Lithium Ion Battery Separator Material Market

Lithium Ion Battery Separator Material Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_709430 | Last Updated : December 09, 2025 |

Format : ![]()

![]()

![]()

![]()

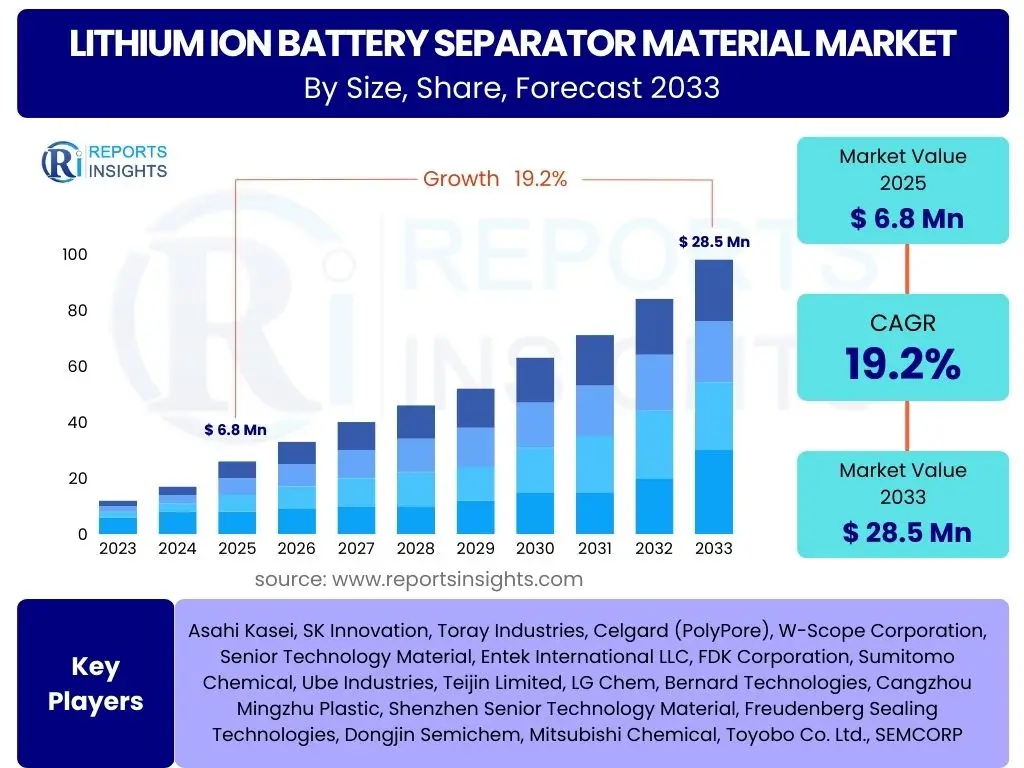

Lithium Ion Battery Separator Material Market Size

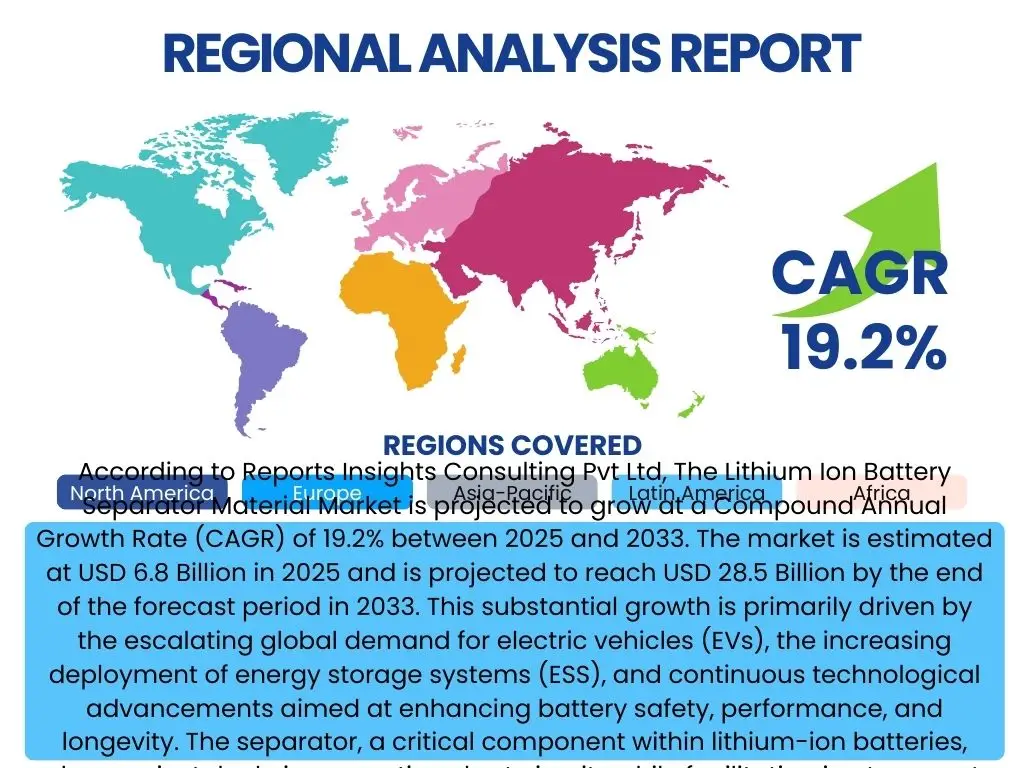

According to Reports Insights Consulting Pvt Ltd, The Lithium Ion Battery Separator Material Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 19.2% between 2025 and 2033. The market is estimated at USD 6.8 Billion in 2025 and is projected to reach USD 28.5 Billion by the end of the forecast period in 2033. This substantial growth is primarily driven by the escalating global demand for electric vehicles (EVs), the increasing deployment of energy storage systems (ESS), and continuous technological advancements aimed at enhancing battery safety, performance, and longevity. The separator, a critical component within lithium-ion batteries, plays a pivotal role in preventing short circuits while facilitating ion transport, making its material and design paramount for battery efficiency and safety.

Key Lithium Ion Battery Separator Material Market Trends & Insights

User queries regarding the Lithium Ion Battery Separator Material market frequently focus on technological advancements, material innovation, and the evolving demands from end-use sectors. Key insights reveal a strong emphasis on enhancing safety, increasing energy density, and reducing overall battery costs, which are collectively shaping the research and development landscape for separator materials. There is a noticeable shift towards advanced coating technologies and novel material compositions designed to withstand higher temperatures and reduce the risk of thermal runaway, a critical concern in high-performance battery applications such as electric vehicles. Furthermore, the drive for thinner, more uniform, and mechanically stronger separators is intensifying to enable compact battery designs and improve gravimetric energy density.

Another prominent trend observed is the growing interest in sustainable and environmentally friendly manufacturing processes for separator materials. As the global focus on carbon neutrality and circular economy principles expands, manufacturers are exploring bio-based materials and improved recycling methods for battery components, including separators. This also encompasses efforts to optimize supply chains and reduce the environmental footprint associated with material extraction and processing. These trends collectively underscore a dynamic market that is continuously innovating to meet stringent performance requirements and evolving regulatory standards across various applications.

- Development of ceramic-coated separators for enhanced thermal stability and safety.

- Increasing adoption of ultra-thin separators to boost energy density.

- Focus on sustainable and recyclable separator materials and manufacturing processes.

- Integration of advanced functional layers for improved electrolyte wettability and ion conductivity.

- Shift towards dry processing methods for reduced environmental impact and cost efficiency.

- Growing research into solid-state battery compatible separator technologies.

AI Impact Analysis on Lithium Ion Battery Separator Material

Common user questions regarding AI's impact on the Lithium Ion Battery Separator Material domain revolve around its potential to revolutionize material discovery, optimize manufacturing processes, and enhance quality control. Users are keen to understand how artificial intelligence and machine learning algorithms can accelerate the development of novel separator materials with superior properties, reducing the traditionally long R&D cycles. There is significant interest in AI's role in predicting material performance under various operational conditions, thereby guiding experimental design and material selection more efficiently. This includes the use of AI for simulating atomic and molecular interactions to identify promising new polymer blends or coating formulations that could lead to breakthroughs in safety and performance.

Beyond material innovation, AI is also expected to significantly impact the production efficiency and quality assurance of separator manufacturing. Users anticipate AI-driven systems to monitor and control complex manufacturing parameters in real-time, leading to reduced defects, improved yield rates, and enhanced product consistency. Predictive maintenance applications for manufacturing equipment, enabled by AI, are also a key area of interest, as they can minimize downtime and operational costs. Furthermore, AI's capability to analyze vast datasets from testing and operational feedback can provide invaluable insights for continuous product improvement and adaptation to market demands, ultimately fostering a more agile and responsive separator material industry.

- Accelerated discovery and design of novel separator materials through machine learning.

- Optimization of manufacturing parameters for improved yield, consistency, and reduced waste.

- Enhanced quality control and defect detection during production using AI-powered vision systems.

- Predictive analytics for material performance and degradation under various operating conditions.

- Supply chain optimization and demand forecasting for raw materials using AI algorithms.

- Development of digital twins for simulating and testing new separator designs virtually.

Key Takeaways Lithium Ion Battery Separator Material Market Size & Forecast

User inquiries about key takeaways from the Lithium Ion Battery Separator Material market size and forecast often center on identifying the primary growth drivers, understanding market opportunities, and recognizing critical challenges that could influence future market trajectory. A crucial insight is the undeniable dominance of the electric vehicle sector as the preeminent catalyst for market expansion, dictating both the volume and performance requirements for separators. The forecast indicates sustained robust growth, propelled by global decarbonization efforts and supportive government policies promoting EV adoption and renewable energy integration. Stakeholders should recognize the imperative for continuous innovation in separator technology to meet evolving demands for enhanced safety, extended range, and faster charging capabilities in advanced battery applications.

Furthermore, the market's future health is intrinsically linked to advancements in energy storage systems (ESS), which are seeing increasing deployment in grid-scale and residential applications. These applications demand long-duration, high-cycle-life batteries, placing unique demands on separator materials for durability and reliability. The geographic distribution of manufacturing capabilities and the stability of raw material supply chains will also play significant roles in shaping regional market dynamics and competitive landscapes. Investors and market participants should particularly focus on regions with high EV manufacturing capacity and strong government support for battery innovation, as these areas are poised for substantial market expansion.

- Electric Vehicle (EV) adoption remains the primary growth engine for the separator market.

- Technological advancements in separator coatings and materials are crucial for meeting higher battery performance and safety standards.

- Asia Pacific will maintain its leadership in both production and consumption, driven by extensive battery manufacturing infrastructure.

- The energy storage systems (ESS) segment presents a significant, rapidly expanding application area.

- Sustainability and recycling initiatives are emerging as key competitive differentiators.

Lithium Ion Battery Separator Material Market Drivers Analysis

The Lithium Ion Battery Separator Material market is profoundly influenced by several key drivers, predominantly the global surge in demand for electric vehicles (EVs). Governments worldwide are implementing stringent emission regulations and offering substantial incentives for EV adoption, directly fueling the need for high-performance lithium-ion batteries and, consequently, advanced separator materials. This demand extends beyond passenger vehicles to electric buses, trucks, and other commercial transport, all requiring robust and safe battery solutions. The continuous innovation in battery technology, aiming for higher energy density, faster charging, and extended cycle life, also drives the development and adoption of specialized separator materials that can support these enhanced performance metrics.

Additionally, the expansion of the energy storage systems (ESS) market, including grid-scale, commercial, and residential applications, significantly contributes to market growth. As renewable energy sources like solar and wind become more prevalent, the need for efficient and reliable battery storage solutions to manage intermittency and ensure grid stability becomes paramount. These ESS applications often require large-format batteries, which necessitates a consistent supply of durable and cost-effective separator materials. The rapid growth of the consumer electronics sector, particularly in emerging economies, further bolsters demand for small to medium-sized lithium-ion batteries, though its impact is less pronounced than that of EVs and ESS in terms of overall material volume.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Rapid Growth of Electric Vehicle (EV) Production | +8.5% | Global, particularly Asia Pacific, Europe, North America | Short to Long Term (2025-2033) |

| Increasing Demand for Energy Storage Systems (ESS) | +5.0% | Global, with strong growth in North America, Europe, China | Mid to Long Term (2026-2033) |

| Technological Advancements in Battery Performance & Safety | +3.5% | Global, driven by R&D hubs in Japan, Korea, Germany, USA | Short to Long Term (2025-2033) |

| Favorable Government Policies & Subsidies for EVs | +2.0% | Europe, China, USA, India | Mid Term (2025-2030) |

| Growth in Portable Consumer Electronics Market | +0.2% | Asia Pacific, North America, Europe | Short Term (2025-2027) |

Lithium Ion Battery Separator Material Market Restraints Analysis

Despite significant growth prospects, the Lithium Ion Battery Separator Material market faces several notable restraints. One primary challenge is the high manufacturing cost associated with producing advanced separator materials, particularly those involving multi-layer structures, ceramic coatings, or specialized polymers. The intricate production processes, coupled with the need for stringent quality control to ensure uniform thickness and porosity, contribute to elevated operational expenditures. This cost factor can impact the overall competitiveness of lithium-ion batteries, especially in price-sensitive applications, potentially slowing the adoption rate of higher-performance separators in certain segments. Additionally, the capital expenditure required for setting up and scaling advanced separator manufacturing facilities is substantial, posing a barrier to entry for new market players and limiting rapid expansion.

Another significant restraint is the inherent safety concerns associated with lithium-ion batteries, particularly the risk of thermal runaway. While separators are designed to mitigate this risk, any compromise in their integrity due to manufacturing defects, mechanical stress, or thermal stress can lead to severe safety incidents. The public perception of battery safety issues, often amplified by isolated incidents, can influence consumer confidence and regulatory scrutiny, potentially leading to delays in product adoption or more stringent, costly compliance requirements. Furthermore, the volatility in raw material prices, such as polyolefin resins and ceramic precursors, can introduce instability into the production costs of separators, making long-term planning and pricing strategies more complex for manufacturers. Supply chain disruptions, often due to geopolitical factors or natural disasters, can also impede the consistent availability of these critical raw materials, impacting production schedules and market supply.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Manufacturing Costs of Advanced Separators | -3.0% | Global, affecting emerging economies more | Mid to Long Term (2025-2033) |

| Safety Concerns (Thermal Runaway Risks) | -2.5% | Global, particularly in high-performance applications | Short to Mid Term (2025-2030) |

| Volatility in Raw Material Prices & Supply Chain Issues | -2.0% | Global, with regional variations in impact | Short to Mid Term (2025-2028) |

| Complex Manufacturing Processes & Quality Control | -1.5% | Global, impacting new entrants and small players | Long Term (2025-2033) |

| Intense Competition and Pricing Pressures | -1.0% | Asia Pacific, impacting established players | Short to Mid Term (2025-2029) |

Lithium Ion Battery Separator Material Market Opportunities Analysis

The Lithium Ion Battery Separator Material market is replete with significant opportunities stemming from ongoing technological innovation and the emergence of new battery chemistries. A primary opportunity lies in the development of advanced separator technologies specifically tailored for next-generation batteries, such as solid-state batteries. These batteries promise higher energy densities and enhanced safety, but require separators with entirely different properties, including high mechanical strength, excellent electrolyte compatibility (or solid electrolyte integration), and superior thermal stability. Companies that can successfully develop and commercialize such separators will gain a substantial competitive advantage as solid-state battery technology matures and enters mass production. This area represents a paradigm shift from traditional liquid electrolyte-based lithium-ion battery separators.

Another major opportunity involves the proliferation of advanced coating technologies, such as ceramic or polymer composite coatings, onto base separator films. These coatings significantly enhance separator performance by improving thermal stability, puncture resistance, and electrolyte wettability, thereby contributing to safer and more efficient batteries. The market for these coated separators is expanding rapidly, driven by the increasing demand for high-performance batteries in EVs and ESS applications. Furthermore, the growing emphasis on sustainability and circular economy principles presents opportunities for developing biodegradable or easily recyclable separator materials. Innovations in manufacturing processes that reduce energy consumption and waste also represent a significant opportunity for market players to differentiate themselves and meet evolving regulatory and consumer expectations. Expanding into new niche applications like medical devices, aerospace, and specialized industrial tools, which demand high-reliability and custom-designed battery solutions, also offers avenues for growth.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development of Separators for Solid-State Batteries | +4.5% | Global, R&D focused in Japan, Korea, Europe, USA | Long Term (2028-2033) |

| Advancements in Ceramic and Polymer Coating Technologies | +3.8% | Global, with widespread adoption in Asia Pacific and Europe | Short to Mid Term (2025-2030) |

| Focus on Sustainable and Recyclable Material Solutions | +2.5% | Europe, North America, Japan | Mid to Long Term (2027-2033) |

| Expansion into New High-Performance Battery Applications | +1.5% | Global, niche markets in North America, Europe | Mid Term (2026-2031) |

| Optimization of Manufacturing Processes for Cost Reduction | +1.0% | Global, particularly in competitive markets like China | Short to Mid Term (2025-2029) |

Lithium Ion Battery Separator Material Market Challenges Impact Analysis

The Lithium Ion Battery Separator Material market faces substantial challenges, primarily revolving around the continuous pressure to achieve both high energy density and uncompromising safety in battery design. As battery manufacturers strive for greater range and power in EVs, the demand for thinner separators to maximize active material content intensifies. However, reducing separator thickness without compromising mechanical strength, thermal stability, and puncture resistance is a formidable engineering challenge. A failure in this delicate balance can significantly increase the risk of internal short circuits and thermal runaway events, posing a critical safety hazard. Meeting these conflicting requirements often involves complex material science and manufacturing precision, which adds to development costs and time. Furthermore, the development of new electrolyte systems, which often include aggressive additives or operate at higher voltages, necessitates separator materials that can withstand harsher chemical environments without degradation, adding another layer of complexity to material selection and design.

Another significant challenge for the market is the intense competition and intellectual property landscape. The market is dominated by a few major players with extensive R&D capabilities and patented technologies. New entrants or smaller companies face considerable hurdles in developing proprietary technologies that can compete on performance and cost. The capital-intensive nature of setting up advanced manufacturing facilities also acts as a barrier, limiting diversification and market entry. Furthermore, the global supply chain for raw materials used in separator production can be susceptible to geopolitical tensions, trade disputes, or environmental regulations, leading to price volatility and supply shortages. Ensuring a stable and ethically sourced supply of high-quality materials, while simultaneously managing costs and regulatory compliance, presents a continuous operational and strategic challenge for separator manufacturers.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Balancing High Energy Density with Enhanced Safety | -3.5% | Global, critical for EV and ESS applications | Short to Long Term (2025-2033) |

| Intense Competition and Intellectual Property Rights | -2.8% | Asia Pacific, Europe, North America | Mid to Long Term (2025-2033) |

| Stringent Regulatory Compliance and Certification | -2.0% | Europe, North America, Japan, South Korea | Short to Mid Term (2025-2029) |

| Securing Stable and Cost-Effective Raw Material Supply | -1.5% | Global, affecting all manufacturing regions | Short Term (2025-2027) |

| Technological Roadblocks in Next-Generation Battery Integration | -1.0% | Global, R&D focused regions | Mid to Long Term (2028-2033) |

Lithium Ion Battery Separator Material Market - Updated Report Scope

This comprehensive market report provides an in-depth analysis of the Lithium Ion Battery Separator Material market, covering historical performance from 2019 to 2023, detailed market estimates for the base year 2024, and forward-looking projections up to 2033. It encapsulates a thorough examination of market dynamics, including key drivers, restraints, opportunities, and challenges that shape the industry landscape. The scope extends to a granular segmentation analysis across various material types, end-use applications, and regional markets, offering a holistic view of current trends and future growth avenues. The report also highlights the competitive environment by profiling leading market participants, their strategic initiatives, and market shares, providing invaluable insights for stakeholders navigating this rapidly evolving sector.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 6.8 Billion |

| Market Forecast in 2033 | USD 28.5 Billion |

| Growth Rate | 19.2% |

| Number of Pages | 245 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Asahi Kasei, SK Innovation, Toray Industries, Celgard (PolyPore), W-Scope Corporation, Senior Technology Material, Entek International LLC, FDK Corporation, Sumitomo Chemical, Ube Industries, Teijin Limited, LG Chem, Bernard Technologies, Cangzhou Mingzhu Plastic, Shenzhen Senior Technology Material, Freudenberg Sealing Technologies, Dongjin Semichem, Mitsubishi Chemical, Toyobo Co. Ltd., SEMCORP |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Lithium Ion Battery Separator Material market is extensively segmented to provide granular insights into its diverse components and applications. These segmentations are critical for understanding specific market dynamics, identifying high-growth areas, and tailoring strategic approaches. The division by material type showcases the prevalent use of polyolefin-based separators, while also highlighting the emergence of advanced ceramic-coated and nonwoven materials that offer superior performance characteristics, particularly in high-demand applications. This allows for a detailed examination of material-specific innovation and adoption trends, reflecting the continuous pursuit of enhanced safety and efficiency.

Further segmentation by end-use application distinguishes the market's reliance on various sectors, with electric vehicles and energy storage systems being the dominant forces. This categorisation helps in quantifying the demand generated by each application and understanding the specific requirements that drive separator material development for these diverse uses. Additionally, segmenting by thickness and form provides insights into manufacturing capabilities and the evolving preference for ultra-thin, multi-layer separators that contribute to higher energy density and improved battery performance. Analyzing these segments collectively offers a comprehensive picture of the market's structure and the interplay between technological advancements and application-specific demands.

- By Material:

- Polyolefin (Polypropylene (PP), Polyethylene (PE))

- Ceramic Coated Separators

- Nonwoven Separators

- Others (e.g., Composite, Polymer Blends)

- By End-use Application:

- Automotive (Electric Vehicles (EVs), Plug-in Hybrid Electric Vehicles (PHEVs))

- Consumer Electronics (Smartphones, Laptops, Tablets, Wearables)

- Energy Storage Systems (Grid-scale Storage, Residential Storage, Commercial Storage)

- Industrial (Power Tools, Forklifts, Robotics)

- Medical Devices

- By Thickness:

- Less than 10 µm

- 10-20 µm

- More than 20 µm

- By Form:

- Single Layer

- Multi-Layer (e.g., PP/PE/PP)

Regional Highlights

- Asia Pacific (APAC): This region is expected to dominate the Lithium Ion Battery Separator Material market, primarily driven by the robust presence of major battery manufacturers and the largest electric vehicle production bases, particularly in China, South Korea, and Japan. Government initiatives supporting new energy vehicles and renewable energy storage further bolster market growth.

- Europe: The European market is experiencing significant growth due to stringent emission regulations, substantial investments in EV manufacturing (Gigafactories), and ambitious renewable energy targets. Countries like Germany, France, and Scandinavia are at the forefront of battery technology adoption and R&D.

- North America: Driven by increasing EV adoption, supportive policies, and investments in domestic battery production facilities, North America is a rapidly expanding market. The United States, in particular, is witnessing substantial growth in both EV manufacturing and energy storage deployments.

- Latin America: While a smaller market, Latin America is showing emerging growth, especially in electric two-wheelers and public transport electrification in countries like Brazil and Mexico, creating nascent demand for battery separators.

- Middle East and Africa (MEA): This region is at an early stage of adoption but offers long-term potential, particularly with national strategies focused on diversifying economies, investing in renewable energy projects, and growing interest in electric mobility in key markets like the UAE and South Africa.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Lithium Ion Battery Separator Material Market.- Asahi Kasei

- SK Innovation

- Toray Industries

- Celgard (PolyPore)

- W-Scope Corporation

- Senior Technology Material

- Entek International LLC

- FDK Corporation

- Sumitomo Chemical

- Ube Industries

- Teijin Limited

- LG Chem

- Bernard Technologies

- Cangzhou Mingzhu Plastic

- Shenzhen Senior Technology Material

- Freudenberg Sealing Technologies

- Dongjin Semichem

- Mitsubishi Chemical

- Toyobo Co. Ltd.

- SEMCORP

Frequently Asked Questions

What is a lithium-ion battery separator material?

A lithium-ion battery separator material is a porous membrane positioned between the anode and cathode within a lithium-ion battery. Its primary function is to physically separate the electrodes to prevent short circuits while allowing the free flow of lithium ions through an electrolyte during charging and discharging cycles.

Why is the separator important in a Li-ion battery?

The separator is crucial for both the safety and performance of a Li-ion battery. It prevents direct electronic contact between the positive and negative electrodes, thus averting short circuits and potential thermal runaway. Concurrently, its porous structure ensures efficient ion transport, which is essential for the battery's operational efficiency, power output, and charge/discharge rates.

What are the key types of separator materials?

The key types of separator materials include polyolefin-based membranes (such as polypropylene (PP) and polyethylene (PE)), which are widely used due to their excellent mechanical properties and chemical stability. Additionally, ceramic-coated separators are gaining prominence for enhanced thermal stability and safety, while nonwoven and composite separators are also being developed for specialized applications.

Which industries primarily use Li-ion battery separators?

The primary industries utilizing Li-ion battery separators are the automotive sector, especially for electric vehicles (EVs) and hybrid electric vehicles (HEVs), and the energy storage systems (ESS) market for grid-scale, commercial, and residential applications. Other significant sectors include consumer electronics (smartphones, laptops) and various industrial and medical devices.

What are the future trends for Li-ion battery separators?

Future trends for Li-ion battery separators include the development of thinner and more mechanically robust materials, increased adoption of ceramic and functional coatings for enhanced safety and performance, and the exploration of sustainable and recyclable separator options. Significant research is also focused on developing novel separator solutions compatible with next-generation solid-state batteries.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted