Logistic Real Estate Market

Logistic Real Estate Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_706011 | Last Updated : August 17, 2025 |

Format : ![]()

![]()

![]()

![]()

Logistic Real Estate Market Size

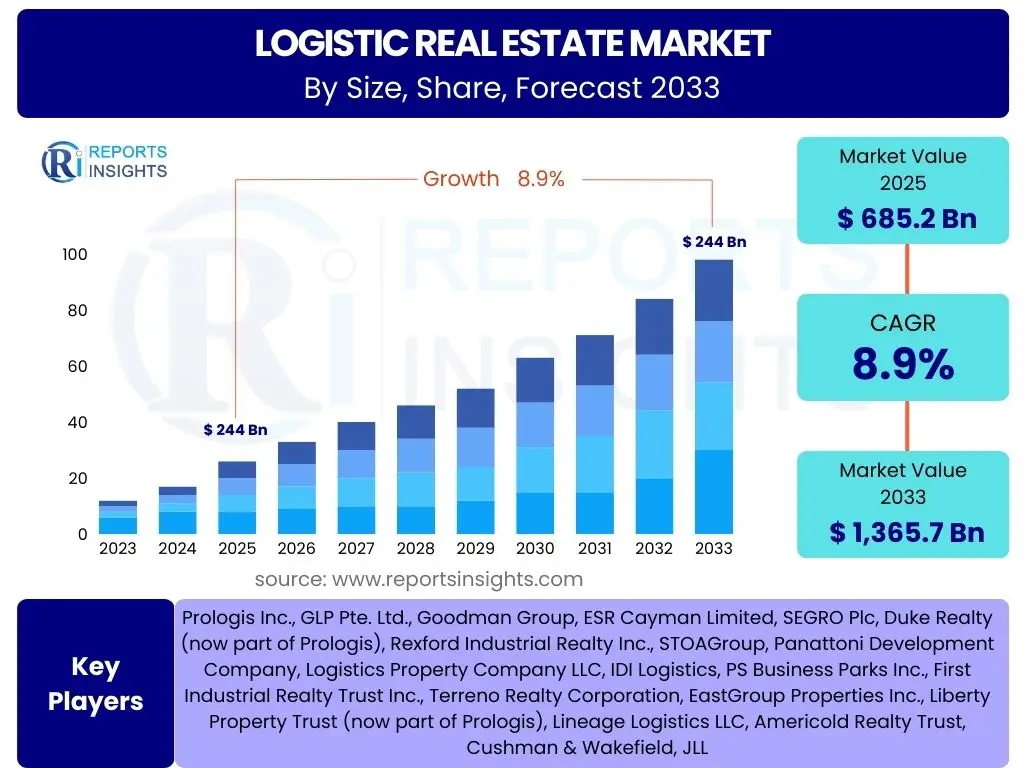

According to Reports Insights Consulting Pvt Ltd, The Logistic Real Estate Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 8.9% between 2025 and 2033. The market is estimated at USD 685.2 Billion in 2025 and is projected to reach USD 1,365.7 Billion by the end of the forecast period in 2033.

Key Logistic Real Estate Market Trends & Insights

The logistic real estate market is experiencing significant transformation driven by evolving consumer demands and technological advancements. Common inquiries revolve around the impact of e-commerce, the need for supply chain resilience, the adoption of automation, and the growing emphasis on sustainable practices. Users are keen to understand how these macro trends are reshaping facility design, location strategies, and investment priorities within the sector. The shift towards last-mile delivery and localized distribution networks is also a frequently discussed topic, highlighting a move away from traditional large-scale warehousing in favor of more agile and strategically positioned assets.

Further analysis indicates a strong interest in how geopolitical factors and trade dynamics influence real estate decisions. The increasing complexity of global supply chains necessitates greater flexibility and diversification in logistic networks, directly impacting demand for modern, adaptable facilities. There is a clear trend towards integrating advanced analytics and IoT within logistic properties to enhance operational efficiency and predictive maintenance, making 'smart warehouses' a key area of focus for both developers and tenants. Furthermore, the imperative for environmental, social, and governance (ESG) compliance is no longer a niche concern but a fundamental driver, pushing developers towards greener building standards and energy-efficient designs to meet corporate sustainability goals and investor expectations.

- Accelerated growth of e-commerce driving demand for warehousing and distribution centers.

- Increased focus on supply chain resilience and diversification, leading to nearshoring and regional hub development.

- Rising adoption of automation and robotics within warehouses, necessitating specialized facility designs.

- Growing demand for sustainable and green logistic properties, driven by ESG mandates and energy efficiency goals.

- Expansion of urban logistics and last-mile delivery hubs to meet faster delivery expectations.

- Development of multi-story warehouses in densely populated areas due to land scarcity.

- Integration of advanced data analytics and IoT for smart warehouse management and optimization.

- Shift towards flexible lease terms and co-warehousing models to accommodate fluctuating demand.

- Increased investment in cold storage facilities driven by pharmaceutical and fresh food logistics.

AI Impact Analysis on Logistic Real Estate

User queries regarding AI's impact on logistic real estate primarily focus on its role in enhancing operational efficiency, optimizing space utilization, and enabling predictive maintenance. There is significant interest in how AI algorithms can revolutionize warehouse management systems, leading to more intelligent inventory placement, expedited order fulfillment, and autonomous navigation for robotic equipment. Concerns often revolve around the initial investment costs, the need for specialized infrastructure to support AI technologies, and the potential impact on labor requirements within logistic facilities. However, the overarching expectation is that AI will be a transformative force, enabling greater throughput and accuracy while reducing human error.

Furthermore, users are keen to understand AI's implications for facility design and development. AI-powered analytics can inform site selection by predicting optimal locations based on traffic patterns, demographic shifts, and supply chain bottlenecks. Predictive analytics can also assess building performance, identifying potential maintenance issues before they arise, thereby reducing downtime and operational costs. The integration of AI in building management systems promises to create truly 'smart' buildings that adapt to operational needs, optimize energy consumption, and enhance security, contributing significantly to the long-term value and efficiency of logistic assets. This technological evolution is pushing the boundaries of traditional real estate management towards a more data-driven and autonomous operational model.

- Enhanced warehouse automation and robotics coordination through AI-driven systems.

- Optimized inventory management and slotting using predictive AI algorithms.

- Improved route optimization and last-mile delivery efficiency via AI analytics.

- Predictive maintenance for equipment and infrastructure, minimizing downtime.

- Demand forecasting and supply chain planning enhanced by machine learning models.

- Smart building management systems for energy efficiency and operational control.

- Automated quality control and damage detection in logistics operations.

- Data-driven site selection and facility design optimization.

- Enhanced security and surveillance through AI-powered anomaly detection.

Key Takeaways Logistic Real Estate Market Size & Forecast

Key takeaways from the logistic real estate market size and forecast consistently highlight the sector's robust growth trajectory, primarily fueled by the sustained expansion of e-commerce and the increasing complexity of global supply chains. Users frequently inquire about the longevity of this growth, the most promising investment avenues, and the critical factors that will shape future market dynamics. The market's resilience, even amidst economic fluctuations, underscores its essential role in the modern economy, positioning it as an attractive asset class for investors seeking stable long-term returns. The forecast suggests a continued upward trend, driven by both organic demand and strategic advancements in logistics infrastructure.

Another crucial insight is the accelerating demand for modern, high-specification facilities that can accommodate advanced automation, adhere to stringent environmental standards, and support intricate multi-channel distribution strategies. The market is not merely growing in size but also evolving in sophistication, with a premium placed on properties that offer technological readiness and strategic geographical positioning. Investment opportunities are increasingly concentrated in urban logistics, cold storage, and specialized facilities that cater to specific industry needs, reflecting a nuanced market that rewards foresight and adaptability. This transformation underscores a shift from general-purpose warehousing to highly specialized and technologically integrated logistic hubs.

- The logistic real estate market is poised for significant, sustained growth through 2033.

- E-commerce remains the primary catalyst for demand for modern warehousing and distribution centers.

- Investment is shifting towards strategically located, high-tech, and sustainable properties.

- Supply chain resilience and diversification are driving new development and re-localization efforts.

- The sector demonstrates strong resilience against economic downturns due to its essential nature.

- Urban logistics and last-mile facilities represent high-growth investment opportunities.

- Technological integration, including automation and AI, is becoming a prerequisite for competitive facilities.

Logistic Real Estate Market Drivers Analysis

The logistic real estate market's expansion is fundamentally propelled by several interconnected global trends. The exponential rise of e-commerce, amplified by changes in consumer purchasing habits, necessitates an expansive network of warehouses and distribution centers to facilitate rapid order fulfillment and last-mile delivery. This demand extends beyond sheer volume, requiring specialized facilities capable of handling diverse product types and supporting complex inventory management systems. Concurrently, increasing urbanization concentrates consumer bases, driving the need for strategically located, often multi-story, logistics hubs within or proximate to metropolitan areas to optimize delivery times and reduce transportation costs.

Furthermore, the imperative for supply chain resilience and diversification, largely influenced by recent global disruptions, is encouraging companies to re-evaluate and often expand their geographic footprint, leading to new construction and modernization of existing logistic assets. Technological advancements, particularly in automation, AI, and IoT, are transforming warehouses into highly efficient, data-driven operations, which in turn fuels demand for purpose-built or retrofitted properties. Lastly, significant infrastructure development, including improved road networks, port expansions, and intermodal facilities, enhances connectivity and accessibility for logistic operations, thereby increasing the attractiveness and operational efficiency of real estate situated within these improved corridors.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| E-commerce Growth & Online Retail Penetration | +2.5% | Global, particularly North America, Asia Pacific, Europe | 2025-2033 |

| Supply Chain Resilience & Diversification | +1.8% | North America, Europe, Southeast Asia | 2025-2030 |

| Urbanization & Demand for Last-Mile Delivery | +1.5% | Major Metropolitan Areas Globally | 2025-2033 |

| Technological Advancements (Automation, AI, IoT) | +1.2% | Developed Economies, Innovating Regions | 2026-2033 |

| Infrastructure Development & Connectivity | +0.8% | Emerging Markets, Key Trade Routes | 2025-2033 |

Logistic Real Estate Market Restraints Analysis

Despite robust growth, the logistic real estate market faces several significant restraints that could temper its expansion. One of the primary challenges is the scarcity of available land, particularly in prime urban and peri-urban locations essential for last-mile delivery and efficient distribution. This land constraint often leads to inflated property prices and increased development costs, making it difficult for developers to acquire suitable sites at economically viable rates. Additionally, stringent regulatory hurdles, including complex zoning laws, environmental impact assessments, and lengthy permitting processes, can significantly delay project timelines and increase the overall cost of development, discouraging new investments.

Another notable restraint is the escalating cost of construction materials and labor, which directly impacts project profitability and the affordability of new logistic facilities. Global supply chain disruptions can exacerbate these material shortages and price volatilities, further complicating development efforts. Furthermore, a persistent shortage of skilled labor for both construction and operations within logistics facilities can impede expansion and efficient functioning. Lastly, geopolitical instability, trade wars, and protectionist policies can disrupt established supply chains, leading to uncertainty in demand for logistic space and deterring cross-border investments, thereby creating a cautious investment environment in certain regions.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Land Scarcity & High Acquisition Costs | -1.0% | Global, particularly Tier 1 Cities in Developed Markets | 2025-2033 |

| Regulatory Hurdles & Permitting Delays | -0.7% | Europe, parts of Asia Pacific, North America | 2025-2030 |

| Rising Construction Costs & Labor Shortages | -0.5% | Global | 2025-2029 |

| Geopolitical Instability & Trade Disruptions | -0.4% | Specific Conflict Zones, Major Trade Blocs | 2025-2028 |

| High Interest Rates & Capital Accessibility | -0.3% | Global, particularly emerging economies | 2025-2027 |

Logistic Real Estate Market Opportunities Analysis

The logistic real estate market presents numerous opportunities for growth and innovation, driven by evolving industry needs and technological advancements. One significant area is the expansion of cold storage facilities, fueled by the rising demand for fresh food, pharmaceuticals, and other temperature-sensitive goods, requiring specialized infrastructure that maintains precise climate control. The burgeoning pharmaceutical and life sciences sector, in particular, requires highly specialized cold chain logistics, opening up a niche but high-value segment within the market. This creates a compelling opportunity for developers and investors to cater to increasingly complex storage and distribution requirements.

Another major opportunity lies in the development of multi-story warehouses, especially in land-constrained urban areas. These innovative structures maximize vertical space, addressing land scarcity and enabling closer proximity to dense consumer populations for efficient last-mile delivery. The integration of advanced technologies, such as automation, robotics, and artificial intelligence, also presents an opportunity to create 'smart warehouses' that enhance operational efficiency, reduce labor costs, and provide real-time data for optimized logistics. Furthermore, the growing emphasis on sustainability and ESG principles is driving demand for green buildings, offering opportunities for developers to invest in energy-efficient designs, renewable energy sources, and sustainable construction practices that align with corporate responsibility goals and attract environmentally conscious tenants.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development of Cold Storage Facilities | +1.5% | Global, high demand in APAC, North America, Europe | 2025-2033 |

| Expansion of Multi-Story & Urban Logistics Centers | +1.2% | Tier 1 Cities in Asia Pacific, Europe, North America | 2025-2033 |

| Integration of Advanced Automation & AI in Facilities | +1.0% | Developed Economies, Tech-Forward Regions | 2026-2033 |

| Investment in Sustainable & Green Logistics Properties | +0.8% | Europe, North America, Countries with strong ESG mandates | 2025-2033 |

| Reconfiguration of Supply Chains (Reshoring/Nearshoring) | +0.7% | North America, Europe, India, Southeast Asia | 2025-2030 |

Logistic Real Estate Market Challenges Impact Analysis

The logistic real estate market faces several formidable challenges that require strategic responses from developers, investors, and operators. Rapid technological advancements, while offering opportunities, also pose a challenge as existing facilities may become obsolete if not consistently upgraded to accommodate new automation and AI systems. This necessitates significant capital expenditure for retrofitting or new development, increasing the financial burden on stakeholders. Furthermore, the ongoing global economic uncertainties, including inflationary pressures and potential recessionary trends, can impact consumer spending and trade volumes, leading to fluctuations in demand for logistic space and affecting rental yields. Such macroeconomic volatility demands agile investment and operational strategies to mitigate risks.

Another significant challenge is the increasing intensity of competition within the market, as more institutional investors and developers enter the logistic real estate sector attracted by its robust performance. This heightened competition can lead to bidding wars for prime assets, driving up acquisition costs and compressing yields. Additionally, climate change and the increasing frequency of extreme weather events pose physical risks to logistic properties, requiring resilient designs and strategic location choices to ensure business continuity. The sector must also contend with a persistent shortage of skilled labor for highly automated facilities, necessitating investment in training and talent retention programs to maintain operational efficiency and keep pace with technological evolution.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Rapid Technological Obsolescence of Existing Facilities | -0.8% | Developed Markets, Older Industrial Zones | 2026-2033 |

| Economic Volatility & Inflationary Pressures | -0.6% | Global, particularly regions with high inflation | 2025-2028 |

| Intensified Market Competition & Yield Compression | -0.5% | Major Investment Hubs Globally | 2025-2033 |

| Climate Change Risks & Need for Resilient Infrastructure | -0.4% | Coastal Areas, Flood Plains, Disaster-Prone Regions | 2027-2033 |

| Talent Shortage for Automated & Tech-Driven Operations | -0.3% | Global, especially in rapidly automating regions | 2025-2033 |

Logistic Real Estate Market - Updated Report Scope

This comprehensive report provides an in-depth analysis of the global Logistic Real Estate Market, offering detailed insights into market dynamics, segmentation, regional trends, and competitive landscape. The scope encompasses a thorough examination of market drivers, restraints, opportunities, and challenges, along with a forward-looking forecast period to provide stakeholders with actionable intelligence for strategic decision-making. The report aims to deliver a holistic view of the market's evolution, highlighting key shifts in demand, technological integration, and investment patterns across various property types and end-use industries.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 685.2 Billion |

| Market Forecast in 2033 | USD 1,365.7 Billion |

| Growth Rate | 8.9% |

| Number of Pages | 247 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Prologis Inc., GLP Pte. Ltd., Goodman Group, ESR Cayman Limited, SEGRO Plc, Duke Realty (now part of Prologis), Rexford Industrial Realty Inc., STOAGroup, Panattoni Development Company, Logistics Property Company LLC, IDI Logistics, PS Business Parks Inc., First Industrial Realty Trust Inc., Terreno Realty Corporation, EastGroup Properties Inc., Liberty Property Trust (now part of Prologis), Lineage Logistics LLC, Americold Realty Trust, Cushman & Wakefield, JLL |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The logistic real estate market is extensively segmented to provide a granular view of its diverse components and dynamics. These segments allow for a targeted analysis of demand drivers, regional preferences, and technological adoption across various property types, end-use industries, facility sizes, and ownership models. Understanding these segmentations is critical for stakeholders to identify niche opportunities, optimize investment strategies, and tailor development initiatives to specific market needs.

- By Property Type

- Warehouses & Distribution Centers (Class A, Class B, Class C)

- Industrial Parks

- Cold Storage Facilities

- Cross-Dock Facilities

- Last-Mile Delivery Hubs

- Flex & Light Industrial Properties

- By End-Use Industry

- E-commerce & Retail

- Manufacturing

- Third-Party Logistics (3PL)

- Food & Beverage

- Pharmaceutical & Healthcare

- Automotive

- Consumer Goods

- Other Industries

- By Size

- Small (less than 50,000 sq ft)

- Medium (50,000 - 200,000 sq ft)

- Large (more than 200,000 sq ft)

- By Ownership

- Owner-Occupied

- Leased/Rented

Regional Highlights

- North America: Continues to be a dominant market, driven by robust e-commerce growth, advanced logistics infrastructure, and a strong push for supply chain resilience. Key markets include the major port cities and logistics corridors in the U.S. (e.g., California, Texas, New Jersey, Pennsylvania) and Canada. Demand for Class A facilities and automation-ready spaces is particularly high.

- Europe: Characterized by strong demand for modern warehousing, particularly in core Western European markets (e.g., Germany, France, UK, Netherlands) and emerging Central and Eastern European logistics hubs (e.g., Poland, Czech Republic) due to lower costs and strategic location. Emphasis on ESG compliance and multi-modal transport connectivity is a significant regional trend.

- Asia Pacific (APAC): The fastest-growing region, fueled by burgeoning e-commerce markets (China, India, Southeast Asia), rapid urbanization, and significant infrastructure investments. Land scarcity in tier-one cities drives the development of multi-story warehouses and vertical logistics solutions. Cold chain and pharmaceutical logistics are emerging as strong sub-segments.

- Latin America: Experiencing substantial growth, particularly in Mexico (due to nearshoring trends and proximity to the U.S. market) and Brazil. E-commerce expansion and infrastructure improvements are key drivers, though economic volatility and regulatory complexities can pose challenges.

- Middle East and Africa (MEA): Growth is driven by strategic geographic positioning, government investments in logistics infrastructure (e.g., UAE, Saudi Arabia, Egypt), and increasing regional trade. Development of logistics free zones and a focus on diversifying economies away from oil are creating new demand for modern facilities.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Logistic Real Estate Market.- Prologis Inc.

- GLP Pte. Ltd.

- Goodman Group

- ESR Cayman Limited

- SEGRO Plc

- Duke Realty (now part of Prologis)

- Rexford Industrial Realty Inc.

- STOAGroup

- Panattoni Development Company

- Logistics Property Company LLC

- IDI Logistics

- PS Business Parks Inc.

- First Industrial Realty Trust Inc.

- Terreno Realty Corporation

- EastGroup Properties Inc.

- Liberty Property Trust (now part of Prologis)

- Lineage Logistics LLC

- Americold Realty Trust

- Cushman & Wakefield

- JLL

Frequently Asked Questions

Analyze common user questions about the Logistic Real Estate market and generate a concise list of summarized FAQs reflecting key topics and concerns.What factors are driving the growth of the logistic real estate market?

The primary drivers include the exponential growth of e-commerce, increasing demand for faster delivery, the need for resilient and diversified supply chains, technological advancements like automation and AI, and ongoing urbanization necessitating urban logistics facilities.

How is technology impacting logistic real estate design and operations?

Technology is leading to highly automated and smart warehouses, featuring advanced robotics, AI-driven inventory management, IoT for real-time monitoring, and optimized layouts. This enhances efficiency, reduces labor costs, and supports complex e-commerce fulfillment, influencing demand for purpose-built or retrofitted facilities.

What are the key investment opportunities in the current logistic real estate market?

Key opportunities lie in cold storage facilities, multi-story urban logistics centers, last-mile delivery hubs, and properties designed for advanced automation. Investments are also strong in regions experiencing rapid e-commerce growth and supply chain reconfiguration, such as Asia Pacific and certain North American and European corridors.

What challenges does the logistic real estate market face?

Major challenges include land scarcity in prime locations, rising construction and labor costs, complex regulatory hurdles, increasing competition leading to yield compression, and the need for continuous technological upgrades to avoid obsolescence. Economic volatility and climate change risks also pose significant challenges.

Which regions are leading the growth in the logistic real estate sector?

Asia Pacific, particularly China, India, and Southeast Asian nations, is the fastest-growing region due to booming e-commerce and urbanization. North America remains a dominant market with high demand for modern logistics space, while Europe also shows strong growth driven by cross-border trade and sustainability initiatives.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted