Magnesite Market

Magnesite Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_709400 | Last Updated : December 08, 2025 |

Format : ![]()

![]()

![]()

![]()

Magnesite Market Size

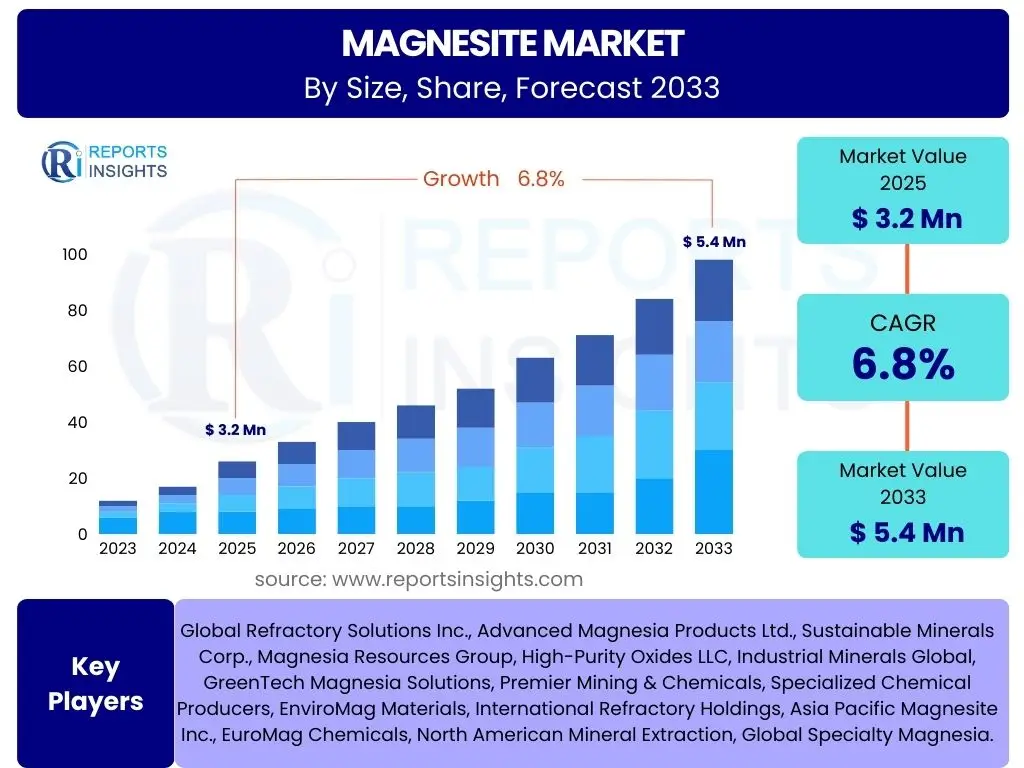

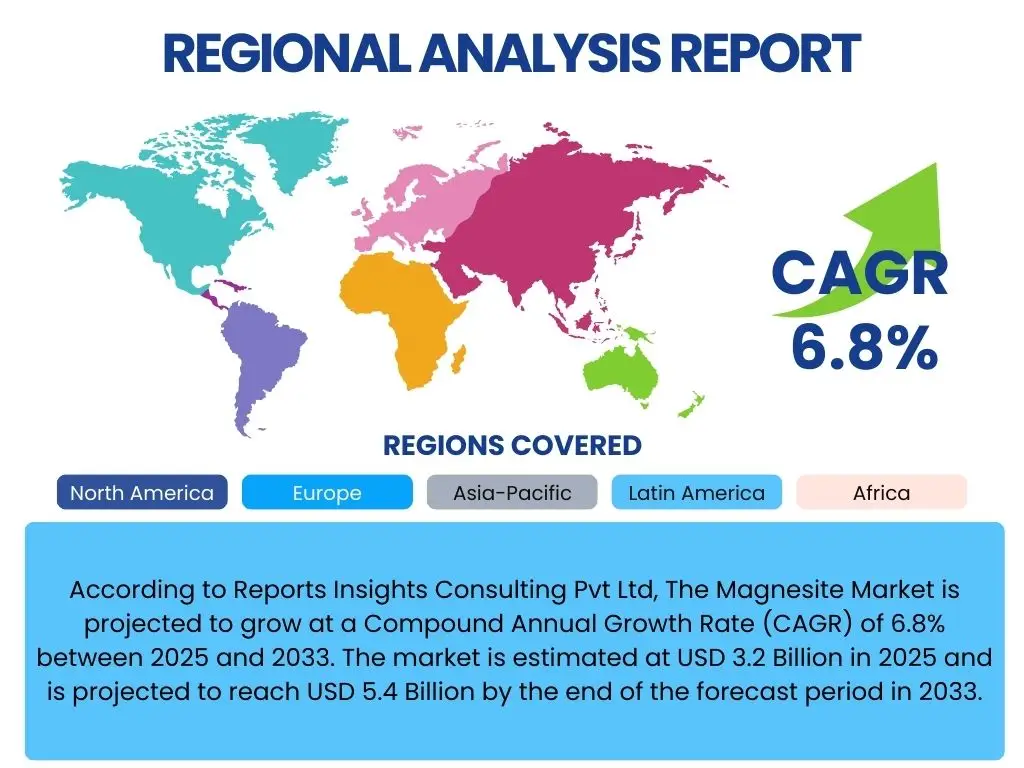

According to Reports Insights Consulting Pvt Ltd, The Magnesite Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2025 and 2033. The market is estimated at USD 3.2 Billion in 2025 and is projected to reach USD 5.4 Billion by the end of the forecast period in 2033.

Key Magnesite Market Trends & Insights

Analysis of common user inquiries reveals a strong focus on evolving industrial demands, particularly from the steel and refractory sectors, as well as the increasing adoption of magnesite in environmental applications. Users are keenly interested in how sustainability initiatives and the push for greener technologies are influencing magnesite consumption patterns. There is also significant curiosity regarding technological advancements in magnesite processing and beneficiation, which are aimed at enhancing purity and expanding application areas. The market is experiencing a shift towards higher-purity magnesia products, driven by the stringent requirements of advanced industrial processes.

Furthermore, user questions frequently highlight the impact of geopolitical factors and supply chain resilience on magnesite availability and pricing. Concerns about raw material sourcing from major producing countries and the potential for supply disruptions are prevalent. The increasing emphasis on circular economy principles is also driving interest in recycling and resource efficiency within magnesite-consuming industries, prompting innovations in material recovery and reuse. These trends collectively indicate a dynamic market influenced by both traditional industrial demands and emerging sustainability imperatives.

- Growing demand for high-purity magnesia in refractory and chemical industries.

- Increasing application in environmental protection, such as wastewater treatment and CO2 capture.

- Technological advancements in magnesite extraction and processing for enhanced quality.

- Regional shifts in production and consumption patterns, particularly in Asia Pacific.

- Emphasis on sustainable sourcing and production practices, driving interest in eco-friendly alternatives.

AI Impact Analysis on Magnesite

Common user questions regarding AI's impact on the magnesite sector revolve around optimizing mining operations, enhancing processing efficiency, and improving supply chain management. Users are exploring how predictive analytics and machine learning algorithms can be applied to forecast demand more accurately, manage inventory, and optimize logistics, thereby reducing operational costs and waste. There is considerable interest in AI-driven solutions for quality control during magnesite production, from raw material assessment to final product purity analysis, aiming for consistent output and reduced defects. The integration of AI for monitoring equipment performance in mining and processing facilities is also a key area of inquiry, promising increased uptime and predictive maintenance capabilities.

Beyond operational efficiencies, users are also investigating AI's potential in discovering new magnesite deposits through advanced geological data analysis and in developing novel applications for magnesite-based materials. The application of AI in material science research could accelerate the development of advanced refractory materials or new compounds utilizing magnesite, tailored for specific industrial needs. While the direct impact on magnesite's physical properties or fundamental applications remains limited, AI's role in optimizing the entire value chain, from exploration to end-use, is widely anticipated to enhance profitability and sustainability within the industry.

- Optimization of magnesite mining and extraction processes through predictive analytics.

- Enhanced efficiency in mineral processing and beneficiation using machine learning.

- Improved supply chain management, logistics, and demand forecasting for magnesite products.

- AI-driven quality control and purity assessment in magnesite production.

- Potential for AI to accelerate discovery of new deposits and novel applications.

Key Takeaways Magnesite Market Size & Forecast

User inquiries into key takeaways from the magnesite market size and forecast consistently highlight the robust growth trajectory driven by industrial expansion and emerging applications. The consistent Compound Annual Growth Rate (CAGR) projected signifies a stable yet evolving market, indicating sustained demand from its primary end-use sectors while also pointing to diversification into new areas. A significant insight is the increasing valuation, reflecting both volume growth and a potential shift towards higher-value, specialized magnesite products, suggesting opportunities for producers to innovate and capture premium segments. The long-term forecast period provides a clear outlook for strategic planning, signaling confidence in the market's enduring relevance within the global economy.

Furthermore, the insights reveal that market participants should focus on adaptability to regulatory changes and technological advancements, which are increasingly influencing market dynamics. The forecasted growth is not merely organic but is also shaped by global macroeconomic factors, infrastructure development, and environmental policies promoting sustainable material usage. Understanding the interplay between these elements is crucial for stakeholders to capitalize on the market's potential, mitigate risks, and position themselves competitively within a landscape that values both traditional utility and modern sustainability principles. The market's resilience and capacity for innovation stand out as critical factors for future success.

- Projected stable growth indicates a reliable market outlook for investors.

- The increasing market valuation reflects growing demand across diverse applications.

- Strategic focus on high-purity magnesia products is crucial for market share.

- Long-term forecast underscores opportunities for new investments and capacity expansion.

- Adaptation to evolving industrial and environmental regulations is key for sustained growth.

Magnesite Market Drivers Analysis

The global magnesite market is significantly propelled by the burgeoning demand from the steel and refractory industries, which utilize magnesia-based refractories for their high melting points and excellent resistance to thermal shock and chemical corrosion. As global steel production continues to rise, particularly in emerging economies, the consumption of magnesite as a vital raw material for refractory linings in furnaces, kilns, and other high-temperature industrial processes also experiences a corresponding surge. This foundational demand forms the bedrock of the market's growth, ensuring a consistent need for both crude and processed magnesite products.

Additionally, the expanding use of magnesite in environmental applications, such as wastewater treatment, flue gas desulfurization, and CO2 capture technologies, is emerging as a powerful growth driver. With increasing global awareness and stringent regulations regarding industrial emissions and water quality, there is a growing imperative for effective and sustainable solutions, for which magnesite offers a cost-effective and environmentally friendly option. This diversification into green technologies opens new avenues for market expansion beyond traditional industrial uses, contributing substantially to the overall market growth. The versatility of magnesite in these critical applications highlights its importance in addressing contemporary environmental challenges.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing Demand from Steel & Refractory Industries | +2.5% | Asia Pacific, Europe, North America | Short to Medium Term |

| Increasing Use in Environmental Applications | +1.8% | Europe, North America, China | Medium to Long Term |

| Expansion of Cement and Construction Sectors | +1.2% | Asia Pacific, Latin America | Medium Term |

| Technological Advancements in Magnesia Processing | +0.8% | Global | Long Term |

| Rising Demand for Specialty Chemicals and Fertilizers | +0.5% | Global | Medium Term |

Magnesite Market Restraints Analysis

The magnesite market faces significant restraints from the volatility of raw material prices and the high energy consumption associated with its mining and processing. Fluctuations in energy costs directly impact operational expenditures, especially for calcination processes which are energy-intensive, subsequently affecting the final product pricing and profit margins for producers. Geopolitical factors and trade policies in major producing regions can further exacerbate raw material price instability, making long-term planning and investment challenging for market participants. These cost pressures can deter new entrants and may lead to consolidation among existing players.

Furthermore, stringent environmental regulations pertaining to mining activities and industrial emissions pose another considerable restraint. Governments worldwide are imposing stricter rules on land use, waste management, and air pollution, requiring magnesite producers to invest heavily in compliance technologies and sustainable practices. While beneficial for the environment, these regulations can increase operational costs, prolong project timelines, and potentially limit production capacities in certain regions. The availability of substitute materials, particularly in less demanding applications, also acts as a restraint, as industries may opt for alternative refractory or chemical inputs if magnesite prices become uncompetitive or supply becomes unreliable.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Volatile Raw Material Prices and High Energy Costs | -1.5% | Global | Short to Medium Term |

| Stringent Environmental Regulations | -1.0% | Europe, North America, China | Medium to Long Term |

| Availability of Substitute Materials | -0.7% | Global | Medium Term |

| Supply Chain Disruptions and Geopolitical Instability | -0.8% | Global | Short Term |

| Limited High-Purity Magnesite Reserves | -0.4% | Specific Mining Regions | Long Term |

Magnesite Market Opportunities Analysis

The magnesite market is poised for significant opportunities driven by the increasing demand for high-purity magnesia in specialized applications, particularly in the pharmaceutical, chemical, and agricultural sectors. As these industries require materials with precise specifications and minimal impurities, the development and commercialization of advanced beneficiation techniques for producing ultra-pure magnesia present a lucrative avenue for market expansion. Innovations in magnesia-based compounds, such as magnesium hydroxide and magnesium oxide, tailored for specific functions like flame retardants, wastewater adsorbents, and nutritional supplements, can unlock new high-value market segments and enhance profit margins for producers capable of meeting these stringent quality demands.

Furthermore, the growing global focus on sustainable practices and circular economy initiatives creates substantial opportunities for magnesite. The potential for magnesite in carbon capture, utilization, and storage (CCUS) technologies, as well as its use in developing eco-friendly building materials and soil conditioners, aligns perfectly with evolving environmental mandates. Investments in research and development to explore novel applications, improve energy efficiency in production, and enhance resource recovery can position companies at the forefront of sustainable industrial solutions. Additionally, the development of new magnesite deposits or the optimization of existing ones through advanced geological exploration techniques offers long-term supply security and strategic advantages, especially in regions with burgeoning industrial growth and infrastructure development.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Rising Demand for High-Purity Magnesia in Specialty Applications | +1.7% | Global | Medium to Long Term |

| Expansion into Carbon Capture and Sustainable Technologies | +1.3% | Europe, North America, Asia Pacific | Long Term |

| Development of New Magnesite-Based Products and Compounds | +0.9% | Global | Medium to Long Term |

| Untapped Reserves and Exploration of New Mining Areas | +0.6% | Africa, Latin America, Central Asia | Long Term |

| Strategic Partnerships and Collaborations for R&D | +0.5% | Global | Medium Term |

Magnesite Market Challenges Impact Analysis

The magnesite market is confronted by significant challenges, notably intense competition from synthetic and alternative refractory materials. The availability of substitute products, such as alumina, chrome, and silica-based refractories, particularly in applications where cost-effectiveness outweighs specific performance advantages, can exert downward pressure on magnesite prices and market share. This competitive landscape necessitates continuous innovation in product performance and cost efficiency for magnesite producers to maintain their market position. The challenge intensifies when geopolitical factors or trade disputes disrupt the supply chain of natural magnesite, compelling industries to seek readily available alternatives.

Another critical challenge involves the environmental and social impacts associated with magnesite mining and processing. Communities and regulatory bodies are increasingly scrutinizing the ecological footprint of mineral extraction, including habitat destruction, water pollution, and dust emissions. Addressing these concerns often requires substantial investments in environmental impact assessments, remediation efforts, and community engagement programs, which can increase operational costs and extend project timelines. Furthermore, securing social license to operate in new or expanding mining regions can be complex, demanding adherence to ethical labor practices and transparent stakeholder engagement. These multifaceted challenges necessitate a proactive and sustainable approach to operations and market development.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Intense Competition from Substitute Materials | -1.2% | Global | Short to Medium Term |

| Environmental and Social Impact Concerns of Mining | -0.9% | Europe, North America, Australia | Medium to Long Term |

| Fluctuating Demand from Key End-Use Industries | -0.6% | Global | Short Term |

| Technological Barriers in High-Purity Production | -0.5% | Global | Medium Term |

| Logistical Complexities in Remote Mining Regions | -0.3% | Developing Regions | Short to Medium Term |

Magnesite Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the global Magnesite Market, encompassing historical data, current market dynamics, and future projections. It offers a detailed examination of market size, growth drivers, restraints, opportunities, and challenges, alongside a thorough segmentation analysis by product type, application, and region. The report aims to equip stakeholders with critical insights for strategic decision-making and investment planning within this evolving industrial landscape.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 3.2 Billion |

| Market Forecast in 2033 | USD 5.4 Billion |

| Growth Rate | 6.8% |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Global Refractory Solutions Inc., Advanced Magnesia Products Ltd., Sustainable Minerals Corp., Magnesia Resources Group, High-Purity Oxides LLC, Industrial Minerals Global, GreenTech Magnesia Solutions, Premier Mining & Chemicals, Specialized Chemical Producers, EnviroMag Materials, International Refractory Holdings, Asia Pacific Magnesite Inc., EuroMag Chemicals, North American Mineral Extraction, Global Specialty Magnesia. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The magnesite market is intricately segmented to reflect its diverse applications and product forms, allowing for a granular analysis of demand and supply dynamics across various industries. Understanding these segments is crucial for identifying key growth areas and strategic investment opportunities. The primary segmentations include product type, which differentiates between various processed forms of magnesia, and application, which spans a wide array of industrial uses from high-temperature refractories to environmental solutions and agricultural inputs. Each segment exhibits unique growth drivers and market characteristics, influenced by specific technological advancements, regulatory frameworks, and regional industrial developments.

Further granularity is provided through end-use industry segmentation, which highlights the primary sectors consuming magnesite and its derivatives. This detailed breakdown enables a more targeted approach to market analysis, revealing how shifts in global manufacturing, construction, or chemical production directly impact magnesite demand. For instance, the steel industry's performance remains a critical determinant for dead burned magnesia, while the burgeoning environmental sector drives caustic calcined magnesia applications. Such comprehensive segmentation facilitates a nuanced understanding of market trends, allowing stakeholders to anticipate changes and adapt their strategies accordingly.

- By Product Type:

- Dead Burned Magnesia (DBM): Primarily used in refractories due to its high thermal stability.

- Caustic Calcined Magnesia (CCM): Versatile in chemical, agricultural, and environmental applications.

- Fused Magnesia (FM): High-performance refractory material for extreme conditions.

- Magnesium Carbonate: Used in pharmaceuticals, insulation, and fireproofing.

- Others: Including various forms and derivatives for niche applications.

- By Application:

- Refractories: Linings for furnaces, kilns, and other high-temperature equipment.

- Chemicals: Production of magnesium salts, pharmaceuticals, and rubber additives.

- Agriculture: Fertilizers, animal feed supplements, and soil conditioners.

- Construction: Components in cements, insulation boards, and fire-resistant materials.

- Environmental: Wastewater treatment, flue gas desulfurization, and carbon capture.

- Others: Including pulp & paper, abrasives, and automotive parts.

- By End-Use Industry:

- Steel Industry: Major consumer for refractory linings in steel-making.

- Cement Industry: Used in refractory bricks for cement kilns.

- Non-Ferrous Metals: Refractory applications in aluminum, copper, and lead production.

- Glass Industry: Linings for glass melting furnaces.

- Pulp & Paper: Used as a process chemical.

- Pharmaceuticals: Ingredients in antacids and laxatives.

- Others: Diverse industrial and manufacturing processes.

Regional Highlights

- Asia Pacific: Dominates the global magnesite market due to robust growth in the steel, cement, and construction industries, particularly in China and India. The region also benefits from significant magnesite reserves and expanding industrial infrastructure.

- Europe: A mature market with strong demand from the refractory and chemical sectors, coupled with increasing focus on environmental applications and high-purity magnesia. Stringent environmental regulations also drive innovation in sustainable magnesite uses.

- North America: Exhibits steady demand for magnesite, driven by the steel industry, specialty chemicals, and growing adoption in environmental protection technologies. Focus on domestic sourcing and advanced processing technologies is a key trend.

- Latin America: Emerging as a significant region with potential for new mining projects and increasing consumption in local industrial sectors, including construction and agriculture.

- Middle East & Africa (MEA): Growing infrastructure development and industrialization are stimulating demand for refractories and construction materials. The region also holds untapped magnesite reserves, presenting long-term opportunities for exploration and production.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Magnesite Market.- Global Refractory Solutions Inc.

- Advanced Magnesia Products Ltd.

- Sustainable Minerals Corp.

- Magnesia Resources Group

- High-Purity Oxides LLC

- Industrial Minerals Global

- GreenTech Magnesia Solutions

- Premier Mining & Chemicals

- Specialized Chemical Producers

- EnviroMag Materials

- International Refractory Holdings

- Asia Pacific Magnesite Inc.

- EuroMag Chemicals

- North American Mineral Extraction

- Global Specialty Magnesia

- Continental Magnesium Solutions

- Universal Minerals & Mining

- Regional Industrial Magnesia

- Future Chemical Innovations

- Strategic Mineral Supplies

Frequently Asked Questions

Analyze common user questions about the Magnesite market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is magnesite primarily used for?

Magnesite is primarily used in the production of refractories, which are essential for high-temperature industrial processes in the steel, cement, and glass industries. It is also increasingly utilized in chemical, agricultural, and environmental applications.

What are the different types of magnesia products?

The main types of magnesia products derived from magnesite are Dead Burned Magnesia (DBM), Caustic Calcined Magnesia (CCM), and Fused Magnesia (FM), each distinguished by its processing temperature and specific industrial applications.

Which region accounts for the largest share of the magnesite market?

The Asia Pacific region currently holds the largest share of the magnesite market, driven by significant industrial growth and robust demand from its steel, cement, and construction sectors, particularly in countries like China and India.

What factors are driving the growth of the magnesite market?

Key drivers include the expanding demand from the steel and refractory industries, increasing adoption in environmental applications such as wastewater treatment and CO2 capture, and growth in the chemical and construction sectors.

What challenges does the magnesite market face?

Challenges include intense competition from substitute refractory materials, volatile raw material prices and high energy costs for processing, and stringent environmental regulations impacting mining and production activities.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted