Extreme Ultraviolet Lithography System Market

Extreme Ultraviolet Lithography System Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_701139 | Last Updated : July 29, 2025 |

Format : ![]()

![]()

![]()

![]()

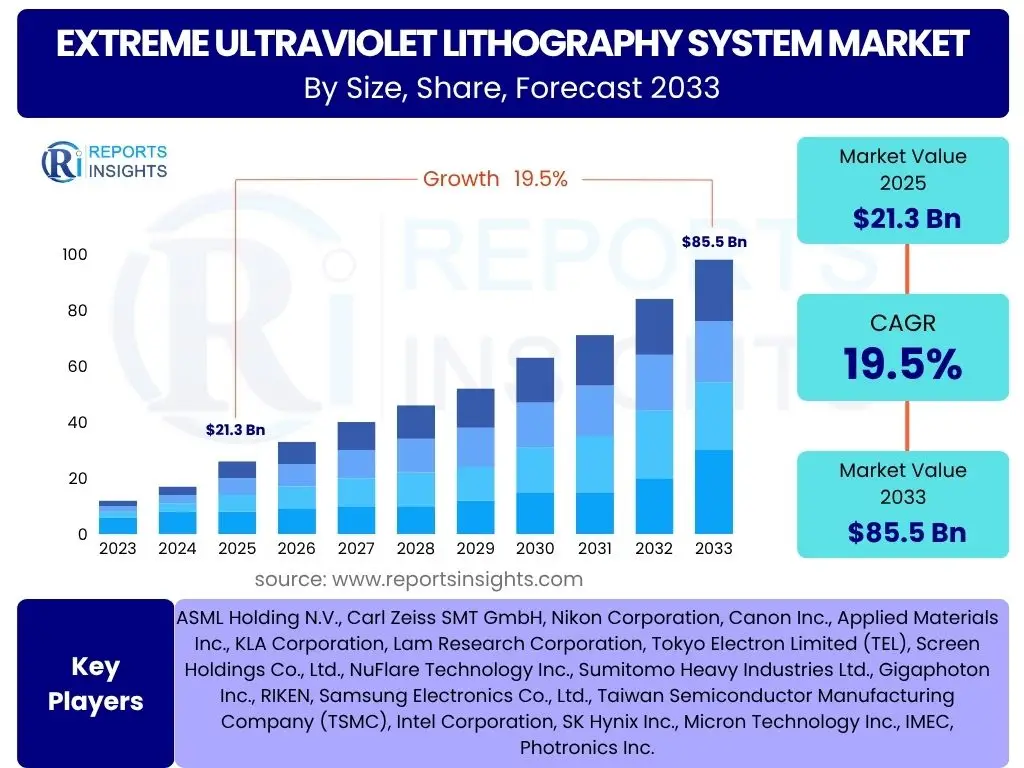

Extreme Ultraviolet Lithography System Market Size

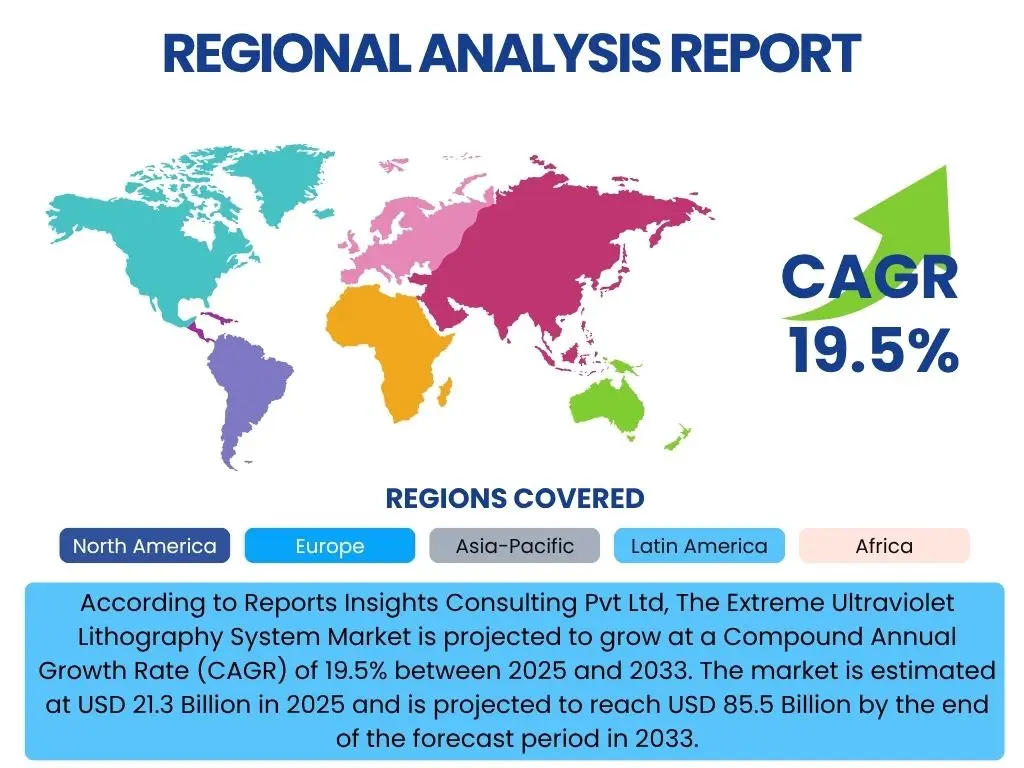

According to Reports Insights Consulting Pvt Ltd, The Extreme Ultraviolet Lithography System Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 19.5% between 2025 and 2033. The market is estimated at USD 21.3 Billion in 2025 and is projected to reach USD 85.5 Billion by the end of the forecast period in 2033.

Key Extreme Ultraviolet Lithography System Market Trends & Insights

The Extreme Ultraviolet (EUV) Lithography System market is profoundly influenced by the relentless demand for higher transistor density and improved chip performance, driving the semiconductor industry towards advanced node manufacturing. A primary trend is the accelerating adoption of EUV technology for producing logic chips at 7nm, 5nm, and increasingly, 3nm and 2nm nodes. This necessitates continuous innovation in light sources, optical components, and patterning techniques, pushing the boundaries of what is achievable in semiconductor fabrication. The industry is also witnessing a concerted effort to enhance EUV system throughput and reliability, addressing previous concerns related to cost and operational efficiency.

Another significant trend is the development and anticipated commercialization of High-NA (High Numerical Aperture) EUV systems. This next-generation technology promises even finer resolution, essential for sub-2nm node development, although it introduces new complexities in mask design and manufacturing. Furthermore, there is a growing focus on optimizing the entire EUV ecosystem, including pellicles, resist materials, and metrology solutions, to improve yield and reduce overall production costs. Geopolitical considerations and the pursuit of supply chain resilience are also shaping market trends, driving regional investments in advanced manufacturing capabilities and fostering collaboration within the semiconductor value chain.

- Accelerated adoption for advanced logic and memory nodes (7nm, 5nm, 3nm).

- Development and impending commercialization of High-NA EUV systems.

- Increased focus on improving EUV system throughput and operational reliability.

- Enhanced R&D in EUV resist materials, pellicles, and metrology.

- Integration of advanced process control and defect management solutions.

- Strategic investments in regional semiconductor manufacturing ecosystems.

- Emphasis on supply chain diversification and resilience.

AI Impact Analysis on Extreme Ultraviolet Lithography System

Artificial Intelligence (AI) is transforming the Extreme Ultraviolet (EUV) Lithography System market by introducing unprecedented levels of precision, efficiency, and autonomy into the complex fabrication process. Users are keenly interested in how AI can mitigate the inherent challenges of EUV, such as defectivity, yield management, and process variability. AI algorithms are increasingly deployed for advanced pattern recognition and anomaly detection, significantly improving the identification and classification of subtle defects on wafers and masks that are otherwise difficult or impossible to detect manually. This capability is critical for maintaining high yield rates in the production of highly intricate semiconductor devices.

Furthermore, AI plays a crucial role in optimizing the operational parameters of EUV scanners. Through machine learning models, parameters such as dose, focus, and illumination settings can be dynamically adjusted in real-time to compensate for process variations, leading to improved critical dimension (CD) control and overlay accuracy. Users anticipate that AI-driven predictive maintenance will revolutionize the uptime of these highly expensive and sensitive machines by anticipating equipment failures and scheduling proactive interventions. AI also accelerates the design and optimization of photomasks and optical proximity correction (OPC), reducing design cycles and enhancing manufacturability by simulating and predicting lithographic outcomes before physical fabrication. The integration of AI tools promises a paradigm shift from reactive problem-solving to proactive process optimization within the EUV domain.

- Enhanced Defect Detection and Classification: AI algorithms analyze vast datasets from inspection tools to identify and categorize microscopic defects with higher accuracy and speed, crucial for yield improvement.

- Predictive Maintenance and System Optimization: AI models predict potential equipment failures and recommend proactive maintenance, minimizing downtime and maximizing the operational efficiency of costly EUV systems.

- Automated Process Control and Recipe Generation: Machine learning optimizes lithography parameters (e.g., dose, focus, illumination) in real-time, adapting to variations and ensuring consistent patterning performance.

- Design for Manufacturability (DFM) Enhancement: AI assists in optimizing photomask designs and optical proximity correction (OPC) by simulating lithographic outcomes, reducing design iterations and improving yield.

- Accelerated R&D for New Materials: AI-driven computational chemistry and materials science accelerate the discovery and optimization of new photoresists and other materials critical for advanced EUV processes.

Key Takeaways Extreme Ultraviolet Lithography System Market Size & Forecast

The Extreme Ultraviolet (EUV) Lithography System market is poised for substantial expansion, reflecting its indispensable role in the ongoing miniaturization of semiconductor components. The market's robust Compound Annual Growth Rate (CAGR) signifies a strong global commitment to developing advanced logic and memory chips, which are the backbone of emerging technologies such as Artificial Intelligence, 5G, High-Performance Computing, and the Internet of Things. Users recognize that EUV technology is no longer an experimental frontier but a critical production tool, driving significant investments from leading semiconductor manufacturers and foundries worldwide. The forecast indicates sustained growth driven by the continuous demand for more powerful and energy-efficient electronic devices.

A significant takeaway is the market's high barrier to entry, largely due to the immense research and development costs, technical complexities, and the highly specialized supply chain involved. This results in an oligopolistic market structure dominated by a few key players who possess the requisite expertise and infrastructure. The market's future trajectory is highly dependent on continuous technological breakthroughs, particularly in enhancing throughput, improving yield, and developing next-generation EUV solutions like High-NA EUV. Furthermore, geopolitical factors and the imperative for supply chain resilience are increasingly influencing strategic decisions, prompting regional self-sufficiency initiatives in semiconductor manufacturing, thereby supporting the localized growth of the EUV ecosystem.

- Market projected for significant growth, reaching USD 85.5 Billion by 2033 with a CAGR of 19.5%.

- EUV lithography is critical for manufacturing advanced semiconductor nodes (7nm, 5nm, 3nm, 2nm).

- Demand driven by AI, 5G, HPC, IoT, and advanced consumer electronics.

- High capital expenditure and complex R&D characterize the market, creating significant entry barriers.

- Technological advancements in High-NA EUV and improved system throughput are key growth enablers.

- Geopolitical factors are influencing regional investments and supply chain strategies in EUV adoption.

- The market is dominated by a limited number of highly specialized equipment manufacturers.

Extreme Ultraviolet Lithography System Market Drivers Analysis

The Extreme Ultraviolet (EUV) Lithography System market is fundamentally propelled by the insatiable global demand for advanced semiconductors, which are the core components of modern electronic devices and cutting-edge technologies. As consumer electronics, data centers, and automotive industries increasingly require higher performance, lower power consumption, and greater functionality, the need for smaller and more complex integrated circuits becomes paramount. EUV technology is the enabler for patterning these ultra-fine features at sub-7nm nodes, which is beyond the capabilities of conventional deep ultraviolet (DUV) lithography. This pervasive requirement across numerous end-use sectors drives sustained investment in EUV systems.

Furthermore, the proliferation of disruptive technologies such as Artificial Intelligence (AI), 5G connectivity, and High-Performance Computing (HPC) significantly boosts the demand for highly sophisticated processors and memory chips. These applications demand unprecedented levels of transistor density and computational power, which can only be achieved through advanced manufacturing processes utilizing EUV lithography. Governments and private entities are also investing heavily in R&D and establishing new foundries equipped with EUV, driven by strategic national interests in semiconductor self-sufficiency and technological leadership. This confluence of technological imperative, market demand, and strategic investment forms the primary drivers for the EUV lithography system market's robust growth.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Demand for Advanced Semiconductors (Sub-7nm Nodes) | +3.5% | Global | Short-to-Mid Term (2025-2029) |

| Proliferation of AI, 5G, and IoT Technologies | +2.8% | North America, Asia Pacific, Europe | Mid-to-Long Term (2027-2033) |

| High-NA EUV Technology Development and Adoption | +2.0% | Global | Mid-to-Long Term (2028-2033) |

| Strategic Investments in Regional Semiconductor Manufacturing | +1.5% | Asia Pacific, North America, Europe | Short-to-Mid Term (2025-2029) |

Extreme Ultraviolet Lithography System Market Restraints Analysis

Despite its critical role in advanced semiconductor manufacturing, the Extreme Ultraviolet (EUV) Lithography System market faces significant restraints that can temper its growth trajectory. The most prominent restraint is the exceptionally high cost associated with EUV equipment. A single EUV scanner can cost hundreds of millions of dollars, making it a substantial capital expenditure for semiconductor manufacturers. This high upfront investment limits the number of companies that can adopt the technology, concentrating advanced manufacturing capabilities among a few industry giants and potentially slowing broader market penetration, especially for smaller or emerging players.

Another key restraint is the inherent technical complexity and sensitivity of EUV systems. The technology operates at vacuum conditions, requires highly precise optics, and utilizes a unique plasma light source, all of which demand meticulous engineering and maintenance. This complexity contributes to challenges in achieving high throughput and consistent yield rates, as even minor variations can lead to defects and costly production losses. Furthermore, the limited number of suppliers for critical components within the EUV ecosystem, particularly for light sources and optical elements, creates a bottleneck in the supply chain. Geopolitical tensions and export control regulations can further exacerbate these supply chain vulnerabilities, posing risks to the timely delivery and deployment of EUV systems globally, thereby acting as a significant market restraint.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Capital Expenditure of EUV Systems | -2.2% | Global | Short-to-Mid Term (2025-2029) |

| Technical Complexity and Yield Management Challenges | -1.8% | Global | Ongoing (2025-2033) |

| Limited Supplier Base for Critical Components | -1.5% | Global | Short-to-Mid Term (2025-2029) |

| Skilled Labor Shortage and Training Requirements | -1.0% | Global | Mid-to-Long Term (2027-2033) |

Extreme Ultraviolet Lithography System Market Opportunities Analysis

The Extreme Ultraviolet (EUV) Lithography System market is characterized by several compelling opportunities that promise to accelerate its growth and expand its applications beyond traditional logic chip manufacturing. A significant opportunity lies in the continuous push towards even smaller feature sizes, specifically the development and adoption of High-NA (High Numerical Aperture) EUV lithography. This next-generation technology offers the potential to extend Moore's Law well into the sub-2nm nodes, enabling further miniaturization and performance enhancements for future generations of microprocessors and memory chips. Investment in High-NA EUV represents a frontier for innovation and a long-term growth catalyst for the market.

Furthermore, the diversification of EUV applications presents a substantial opportunity. While historically focused on logic devices, EUV is increasingly being explored and adopted for advanced memory manufacturing, particularly for high-density NAND flash and DRAM. Beyond traditional chip types, EUV could potentially find applications in advanced packaging technologies, heterogeneous integration, and specialized photonic or quantum computing components, opening up new revenue streams and market segments. The growing emphasis on regional self-sufficiency in semiconductor manufacturing across North America, Europe, and Asia Pacific also creates opportunities for localized EUV ecosystem development and increased domestic production capacity. Collaborative R&D initiatives aimed at improving throughput, reducing defectivity, and developing more robust EUV materials (like new photoresists) also represent significant opportunities for technological advancement and market expansion, addressing key challenges and increasing the overall efficiency of EUV production.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Commercialization and Adoption of High-NA EUV Systems | +2.5% | Global | Mid-to-Long Term (2028-2033) |

| Expansion of EUV Applications Beyond Logic (e.g., Advanced Memory, Photonics) | +1.9% | Global | Mid-to-Long Term (2027-2033) |

| Strategic Investments in Regional Semiconductor Fabs | +1.7% | Asia Pacific, North America, Europe | Short-to-Mid Term (2025-2029) |

| Advancements in EUV Resist Materials and Pellicle Technology | +1.2% | Global | Ongoing (2025-2033) |

Extreme Ultraviolet Lithography System Market Challenges Impact Analysis

The Extreme Ultraviolet (EUV) Lithography System market, despite its high growth potential, grapples with several formidable challenges that necessitate continuous innovation and significant investment. One of the primary challenges is achieving consistent and high production yields, given the extreme sensitivity of EUV processes to defects. Even minuscule particles or imperfections on the photomask or wafer can lead to critical defects on the chip, resulting in costly scrap. This stringent requirement for ultra-clean environments and advanced defect inspection capabilities adds complexity and expense to the manufacturing process, impacting overall throughput and profitability for semiconductor fabs.

Another significant challenge revolves around the development and availability of a robust and mature EUV ecosystem. This includes not only the lithography tools themselves but also critical ancillary components such as high-quality photomasks (which are highly complex and expensive to produce without defects), advanced photoresist materials with improved sensitivity and resolution, and durable pellicles that protect masks from contamination. The limited number of suppliers for these specialized components creates potential bottlenecks and elevates supply chain risks. Furthermore, the immense power consumption of EUV systems and the disposal of associated waste present environmental and operational challenges that require sustainable solutions. Overcoming these technical and supply chain hurdles is crucial for the widespread and cost-effective adoption of EUV technology.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Maintaining High Yields and Defect Control | -1.8% | Global | Ongoing (2025-2033) |

| Development and Availability of EUV Mask Infrastructure | -1.5% | Global | Short-to-Mid Term (2025-2029) |

| EUV Resist Material Performance and Sensitivity | -1.2% | Global | Ongoing (2025-2033) |

| High Power Consumption and Operational Costs | -0.8% | Global | Long Term (2030-2033) |

Extreme Ultraviolet Lithography System Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the Extreme Ultraviolet (EUV) Lithography System market, covering historical data, current market dynamics, and future growth projections. It meticulously details market size and forecast, key trends, drivers, restraints, opportunities, and challenges influencing the industry landscape from 2019 to 2033. The report offers detailed segmentation analysis by various factors, including components, applications, and end-use industries, alongside a thorough regional assessment. Furthermore, it profiles key market players, providing insights into their strategies, product portfolios, and competitive positioning within the global EUV lithography ecosystem.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 21.3 Billion |

| Market Forecast in 2033 | USD 85.5 Billion |

| Growth Rate | 19.5% |

| Number of Pages | 247 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | ASML Holding N.V., Carl Zeiss SMT GmbH, Nikon Corporation, Canon Inc., Applied Materials Inc., KLA Corporation, Lam Research Corporation, Tokyo Electron Limited (TEL), Screen Holdings Co., Ltd., NuFlare Technology Inc., Sumitomo Heavy Industries Ltd., Gigaphoton Inc., RIKEN, Samsung Electronics Co., Ltd., Taiwan Semiconductor Manufacturing Company (TSMC), Intel Corporation, SK Hynix Inc., Micron Technology Inc., IMEC, Photronics Inc. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Extreme Ultraviolet (EUV) Lithography System market is meticulously segmented to provide a granular understanding of its complex structure and diverse growth drivers. This segmentation is crucial for identifying specific market dynamics, technological advancements, and strategic opportunities across various dimensions. The market is primarily analyzed by component, shedding light on the critical elements that constitute an EUV system and their individual contributions to the overall value chain. This includes the high-power light source, ultra-precision optics, highly sophisticated masks and pellicles, and advanced wafer stages, among other supporting technologies.

Beyond components, the market is segmented by application, differentiating between logic manufacturing and memory manufacturing (DRAM, NAND), which represent the core areas where EUV technology is deployed. Further application segmentation includes foundry services versus Integrated Device Manufacturers (IDMs), illustrating the diverse business models leveraging EUV. This distinction highlights the market's dependence on both dedicated chip manufacturers and companies that design and produce their own semiconductors. Each application segment has unique requirements and adoption rates for EUV, influenced by factors like product roadmap, capital investment capacity, and strategic partnerships.

Finally, the market is categorized by end-use industry, providing insights into the ultimate demand drivers for EUV-enabled chips. This covers a broad spectrum including consumer electronics, automotive, data centers, AI & machine learning, healthcare, aerospace & defense, and telecommunications. Understanding these end-use segments helps to project future demand for advanced semiconductors and, consequently, for EUV lithography systems. The intricate interplay between these segments defines the competitive landscape and offers a comprehensive view of the market's current state and future potential, guiding strategic decisions for all stakeholders.

- By Component:

- Light Source

- Optics

- Masks & Pellicles

- Wafer Stage

- Others (e.g., Metrology, Software)

- By Application:

- Logic Manufacturing

- Memory Manufacturing (DRAM, NAND)

- Foundry Services

- Integrated Device Manufacturers (IDMs)

- By End-Use Industry:

- Consumer Electronics

- Automotive

- Data Centers

- AI & Machine Learning

- Healthcare & Medical Devices

- Aerospace & Defense

- Telecommunications

Regional Highlights

- North America: A significant hub for semiconductor design, research and development, and advanced manufacturing. The region benefits from substantial investments by leading technology companies and government initiatives aimed at strengthening domestic semiconductor capabilities. The presence of major foundries and IDMs, alongside strong innovation ecosystems, drives high demand for EUV systems.

- Europe: Home to key EUV equipment manufacturers and critical component suppliers. The region plays a pivotal role in the global EUV supply chain, particularly in optics and light source technology. European research institutions and collaborative projects contribute significantly to advancements in lithography, fostering a robust R&D environment.

- Asia Pacific (APAC): The dominant region in semiconductor manufacturing, led by Taiwan, South Korea, China, and Japan. This region accounts for the largest share of EUV system installations due to the presence of major foundries and memory manufacturers. Rapid expansion of fabrication capacity and strategic national investments in advanced nodes ensure continued leadership in EUV adoption and production.

- Latin America, Middle East, and Africa (MEA): While currently smaller in terms of EUV adoption, these regions are emerging as potential growth areas driven by increasing digitalization, infrastructure development, and nascent semiconductor initiatives. Investments in data centers and local technology ecosystems could gradually increase demand for advanced chips, indirectly stimulating EUV adoption in the long term.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Extreme Ultraviolet Lithography System Market.- ASML Holding N.V.

- Carl Zeiss SMT GmbH

- Nikon Corporation

- Canon Inc.

- Applied Materials Inc.

- KLA Corporation

- Lam Research Corporation

- Tokyo Electron Limited (TEL)

- Screen Holdings Co., Ltd.

- NuFlare Technology Inc.

- Sumitomo Heavy Industries Ltd.

- Gigaphoton Inc.

- RIKEN

- Samsung Electronics Co., Ltd.

- Taiwan Semiconductor Manufacturing Company (TSMC)

- Intel Corporation

- SK Hynix Inc.

- Micron Technology Inc.

- IMEC

- Photronics Inc.

Frequently Asked Questions

Analyze common user questions about the Extreme Ultraviolet Lithography System market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is the projected market size and growth rate for the Extreme Ultraviolet Lithography System market?

The Extreme Ultraviolet Lithography System market is projected to reach USD 85.5 Billion by 2033, growing at a Compound Annual Growth Rate (CAGR) of 19.5% from USD 21.3 Billion in 2025.

What are the primary applications of EUV technology in the semiconductor industry?

EUV technology is primarily used for manufacturing advanced logic chips (at 7nm, 5nm, 3nm, and 2nm nodes) and high-density memory chips (DRAM, NAND flash), enabling higher performance and greater transistor density in modern electronic devices.

Who are the leading companies providing Extreme Ultraviolet Lithography Systems and related components?

Key players include equipment manufacturers like ASML Holding N.V., optics specialists such as Carl Zeiss SMT GmbH, and other critical suppliers in the EUV ecosystem, alongside major semiconductor manufacturers adopting the technology.

What are the main challenges faced by the Extreme Ultraviolet Lithography System market?

Key challenges include the exceptionally high capital cost of EUV systems, the technical complexity of achieving high yield and defect control, the limited supplier base for critical components (like masks and resists), and high operational power consumption.

How is Artificial Intelligence (AI) impacting the Extreme Ultraviolet Lithography market?

AI is significantly impacting EUV by enhancing defect detection, optimizing process control for improved yield, enabling predictive maintenance for system uptime, and accelerating the design and manufacturing of complex photomasks.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted