LNG Liquefaction Equipment Market

LNG Liquefaction Equipment Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_709786 | Last Updated : December 17, 2025 |

Format : ![]()

![]()

![]()

![]()

LNG Liquefaction Equipment Market Size

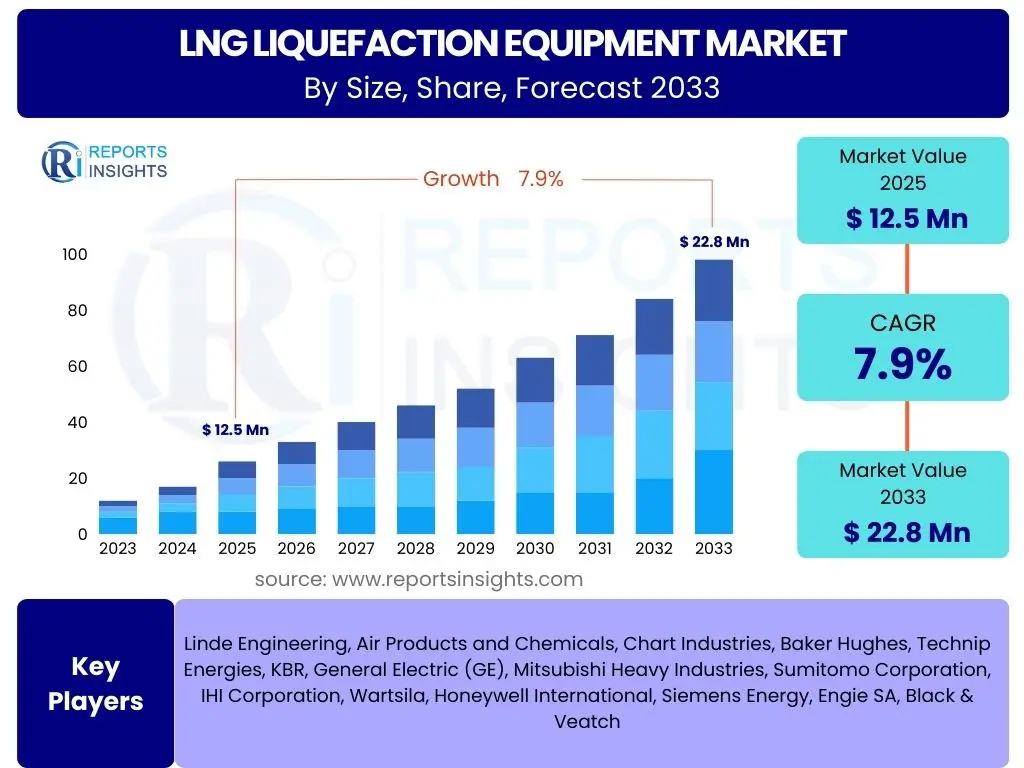

According to Reports Insights Consulting Pvt Ltd, The LNG Liquefaction Equipment Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 7.9% between 2025 and 2033. The market is estimated at USD 12.5 Billion in 2025 and is projected to reach USD 22.8 Billion by the end of the forecast period in 2033. This growth is primarily fueled by increasing global demand for natural gas as a cleaner bridging fuel, coupled with ongoing investments in new liquefaction terminals and expansion projects. The market's expansion is further supported by technological advancements aimed at improving efficiency and reducing the environmental footprint of LNG production facilities.

The trajectory of the LNG liquefaction equipment market is significantly influenced by global energy security concerns and the transition towards lower-carbon energy sources. Countries are increasingly seeking reliable and diverse energy supplies, positioning LNG as a crucial component of their energy mix. This demand stimulates investment in both large-scale export facilities and smaller, more flexible liquefaction solutions, driving the procurement of advanced equipment. Additionally, the drive for operational optimization and cost reduction within the LNG industry is pushing manufacturers to innovate, offering more efficient and modular equipment solutions that cater to various project scales and environmental regulations.

Key LNG Liquefaction Equipment Market Trends & Insights

The LNG Liquefaction Equipment market is currently undergoing transformative changes, driven by a confluence of technological advancements, evolving energy policies, and shifting market demands. Users frequently inquire about the leading trends shaping investment decisions and operational strategies within this sector. Key among these are the increasing adoption of modular and standardized liquefaction solutions, which offer faster deployment and scalability, particularly for mid-scale and small-scale projects. Furthermore, there is a pronounced focus on enhancing energy efficiency and reducing greenhouse gas emissions across the liquefaction process, pushing for innovations in compression, refrigeration, and heat exchange technologies. The industry is also observing a shift towards greater integration of digital solutions for predictive maintenance and operational optimization, alongside a growing interest in carbon capture and storage readiness for future-proofing facilities.

- Modularization and Standardization: Increased preference for pre-fabricated, skidded, and standardized units for quicker deployment, reduced construction costs, and enhanced project scalability across various capacities.

- Energy Efficiency Improvement: Focus on advanced refrigeration cycles, highly efficient compressors, and improved heat exchange technologies to reduce power consumption and operational expenses.

- Decarbonization Efforts: Integration of carbon capture and storage (CCS) technologies, exploration of electric drives for compressors, and readiness for hydrogen blending to minimize the carbon footprint of liquefaction plants.

- Small-Scale and Mid-Scale LNG: Rising demand for smaller, more flexible liquefaction plants catering to regional energy needs, marine bunkering, heavy-duty transport, and remote power generation.

- Digitalization and Automation: Implementation of advanced control systems, AI-driven predictive maintenance, and real-time data analytics for optimizing plant performance, reducing downtime, and enhancing safety.

- Floating Liquefied Natural Gas (FLNG): Continued development and deployment of offshore liquefaction facilities, offering flexibility in accessing remote gas reserves and reducing land-use requirements.

- Sustainability and Environmental Compliance: Strict adherence to environmental regulations and increasing emphasis on technologies that minimize emissions and manage water resources efficiently throughout the liquefaction process.

AI Impact Analysis on LNG Liquefaction Equipment

User inquiries regarding the impact of Artificial Intelligence (AI) on LNG liquefaction equipment frequently center on its potential to revolutionize operational efficiency, safety, and predictive maintenance. Stakeholders are keen to understand how AI can move beyond traditional automation to deliver real-time insights, optimize complex processes, and mitigate risks. The consensus points towards AI’s critical role in transforming how liquefaction plants are managed, from optimizing refrigeration cycles to predicting equipment failures. There is also significant interest in AI's capacity to enhance the design phase of new equipment, leading to more efficient and reliable systems, as well as its application in supply chain management for spare parts and operational planning. The expectations are high for AI to reduce operational expenditures, improve energy efficiency, and increase overall plant reliability and safety.

Furthermore, the discussion extends to AI's role in supporting the industry's decarbonization goals. By precisely controlling process parameters, AI can help minimize energy consumption and reduce emissions, including methane slip, which is a major environmental concern. The ability of AI to analyze vast datasets from sensors and operational logs allows for the identification of subtle anomalies that precede equipment malfunctions, thereby enabling proactive interventions and extending asset lifespans. This level of foresight not only enhances safety but also translates directly into significant cost savings and improved operational continuity, making AI an indispensable tool for future LNG liquefaction operations and equipment design.

- Predictive Maintenance: AI algorithms analyze sensor data from compressors, turbines, and heat exchangers to predict potential failures, enabling proactive maintenance and reducing unscheduled downtime.

- Operational Optimization: AI-driven systems fine-tune process parameters such as temperature, pressure, and flow rates in real-time to maximize liquefaction efficiency and minimize energy consumption.

- Enhanced Safety: AI monitors operational conditions and detects anomalies that could lead to hazardous situations, providing early warnings and facilitating rapid response.

- Energy Management: AI optimizes power consumption across the plant, especially for large electrical loads like compressors, contributing to lower operational costs and reduced emissions.

- Process Control and Automation: Advanced AI models automate complex control sequences, improving process stability and reducing the need for manual intervention.

- Equipment Design Enhancement: AI can be used in the design phase to simulate performance under various conditions, identifying optimal configurations for new liquefaction equipment components, such as expanders and refrigerants.

- Supply Chain Optimization: AI assists in forecasting demand for spare parts, optimizing inventory levels, and streamlining logistics for equipment components, ensuring timely availability and reducing carrying costs.

Key Takeaways LNG Liquefaction Equipment Market Size & Forecast

Common user questions regarding key takeaways from the LNG Liquefaction Equipment market size and forecast consistently highlight the drivers of growth, the impact of sustainability trends, and the strategic opportunities for market participants. The overarching insight is that the market is poised for robust expansion, primarily due to the increasing global natural gas demand, driven by energy transition strategies and energy security mandates. This growth will be significantly shaped by the twin imperatives of efficiency and environmental responsibility, pushing for innovations in modularity, energy conservation, and emissions reduction across all equipment categories. The forecast suggests that investments in both large-scale export facilities and agile, small-scale LNG projects will continue to define market dynamics, offering diverse avenues for equipment manufacturers and technology providers.

A critical takeaway for stakeholders is the evolving competitive landscape, where technological differentiation will be paramount. Companies that can offer solutions integrating advanced automation, AI-driven predictive capabilities, and sustainable design features will gain a significant advantage. Furthermore, the market's regional dynamics, particularly the burgeoning demand from Asia-Pacific and the strategic importance of North American gas exports, will dictate where major investments in liquefaction infrastructure and equipment will occur. Understanding these regional nuances, alongside the global shift towards cleaner energy, is essential for any entity looking to capitalize on the sustained growth projected for the LNG liquefaction equipment market over the next decade.

- Sustainable Market Expansion: The market is projected for significant growth, driven by global natural gas demand as a crucial bridging fuel in the energy transition.

- Technological Innovation Imperative: Future growth is heavily reliant on advancements in energy efficiency, modularity, and decarbonization technologies for liquefaction equipment.

- Dual Market Focus: Opportunities exist across both large-scale export-oriented projects and flexible, small-scale LNG solutions catering to diverse regional demands.

- AI as a Core Enabler: Artificial intelligence and digitalization will increasingly define operational efficiency, predictive maintenance, and overall plant reliability, becoming a key differentiator for equipment providers.

- Regional Demand Dynamics: Asia-Pacific remains a primary growth engine for LNG consumption, while North America and emerging economies in Africa and Latin America present significant investment potential for liquefaction infrastructure.

- Capital Expenditure Intensity: High upfront capital costs for new projects will continue to influence market entry and expansion strategies for both producers and equipment suppliers.

LNG Liquefaction Equipment Market Drivers Analysis

The LNG liquefaction equipment market is propelled by a robust set of drivers, fundamentally rooted in global energy dynamics and environmental objectives. A primary driver is the escalating global demand for natural gas, considered a cleaner alternative to coal and oil for power generation and industrial applications, especially in emerging economies. This sustained demand necessitates significant investments in liquefaction capacity to facilitate gas transportation across continents. Furthermore, the increasing focus on energy security and diversification of supply routes, exacerbated by geopolitical shifts, prompts many nations to enhance their LNG import and export capabilities, thereby fueling the need for advanced liquefaction equipment.

Technological advancements also play a crucial role, with innovations in liquefaction processes leading to more efficient, cost-effective, and environmentally friendly equipment. This includes the development of modular and floating LNG (FLNG) solutions, which offer greater flexibility and quicker deployment, opening up previously uneconomical gas reserves. Moreover, government policies and incentives promoting the use of natural gas and reducing carbon emissions are indirectly boosting the market, as natural gas liquefaction is a key enabler for meeting these objectives. The expansion of natural gas infrastructure globally, including pipelines and storage facilities, further underpins the growth in demand for liquefaction equipment.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing Global Natural Gas Demand | +2.1% | Asia Pacific, Europe, Emerging Markets | 2025-2033 (Long-term) |

| Energy Security and Diversification | +1.8% | Europe, North America, East Asia | 2025-2030 (Medium-term) |

| Technological Advancements in Liquefaction | +1.5% | Global | 2025-2033 (Ongoing) |

| Expansion of Gas Infrastructure | +1.2% | North America, Middle East, Africa | 2026-2033 (Medium to Long-term) |

| Supportive Government Policies | +0.8% | Global, especially EU and Asia | 2025-2030 (Medium-term) |

LNG Liquefaction Equipment Market Restraints Analysis

Despite the strong growth drivers, the LNG liquefaction equipment market faces several significant restraints that could temper its expansion. One of the most prominent challenges is the high capital expenditure required for designing, constructing, and commissioning liquefaction plants. These substantial upfront costs can deter potential investors, particularly for large-scale projects, and extend the payback period, making financial closure complex. This capital intensity often leads to delays or cancellations of planned projects, directly impacting the demand for new equipment. Furthermore, the regulatory landscape governing environmental approvals, safety standards, and operational permits for LNG facilities is increasingly stringent and complex. Navigating these regulations can be time-consuming and costly, imposing additional hurdles for market participants.

Another critical restraint is the inherent volatility of natural gas prices, which can significantly affect the economic viability of new liquefaction projects. Fluctuations in global energy markets introduce uncertainty for project developers and off-takers, making long-term investment decisions riskier. Geopolitical instabilities and trade disputes also pose a threat, as they can disrupt supply chains for essential equipment components, lead to sanctions, or impact the overall investment climate in key regions. Additionally, public opposition and environmental concerns related to the development of large industrial facilities, including the potential for methane emissions and impacts on local ecosystems, can slow down or halt project progression, thereby limiting market growth.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Capital Expenditure | -1.5% | Global | 2025-2033 (Long-term) |

| Volatile Natural Gas Prices | -1.2% | Global | 2025-2030 (Medium-term) |

| Stringent Environmental Regulations | -1.0% | Europe, North America, Oceania | 2025-2033 (Ongoing) |

| Geopolitical Instability and Trade Disputes | -0.9% | Global, particularly major gas-producing/consuming regions | 2025-2028 (Short to Medium-term) |

| Supply Chain Disruptions | -0.7% | Global | 2025-2027 (Short-term) |

LNG Liquefaction Equipment Market Opportunities Analysis

The LNG liquefaction equipment market is rife with opportunities, particularly stemming from the evolving global energy landscape and technological innovation. One significant area is the increasing adoption of small-scale and mid-scale LNG facilities. These smaller plants cater to diverse applications such as marine bunkering, remote power generation, and industrial fuel supply in regions without extensive pipeline networks, offering faster project timelines and lower upfront investment compared to traditional mega-projects. This trend opens new market segments for equipment providers who can offer flexible, modular, and cost-effective solutions tailored to these specialized needs.

Furthermore, the push for decarbonization within the energy sector presents a unique opportunity for advanced equipment that integrates carbon capture and storage (CCS) technologies or can facilitate the use of renewable energy sources for liquefaction. Manufacturers developing highly energy-efficient compressors, expanders, and heat exchangers will find increased demand as operators seek to reduce their carbon footprint and operational costs. The growing interest in Floating Liquefied Natural Gas (FLNG) vessels also represents a substantial opportunity, enabling the monetization of offshore gas reserves that are otherwise uneconomical to develop. As global gas demand continues to grow and environmental regulations tighten, innovation in sustainable and adaptable liquefaction solutions will be key to unlocking these market opportunities.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growth in Small-Scale & Mid-Scale LNG | +1.9% | Asia Pacific, Africa, Latin America | 2025-2033 (Long-term) |

| Demand for Floating LNG (FLNG) Solutions | +1.4% | Offshore regions, Africa, Southeast Asia | 2026-2033 (Medium to Long-term) |

| Integration of Carbon Capture & Storage (CCS) | +1.1% | Europe, North America, Australia | 2028-2033 (Long-term) |

| Advancements in Energy-Efficient Technologies | +1.0% | Global | 2025-2033 (Ongoing) |

| Expansion into New End-Use Applications | +0.8% | Global (Marine, Heavy-duty Transport) | 2025-2030 (Medium-term) |

LNG Liquefaction Equipment Market Challenges Impact Analysis

The LNG liquefaction equipment market faces several formidable challenges that require strategic navigation from industry participants. One primary challenge is the intense competition and price pressure from established global manufacturers and new entrants, which can compress profit margins and demand continuous innovation. This competitive environment necessitates significant R&D investments to maintain technological leadership and offer differentiated solutions. Furthermore, the complexity of designing and manufacturing highly specialized liquefaction equipment, which operates under extreme cryogenic conditions and requires stringent safety standards, poses a significant technical challenge. Ensuring the reliability and longevity of such equipment is paramount for successful project execution and long-term operational viability.

Another key challenge involves managing the global supply chain, which can be susceptible to disruptions from geopolitical events, natural disasters, or pandemics. Sourcing specialized components, materials, and skilled labor from various international locations while maintaining quality and adherence to project timelines is a constant concern. Moreover, the industry grapples with a shortage of highly skilled engineers and technical personnel with expertise in cryogenic processes and large-scale plant operations. Attracting and retaining such talent is critical for designing, installing, and maintaining advanced liquefaction equipment. Addressing these multifaceted challenges will be essential for sustained growth and profitability within the LNG liquefaction equipment market.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Intense Competition and Price Pressure | -1.3% | Global | 2025-2033 (Ongoing) |

| Technological Complexity and R&D Costs | -1.1% | Global | 2025-2033 (Long-term) |

| Skilled Labor Shortage | -0.9% | Global, particularly developed economies | 2025-2030 (Medium-term) |

| Supply Chain Volatility | -0.8% | Global | 2025-2028 (Short to Medium-term) |

| Integration of New Technologies (e.g., AI, CCS) | -0.6% | Global | 2026-2033 (Medium to Long-term) |

LNG Liquefaction Equipment Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the global LNG Liquefaction Equipment Market, covering historical performance, current market dynamics, and future projections. The report offers detailed insights into market size, growth drivers, restraints, opportunities, and challenges affecting the industry from 2019 to 2033. It meticulously segments the market by equipment type, component, and application, alongside a thorough regional and country-level analysis. Key competitive landscapes, technological advancements, and the impact of emerging trends such as AI integration and decarbonization efforts are also examined to provide a holistic view for stakeholders seeking strategic intelligence.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 12.5 Billion |

| Market Forecast in 2033 | USD 22.8 Billion |

| Growth Rate | 7.9% |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Linde Engineering, Air Products and Chemicals, Chart Industries, Baker Hughes, Technip Energies, KBR, General Electric (GE), Mitsubishi Heavy Industries, Sumitomo Corporation, IHI Corporation, Wartsila, Honeywell International, Siemens Energy, Engie SA, Black & Veatch |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The LNG liquefaction equipment market is broadly segmented to reflect the diverse operational scales, technological approaches, and end-use applications driving demand across the globe. This segmentation provides a granular view of market dynamics, allowing for a detailed analysis of growth opportunities and competitive landscapes within each category. The primary segmentation criteria include the type of liquefaction facility, the key components utilized in the process, the specific refrigeration cycles employed, and the varied applications for the produced LNG. Understanding these segments is crucial for stakeholders to identify niche markets, target specific customer needs, and develop tailored equipment solutions that align with the evolving demands of the global energy sector.

Each segment possesses distinct characteristics and growth trajectories, influenced by factors such as project size, investment costs, geographic location, and environmental regulations. For instance, the small-scale LNG segment is experiencing rapid growth due to its versatility and ability to serve remote markets, while large-scale projects continue to dominate overall capacity for global exports. Similarly, advancements in specific components like compressors and heat exchangers, or the optimization of various refrigeration cycles, can significantly impact the efficiency and cost-effectiveness of liquefaction plants. Analyzing these segments helps in understanding the technological preferences and investment patterns across different parts of the LNG value chain.

- By Type:

- Large-Scale: Facilities with capacity typically exceeding 5 million tons per annum (MTPA), focused on global export markets.

- Mid-Scale: Plants with capacities ranging from 0.5 MTPA to 5 MTPA, often serving regional export or large industrial applications.

- Small-Scale: Facilities with capacities below 0.5 MTPA, catering to local distribution, marine bunkering, or remote power generation.

- Floating Liquefied Natural Gas (FLNG): Offshore units designed for liquefaction, storage, and offloading of natural gas from offshore fields.

- By Component:

- Compressors: Critical for gas compression in refrigeration cycles.

- Heat Exchangers: Essential for cooling and liquefaction of natural gas.

- Expanders: Used in specific refrigeration cycles to achieve cryogenic temperatures.

- Storage Tanks: For holding liquefied natural gas at cryogenic temperatures.

- Pumps: For transferring refrigerant and LNG within the facility.

- Valves: For controlling flow and pressure in the process.

- Control Systems: Automation and monitoring systems for plant operation.

- Others: Include various auxiliary equipment, instrumentation, and piping.

- By Refrigeration Cycle:

- Mixed Refrigerant Cycle (MRC): Widely used due to high efficiency and flexibility.

- Propane Pre-Cooled Mixed Refrigerant (C3MR): A highly efficient and common cycle, especially for large-scale plants.

- Single Mixed Refrigerant (SMR): Simplified cycle suitable for smaller plants.

- Nitrogen Expander Cycle: Used for small-scale or specific applications due to its simplicity and safety.

- Others: Includes other specialized or proprietary refrigeration technologies.

- By Application:

- Export Terminals: Large-scale facilities primarily for shipping LNG internationally.

- Fuel for Marine Vessels: Supplying LNG as bunker fuel for ships.

- Power Generation: Using LNG as fuel for electricity production.

- Industrial Fuel: Providing LNG for various industrial heating and process needs.

- Transport Fuel (Trucks, Rail): Supplying LNG for heavy-duty vehicles.

- Bunkering: Directly fueling ships with LNG.

Regional Highlights

- North America: This region, particularly the United States, is a major exporter of LNG due to abundant shale gas reserves. Significant investments in new liquefaction terminals and expansion projects continue to drive demand for large-scale and mid-scale equipment. Canada is also emerging with new export facilities.

- Europe: Driven by energy security concerns and the need to diversify gas supplies, Europe is investing heavily in regasification capacity, which indirectly stimulates the global liquefaction equipment market. Demand for small-scale LNG for bunkering and truck fueling is also growing as part of decarbonization efforts.

- Asia Pacific (APAC): The largest market for LNG consumption, with countries like China, Japan, India, and South Korea being major importers. Rapid industrialization and increasing energy demand in the region fuel the need for new large-scale liquefaction projects, particularly in Australia, Malaysia, and Indonesia, and a growing interest in small-scale LNG for regional distribution.

- Latin America: Countries like Brazil and Argentina show increasing interest in LNG for power generation and industrial use. Opportunities exist for both large-scale export projects, leveraging substantial gas reserves, and small-scale solutions for remote areas.

- Middle East and Africa (MEA): This region is a significant producer and exporter of natural gas, with countries like Qatar, Saudi Arabia, Nigeria, and Mozambique undertaking major liquefaction projects. The development of new gas fields and the drive for monetization of gas resources are key market drivers for advanced liquefaction equipment.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the LNG Liquefaction Equipment Market.- Linde Engineering

- Air Products and Chemicals

- Chart Industries

- Baker Hughes

- Technip Energies

- KBR

- General Electric (GE)

- Mitsubishi Heavy Industries

- Sumitomo Corporation

- IHI Corporation

- Wartsila

- Honeywell International

- Siemens Energy

- Engie SA

- Black & Veatch

Frequently Asked Questions

What are the primary factors driving growth in the LNG Liquefaction Equipment Market?

The market's growth is primarily driven by increasing global demand for natural gas as a cleaner energy source, heightened focus on energy security and supply diversification, and continuous technological advancements improving liquefaction efficiency and flexibility.

How is Artificial Intelligence impacting the design and operation of LNG liquefaction equipment?

AI is transforming the sector by enabling predictive maintenance, optimizing operational parameters for enhanced efficiency, improving safety protocols, and facilitating smarter equipment design through simulation and data analysis, ultimately reducing operational costs and downtime.

What role do small-scale and mid-scale LNG facilities play in the market?

Small-scale and mid-scale LNG facilities are crucial for serving niche markets such as marine bunkering, remote power generation, and industrial fuel supply. They offer faster deployment, lower capital expenditure, and greater flexibility, opening new growth avenues for equipment manufacturers.

What are the major challenges facing the LNG Liquefaction Equipment Market?

Key challenges include high capital expenditure requirements for projects, volatility in natural gas prices, stringent environmental regulations, geopolitical instability affecting supply chains, and a shortage of skilled technical labor, all of which can impact project viability and market expansion.

Which regions are expected to be key growth areas for LNG liquefaction equipment?

The Asia Pacific region, driven by robust energy demand from countries like China and India, remains a dominant growth area. North America, with its abundant gas reserves, and the Middle East and Africa, with new monetization projects, are also significant regions for investment and equipment demand.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted