Marine Fuel Oil Market

Marine Fuel Oil Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_705221 | Last Updated : August 11, 2025 |

Format : ![]()

![]()

![]()

![]()

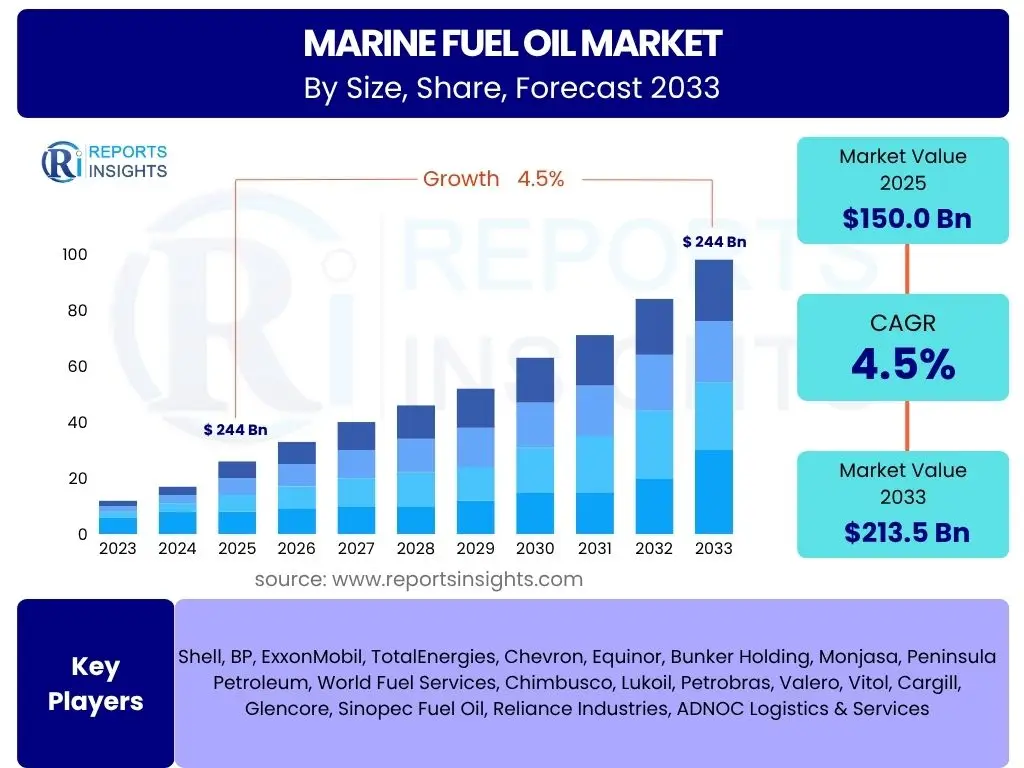

Marine Fuel Oil Market Size

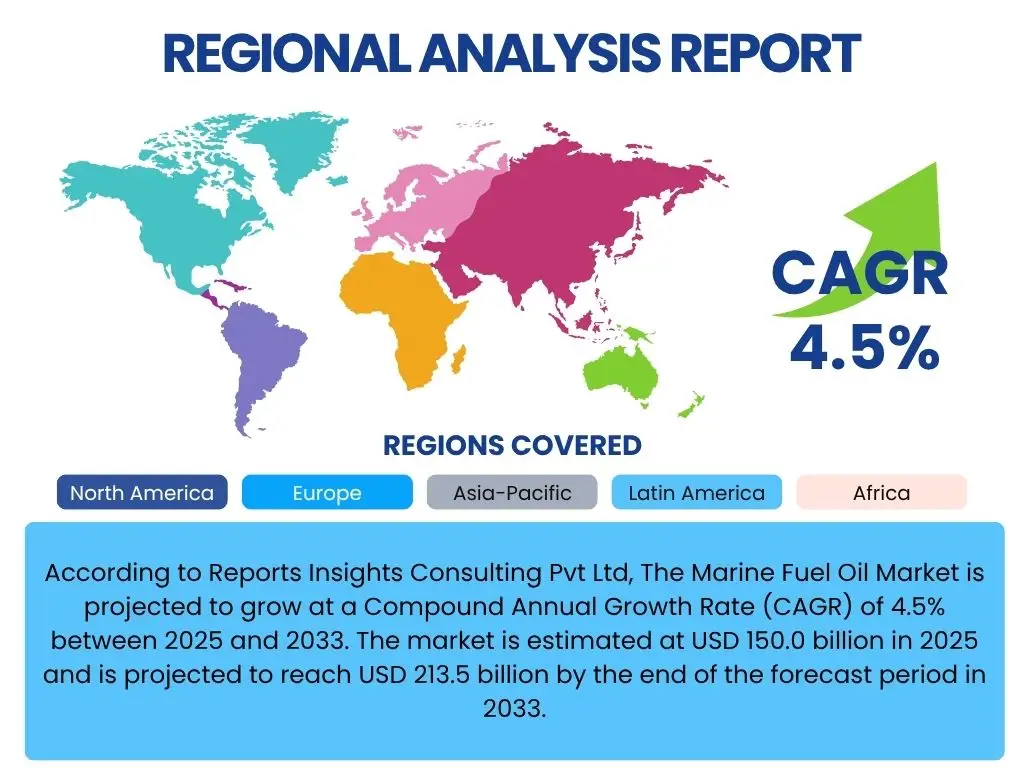

According to Reports Insights Consulting Pvt Ltd, The Marine Fuel Oil Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 4.5% between 2025 and 2033. The market is estimated at USD 150.0 billion in 2025 and is projected to reach USD 213.5 billion by the end of the forecast period in 2033.

Key Marine Fuel Oil Market Trends & Insights

The marine fuel oil market is undergoing a significant transformation driven by stringent environmental regulations, technological advancements, and a growing emphasis on sustainability. Key industry participants and stakeholders are keenly observing the shift towards lower-sulfur fuels and the emergence of alternative energy sources. The market dynamics are primarily influenced by the global shipping industry's decarbonization goals, pushing for innovation in fuel production, distribution, and consumption.

A prominent trend involves the increasing adoption of Very Low Sulfur Fuel Oil (VLSFO) and Marine Gas Oil (MGO) following the IMO 2020 sulfur cap. Concurrently, there is a burgeoning interest in Liquefied Natural Gas (LNG) as a transitional fuel, alongside burgeoning research and pilot projects for future marine fuels such as methanol, ammonia, and hydrogen. The development of bunkering infrastructure for these new fuels, coupled with advancements in engine technology, signifies a long-term strategic shift within the industry, aiming for a more environmentally benign maritime sector.

- Transition towards lower sulfur fuels (VLSFO, MGO) driven by IMO 2020 regulations.

- Growing adoption of Liquefied Natural Gas (LNG) as a marine fuel, especially for new builds.

- Increasing research and development into zero-emission alternative fuels like methanol, ammonia, and hydrogen.

- Digitalization and optimization of fuel procurement and consumption processes.

- Expansion and adaptation of bunkering infrastructure to support diverse fuel types.

- Focus on energy efficiency measures and propulsion technologies to reduce fuel consumption.

- Development of carbon capture and storage technologies for conventional fuels.

AI Impact Analysis on Marine Fuel Oil

Artificial Intelligence (AI) is increasingly recognized as a transformative technology within the marine fuel oil sector, addressing critical operational challenges and enabling enhanced decision-making. Stakeholders frequently inquire about AI's capacity to optimize fuel consumption, predict market price fluctuations, and streamline complex supply chain logistics. The consensus points towards AI's potential to significantly reduce operational costs, minimize environmental impact through efficient resource utilization, and improve overall fleet management.

The integration of AI algorithms allows for real-time data analysis from vessel operations, weather patterns, and market conditions, leading to optimized routing, precise fuel bunkering decisions, and predictive maintenance. This data-driven approach not only contributes to considerable fuel savings but also assists in compliance with evolving environmental regulations by enabling more accurate emissions monitoring and reporting. Furthermore, AI's role in demand forecasting and supply chain management is crucial for ensuring fuel availability and mitigating risks associated with supply disruptions or price volatility.

- AI-driven vessel routing and speed optimization for reduced fuel consumption.

- Predictive analytics for marine fuel price forecasting and procurement strategy.

- Enhanced supply chain management and logistics optimization for bunkering operations.

- Real-time monitoring and analysis of engine performance to optimize fuel efficiency.

- Automated compliance reporting for emissions and fuel consumption.

- Development of smart bunkering platforms for transparent and efficient transactions.

- Advanced data analysis to identify optimal fuel blends and reduce operational costs.

Key Takeaways Marine Fuel Oil Market Size & Forecast

The Marine Fuel Oil market is poised for steady growth, reflecting the indispensable role of maritime trade in the global economy and the ongoing efforts towards sustainable shipping. A primary takeaway is the significant financial commitment required for the industry to transition to cleaner fuels, necessitating strategic investments in both vessel modifications and bunkering infrastructure. The forecast indicates that while conventional marine fuels will continue to dominate the market in the near term, the share of alternative and low-carbon fuels is expected to expand considerably, particularly towards the latter half of the forecast period.

Market expansion is not merely quantitative but also qualitative, driven by innovation in fuel production, distribution, and consumption technologies. The regulatory landscape, particularly driven by the International Maritime Organization (IMO) targets, serves as a powerful catalyst for this transformation. Stakeholders must consider the dual challenges of managing volatile fuel prices and navigating a complex, evolving regulatory environment while capitalizing on opportunities presented by new fuel technologies and digital solutions. The long-term outlook emphasizes resilience, adaptability, and collaboration across the maritime value chain to achieve decarbonization goals.

- Sustainable growth projected, driven by global trade expansion and regulatory compliance.

- Significant shift from high-sulfur to low-sulfur and alternative fuels is underway.

- Regulatory mandates, especially from IMO, are the primary drivers for market evolution.

- Investment in new bunkering infrastructure for alternative fuels is critical for future growth.

- Digitalization and AI will play a vital role in optimizing fuel efficiency and supply chains.

- Geopolitical stability and crude oil price volatility remain key external factors influencing market dynamics.

- Collaboration across the maritime ecosystem is essential for successful decarbonization.

Marine Fuel Oil Market Drivers Analysis

The marine fuel oil market is significantly influenced by a confluence of macroeconomic factors and industry-specific imperatives. The primary driver remains the consistent growth in global seaborne trade, which directly correlates with demand for marine fuel. As global economies expand and supply chains become increasingly interconnected, the need for efficient and reliable maritime transport intensifies, thereby bolstering fuel consumption.

Furthermore, the implementation of stringent environmental regulations, particularly the IMO 2020 sulfur cap, has spurred demand for compliant very low sulfur fuel oil (VLSFO) and marine gas oil (MGO). This regulatory push is not just about sulfur content; it also sets a precedent for future decarbonization targets, driving innovation and investment in alternative fuels and energy-efficient vessel technologies. The modernization of existing fleets and the construction of new, more efficient vessels also contribute to evolving fuel consumption patterns, indirectly driving demand for cleaner or more specialized fuels.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growth in Global Seaborne Trade and Shipping Activities | +1.5% to +2.0% | Global, particularly Asia-Pacific, Europe, North America | Short to Long-term (2025-2033) |

| Strict Environmental Regulations (e.g., IMO 2020, future GHG targets) | +1.0% to +1.5% | Global, especially major shipping routes and Emission Control Areas (ECAs) | Short to Medium-term (2025-2029) |

| Increasing Adoption of LNG and Other Alternative Fuels | +0.8% to +1.2% | Europe, Asia-Pacific, North America (key bunkering hubs) | Medium to Long-term (2027-2033) |

| Technological Advancements in Vessel Design and Propulsion Systems | +0.5% to +0.8% | Global, particularly leading shipbuilding nations (South Korea, China, Japan) | Medium to Long-term (2028-2033) |

Marine Fuel Oil Market Restraints Analysis

While the marine fuel oil market exhibits growth potential, it is simultaneously constrained by several significant factors. Price volatility in crude oil, which directly influences the cost of marine fuels, presents a persistent challenge. Sudden fluctuations in crude oil prices can significantly impact shipping companies' operational budgets, leading to delayed investment decisions or adjustments in trade routes, thereby dampening fuel demand predictability.

Moreover, the escalating stringency of environmental regulations, while a driver for new fuel adoption, also acts as a restraint for traditional high-sulfur fuel oil (HSFO) use. The considerable capital expenditure required for fleet conversion (e.g., installing scrubbers or building new alternative-fuel-ready vessels) and the development of new bunkering infrastructure for fuels like LNG, methanol, or ammonia can slow down the transition for many shipping companies, particularly smaller operators. Geopolitical tensions and trade protectionism also pose risks, potentially disrupting global trade flows and subsequently reducing the demand for marine fuel.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Volatile Crude Oil Prices and Price Spreads | -1.0% to -1.5% | Global | Short to Medium-term (2025-2030) |

| High Capital Expenditure for Alternative Fuel Infrastructure and Vessel Retrofits | -0.8% to -1.2% | Global, particularly developing regions | Medium to Long-term (2026-2033) |

| Increasing Regulatory Costs and Compliance Burden for Traditional Fuels | -0.5% to -0.8% | Global, especially in major port states | Short to Medium-term (2025-2029) |

| Geopolitical Tensions and Trade Protectionism | -0.5% to -1.0% | Specific trade routes, global impact | Short-term (2025-2027) |

Marine Fuel Oil Market Opportunities Analysis

The marine fuel oil market is abundant with opportunities stemming from the global maritime industry's imperative for decarbonization and efficiency. A significant opportunity lies in the burgeoning market for alternative marine fuels such as LNG, methanol, ammonia, and hydrogen. As regulatory pressures intensify and technological advancements render these fuels more viable, their adoption is expected to surge, creating new supply chain and bunkering infrastructure development avenues.

Furthermore, the digitalization of the maritime sector offers substantial opportunities for optimizing fuel consumption and procurement. Advanced analytics, AI-driven platforms, and IoT integration can provide shipping companies with real-time data on fuel efficiency, predictive maintenance needs, and optimal bunkering strategies. This not only leads to cost savings but also enhances operational transparency and environmental performance. The growing focus on developing sustainable and circular economy practices within the shipping industry, including bio-bunkering and waste-to-fuel initiatives, presents another fertile ground for market expansion and innovation.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development and Adoption of Alternative Fuels (LNG, Methanol, Ammonia, Hydrogen) | +1.2% to +1.8% | Global, with focus on major bunkering hubs (Singapore, Rotterdam, Houston) | Medium to Long-term (2027-2033) |

| Integration of Digital Technologies (AI, IoT, Big Data) for Fuel Optimization | +0.8% to +1.2% | Global, particularly technologically advanced shipping companies | Short to Long-term (2025-2033) |

| Expansion of Green Ports and Bunkering Infrastructure for Future Fuels | +0.7% to +1.0% | Coastal nations, emerging maritime economies | Medium to Long-term (2028-2033) |

| Growth in the Biofuel Blending and Sustainable Fuel Production Segment | +0.5% to +0.8% | Europe, North America, parts of Asia-Pacific | Medium-term (2026-2031) |

Marine Fuel Oil Market Challenges Impact Analysis

The marine fuel oil market faces several significant challenges that could impede its growth trajectory and complicate operational strategies. Regulatory uncertainty surrounding future emission standards, particularly for greenhouse gases, creates hesitation among shipowners regarding long-term investments in specific fuel technologies. This lack of clear, globally harmonized policies can lead to fragmented market development and suboptimal investment decisions.

Furthermore, the establishment of a robust and scalable infrastructure for new alternative fuels presents a formidable hurdle. This includes not only bunkering facilities but also production capacity, storage solutions, and efficient distribution networks for fuels like ammonia or hydrogen, which currently lack widespread commercial availability. Safety concerns associated with handling and bunkering novel fuels, coupled with the need for specialized crew training, add another layer of complexity. Lastly, the significant cost differential between traditional fuels and emerging alternatives poses a considerable financial burden for operators, potentially slowing down the transition unless supportive policies or financial incentives are universally adopted.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Regulatory Uncertainty and Lack of Global Harmonization on Future Emissions | -1.0% to -1.5% | Global | Short to Medium-term (2025-2030) |

| Infrastructure Limitations for New Alternative Fuels | -0.8% to -1.2% | Developing regions, smaller ports | Medium to Long-term (2026-2033) |

| High Cost of Alternative Fuels and Technology Adoption | -0.7% to -1.0% | Global, particularly smaller shipping companies | Short to Medium-term (2025-2029) |

| Safety and Training Concerns Related to Handling Novel Fuels | -0.5% to -0.7% | Global, particularly for crew and port operators | Medium-term (2026-2031) |

Marine Fuel Oil Market - Updated Report Scope

This report provides a comprehensive analysis of the global Marine Fuel Oil market, offering detailed insights into market dynamics, size estimations, and future growth projections. It delineates the market landscape through extensive segmentation by fuel type, application, and end-use, complemented by a thorough regional analysis. The scope extends to identifying key market drivers, restraints, opportunities, and challenges that shape industry trends and competitive strategies. Furthermore, the report assesses the impact of emerging technologies like AI on fuel consumption and supply chain efficiency, providing a holistic view for stakeholders navigating the evolving maritime energy sector.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 150.0 billion |

| Market Forecast in 2033 | USD 213.5 billion |

| Growth Rate | 4.5% |

| Number of Pages | 245 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Shell, BP, ExxonMobil, TotalEnergies, Chevron, Equinor, Bunker Holding, Monjasa, Peninsula Petroleum, World Fuel Services, Chimbusco, Lukoil, Petrobras, Valero, Vitol, Cargill, Glencore, Sinopec Fuel Oil, Reliance Industries, ADNOC Logistics & Services |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Marine Fuel Oil market is extensively segmented to provide a granular understanding of its diverse components and evolving demand patterns. These segments are primarily defined by the type of fuel used, the specific application or vessel type, and the ultimate end-use sector. Each segment reflects unique market dynamics, regulatory impacts, and technological preferences, allowing for targeted analysis of growth opportunities and challenges across the maritime industry.

The segmentation by fuel type highlights the industry's shift from conventional high-sulfur options to a broader array of compliant and alternative fuels, driven by environmental mandates. Application-based segmentation underscores the varying fuel requirements and consumption profiles of different vessel categories, from large container ships to specialized offshore vessels. Finally, end-use segmentation differentiates demand from commercial shipping, which forms the bulk of the market, from niche applications such as offshore exploration or leisure boating, providing a comprehensive market overview.

- By Fuel Type

- Very Low Sulfur Fuel Oil (VLSFO)

- High Sulfur Fuel Oil (HSFO)

- Marine Gas Oil (MGO)

- Liquefied Natural Gas (LNG)

- Methanol

- Ammonia

- Hydrogen

- Biofuels

- By Application

- Container Ships

- Tankers

- Bulk Carriers

- Cruise Ships

- Ro-Ro Vessels

- Offshore Vessels

- Naval Vessels

- Fishing Vessels

- By End-Use

- Commercial Shipping

- Offshore Exploration & Production

- Leisure & Others

Regional Highlights

- Asia-Pacific (APAC): Dominates the global marine fuel oil market, driven by high trade volumes, the presence of major bunkering hubs like Singapore and Fujairah (UAE, geographically MEA but significant APAC trade), and substantial shipbuilding activity in China, South Korea, and Japan. The region is a key adopter of both low-sulfur fuels and emerging alternative fuels.

- Europe: A significant market characterized by stringent environmental regulations (e.g., Emission Control Areas), leading to early adoption of low-sulfur fuels and pioneering initiatives in LNG, methanol, and other green fuels. Major bunkering ports include Rotterdam and Gibraltar.

- North America: Features a mature shipping market with significant demand from commercial and offshore sectors. Compliance with ECA regulations in coastal areas drives demand for MGO and LNG. The Gulf Coast, particularly Houston, is a crucial bunkering hub.

- Middle East and Africa (MEA): Critical due to its strategic location along major trade routes and as a major oil-producing region. Fujairah is one of the world's largest bunkering ports. The region is seeing increasing investment in bunkering infrastructure for diversified fuel types.

- Latin America: An emerging market with growing trade activities, particularly in Brazil, Mexico, and Panama. The Panama Canal's strategic importance contributes to significant marine fuel demand. Investment in bunkering facilities and alternative fuels is gradually increasing.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Marine Fuel Oil Market.- Shell

- BP

- ExxonMobil

- TotalEnergies

- Chevron

- Equinor

- Bunker Holding

- Monjasa

- Peninsula Petroleum

- World Fuel Services

- Chimbusco

- Lukoil

- Petrobras

- Valero

- Vitol

- Cargill

- Glencore

- Sinopec Fuel Oil

- Reliance Industries

- ADNOC Logistics & Services

Frequently Asked Questions

What is the current growth rate for the Marine Fuel Oil Market?

The Marine Fuel Oil Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 4.5% between 2025 and 2033, indicating a steady expansion driven by global trade and evolving fuel demands.

How are environmental regulations impacting the Marine Fuel Oil Market?

Environmental regulations, particularly the IMO 2020 sulfur cap and upcoming greenhouse gas emission targets, are profoundly impacting the market by driving a significant shift from high-sulfur fuel oil to very low sulfur fuel oil (VLSFO), marine gas oil (MGO), and a growing array of alternative, lower-carbon fuels such as LNG, methanol, and ammonia.

What are the key alternative fuels gaining traction in the marine sector?

Key alternative fuels gaining traction include Liquefied Natural Gas (LNG) due to its lower emissions, and emerging fuels such as methanol, ammonia, and hydrogen, which are critical for achieving long-term decarbonization goals, despite current infrastructure and cost challenges.

How does AI contribute to efficiency in the Marine Fuel Oil Market?

AI contributes significantly by optimizing vessel routing and speed for reduced fuel consumption, providing predictive analytics for fuel price forecasting, enhancing supply chain management for bunkering operations, and enabling real-time monitoring of engine performance to maximize fuel efficiency and ensure regulatory compliance.

What challenges does the Marine Fuel Oil Market face in transitioning to new fuels?

The market faces challenges such as regulatory uncertainty regarding future emission standards, high capital expenditure for new bunkering infrastructure and vessel conversions, the higher cost of alternative fuels compared to conventional options, and safety concerns related to handling and storing novel fuel types.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted