Lithography Stepper Market

Lithography Stepper Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_701227 | Last Updated : July 29, 2025 |

Format : ![]()

![]()

![]()

![]()

Lithography Stepper Market Size

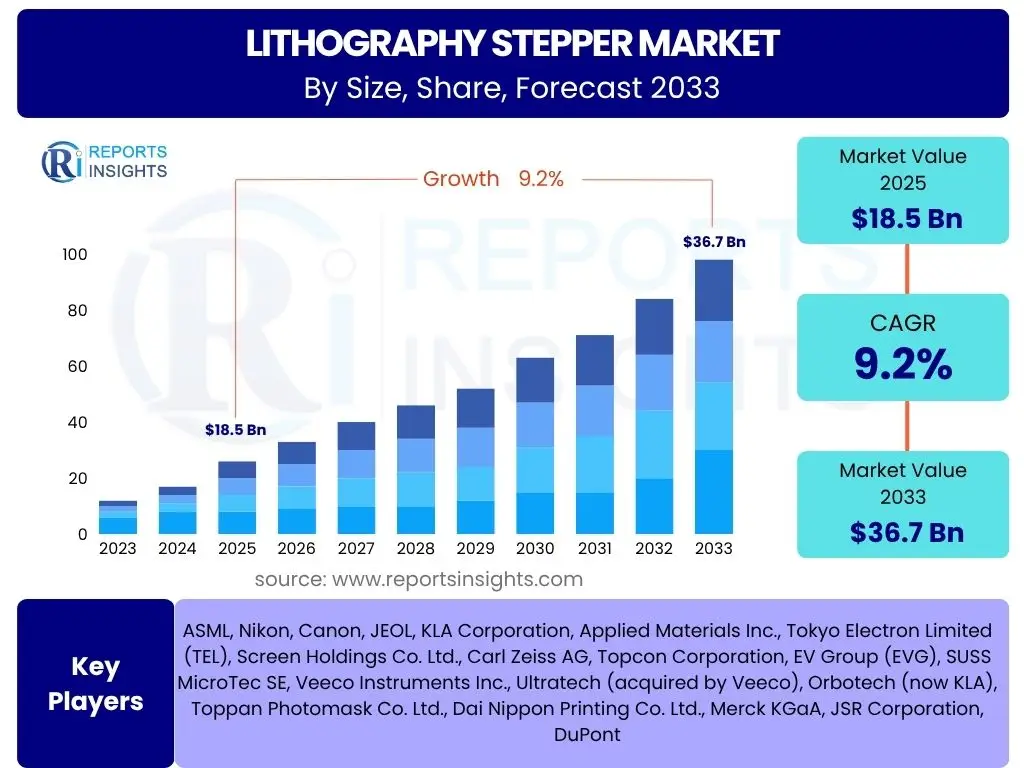

According to Reports Insights Consulting Pvt Ltd, The Lithography Stepper Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 9.2% between 2025 and 2033. The market is estimated at USD 18.5 Billion in 2025 and is projected to reach USD 36.7 Billion by the end of the forecast period in 2033.

The robust growth forecast for the lithography stepper market is primarily driven by the relentless demand for advanced semiconductors across various industries. As digital transformation accelerates globally, the need for high-performance computing, artificial intelligence, 5G connectivity, and the Internet of Things (IoT) devices continues to surge. Lithography steppers, being the foundational equipment for semiconductor manufacturing, directly benefit from this escalating demand, as they are crucial for producing the intricate circuitry required for next-generation chips. The increasing complexity and miniaturization of semiconductor devices necessitate more advanced and precise lithography solutions, further fueling market expansion.

Technological advancements, particularly the widespread adoption of Extreme Ultraviolet (EUV) lithography, are significant contributors to the market's projected expansion. EUV technology enables the fabrication of smaller, more powerful, and energy-efficient chips, which are essential for emerging applications. Furthermore, significant investments in new fabrication facilities (fabs) and capacity expansions by leading semiconductor manufacturers globally, particularly in Asia Pacific, North America, and Europe, are creating a sustained demand for state-of-the-art lithography equipment. Geopolitical factors emphasizing semiconductor supply chain resilience also encourage regional investments, contributing to the overall market growth trajectory.

Key Lithography Stepper Market Trends & Insights

Common user inquiries about the Lithography Stepper market often revolve around the evolution of chip manufacturing, the impact of next-generation technologies, and the strategic shifts influencing the industry. Users frequently seek information on the latest advancements in lithography, such as the transition to shorter wavelengths and higher numerical apertures, and how these innovations enable the production of more compact and powerful integrated circuits. There is also significant interest in understanding the ongoing shift towards multi-patterning techniques and advanced packaging, which complement core lithography processes to meet the demands for increased transistor density and improved performance.

Furthermore, users are keen to grasp the implications of rising global semiconductor demand, driven by AI, 5G, IoT, and high-performance computing, on the lithography equipment market. They often question how geopolitical dynamics and supply chain vulnerabilities are prompting regional investments in semiconductor manufacturing capabilities, thereby influencing the demand for lithography steppers. The integration of advanced computational lithography and metrology solutions, aimed at enhancing yield and efficiency, also forms a key area of user interest, reflecting a broader trend towards highly automated and optimized fabrication processes.

Finally, there's a growing awareness and concern about the environmental footprint of semiconductor manufacturing, leading to questions about sustainable practices within the lithography stepper industry. This includes inquiries into energy efficiency improvements, reduced chemical usage, and the development of more environmentally friendly processes. The collective insights derived from these user queries highlight a market characterized by rapid technological evolution, strategic geopolitical considerations, and a sustained pursuit of higher performance and efficiency.

- Dominance of Extreme Ultraviolet (EUV) Lithography: Increasing adoption for advanced node manufacturing (7nm and below) due to its capability to achieve higher resolution and integrate more transistors.

- Growth of Multi-Patterning Techniques: Continued reliance on techniques like multiple patterning (e.g., self-aligned double patterning SADP, self-aligned quadruple patterning SAQP) to extend DUV lithography capabilities for sub-10nm nodes.

- Computational Lithography Advancements: Enhanced use of advanced algorithms and computational models for mask optimization, process correction, and defect reduction, improving yield and throughput.

- Increased Focus on Advanced Packaging: The integration of lithography solutions tailored for heterogeneous integration and 3D stacking technologies, moving beyond traditional 2D scaling.

- Expansion of Foundries and IDM Investments: Significant capital expenditure by leading foundries and Integrated Device Manufacturers (IDMs) globally to build new fabs and expand existing capacities.

- Supply Chain Resilience and Regionalization: Efforts by governments and companies to diversify and secure semiconductor supply chains, leading to increased investments in lithography equipment in various regions.

- Sustainability and Energy Efficiency: Growing emphasis on developing more energy-efficient lithography processes and equipment to reduce environmental impact and operational costs.

- Rise of High Numerical Aperture (High-NA) EUV: Development and anticipated deployment of next-generation EUV systems with higher NA for even finer feature sizes and further miniaturization.

AI Impact Analysis on Lithography Stepper

Common user questions regarding the impact of Artificial Intelligence (AI) on Lithography Steppers often center on how AI can enhance the precision, efficiency, and yield of semiconductor manufacturing processes. Users are keen to understand the practical applications of AI in real-time process control, predictive maintenance of complex lithography equipment, and advanced defect detection. There is considerable interest in how machine learning algorithms can analyze vast datasets generated during lithography to optimize parameters, predict potential failures, and improve overall throughput, addressing the inherent complexities and stringent requirements of nanoscale fabrication.

Furthermore, inquiries frequently touch upon AI's role in computational lithography, particularly in accelerating the design of photomasks and optimizing illumination conditions for improved pattern fidelity. Users explore how AI can contribute to simulating and verifying lithography processes more rapidly, thereby reducing costly physical prototyping cycles and accelerating time-to-market for new chip designs. The potential for AI-driven automation in various stages of the lithography workflow, from initial design to final wafer inspection, also garners significant attention, highlighting expectations for reduced human intervention and enhanced operational consistency.

Finally, there are questions about the integration of AI with metrology and inspection tools, enabling more accurate and faster analysis of lithographic patterns and defects. Users are interested in how AI can identify subtle anomalies that might be missed by traditional methods, leading to earlier detection of issues and proactive process adjustments. These collective themes underscore a strong belief in AI's transformative potential to revolutionize lithography, making it more intelligent, autonomous, and capable of meeting the escalating demands of advanced semiconductor manufacturing.

- Enhanced Process Optimization: AI algorithms analyze real-time data from lithography processes to dynamically adjust parameters for optimal performance, leading to improved pattern fidelity and reduced variability.

- Predictive Maintenance: AI models predict potential equipment failures in lithography steppers, enabling proactive maintenance and reducing downtime, thereby maximizing equipment utilization and throughput.

- Advanced Defect Detection and Classification: AI-powered vision systems and machine learning enhance the speed and accuracy of defect detection on wafers, differentiating between various types of defects for root cause analysis and yield improvement.

- Accelerated Computational Lithography: AI optimizes photomask design and optical proximity correction (OPC) processes, significantly reducing computation time and improving the accuracy of pattern transfer.

- Improved Yield Management: AI integrates data from multiple fabrication steps, including lithography, to identify correlations and optimize the overall manufacturing flow, directly contributing to higher chip yields.

- Automated Anomaly Detection: AI continuously monitors lithography equipment performance and detects subtle anomalies that may indicate potential issues, allowing for early intervention before critical failures occur.

- Adaptive Learning for New Materials and Processes: AI accelerates the development and integration of new resist materials and patterning techniques by rapidly analyzing experimental data and suggesting optimal process windows.

- Increased Automation and Robotics: AI facilitates more intelligent automation of wafer handling, loading, and unloading within the lithography cell, improving efficiency and reducing human error.

Key Takeaways Lithography Stepper Market Size & Forecast

Analyzing common user questions about the Lithography Stepper market size and forecast reveals a primary interest in understanding the fundamental drivers behind the market's robust growth, particularly the insatiable global demand for semiconductors. Users frequently inquire about the specific technologies and applications that are most significantly impacting this growth, such as advanced computing, artificial intelligence, and the rapid expansion of 5G infrastructure. There is also a keen focus on the strategic importance of Extreme Ultraviolet (EUV) lithography and its role in enabling next-generation chip manufacturing, which is seen as a cornerstone of future technological advancement.

Furthermore, stakeholders often seek insights into the geographical distribution of market growth, identifying key regions like Asia Pacific, North America, and Europe as critical investment hubs for new fabrication facilities. Users are interested in how geopolitical strategies, aimed at strengthening domestic semiconductor supply chains, are influencing capital expenditure on lithography equipment. The discussions also highlight the significant financial investments required for R&D and fab construction, underscoring the high barriers to entry and the capital-intensive nature of this industry.

In essence, the key takeaways from the market size and forecast analysis emphasize a dynamic market driven by relentless technological innovation, increasing global chip demand, and strategic governmental and corporate investments. The future of the lithography stepper market is inextricably linked to the broader semiconductor industry's trajectory, with a clear trend towards miniaturization, higher performance, and resilient supply chains, all underpinned by continuous advancements in patterning technology.

- Significant Growth Trajectory: The Lithography Stepper market is poised for substantial growth, driven by the escalating global demand for advanced semiconductors across diverse applications.

- EUV Lithography as a Game Changer: Extreme Ultraviolet (EUV) technology is a pivotal growth enabler, allowing for the fabrication of smaller, more powerful, and energy-efficient chips essential for future computing.

- Strategic Global Investments: Major investments in new fabrication plants and capacity expansions globally, particularly in key semiconductor manufacturing regions, are propelling equipment demand.

- Miniaturization and Performance Imperative: The continuous push for higher transistor density and improved chip performance necessitates advanced lithography solutions capable of ever-finer patterning.

- Resilience in Supply Chains: Geopolitical efforts to secure and regionalize semiconductor supply chains are encouraging diversified investments in lithography equipment across multiple geographies.

- High Capital Intensity: The market remains highly capital-intensive, with significant R&D expenditures and substantial investment requirements for state-of-the-art lithography systems.

Lithography Stepper Market Drivers Analysis

The Lithography Stepper market is propelled by a confluence of powerful drivers stemming from the global demand for advanced electronics and strategic industry shifts. At its core, the insatiable appetite for semiconductors, fueled by the proliferation of smart devices, artificial intelligence, 5G technology, and high-performance computing, directly translates into an escalating need for sophisticated lithography equipment. As these applications demand increasingly powerful, compact, and energy-efficient chips, manufacturers are compelled to invest in cutting-edge lithography solutions capable of producing features at nanometer scales.

Furthermore, the ongoing race for technological leadership in the semiconductor industry drives continuous innovation in lithography. The transition to advanced nodes (7nm, 5nm, 3nm, and beyond) necessitates the adoption of highly advanced lithography techniques, most notably Extreme Ultraviolet (EUV) lithography, and the development of next-generation patterning capabilities. This technological imperative compels semiconductor foundries and Integrated Device Manufacturers (IDMs) to upgrade their fabrication facilities with the latest stepper technology to remain competitive and meet future market demands. Government initiatives and subsidies in various regions, aimed at bolstering domestic semiconductor manufacturing capabilities and reducing reliance on foreign supply chains, also act as significant drivers, encouraging substantial capital investments in new fabs and equipment.

The expansion of new application areas such as automotive electronics, industrial IoT, and specialized AI hardware further contributes to market growth. These sectors require robust, reliable, and often custom-designed chips, stimulating demand for flexible and high-volume lithography solutions. Additionally, advancements in advanced packaging technologies, which allow for the integration of multiple chips into a single package, create a parallel demand for lithography tools capable of precise alignment and patterning on various substrates, broadening the application scope for lithography steppers beyond traditional wafer processing.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Surging Global Demand for Semiconductors | +1.5% | Global, particularly Asia Pacific (China, Taiwan, South Korea), North America, Europe | Long-term (2025-2033) |

| Advancements in Chip Miniaturization & Node Shrink | +1.2% | Global, especially leading-edge foundries | Mid-term to Long-term (2025-2033) |

| Rising Adoption of AI, 5G, & IoT Technologies | +1.0% | Global, across all major economies | Mid-term (2025-2030) |

| Increased Investments in New Fabrication Plants (Fabs) | +0.8% | Asia Pacific (Taiwan, South Korea, Japan), North America (USA), Europe | Short-term to Mid-term (2025-2029) |

| Government Initiatives & Subsidies for Domestic Manufacturing | +0.7% | USA, EU, Japan, China, India | Mid-term to Long-term (2025-2033) |

Lithography Stepper Market Restraints Analysis

Despite its robust growth potential, the Lithography Stepper market faces several significant restraints that could impede its expansion. One of the primary limiting factors is the exceedingly high capital expenditure required for developing, manufacturing, and deploying advanced lithography systems, particularly EUV steppers. These machines cost hundreds of millions of dollars each, making them accessible only to a handful of the largest semiconductor manufacturers and creating substantial financial barriers to entry for new players or smaller companies looking to upgrade their production capabilities. The enormous R&D costs associated with pushing the boundaries of physics for finer patterning also contribute to the high price tags and long development cycles.

Furthermore, the extreme technological complexity inherent in lithography stepper design and operation presents a significant challenge. The precision required for patterning features at atomic scales demands highly specialized expertise, materials, and manufacturing processes, which are difficult to acquire and maintain. This complexity also leads to protracted development times and a limited number of suppliers capable of producing such sophisticated equipment, creating a bottleneck in the supply chain. Geopolitical tensions and trade restrictions, particularly concerning advanced technology transfers, can further disrupt market dynamics by limiting access to critical components or markets, impacting global supply chain stability and investment decisions.

The inherent risk of technology obsolescence also acts as a restraint. As semiconductor technology evolves rapidly, existing lithography steppers can quickly become outdated, necessitating continuous, costly upgrades or replacements. This high rate of technological change requires substantial, ongoing investment from manufacturers to keep pace with demand for next-generation chips. Additionally, the increasing environmental scrutiny and regulatory pressures related to energy consumption and chemical usage in semiconductor manufacturing pose operational challenges, potentially leading to higher compliance costs and limitations on expansion without adopting more sustainable, albeit often more expensive, practices.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Capital & R&D Costs | -0.8% | Global, impacts smaller players disproportionately | Long-term (2025-2033) |

| Extreme Technological Complexity & Manufacturing Precision | -0.7% | Global, primarily affecting equipment manufacturers | Long-term (2025-2033) |

| Geopolitical Tensions & Export Controls | -0.6% | Global, particularly US-China, Europe-Asia trade routes | Mid-term (2025-2030) |

| Supply Chain Vulnerabilities & Raw Material Scarcity | -0.5% | Global, affects all regions reliant on key suppliers | Short-term to Mid-term (2025-2028) |

| Skilled Labor Shortage | -0.4% | Global, particularly in advanced manufacturing hubs | Long-term (2025-2033) |

Lithography Stepper Market Opportunities Analysis

The Lithography Stepper market is ripe with opportunities driven by emerging technologies, new application frontiers, and strategic market dynamics. A significant opportunity lies in the continued advancements and broader adoption of Extreme Ultraviolet (EUV) lithography and the development of High-NA EUV systems. As chip designs push towards 2nm and beyond, the demand for these cutting-edge tools will intensify, creating a lucrative segment for the few manufacturers capable of producing them. This technological leap allows for unprecedented miniaturization, unlocking new possibilities for semiconductor performance and density in critical applications such as advanced AI processors and quantum computing components.

Furthermore, the expansion into new vertical markets presents considerable opportunities. Beyond traditional consumer electronics, the increasing integration of semiconductors into automotive systems (e.g., autonomous driving, electric vehicles), healthcare devices (e.g., advanced diagnostics, wearables), and industrial automation (e.g., smart factories, IoT sensors) creates diverse demand for a wide range of chip types, from high-performance to power-efficient, each requiring specialized lithography solutions. This diversification of end-use sectors helps to stabilize demand and reduce reliance on any single market segment. The growing emphasis on advanced packaging technologies, such as 3D stacking and chiplets, also opens new avenues for lithography equipment tailored for heterogeneous integration, enabling higher levels of functionality and performance beyond traditional monolithic scaling.

Strategic partnerships, collaborations, and mergers within the industry offer another significant opportunity. Given the immense cost and complexity of lithography R&D, alliances between equipment manufacturers, material suppliers, and semiconductor foundries can accelerate innovation, share financial burdens, and streamline development cycles for next-generation solutions. Additionally, the development of more sustainable and energy-efficient lithography processes, driven by environmental concerns and rising energy costs, presents an opportunity for manufacturers to differentiate their offerings and appeal to environmentally conscious clients. Lastly, the potential for expanding into emerging semiconductor manufacturing regions, supported by government incentives to build local supply chain resilience, provides new geographical markets for lithography stepper deployment.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development & Commercialization of High-NA EUV Lithography | +1.3% | Global, focused on leading-edge foundries (Taiwan, South Korea, US) | Long-term (2028-2033) |

| Emergence of New Application Areas (Quantum Computing, Advanced Automotive) | +1.1% | Global, driven by technological innovation hubs | Mid-term to Long-term (2027-2033) |

| Strategic Partnerships & Collaborative R&D | +0.9% | Global, especially among key industry players | Mid-term (2025-2030) |

| Expansion into Emerging Semiconductor Manufacturing Regions | +0.7% | India, Southeast Asia, parts of Europe | Mid-term to Long-term (2026-2033) |

| Focus on Sustainable & Energy-Efficient Lithography Solutions | +0.6% | Global, driven by regulatory and ESG pressures | Mid-term (2025-2030) |

Lithography Stepper Market Challenges Impact Analysis

The Lithography Stepper market, while experiencing significant growth, is not without its share of formidable challenges that could impact its future trajectory. One of the most pressing issues is the intense and escalating demand for continuous technological innovation. The industry's relentless pursuit of smaller feature sizes and higher performance chips means that current lithography technologies quickly approach their physical limits, requiring massive, sustained investment in R&D to develop next-generation solutions. This constant innovation cycle places immense financial and technical pressure on equipment manufacturers, demanding breakthroughs in optics, light sources, and materials science that are incredibly complex and capital-intensive to achieve.

Another critical challenge is the inherent complexity and fragility of the global supply chain for lithography equipment. Producing a single advanced lithography stepper involves a vast network of highly specialized suppliers providing precision components, from optics and lasers to robotics and vacuum systems. Disruptions due to geopolitical tensions, natural disasters, or pandemics can severely impact production timelines and escalate costs, leading to delays in fab construction and chip manufacturing. This vulnerability underscores the need for greater supply chain resilience, which itself is a complex and costly endeavor.

Furthermore, the scarcity of highly skilled talent poses a significant impediment. Designing, manufacturing, operating, and maintaining these highly sophisticated lithography systems requires a specialized workforce with expertise in fields such as optics, quantum physics, materials science, and advanced engineering. There is a growing global shortage of such talent, which could constrain the industry's ability to innovate, expand production, and service installed equipment. Finally, the increasingly stringent regulatory landscape, particularly concerning environmental protection and safety standards for the use of hazardous materials and high-energy systems, adds a layer of operational complexity and compliance costs, which can further challenge profitability and operational efficiency.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Escalating R&D Intensity & Technological Hurdles | -0.7% | Global, impacts leading technology firms | Long-term (2025-2033) |

| Supply Chain Disruptions & Fragility | -0.6% | Global, impacts all regions | Short-term to Mid-term (2025-2028) |

| Shortage of Highly Skilled Workforce | -0.5% | Global, especially advanced manufacturing hubs | Long-term (2025-2033) |

| Environmental & Regulatory Compliance Costs | -0.4% | Global, particularly developed economies (EU, US) | Mid-term (2025-2030) |

| High Energy Consumption & Operational Costs | -0.3% | Global, affects profitability of fabs | Long-term (2025-2033) |

Lithography Stepper Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the Lithography Stepper Market, offering a detailed overview of its size, trends, drivers, restraints, opportunities, and challenges across various segments and key regions. The report leverages extensive primary and secondary research to deliver actionable insights into market dynamics, competitive landscape, and future growth prospects, aiding stakeholders in making informed strategic decisions within the evolving semiconductor industry.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 18.5 Billion |

| Market Forecast in 2033 | USD 36.7 Billion |

| Growth Rate | 9.2% CAGR |

| Number of Pages | 247 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | ASML, Nikon, Canon, JEOL, KLA Corporation, Applied Materials Inc., Tokyo Electron Limited (TEL), Screen Holdings Co. Ltd., Carl Zeiss AG, Topcon Corporation, EV Group (EVG), SUSS MicroTec SE, Veeco Instruments Inc., Ultratech (acquired by Veeco), Orbotech (now KLA), Toppan Photomask Co. Ltd., Dai Nippon Printing Co. Ltd., Merck KGaA, JSR Corporation, DuPont |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Lithography Stepper market is meticulously segmented to provide a granular understanding of its diverse components and their respective contributions to overall market dynamics. This segmentation facilitates a deeper analysis of specific technological advancements, application areas, and end-user demands, enabling stakeholders to identify niche opportunities and tailor strategic approaches. The market is primarily categorized by type of lithography technology, reflecting the various methods employed for patterning semiconductor wafers, each with unique capabilities and cost structures.

Further segmentation by application highlights the key industries and manufacturing processes that utilize lithography steppers, ranging from high-volume memory production to advanced logic chip fabrication and emerging packaging techniques. This application-based view offers insights into where the most significant demand originates and how different technologies are being deployed. Finally, the market is segmented by end-user industries, revealing the ultimate consumers of semiconductor devices and the underlying drivers for chip demand across sectors like consumer electronics, automotive, and telecommunications. This multi-dimensional segmentation provides a comprehensive framework for assessing market trends, competitive landscapes, and future growth prospects across the lithography stepper ecosystem.

- By Type:

- Deep Ultraviolet (DUV) Lithography Stepper: Still widely used for mature nodes and certain advanced applications, including KrF and ArF immersion systems.

- Extreme Ultraviolet (EUV) Lithography Stepper: Essential for leading-edge nodes (7nm and below), offering superior resolution.

- X-ray Lithography Stepper: Niche applications, particularly for very fine features where electron beam or EUV are not suitable due to cost or throughput.

- E-beam Lithography Stepper: Primarily for R&D, mask making, and very low-volume, high-resolution prototyping due to its slow throughput.

- Nanoimprint Lithography (NIL) Stepper: Emerging technology for cost-effective patterning, especially for non-critical layers or specialized devices.

- By Application:

- Memory Manufacturing: Includes DRAM (Dynamic Random-Access Memory) and NAND flash memory production, which are high-volume applications requiring efficient lithography.

- Foundry: Fabrication of logic chips, microprocessors, and other complex integrated circuits for various fabless companies. This is a highly demanding segment for advanced lithography.

- Integrated Device Manufacturers (IDMs): Companies that design, manufacture, and sell their own semiconductors, requiring a broad range of lithography capabilities.

- Advanced Packaging: Lithography solutions for techniques like 3D stacking, fan-out wafer-level packaging (FOWLP), and chiplet integration, enabling heterogeneous integration.

- MEMS (Micro-Electro-Mechanical Systems): Used for sensors, actuators, and other miniature devices, often requiring specialized patterning.

- Optoelectronics: Applications in optical devices, LEDs, and photonics, which may have different lithography requirements compared to logic chips.

- By End-User:

- Consumer Electronics: Smartphones, laptops, tablets, smart wearables, and home appliances.

- Automotive: Autonomous driving systems, infotainment, safety features, and electric vehicle components.

- Healthcare: Medical imaging, diagnostics, wearable health monitors, and lab-on-a-chip devices.

- Industrial: Industrial automation, robotics, IoT devices, and power management systems.

- Telecommunications: 5G infrastructure, network equipment, and high-speed communication devices.

- Data Centers: Servers, storage solutions, and networking hardware for cloud computing and data processing.

- Aerospace & Defense: High-reliability components for avionics, satellites, and military applications.

Regional Highlights

- Asia Pacific (APAC):

- Dominant market share due to the presence of major semiconductor manufacturing hubs in Taiwan (TSMC), South Korea (Samsung, SK Hynix), Japan (Sony, Kioxia), and China.

- Significant ongoing investments in new fab construction and capacity expansion, particularly driven by government incentives in China and strategic expansions in Taiwan and South Korea.

- High demand from a burgeoning consumer electronics sector and a strong focus on advanced logic and memory production.

- North America:

- Key region for R&D and innovation in lithography technology, with strong emphasis on advanced node development and next-generation patterning solutions.

- Increasing investments in domestic semiconductor manufacturing capabilities driven by government initiatives (e.g., CHIPS Act in the US) to enhance supply chain resilience.

- Home to leading-edge chip design companies and a growing demand for high-performance computing (HPC) and AI processors.

- Europe:

- Strong presence in niche lithography technologies and advanced materials development, particularly for optics and EUV components.

- Government initiatives like the European Chips Act aim to boost regional semiconductor production, creating opportunities for lithography equipment deployment.

- Significant R&D investments in collaborations between academia, research institutes, and industry players for future lithography advancements.

- Latin America:

- Emerging market with nascent semiconductor manufacturing capabilities, primarily focusing on assembly, testing, and packaging (ATP) operations.

- Potential for future growth as global supply chains diversify and regional governments seek to establish more integrated semiconductor ecosystems.

- Middle East and Africa (MEA):

- Currently a smaller market for lithography steppers, with limited wafer fabrication facilities.

- Growing interest in developing technology sectors and diversifying economies could lead to future investments in semiconductor manufacturing infrastructure.

- Potential for specialized applications in areas like IoT and industrial electronics in the long term.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Lithography Stepper Market.- ASML

- Nikon

- Canon

- JEOL

- KLA Corporation

- Applied Materials Inc.

- Tokyo Electron Limited (TEL)

- Screen Holdings Co. Ltd.

- Carl Zeiss AG

- Topcon Corporation

- EV Group (EVG)

- SUSS MicroTec SE

- Veeco Instruments Inc.

- Ultratech (acquired by Veeco)

- Orbotech (now KLA)

- Toppan Photomask Co. Ltd.

- Dai Nippon Printing Co. Ltd.

- Merck KGaA

- JSR Corporation

- DuPont

Frequently Asked Questions

Analyze common user questions about the Lithography Stepper market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is a lithography stepper and why is it crucial for chip manufacturing?

A lithography stepper is a highly precise machine used in semiconductor fabrication to create patterns on a silicon wafer. It projects a circuit design (from a photomask) onto a photosensitive material (resist) on the wafer, similar to how a camera projects an image. It is crucial because it enables the miniaturization and mass production of integrated circuits, forming the foundational step for all modern electronics.

What is the difference between DUV and EUV lithography?

DUV (Deep Ultraviolet) lithography uses a longer wavelength light source (typically 193nm) and is suitable for manufacturing chips at 28nm nodes and larger, or for multi-patterning techniques for smaller nodes. EUV (Extreme Ultraviolet) lithography uses a much shorter wavelength (13.5nm), enabling the creation of much finer patterns and is essential for producing advanced chips at 7nm nodes and below with fewer patterning steps.

What factors are driving the growth of the Lithography Stepper market?

Key drivers include the soaring global demand for semiconductors across various industries (AI, 5G, IoT), the continuous push for chip miniaturization and higher performance, significant investments in new fabrication facilities (fabs) globally, and government initiatives aimed at bolstering domestic semiconductor manufacturing capabilities.

How does AI impact the lithography stepper industry?

AI significantly impacts the industry by enhancing process optimization for improved pattern fidelity, enabling predictive maintenance for reduced downtime, boosting the accuracy of defect detection, and accelerating computational lithography processes. AI also helps in overall yield management and automated anomaly detection in complex fabrication steps.

Which regions are leading in the Lithography Stepper market?

Asia Pacific holds the largest market share due to the presence of major semiconductor manufacturing hubs in Taiwan, South Korea, Japan, and China. North America is a key region for R&D and innovation, while Europe is strengthening its position with initiatives to boost regional semiconductor production.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted