Medical Terminology Software Market

Medical Terminology Software Market Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_706490 | Last Updated : September 08, 2025 |

Format : ![]()

![]()

![]()

![]()

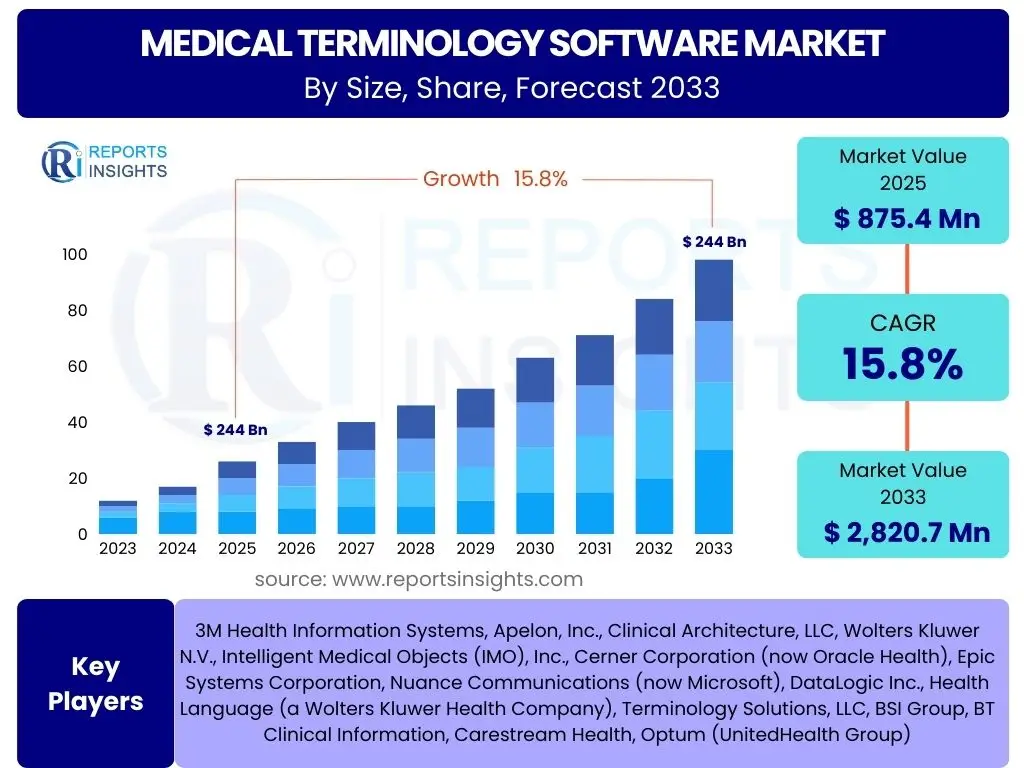

Medical Terminology Software Market Size

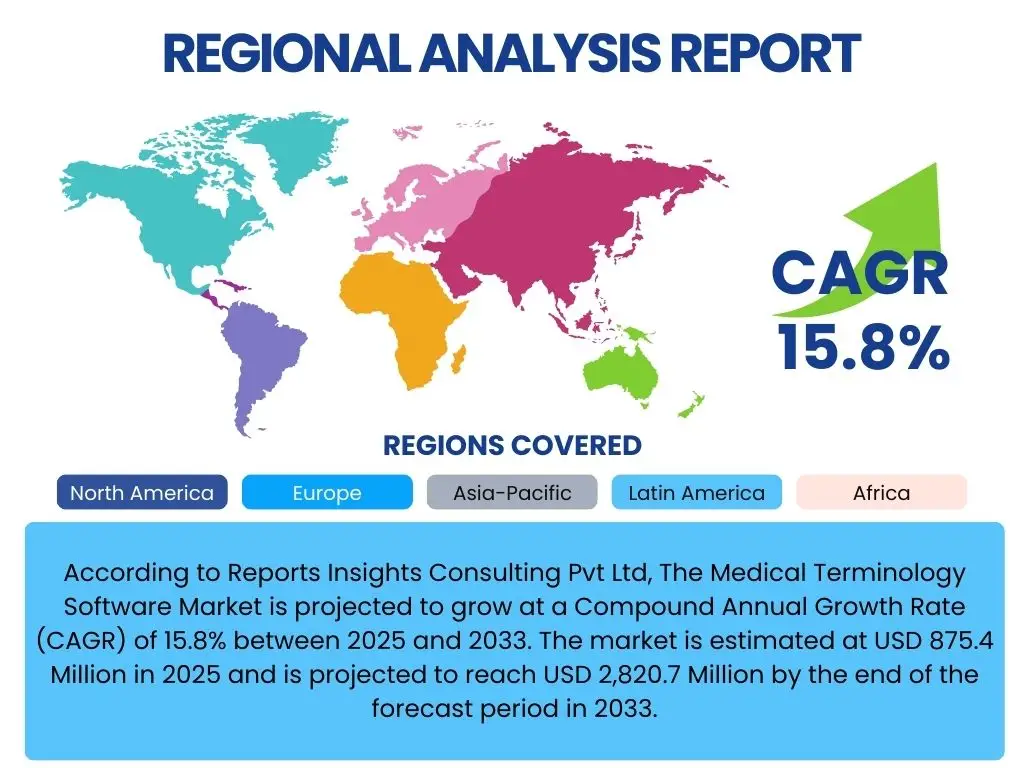

According to Reports Insights Consulting Pvt Ltd, The Medical Terminology Software Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 15.8% between 2025 and 2033. The market is estimated at USD 875.4 Million in 2025 and is projected to reach USD 2,820.7 Million by the end of the forecast period in 2033.

Key Medical Terminology Software Market Trends & Insights

The medical terminology software market is experiencing a significant transformation driven by the ongoing digitalization of healthcare and the increasing emphasis on accurate and standardized clinical data. Users frequently inquire about the latest technological advancements and operational shifts within this domain. A prominent trend involves the widespread adoption of cloud-based solutions, offering enhanced accessibility, scalability, and cost-effectiveness compared to traditional on-premise systems. This shift is crucial for supporting remote workforces and distributed healthcare networks, which have become more prevalent.

Another critical insight is the growing integration of artificial intelligence (AI) and natural language processing (NLP) into terminology software. This integration addresses the complex challenge of unstructured clinical data by enabling automated coding, improved data extraction from free-text notes, and enhanced clinical documentation accuracy. Furthermore, the market is heavily influenced by the imperative for interoperability among disparate healthcare information systems, pushing for greater adherence to standardized terminologies like SNOMED CT, ICD-10, and LOINC to facilitate seamless data exchange and reduce medical errors. The transition to value-based care models also drives demand, as precise terminology is foundational for accurate billing, outcomes measurement, and quality reporting.

- Increased adoption of cloud-based medical terminology solutions.

- Deep integration of AI and Natural Language Processing (NLP) for enhanced data processing.

- Growing demand for interoperability and data standardization across healthcare systems.

- Emphasis on clinical documentation improvement (CDI) and accurate medical coding.

- Shift towards value-based care models necessitating precise terminology for outcomes measurement.

AI Impact Analysis on Medical Terminology Software

User queries regarding the impact of AI on medical terminology software often revolve around its potential to automate complex tasks, improve accuracy, and streamline workflows. AI, particularly through advanced Natural Language Processing (NLP) and machine learning algorithms, is profoundly transforming how medical terminology is managed and applied. It enables the extraction of structured data from vast amounts of unstructured clinical text, such as physician notes, discharge summaries, and pathology reports. This capability significantly reduces the manual effort required for coding and documentation, thereby accelerating processes and mitigating human error. Furthermore, AI-powered systems can identify inconsistencies or ambiguities in documentation, prompting healthcare professionals for clarification and ensuring higher data quality.

The influence of AI extends to predictive analytics and decision support within the medical terminology landscape. AI models can analyze large datasets to identify patterns in disease progression, treatment efficacy, and patient outcomes, all of which rely on accurately coded medical terminology. This supports clinicians in making more informed decisions, enhancing diagnostic precision, and personalizing treatment plans. While AI offers immense potential for efficiency and accuracy, user concerns also touch upon the ethical implications, data privacy, and the need for human oversight to validate AI-generated insights and ensure fairness and transparency in automated processes. Overall, AI is seen as an augmenting force, enhancing the capabilities of medical terminology software rather than replacing human expertise entirely.

- Enhanced Natural Language Processing (NLP) for extracting structured data from clinical text.

- Automation of medical coding and abstracting processes, reducing manual effort and errors.

- Improved data quality and standardization through automated identification of inconsistencies.

- Support for clinical decision support systems by providing real-time, context-aware terminology insights.

- Facilitation of predictive analytics for disease patterns, treatment outcomes, and population health management.

Key Takeaways Medical Terminology Software Market Size & Forecast

Common user questions about the medical terminology software market size and forecast frequently center on the overall growth trajectory, the primary factors driving this growth, and the long-term outlook for investment and innovation. A key takeaway is the robust and sustained growth projected for this market, underpinned by the global push for digital transformation in healthcare. The imperative for accurate and standardized patient data, crucial for clinical decision-making, regulatory compliance, and revenue cycle management, is a fundamental driver. This necessitates advanced software solutions capable of managing complex and evolving medical terminologies efficiently.

Furthermore, the forecast indicates that technological advancements, particularly in AI and cloud computing, will continue to be pivotal in shaping market expansion. These innovations address core challenges such as data interoperability, documentation burden, and coding accuracy, making terminology software indispensable for modern healthcare operations. Stakeholders should recognize the critical role this technology plays in improving patient safety, optimizing operational efficiency, and supporting the transition to value-based healthcare models. The market's resilience and consistent demand stem from its foundational importance to nearly all aspects of contemporary healthcare delivery and research.

- The market is poised for strong, consistent growth throughout the forecast period.

- Digitalization of healthcare infrastructure is the primary catalyst for market expansion.

- Investment in AI and NLP capabilities will be critical for future market leadership.

- Regulatory frameworks and compliance requirements significantly influence adoption rates.

- Accurate data management and interoperability remain core value propositions for the software.

Medical Terminology Software Market Drivers Analysis

The Medical Terminology Software market is primarily driven by the escalating demand for highly accurate and standardized clinical documentation within the healthcare ecosystem. As healthcare systems globally transition towards digital health records and integrated platforms, the need for precise and unambiguous medical terminology becomes paramount. This precision is essential not only for patient safety and quality of care but also for operational efficiencies, including accurate billing, claims processing, and compliance with national and international health regulations. The increasing volume of patient data necessitates automated and sophisticated tools to manage, interpret, and apply complex medical codes and terms, thereby reducing manual errors and improving data integrity across various healthcare settings.

Another significant driver is the growing adoption of Electronic Health Records (EHRs) and Electronic Medical Records (EMRs) across hospitals, clinics, and other healthcare facilities. EHR systems are the backbone of modern healthcare information management, and their effectiveness is heavily reliant on the underlying medical terminology software for data entry, retrieval, and analysis. Furthermore, the global shift towards value-based care models, which emphasize patient outcomes and cost-efficiency over volume, requires meticulous data collection and analysis, making standardized terminology indispensable for performance measurement and reimbursement. The constant evolution of medical knowledge and the associated updates in coding standards, such as ICD-11 and SNOMED CT, also drive the continuous need for advanced terminology software solutions that can rapidly adapt and integrate these changes.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Demand for Accurate Clinical Documentation | +3.5% | Global | Short to Long Term |

| Growing Adoption of Electronic Health Records (EHRs) and EMRs | +3.0% | North America, Europe, APAC | Mid to Long Term |

| Need for Interoperability and Standardized Data Exchange | +2.8% | Global, particularly developed regions | Mid Term |

| Stringent Regulatory Mandates and Compliance Requirements | +2.5% | Global, varies by region | Ongoing |

| Shift Towards Value-Based Healthcare Models | +2.0% | North America, Europe | Long Term |

Medical Terminology Software Market Restraints Analysis

Despite the robust growth drivers, the Medical Terminology Software market faces several notable restraints that could impede its full potential. A primary challenge is the high initial investment and ongoing operational costs associated with implementing and maintaining sophisticated terminology software. Healthcare organizations, particularly smaller clinics and practices, often operate on constrained budgets, making the significant upfront expenditure for software licenses, hardware upgrades, and professional training a deterrent. Beyond initial costs, the continuous need for updates, maintenance, and expert support adds to the total cost of ownership, posing a financial burden that can slow adoption rates, especially in cost-sensitive regions or public healthcare systems.

Another significant restraint is the inherent complexity involved in integrating new terminology software with existing, often legacy, healthcare IT infrastructure. Many healthcare facilities have diverse, siloed systems for patient management, billing, and clinical operations, making seamless integration a formidable technical and logistical challenge. This complexity can lead to prolonged implementation cycles, data migration issues, and potential disruptions to clinical workflows, which healthcare providers are keen to avoid. Furthermore, resistance to change among healthcare professionals, who may be accustomed to traditional documentation methods or face steep learning curves with new software, also acts as a restraint. Data security and privacy concerns, particularly given the sensitive nature of patient health information, remain a persistent challenge, necessitating robust security measures and compliance with regulations like HIPAA and GDPR, adding layers of complexity and cost.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Initial Investment and Operational Costs | -2.5% | Global, particularly emerging economies | Short to Mid Term |

| Complexity of Integration with Legacy Systems | -2.0% | Global | Mid Term |

| Resistance to Adoption and Lack of Skilled Personnel | -1.8% | Global | Short Term |

| Data Security and Privacy Concerns | -1.5% | Global, particularly highly regulated regions | Ongoing |

| Interoperability Challenges Among Disparate Systems | -1.2% | Global | Mid Term |

Medical Terminology Software Market Opportunities Analysis

The Medical Terminology Software market is characterized by numerous untapped opportunities that can significantly fuel future growth. A major avenue for expansion lies in the increasing demand for specialized terminology management solutions within niche medical fields such as genomics, precision medicine, and rare diseases. As these areas advance, the need for highly specific and evolving terminologies to accurately describe complex genetic sequences, personalized treatments, and unique disease classifications becomes critical, opening new market segments for specialized software development. This specialization allows vendors to cater to bespoke requirements and offer high-value solutions beyond generic clinical coding.

Furthermore, the rapid growth of telehealth and remote patient monitoring services presents a substantial opportunity. These digital health initiatives generate vast amounts of real-time clinical data from diverse sources, necessitating robust terminology software to standardize and process this information for effective diagnosis, treatment, and follow-up. The global expansion into emerging economies, particularly in Asia Pacific and Latin America, also offers significant growth prospects. These regions are in the nascent stages of digitalizing their healthcare infrastructures, presenting a greenfield opportunity for medical terminology software providers to implement foundational systems and scale their operations. Strategic partnerships and collaborations with Electronic Health Record (EHR) vendors, healthcare IT providers, and medical device manufacturers can also unlock new distribution channels and facilitate broader market penetration by integrating terminology solutions directly into widely adopted platforms.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Expansion into Emerging Economies | +3.2% | APAC, Latin America, MEA | Long Term |

| Integration with Telehealth and Remote Monitoring Platforms | +2.9% | Global | Mid to Long Term |

| Development of Specialized Terminology for Niche Fields | +2.7% | Global | Long Term |

| Demand for Real-Time Analytics and Clinical Decision Support | +2.5% | Global | Mid Term |

| Strategic Partnerships with EHR Vendors and IT Providers | +2.3% | Global | Short to Mid Term |

Medical Terminology Software Market Challenges Impact Analysis

The Medical Terminology Software market faces several significant challenges that require strategic navigation for sustained growth and innovation. One key challenge is the continuous evolution and expansion of medical knowledge, which necessitates frequent updates and maintenance of terminology standards. Medical terminologies like SNOMED CT, ICD, and CPT are regularly revised and expanded to incorporate new diseases, procedures, and scientific discoveries. Ensuring that software solutions remain current and accurate with these dynamic standards is a complex and resource-intensive undertaking for vendors, directly impacting their development cycles and clients' operational continuity. This constant flux demands highly agile and adaptable software architectures.

Another critical challenge involves ensuring data quality and consistency across disparate healthcare information systems. Even with standardized terminology software, the actual application and coding practices can vary among different healthcare providers, leading to inconsistencies in data capture. This lack of uniformity complicates data aggregation, analysis, and interoperability efforts, undermining the core benefits of terminology management. Furthermore, as AI is increasingly integrated, addressing ethical considerations, such as algorithmic bias and data privacy in AI-driven coding and documentation, becomes paramount. Overcoming technical complexities related to data mapping, semantic interoperability, and the integration of diverse data sources also poses a considerable hurdle. Finally, navigating varied and evolving global regulatory frameworks, each with its own specific requirements for health data management and terminology use, adds another layer of complexity for providers seeking to expand internationally.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Maintaining Currency and Accuracy of Evolving Terminologies | -2.2% | Global | Ongoing |

| Ensuring Data Quality and Consistency Across Disparate Sources | -1.9% | Global | Mid Term |

| Addressing Ethical Considerations and Bias in AI Algorithms | -1.7% | Global | Long Term |

| Overcoming Technical Complexities in Data Standardization | -1.5% | Global | Mid Term |

| Navigating Varied and Evolving Global Regulatory Frameworks | -1.3% | Global, particularly cross-border operations | Ongoing |

Medical Terminology Software Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the Medical Terminology Software market, covering historical data, current market trends, and future growth projections from 2025 to 2033. The scope encompasses detailed segmentation by component, deployment, application, and end-user, offering a holistic view of market dynamics. It also includes a thorough examination of key drivers, restraints, opportunities, and challenges impacting market growth, along with regional insights and competitive landscape analysis.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 875.4 Million |

| Market Forecast in 2033 | USD 2,820.7 Million |

| Growth Rate | 15.8% |

| Number of Pages | 245 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | 3M Health Information Systems, Apelon, Inc., Clinical Architecture, LLC, Wolters Kluwer N.V., Intelligent Medical Objects (IMO), Inc., Cerner Corporation (now Oracle Health), Epic Systems Corporation, Nuance Communications (now Microsoft), DataLogic Inc., Health Language (a Wolters Kluwer Health Company), Terminology Solutions, LLC, BSI Group, BT Clinical Information, Carestream Health, Optum (UnitedHealth Group) |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The medical terminology software market is comprehensively segmented to provide a granular understanding of its diverse facets and varying demands across different applications and user groups. This segmentation helps in identifying specific growth pockets and tailoring solutions to meet specialized needs within the vast healthcare landscape. The market is primarily bifurcated by component into software and services, reflecting the complete ecosystem of offerings, from the core application to the crucial support and implementation services.

Further segmentation by deployment model differentiates between on-premise and cloud-based solutions, indicating the shift towards flexible, scalable cloud platforms. Application-wise, the market is segmented across critical healthcare functions such as clinical documentation, billing and coding, research and development, and health information management, highlighting the software's multifaceted utility. Lastly, end-user segmentation categorizes adoption across healthcare providers (hospitals, clinics), healthcare payers, life sciences companies, and academic and research institutions, showcasing the broad applicability of medical terminology software across the entire healthcare value chain.

- By Component:

- Software: Refers to the core applications and platforms.

- Services: Encompasses implementation, training, consulting, and maintenance.

- By Deployment:

- On-Premise: Software installed and operated on local servers within the organization.

- Cloud-Based: Software hosted on remote servers and accessed via the internet, offering scalability and flexibility.

- By Application:

- Clinical Documentation: For accurate and consistent patient record-keeping.

- Billing & Coding: To ensure precise medical claims processing and revenue cycle management.

- Research & Development: For standardizing data in clinical trials and biomedical research.

- Health Information Management (HIM): Comprehensive management of health data.

- Data Analytics & Reporting: For extracting insights and generating reports from clinical data.

- Others: Including applications in education and public health.

- By End User:

- Healthcare Providers: Hospitals, clinics, ambulatory surgical centers.

- Healthcare Payers: Insurance companies and managed care organizations.

- Life Sciences Companies: Pharmaceutical companies, biotechnology firms, contract research organizations (CROs).

- Academic & Research Institutions: Universities and medical research centers.

- Government Bodies: Health ministries and public health agencies.

Regional Highlights

- North America: Expected to dominate the medical terminology software market due to advanced healthcare infrastructure, high adoption rates of EHRs, stringent regulatory requirements for data standardization, and significant investments in digital health technologies. The presence of key market players and a strong focus on value-based care models further contributes to its leading position.

- Europe: Represents a substantial market share, driven by robust healthcare systems, increasing government initiatives for digital health adoption, and the widespread implementation of standardized terminologies such as SNOMED CT across member states. Emphasis on patient data privacy and interoperability also fuels market growth.

- Asia Pacific (APAC): Projected to exhibit the fastest growth rate during the forecast period. This growth is attributed to the rapidly expanding healthcare sector in countries like China, India, and Japan, increasing healthcare IT spending, rising awareness about the benefits of standardized medical data, and governmental support for digitalization initiatives.

- Latin America: Demonstrates steady growth, influenced by improving healthcare access, growing healthcare expenditure, and increasing awareness of digital health solutions. However, challenges related to infrastructure and budget constraints may temper rapid expansion compared to other regions.

- Middle East and Africa (MEA): Shows emerging potential, particularly in GCC countries, driven by significant government investments in healthcare infrastructure modernization and digital transformation. Increasing demand for efficient health information management systems and improving regulatory frameworks are key growth factors.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Medical Terminology Software Market.- 3M Health Information Systems

- Apelon, Inc.

- Clinical Architecture, LLC

- Wolters Kluwer N.V.

- Intelligent Medical Objects (IMO), Inc.

- Cerner Corporation (now Oracle Health)

- Epic Systems Corporation

- Nuance Communications (now Microsoft)

- DataLogic Inc.

- Health Language (a Wolters Kluwer Health Company)

- Terminology Solutions, LLC

- BSI Group

- BT Clinical Information

- Carestream Health

- Optum (UnitedHealth Group)

- Lexi-Comp, Inc.

- TheraDoc Inc.

- MedDRA MSSO

- Elsevier Inc.

- Orion Health Group Limited

Frequently Asked Questions

Analyze common user questions about the Medical Terminology Software market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is medical terminology software?

Medical terminology software is a specialized application designed to manage, standardize, and process clinical, administrative, and financial data using universally accepted medical codes and terms (e.g., ICD, SNOMED CT, CPT). It ensures accuracy and consistency in electronic health records, billing, research, and data exchange, crucial for efficient healthcare operations and interoperability.

How does AI enhance medical terminology software?

AI, particularly Natural Language Processing (NLP) and machine learning, significantly enhances medical terminology software by automating the extraction of structured data from unstructured clinical text, improving coding accuracy, and identifying inconsistencies. This leads to faster documentation, reduced errors, and better support for clinical decision-making and predictive analytics.

What are the primary benefits of using medical terminology software?

The primary benefits include improved accuracy and consistency in clinical documentation, streamlined billing and coding processes, enhanced data interoperability between disparate systems, reduced manual errors, and better support for regulatory compliance. It also facilitates advanced data analytics for research and population health management, leading to improved patient outcomes and operational efficiency.

What are the key challenges in adopting medical terminology software?

Key challenges involve high initial implementation costs, complexity of integrating with existing legacy IT infrastructures, potential resistance to change from healthcare professionals, and ongoing demands for maintaining updated terminology standards. Data security and privacy concerns, along with navigating evolving global regulatory frameworks, also pose significant hurdles.

Which industries or sectors primarily utilize medical terminology software?

Medical terminology software is primarily utilized by healthcare providers (hospitals, clinics, physician practices), healthcare payers (insurance companies), life sciences companies (pharmaceutical, biotech, CROs), academic and research institutions, and government health agencies. Its application spans clinical care, revenue cycle management, public health, and biomedical research.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted