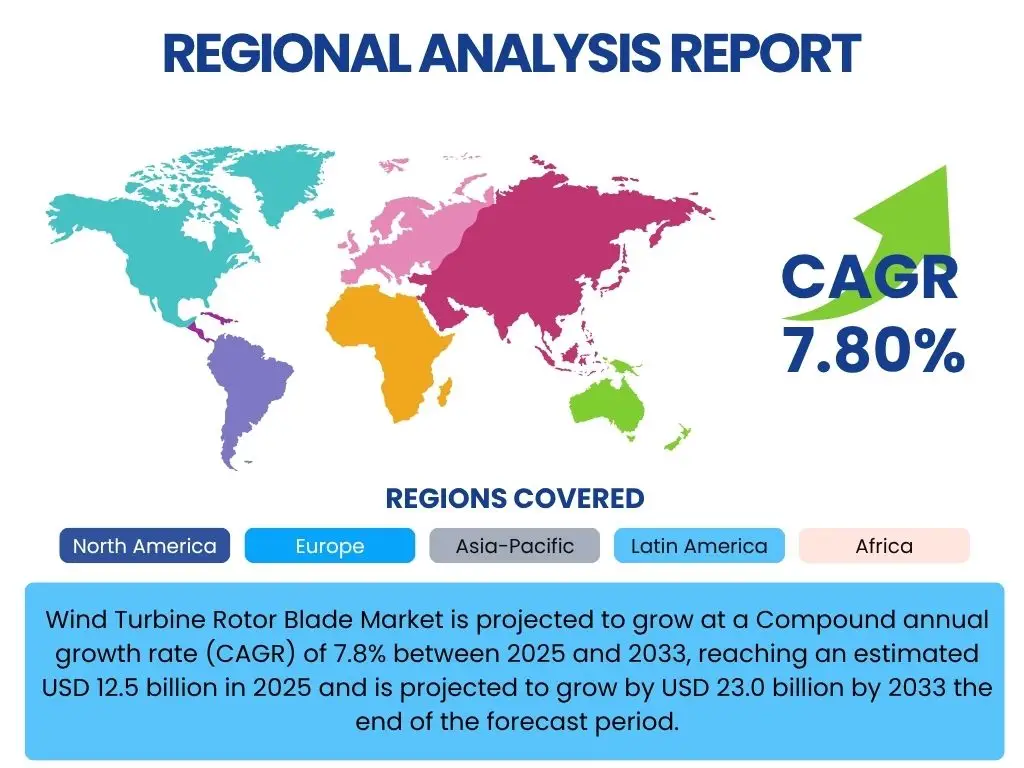

Regional Highlights

The global wind turbine rotor blade market exhibits diverse growth dynamics across key regions, driven by varying policy landscapes, energy demands, and technological advancements. Each region contributes uniquely to the market's overall trajectory, influencing demand, manufacturing capabilities, and innovation trends.

Asia Pacific (APAC) is projected to be the leading region in the wind turbine rotor blade market, primarily driven by robust investments in wind energy, especially in China and India. China, as the world's largest wind power market, continues to rapidly expand its onshore and offshore capacities, fueling immense demand for rotor blades. India is also significantly increasing its renewable energy portfolio, with wind power playing a crucial role, thereby contributing to the region's dominance. These countries benefit from supportive government policies, ambitious renewable energy targets, and a growing domestic manufacturing base, making them pivotal for market expansion.

Europe holds a significant share, characterized by its pioneering efforts in offshore wind technology and strong commitment to decarbonization. Countries like Germany, the United Kingdom, and Denmark are at the forefront of offshore wind farm development, requiring advanced and often larger rotor blades designed for challenging marine environments. The region's emphasis on innovation, sustainability, and supportive regulatory frameworks continues to drive demand for high-performance and recyclable blades. North America, particularly the United States, is another key region, with increasing investments in both onshore and emerging offshore wind projects. Favorable government incentives, coupled with an aging fossil fuel infrastructure, are accelerating the transition to wind energy, thereby boosting the demand for wind turbine rotor blades across the continent.

- Asia Pacific (APAC): Leading the market due to massive wind farm installations in China and India. China's ambitious targets for both onshore and offshore wind power, coupled with its robust manufacturing capabilities, make it a pivotal market. India's increasing energy demand and governmental push for renewables also contribute significantly.

- Europe: A major player, particularly in the offshore wind sector. Countries like Germany, the UK, and Denmark are driving demand for advanced, larger, and more durable blades for their extensive offshore projects. Strong regulatory support for renewable energy and a focus on circular economy principles influence material innovation.

- North America: Showing substantial growth, primarily in the United States. Policy initiatives such as tax credits and renewable portfolio standards are stimulating onshore wind development, while the emerging offshore wind market along the East Coast presents new opportunities for specialized blade designs.

- Latin America: Emerging as a growth region, with countries like Brazil, Mexico, and Chile investing in wind energy to diversify their power grids. The abundant wind resources in these regions, combined with efforts to attract foreign investment, are boosting demand for wind turbine components.

- Middle East & Africa (MEA): Gradually increasing its adoption of wind power as part of broader renewable energy diversification strategies. Countries like South Africa, Egypt, and Saudi Arabia are exploring large-scale wind projects, opening up future market potential for rotor blades, though currently at an earlier stage of development compared to other regions.

Top Key Players:

The market research report covers the analysis of key stake holders of the Wind Turbine Rotor Blade Market. Some of the leading players profiled in the report include -:- China National Materials

- Gamesa

- General Electric

- Siemens

- Sinoi GMBH

- Suzlon Energy

- Vestas Wind Systems

- Acciona

- Enercon GMBH

- Nordex

- Powerblades GMBH

- SGL Rotec GMBH

Frequently Asked Questions:

What are wind turbine rotor blades primarily made of?

Wind turbine rotor blades are predominantly made from composite materials, typically a blend of fiberglass or carbon fiber reinforced with thermoset resins like epoxy or polyester. These materials offer the optimal combination of lightweight strength, flexibility, and durability required to efficiently capture wind energy and withstand environmental stresses.

How long do wind turbine blades typically last?

Modern wind turbine blades are designed to have a lifespan of approximately 20 to 25 years. This duration can vary based on operational conditions, maintenance practices, and the specific design and materials used. Regular inspections and maintenance are crucial to achieving and extending this expected operational life.

What is the future outlook for wind turbine blade technology?

The future of wind turbine blade technology is characterized by increasing size for greater energy capture, advanced materials for enhanced strength and lighter weight, and a strong focus on sustainability. This includes the development of recyclable thermoplastic composites and modular blade designs to improve logistics and address end-of-life disposal challenges.

What are the key factors driving the growth of the wind turbine rotor blade market?

The key factors driving the growth of the wind turbine rotor blade market include the global shift towards renewable energy sources, supportive government policies and incentives for wind power development, continuous technological advancements leading to more efficient blade designs, and the rapid expansion of the offshore wind energy sector.

How does offshore wind energy impact wind turbine blade design?

Offshore wind energy significantly impacts blade design by necessitating larger, more robust blades capable of withstanding harsher marine environments, including stronger winds, salt corrosion, and more extreme weather conditions. These blades often feature enhanced structural integrity, specialized coatings, and designs optimized for maximizing energy capture in consistent offshore wind speeds.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted