Computational Medicine and Drug Discovery Software Market

Computational Medicine and Drug Discovery Software Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_702262 | Last Updated : July 31, 2025 |

Format : ![]()

![]()

![]()

![]()

Computational Medicine and Drug Discovery Software Market Size

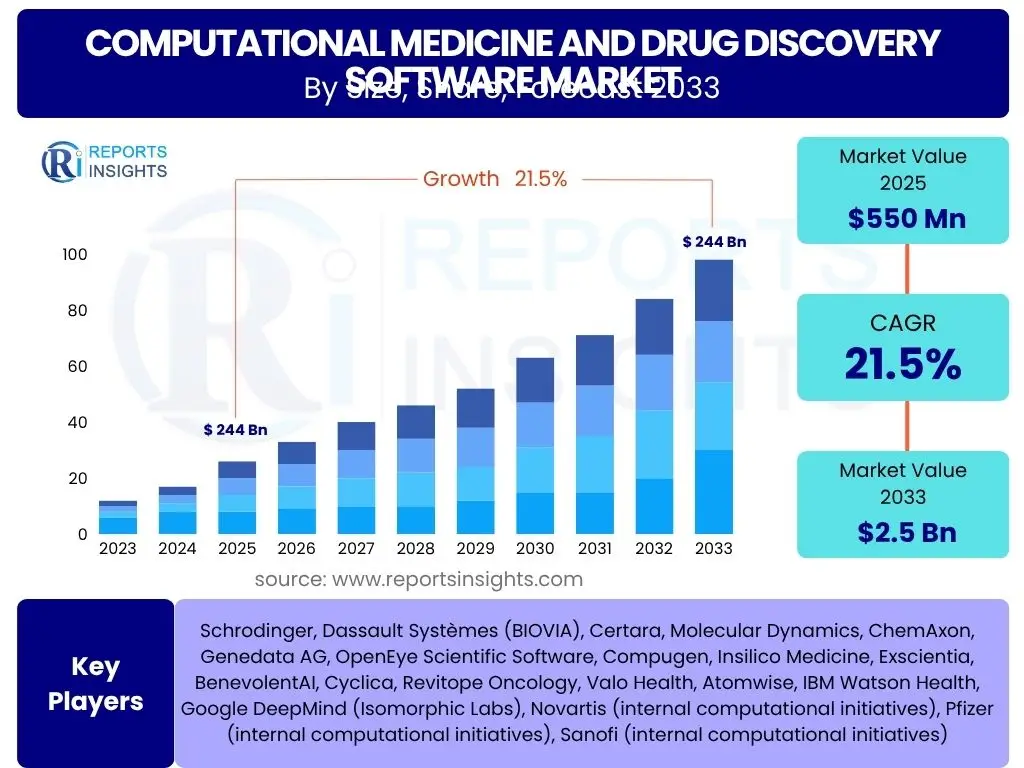

According to Reports Insights Consulting Pvt Ltd, The Computational Medicine and Drug Discovery Software Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 21.5% between 2025 and 2033. The market is estimated at USD 550 million in 2025 and is projected to reach USD 2.5 billion by the end of the forecast period in 2033.

Key Computational Medicine and Drug Discovery Software Market Trends & Insights

The Computational Medicine and Drug Discovery Software market is experiencing significant evolution driven by several interconnected trends. A primary insight reveals a widespread shift towards in-silico methods, increasingly favored for their ability to accelerate various stages of drug development and reduce associated costs. This paradigm shift is fueled by advancements in computational power and the growing complexity of biological data, necessitating sophisticated analytical tools.

Furthermore, the industry is witnessing a robust trend towards personalized medicine, where computational tools are pivotal in analyzing individual patient data to tailor treatments. This involves integrating multi-omics data, electronic health records, and clinical trial results to develop highly specific therapeutic approaches. The demand for efficiency and precision in drug development, coupled with rising R&D investments, continues to propel the adoption of advanced computational solutions across pharmaceutical and biotechnology sectors.

Another emerging trend is the increasing collaboration between technology providers and pharmaceutical companies, fostering the development of highly specialized and integrated software platforms. Cloud-based deployment models are gaining traction, offering scalability, accessibility, and reduced infrastructure costs, which are particularly beneficial for smaller biotech firms and academic institutions. These trends collectively underscore the market's trajectory towards more agile, data-driven, and patient-centric drug discovery processes.

- Accelerated adoption of in-silico drug discovery techniques.

- Growing emphasis on personalized and precision medicine.

- Increased integration of artificial intelligence and machine learning.

- Shift towards cloud-based and Software-as-a-Service (SaaS) deployment models.

- Rising investments in pharmaceutical and biotechnology R&D.

- Expansion of computational approaches into clinical trial optimization.

- Development of multi-omics data analysis platforms.

AI Impact Analysis on Computational Medicine and Drug Discovery Software

The integration of Artificial Intelligence (AI) is profoundly transforming the computational medicine and drug discovery software landscape, marking a pivotal shift in how new therapies are identified, developed, and optimized. Users frequently inquire about AI's capacity to accelerate research, enhance predictive accuracy, and manage vast datasets. AI-driven algorithms, including machine learning and deep learning, are proving instrumental in tasks such as target identification by sifting through genomic and proteomic data, identifying potential disease pathways, and predicting drug-target interactions with unprecedented speed and precision. This significantly reduces the time and resources traditionally required in the initial phases of drug development, moving from hypothesis-driven research to data-driven discovery.

Moreover, AI's influence extends to lead optimization, where it can rapidly screen millions of compounds virtually, predict their efficacy, toxicity, and pharmacokinetic properties, and suggest modifications to improve their therapeutic profile. This capability addresses a core user concern: the high attrition rate of drug candidates in preclinical and clinical stages. By improving the quality of drug candidates earlier in the pipeline, AI minimizes costly failures. Furthermore, Generative AI models are now being explored to design novel molecules from scratch, potentially unlocking new chemical spaces previously unexplored by traditional methods. This offers a revolutionary approach to creating new drug candidates with desired properties.

However, user concerns often revolve around data privacy, the interpretability of AI models (the "black box" problem), and the ethical implications of AI in healthcare. While AI offers immense potential for predictive modeling in clinical trials, optimizing patient selection, and analyzing real-world data, the validation and regulatory approval of AI-derived insights remain critical challenges. Addressing these concerns necessitates robust data governance, explainable AI (XAI) frameworks, and collaborative efforts between AI developers, computational biologists, and regulatory bodies to build trust and ensure responsible innovation in this rapidly evolving domain.

- Accelerated target identification and validation using machine learning.

- Enhanced virtual screening and lead optimization through predictive AI models.

- Improved accuracy in predicting drug-target interactions and ADMET properties.

- Automation of data analysis from high-throughput screening and multi-omics experiments.

- Development of novel molecular structures through generative AI.

- Optimization of clinical trial design and patient stratification.

- Real-time monitoring and analysis of patient response in personalized medicine.

Key Takeaways Computational Medicine and Drug Discovery Software Market Size & Forecast

The Computational Medicine and Drug Discovery Software market is poised for substantial growth, reflecting a fundamental shift in how pharmaceutical research and development is conducted globally. A key takeaway is the undeniable acceleration in the adoption of in-silico methods, driven by the imperative to reduce the time and cost associated with bringing new drugs to market. The projected CAGR of 21.5% signifies a robust expansion, indicating strong industry confidence and investment in computational approaches as essential tools, rather than supplemental ones.

Furthermore, the forecasted market value of USD 2.5 billion by 2033 underscores the increasing financial commitment to this domain. This growth is not merely incremental but represents a transformative impact on drug discovery paradigms, enabling greater precision, efficiency, and the exploration of complex biological systems previously intractable with traditional experimental methods. The convergence of advanced computing, big data analytics, and biological insights is creating a fertile ground for sustained innovation and market expansion.

Another significant takeaway is the expanding scope of computational applications beyond just initial drug discovery, encompassing personalized medicine, disease modeling, and even optimizing clinical trial phases. This broad utility ensures continued market relevance and demand across the entire drug development lifecycle. The market's trajectory is firmly upward, propelled by technological advancements, rising R&D investments, and the urgent global need for novel and more effective therapeutic interventions.

- Significant market growth driven by demand for faster and more cost-effective drug discovery.

- High CAGR indicates strong investment and adoption of computational solutions.

- Market expansion is fueled by technological advancements and data proliferation.

- Increasing integration of AI and machine learning is a core growth driver.

- Focus on personalized medicine and rare diseases is boosting software utility.

- Cloud-based solutions are lowering entry barriers and increasing accessibility.

Computational Medicine and Drug Discovery Software Market Drivers Analysis

The computational medicine and drug discovery software market is propelled by a confluence of powerful drivers that are reshaping the pharmaceutical and biotechnology industries. A primary driver is the soaring cost and protracted timeline associated with traditional drug development, which incentivizes organizations to seek more efficient and less expensive alternatives. Computational tools offer a viable solution by significantly reducing experimental work, accelerating lead identification, and minimizing preclinical and clinical failures, thereby shortening the drug-to-market cycle and enhancing R&D productivity.

Furthermore, the escalating global healthcare expenditure and the growing prevalence of chronic and complex diseases necessitate a continuous pipeline of innovative therapies. This demand fuels increased R&D investments by pharmaceutical and biotechnology companies, which in turn drives the adoption of advanced computational software. The rise of personalized medicine, requiring the analysis of vast genomic and patient-specific data, also acts as a significant catalyst, as computational platforms are essential for extracting actionable insights from such complex datasets.

Technological advancements, particularly in high-performance computing (HPC), artificial intelligence (AI), and big data analytics, are continually enhancing the capabilities of these software solutions. These innovations enable more accurate simulations, predictive modeling, and the processing of unprecedented volumes of biological and chemical data, making in-silico methods increasingly indispensable. The synergy between these factors creates a robust environment for sustained market growth.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing R&D expenditure by pharmaceutical companies | +1.8% | Global, especially North America, Europe | Long-term (2025-2033) |

| Demand for accelerated and cost-effective drug development | +1.5% | Global | Medium-to-Long Term (2025-2033) |

| Growing focus on personalized and precision medicine | +1.2% | North America, Europe, parts of Asia Pacific | Long-term (2027-2033) |

| Advancements in computing power and AI technologies | +1.0% | Global | Short-to-Medium Term (2025-2029) |

| Increasing complexity of biological data | +0.9% | Global | Medium-to-Long Term (2025-2033) |

Computational Medicine and Drug Discovery Software Market Restraints Analysis

Despite its robust growth, the computational medicine and drug discovery software market faces several significant restraints that could temper its expansion. One of the primary barriers is the high initial investment cost associated with implementing sophisticated computational platforms. This includes not only the software licenses but also the necessary high-performance computing infrastructure, data storage solutions, and specialized personnel required to operate and maintain these systems. Such substantial upfront capital expenditure can be prohibitive for smaller biotechnology firms, academic institutions, and startups, limiting their adoption rates.

Another key restraint is the inherent complexity of integrating these advanced software solutions into existing research workflows. Organizations often face challenges related to data interoperability, legacy system compatibility, and the need for extensive training for scientific staff. The learning curve can be steep, leading to resistance from traditional researchers accustomed to wet-lab experiments. Moreover, ensuring data security and privacy, especially when dealing with sensitive patient genomic and clinical data, presents a continuous challenge that requires robust cybersecurity measures and compliance with stringent regulatory frameworks like GDPR and HIPAA, adding further operational complexities.

Furthermore, the scarcity of highly skilled professionals who possess a dual expertise in computational science and biology or chemistry remains a significant bottleneck. The demand for bioinformaticians, computational chemists, and data scientists with relevant domain knowledge often outstrips supply, leading to recruitment difficulties and higher operational costs. Regulatory uncertainties and the need for rigorous validation of in-silico models for drug approval processes also pose hurdles, as regulatory bodies are still developing guidelines for accepting purely computational evidence, which can slow down adoption in critical stages of drug development.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High initial investment and operational costs | -0.8% | Global, particularly smaller enterprises | Short-to-Medium Term (2025-2029) |

| Complexity of software integration and data interoperability | -0.6% | Global | Medium-to-Long Term (2025-2033) |

| Data security and privacy concerns | -0.5% | Europe (GDPR), North America (HIPAA) | Long-term (2025-2033) |

| Scarcity of skilled computational scientists and bioinformaticians | -0.4% | Global | Long-term (2025-2033) |

| Regulatory uncertainties regarding in-silico model validation | -0.3% | North America, Europe, Asia Pacific | Long-term (2027-2033) |

Computational Medicine and Drug Discovery Software Market Opportunities Analysis

The computational medicine and drug discovery software market is ripe with opportunities that promise to accelerate its growth and expand its application across the healthcare ecosystem. One significant opportunity lies in the burgeoning adoption of cloud-based computational platforms. These solutions offer unparalleled scalability, flexibility, and reduced infrastructure costs, making advanced drug discovery tools accessible to a broader range of users, including academic researchers, small and medium-sized biotech firms, and startups. The shift to cloud models also facilitates collaborative research, enabling geographically dispersed teams to work on complex projects seamlessly, which is crucial for modern drug development.

Emerging markets, particularly in Asia Pacific, Latin America, and parts of the Middle East, present substantial untapped potential. These regions are experiencing significant growth in healthcare infrastructure and R&D investments, driven by increasing disease burdens and a desire for localized drug discovery capabilities. As these economies mature, their demand for advanced computational tools to support their nascent pharmaceutical and biotechnology industries is expected to surge, creating new revenue streams for software providers.

Furthermore, the continuous advancements in related technologies, such as quantum computing and advanced simulation techniques, represent long-term opportunities. While still in nascent stages, these technologies could revolutionize computational capabilities, enabling simulations of unprecedented complexity and accuracy, potentially unlocking new frontiers in drug design and disease understanding. The expansion of applications into new therapeutic areas, including cell and gene therapies, as well as personalized diagnostics, also offers avenues for market diversification and sustained growth, as these modalities inherently rely on precise computational analysis of biological data.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Expansion of cloud-based and SaaS offerings | +1.0% | Global | Short-to-Medium Term (2025-2029) |

| Growth in emerging markets (APAC, Latin America) | +0.9% | Asia Pacific, Latin America, Middle East | Medium-to-Long Term (2027-2033) |

| Integration with advanced genomics and proteomics data | +0.8% | Global | Long-term (2027-2033) |

| Application in new therapeutic areas (e.g., cell & gene therapies) | +0.7% | North America, Europe | Long-term (2027-2033) |

| Development of AI-driven drug discovery platforms | +1.1% | Global | Short-to-Medium Term (2025-2029) |

Computational Medicine and Drug Discovery Software Market Challenges Impact Analysis

The computational medicine and drug discovery software market faces several critical challenges that stakeholders must address to ensure sustained growth and wider adoption. A significant hurdle is the issue of data interoperability and standardization. The vast amount of biological and chemical data generated often resides in disparate formats and siloed systems, making it difficult for computational software to seamlessly integrate, process, and analyze this information. This lack of standardization can lead to data integrity issues, impede collaborative research, and necessitate considerable effort in data cleaning and harmonization, thus reducing the efficiency gains promised by computational tools.

Another formidable challenge is the validation and acceptance of in-silico models. While computational simulations offer powerful predictive capabilities, convincing regulatory bodies and the broader scientific community of their reliability and robustness can be difficult. The "black box" nature of some advanced AI models further exacerbates this, as their decision-making processes may not be easily interpretable, raising concerns about trust and reproducibility. Establishing universally accepted validation protocols and transparent methodologies for computational predictions is essential for their widespread adoption in regulated drug development pipelines.

Furthermore, intellectual property (IP) protection remains a concern, particularly when sensitive proprietary data is processed through third-party cloud-based software or shared in collaborative research environments. Companies are wary of potential data breaches or unauthorized access to their valuable research assets. Addressing these security concerns through robust encryption, secure cloud architectures, and clear contractual agreements is paramount. The rapid pace of technological change also presents a challenge, as software providers must continuously innovate to keep pace with evolving scientific understanding and emerging computational techniques, requiring significant ongoing R&D investment to maintain competitiveness.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Data interoperability and standardization issues | -0.7% | Global | Long-term (2025-2033) |

| Validation and regulatory acceptance of in-silico models | -0.6% | North America, Europe (Regulatory Bodies) | Long-term (2027-2033) |

| Intellectual Property (IP) and data security concerns | -0.5% | Global | Long-term (2025-2033) |

| High cost of skilled talent and training requirements | -0.4% | Global | Medium-to-Long Term (2025-2033) |

| Resistance to adopting new technologies in traditional settings | -0.3% | Global | Short-to-Medium Term (2025-2029) |

Computational Medicine and Drug Discovery Software Market - Updated Report Scope

This report provides a comprehensive and in-depth analysis of the global Computational Medicine and Drug Discovery Software Market, examining market dynamics, segmentation, regional trends, and competitive landscape. It offers strategic insights into market size, growth drivers, restraints, opportunities, and challenges affecting the industry from 2019 to 2033, with a detailed forecast from 2025 to 2033. The scope covers the impact of emerging technologies, particularly Artificial Intelligence, and the evolving regulatory environment on market expansion and innovation across various applications and end-user segments.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 550 million |

| Market Forecast in 2033 | USD 2.5 billion |

| Growth Rate | 21.5% |

| Number of Pages | 247 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Schrodinger, Dassault Systèmes (BIOVIA), Certara, Molecular Dynamics, ChemAxon, Genedata AG, OpenEye Scientific Software, Compugen, Insilico Medicine, Exscientia, BenevolentAI, Cyclica, Revitope Oncology, Valo Health, Atomwise, IBM Watson Health, Google DeepMind (Isomorphic Labs), Novartis (internal computational initiatives), Pfizer (internal computational initiatives), Sanofi (internal computational initiatives) |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Computational Medicine and Drug Discovery Software market is meticulously segmented to provide a detailed understanding of its diverse components, applications, end-users, deployment models, and therapeutic areas. This granular segmentation allows for a precise analysis of market dynamics across different verticals, identifying key growth pockets and strategic opportunities. By understanding how various factors influence each segment, stakeholders can tailor their strategies to target specific market niches and optimize resource allocation effectively.

The segmentation by component differentiates between the core software platforms and the associated services, such as consulting, implementation, and support, which are crucial for effective utilization. Application-based segmentation highlights the primary use cases of these software solutions throughout the drug discovery and development lifecycle, from initial target identification to late-stage clinical trials and the emerging field of personalized medicine. This provides insights into which stages are benefiting most from computational advancements.

Further segmentation by end-user categories, including pharmaceutical companies, contract research organizations, and academic institutions, helps to identify the primary consumers and their specific needs. Deployment models, distinguishing between on-premise and cloud-based solutions, reflect the evolving technological preferences and infrastructure capabilities of users. Finally, the breakdown by therapeutic area provides a focused view on where computational medicine is making the most significant impact, revealing trends in disease-specific research and development efforts, which is vital for both innovators and investors in this highly specialized market.

- By Component: Software, Services

- By Application:

- Drug Discovery

- Target Identification

- Lead Optimization

- Preclinical Trials

- Clinical Trials

- Personalized Medicine

- Disease Modeling

- Omics Research

- Others

- Drug Discovery

- By End-User:

- Pharmaceutical & Biotechnology Companies

- Contract Research Organizations (CROs)

- Academic & Research Institutions

- By Deployment Model:

- On-premise

- Cloud-based

- By Therapeutic Area:

- Oncology

- Neurology

- Cardiovascular Diseases

- Infectious Diseases

- Metabolic Disorders

- Rare Diseases

- Others

Regional Highlights

- North America: Dominates the market due to significant R&D investments by pharmaceutical and biotechnology companies, presence of leading market players, advanced healthcare infrastructure, and high adoption rates of cutting-edge technologies like AI and cloud computing in drug discovery. The United States is a primary hub for innovation and commercialization in this sector.

- Europe: A major market driven by substantial government funding for life sciences research, strong academic-industry collaborations, and increasing focus on personalized medicine initiatives. Countries like the UK, Germany, and Switzerland are key contributors with robust pharmaceutical sectors and active research communities.

- Asia Pacific (APAC): Expected to exhibit the highest growth rate during the forecast period. This growth is attributed to rising healthcare expenditure, increasing R&D activities, expanding pharmaceutical and biotechnology industries, particularly in China, India, and Japan, and a growing patient pool for various diseases. Government initiatives to promote drug discovery and favorable regulatory environments also contribute to market expansion.

- Latin America: Shows emerging potential, with increasing investments in healthcare infrastructure and R&D, particularly in countries like Brazil and Mexico. Adoption of computational tools is gradually rising as pharmaceutical companies in the region seek to enhance efficiency and reduce drug development costs.

- Middle East and Africa (MEA): Represents a nascent but growing market. Increasing focus on improving healthcare quality, diversification of economies, and strategic investments in biotech and pharmaceutical sectors by Gulf countries are expected to drive the adoption of computational medicine software in the long term.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Computational Medicine and Drug Discovery Software Market.- Schrodinger

- Dassault Systèmes (BIOVIA)

- Certara

- Molecular Dynamics

- ChemAxon

- Genedata AG

- OpenEye Scientific Software

- Compugen

- Insilico Medicine

- Exscientia

- BenevolentAI

- Cyclica

- Revitope Oncology

- Valo Health

- Atomwise

- IBM Watson Health

- Google DeepMind (Isomorphic Labs)

- Novartis (internal computational initiatives)

- Pfizer (internal computational initiatives)

- Sanofi (internal computational initiatives)

Frequently Asked Questions

Analyze common user questions about the Computational Medicine and Drug Discovery Software market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is computational medicine and drug discovery software?

Computational medicine and drug discovery software encompasses a range of advanced tools and platforms that utilize mathematical models, simulations, and data analysis to accelerate and optimize various stages of drug research and development. This includes tasks like target identification, lead optimization, virtual screening, and predictive modeling for drug efficacy and toxicity, significantly reducing the reliance on traditional wet-lab experiments.

How does AI impact drug discovery software?

AI, particularly machine learning and deep learning, revolutionizes drug discovery software by enabling faster analysis of vast biological datasets, improving the accuracy of predictive models for drug-target interactions, and automating compound design. It accelerates hit-to-lead processes, optimizes clinical trial design, and helps identify novel therapeutic candidates more efficiently, significantly de-risking and speeding up the overall discovery pipeline.

What are the primary drivers of this market's growth?

Key drivers include the imperative to reduce the high cost and long timelines of traditional drug development, increasing R&D investments by pharmaceutical companies, the growing demand for personalized medicine, and continuous advancements in computational power and AI technologies. These factors collectively push for greater adoption of in-silico methods.

What are the main challenges facing the market?

Major challenges include high initial investment costs for software and infrastructure, difficulties with data interoperability and standardization across diverse platforms, concerns regarding data security and intellectual property, and the ongoing need for rigorous validation and regulatory acceptance of computational models. The shortage of skilled professionals with dual expertise in computation and biology also poses a significant hurdle.

Which regions are leading in the adoption of this software?

North America currently leads the market due to robust R&D spending, the presence of major pharmaceutical companies, and advanced technological infrastructure. Europe also holds a significant share with strong research initiatives. However, the Asia Pacific region is projected to show the fastest growth, driven by increasing healthcare investments and expanding biotechnology sectors.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted