LFP Cathode Material Market

LFP Cathode Material Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_704587 | Last Updated : August 11, 2025 |

Format : ![]()

![]()

![]()

![]()

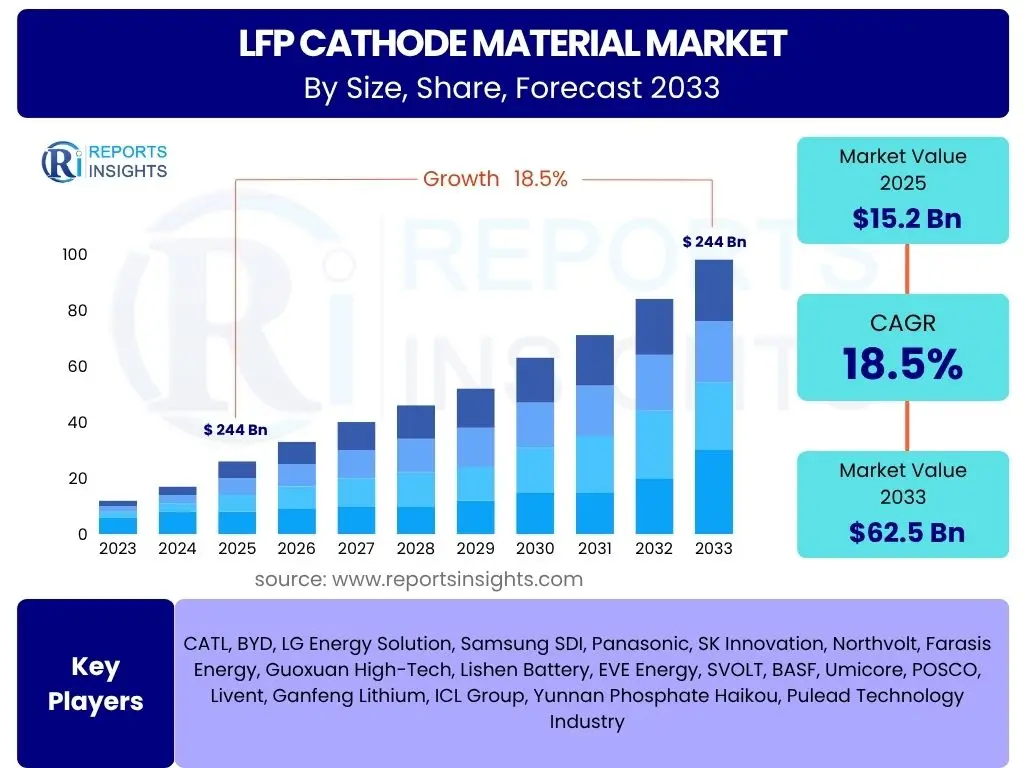

LFP Cathode Material Market Size

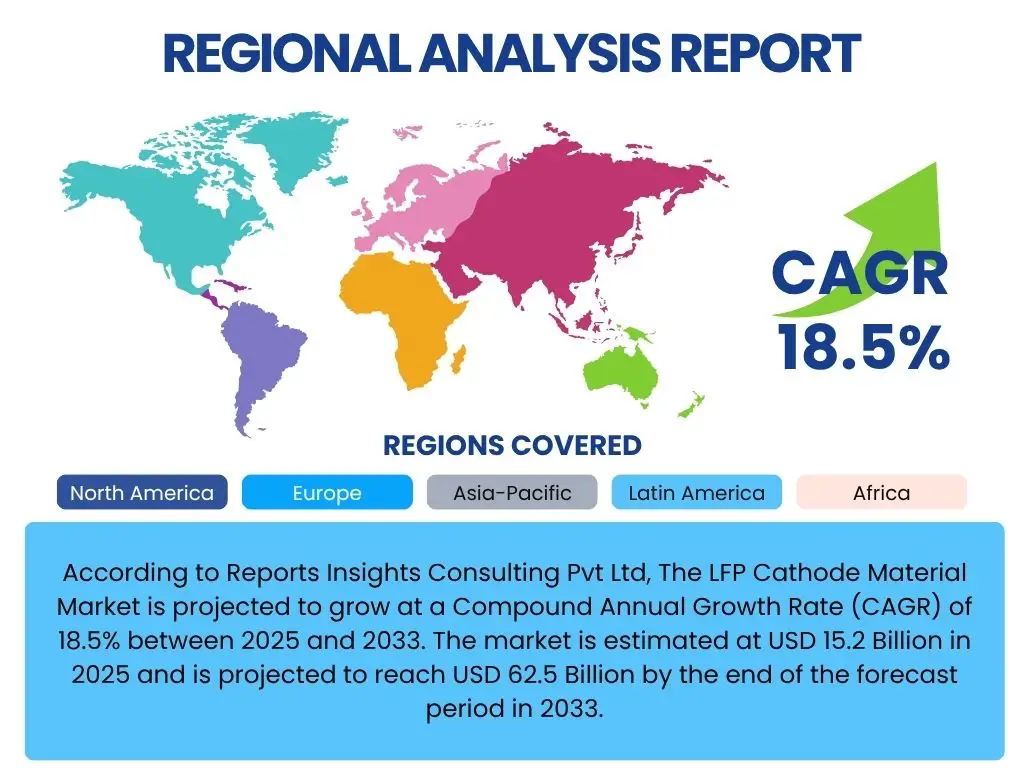

According to Reports Insights Consulting Pvt Ltd, The LFP Cathode Material Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 18.5% between 2025 and 2033. The market is estimated at USD 15.2 Billion in 2025 and is projected to reach USD 62.5 Billion by the end of the forecast period in 2033.

Key LFP Cathode Material Market Trends & Insights

The LFP Cathode Material market is experiencing robust growth driven by its inherent advantages in safety, cost-effectiveness, and longer cycle life, making it increasingly preferred over other battery chemistries for various applications. Common user questions often revolve around LFP's increasing market share in the electric vehicle (EV) segment, particularly for mass-market and commercial vehicles, and its expanding role in stationary energy storage solutions. Users frequently inquire about the technological advancements that are addressing historical limitations of LFP, such as energy density.

Another significant area of interest concerns the geopolitical implications of LFP production and supply chains, as well as the industry's shift towards more sustainable and localized manufacturing. The trend of "cell-to-pack" (CTP) and "cell-to-chassis" (CTC) technologies, which maximize battery capacity by directly integrating cells into the battery pack or vehicle structure, is a key insight that enhances LFP's energy density and cost efficiency, attracting considerable user attention. Furthermore, the evolving regulatory landscape promoting safer battery technologies is also a primary trend shaping market dynamics.

- Dominance in Entry-Level and Mid-Range Electric Vehicles (EVs) and Commercial EVs.

- Significant expansion into Grid-Scale and Residential Energy Storage Systems (ESS).

- Continuous advancements in LFP cell design, including cell-to-pack (CTP) and cell-to-chassis (CTC) integration.

- Enhanced safety profile and extended cycle life offering a competitive edge.

- Increasing focus on localized and diversified supply chains to mitigate geopolitical risks.

- Growing investment in research and development to improve energy density and low-temperature performance.

- Emphasis on sustainability through improved manufacturing processes and recycling initiatives.

AI Impact Analysis on LFP Cathode Material

Common user questions related to the impact of AI on LFP Cathode Material often center on how artificial intelligence and machine learning (AI/ML) can accelerate material discovery, optimize manufacturing processes, and enhance quality control within the LFP production ecosystem. Users are keen to understand if AI can help overcome the inherent energy density limitations of LFP and improve its performance characteristics, such as charging speed and low-temperature operation. The integration of AI for predictive maintenance of manufacturing equipment and supply chain optimization is also a significant area of inquiry.

AI's analytical capabilities are being leveraged to simulate new material compositions, predict their performance, and streamline the R&D cycle for next-generation LFP chemistries. Furthermore, AI-driven process control systems can monitor production lines in real-time, identify anomalies, and fine-tune parameters to improve yield, consistency, and reduce waste. This precision engineering, facilitated by AI, is critical for scaling LFP production to meet burgeoning global demand while maintaining high quality and cost efficiency, addressing key user expectations regarding market maturation and innovation.

- Accelerated discovery and development of novel LFP material compositions with enhanced properties.

- Optimized manufacturing processes leading to higher yield, reduced energy consumption, and lower production costs.

- Improved quality control and defect detection through real-time data analysis and anomaly identification.

- Predictive maintenance for LFP production equipment, minimizing downtime and increasing operational efficiency.

- Enhanced supply chain management and logistics optimization, forecasting demand and managing raw material flow.

- Simulation and modeling of battery performance, enabling faster prototyping and design iteration for LFP cells.

Key Takeaways LFP Cathode Material Market Size & Forecast

The LFP Cathode Material market is poised for significant expansion, driven primarily by its compelling balance of safety, cost-effectiveness, and longevity, which are increasingly prioritized in both the electric vehicle (EV) and energy storage sectors. Users often seek confirmation of this growth trajectory and the underlying factors contributing to LFP's ascendancy. The market's robust compound annual growth rate indicates a strong and sustained demand, underscoring its strategic importance in the global energy transition.

A crucial insight is the LFP technology's evolution, with continuous innovations mitigating some of its historical drawbacks, such as energy density. This ongoing improvement, coupled with favorable economic conditions and increasing governmental support for electrification, positions LFP as a foundational technology for the foreseeable future. The market forecast highlights a substantial increase in valuation, reflecting broad adoption across diverse applications and a maturing supply chain capable of meeting escalating demand.

- Projected exponential growth driven by burgeoning EV adoption and large-scale energy storage deployments.

- LFP's inherent safety and thermal stability are key differentiators fostering widespread acceptance.

- Cost competitiveness positions LFP as the preferred choice for mass-market and commercial applications.

- Technological advancements, including cell-to-pack designs, are enhancing energy density and performance.

- Strategic global investments in LFP production capacity indicate long-term market confidence.

LFP Cathode Material Market Drivers Analysis

The LFP Cathode Material market is experiencing substantial growth propelled by a confluence of economic, technological, and environmental factors. The most prominent driver is the escalating global demand for electric vehicles (EVs), particularly in the entry-level and mid-range segments, where LFP batteries offer an optimal balance of cost, safety, and performance. As consumer awareness regarding climate change and air pollution increases, so does the adoption of EVs, directly fueling the demand for LFP cathodes.

Furthermore, the rapid expansion of grid-scale and residential energy storage systems (ESS) is significantly contributing to market growth. LFP batteries are highly favored for ESS due to their long cycle life, thermal stability, and lower cost per kilowatt-hour, making them ideal for renewable energy integration and grid stabilization. Supportive government policies, incentives for EV adoption, and investments in renewable energy infrastructure worldwide also play a crucial role in accelerating the demand for LFP cathode materials.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Rising Global Electric Vehicle (EV) Adoption | +5.5% | China, Europe, North America, India | 2025-2033 (Long-term) |

| Increasing Demand for Grid-Scale Energy Storage Systems | +4.0% | North America, Europe, APAC (China, Australia) | 2025-2033 (Long-term) |

| Superior Safety Profile and Longer Cycle Life of LFP | +3.0% | Global | 2025-2030 (Medium-term) |

| Cost Competitiveness Against Other Chemistries | +2.5% | Global, particularly emerging markets | 2025-2028 (Short-to-Medium term) |

| Government Initiatives and Subsidies for Green Energy | +2.0% | China, Europe, US, India | 2025-2033 (Long-term) |

LFP Cathode Material Market Restraints Analysis

Despite its significant growth, the LFP Cathode Material market faces certain restraints that could temper its expansion. One primary limitation is the relatively lower energy density of LFP batteries compared to nickel-manganese-cobalt (NMC) or nickel-cobalt-aluminum (NCA) chemistries. While advancements like cell-to-pack technology are mitigating this, it still presents a challenge for high-performance and long-range EV applications where maximizing range per charge is paramount.

Another restraint involves the potential for supply chain volatility and price fluctuations of key raw materials such as lithium and phosphate. Although LFP avoids cobalt and nickel, which have historically seen significant price swings, the increasing demand for lithium globally could lead to supply constraints and cost increases. Furthermore, the performance degradation of LFP batteries in extremely cold temperatures and during very fast charging remains a concern, particularly for consumers in certain climates or those requiring rapid charging capabilities.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Lower Energy Density Compared to NMC/NCA | -2.0% | Global, particularly high-end EV markets | 2025-2030 (Medium-term) |

| Raw Material Price Volatility (Lithium, Phosphate) | -1.5% | Global | 2025-2027 (Short-term) |

| Performance Limitations in Extreme Cold Climates | -1.0% | Northern Europe, North America, Russia | 2025-2033 (Long-term) |

| Slower Charging Rates Compared to Some Alternatives | -0.8% | Global, particularly public charging infrastructure | 2025-2028 (Short-to-Medium term) |

LFP Cathode Material Market Opportunities Analysis

The LFP Cathode Material market presents numerous growth opportunities stemming from technological innovation, expanding application areas, and strategic market positioning. A significant opportunity lies in the continuous advancement of LFP chemistry and battery architecture, such as higher voltage LFP variants and the integration of cell-to-pack and cell-to-chassis designs. These innovations promise to further enhance energy density and overall battery performance, making LFP competitive in a broader range of applications, including longer-range EVs.

Another major avenue for growth is the escalating demand for large-scale grid energy storage solutions. As renewable energy sources like solar and wind become more prevalent, the need for stable and cost-effective energy storage grows exponentially. LFP batteries, with their long cycle life and safety features, are ideally suited for these applications, offering a substantial market opportunity. Furthermore, the development of robust recycling infrastructure for LFP batteries and initiatives for sustainable raw material sourcing also present significant opportunities for long-term market stability and environmental compliance.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Advancements in LFP Cell and Pack Design (CTP/CTC) | +3.5% | Global | 2025-2030 (Medium-term) |

| Expansion into New Application Segments (e.g., Heavy Duty EVs, Marine) | +2.8% | Global | 2028-2033 (Long-term) |

| Growing Demand for Residential and Commercial Energy Storage | +2.2% | North America, Europe, Australia, Japan | 2025-2033 (Long-term) |

| Development of Robust LFP Recycling Infrastructure | +1.5% | Europe, North America, China | 2028-2033 (Long-term) |

| Increased Focus on Localized Production and Supply Chain Diversification | +1.0% | Europe, North America, India | 2025-2033 (Long-term) |

LFP Cathode Material Market Challenges Impact Analysis

The LFP Cathode Material market faces several inherent challenges that could affect its growth trajectory and competitive landscape. One significant challenge is the ongoing pursuit of higher energy density by competing battery chemistries like NMC and NCA, which continue to improve their performance, potentially limiting LFP's penetration in premium and long-range electric vehicle segments. While LFP has made strides, closing this gap entirely remains a formidable engineering task.

Another key challenge is the concentration of LFP cathode material production and raw material processing within specific geographic regions, primarily China. This concentration creates supply chain vulnerabilities, making the market susceptible to geopolitical tensions, trade disputes, or regional disruptions that could impact global availability and pricing. Furthermore, the complexities associated with quality consistency in mass production, especially as new manufacturers enter the market, pose a continuous challenge for maintaining product integrity and performance standards across the industry.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Intense Competition from Other Battery Chemistries (NMC, NCA) | -1.8% | Global, especially premium EV segment | 2025-2033 (Long-term) |

| Geopolitical Risks and Supply Chain Concentration | -1.2% | Global, particularly dependency on APAC | 2025-2030 (Medium-term) |

| Scaling Production While Maintaining Quality Consistency | -0.9% | Global, new entrants and rapid expansion | 2025-2027 (Short-term) |

| Need for Advanced Thermal Management in High-Power Applications | -0.7% | Global, particularly high-performance EVs | 2025-2030 (Medium-term) |

LFP Cathode Material Market - Updated Report Scope

This comprehensive report provides an in-depth analysis of the LFP Cathode Material market, covering its size, growth trajectory, key trends, drivers, restraints, opportunities, and challenges across various segments and major geographical regions. It offers a detailed forecast from 2025 to 2033, examining the market's current landscape and future potential, including the impact of emerging technologies and shifting consumer preferences. The report also profiles leading market participants, offering insights into their strategic initiatives and competitive positioning.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 15.2 Billion |

| Market Forecast in 2033 | USD 62.5 Billion |

| Growth Rate | 18.5% |

| Number of Pages | 267 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | CATL, BYD, LG Energy Solution, Samsung SDI, Panasonic, SK Innovation, Northvolt, Farasis Energy, Guoxuan High-Tech, Lishen Battery, EVE Energy, SVOLT, BASF, Umicore, POSCO, Livent, Ganfeng Lithium, ICL Group, Yunnan Phosphate Haikou, Pulead Technology Industry |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The LFP Cathode Material market is comprehensively segmented to provide a granular view of its diverse applications and technological variations. This segmentation allows for a detailed understanding of demand drivers and market dynamics across different end-use industries and material forms. The primary segmentation is by application, reflecting the major sectors driving LFP adoption, followed by classifications based on the production method and the physical form of the cathode material.

The application segment distinguishes between the burgeoning electric vehicle sector, encompassing various vehicle types, and the rapidly expanding energy storage systems market, which includes grid-scale, residential, and commercial applications. Further segmentation by production method highlights the different industrial processes used to manufacture LFP, while the 'by form' segment addresses whether the material is supplied as a powder or a slurry, influencing its integration into battery manufacturing processes. This multi-layered segmentation is crucial for identifying niche markets and assessing technological preferences.

- By Application:

- Electric Vehicles (Passenger EVs, Commercial EVs, Electric Buses)

- Energy Storage Systems (Grid-Scale, Residential, Commercial & Industrial)

- Consumer Electronics

- Others (e.g., Electric Bicycles, Power Tools)

- By Production Method:

- Solid-Phase Synthesis

- Co-Precipitation Method

- By Form:

- Powder

- Slurry

Regional Highlights

- Asia Pacific (APAC): Dominates the LFP Cathode Material market, primarily driven by China's extensive EV manufacturing base and massive investments in renewable energy and energy storage. Countries like India, Japan, and South Korea are also showing increasing adoption and R&D activities.

- Europe: Witnessing rapid growth due to ambitious decarbonization targets, increasing EV penetration, and significant investments in Gigafactories. Strong government support for sustainable transportation and energy storage solutions fuels demand across Germany, France, and the UK.

- North America: Experiencing substantial growth in the LFP market, propelled by the Inflation Reduction Act (IRA) in the US, which incentivizes domestic battery production and EV adoption. Increasing demand for utility-scale energy storage and commercial EVs is a key driver.

- Latin America: An emerging market with growing interest in EVs and renewable energy projects. While currently smaller, the region presents long-term potential as its automotive and energy sectors mature.

- Middle East and Africa (MEA): Showing nascent growth, primarily driven by large-scale renewable energy projects and nascent EV adoption initiatives in select countries. Investments in smart grids and sustainable infrastructure will gradually increase LFP demand.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the LFP Cathode Material Market.- Contemporary Amperex Technology Co. Limited (CATL)

- BYD Company Limited

- LG Energy Solution

- Samsung SDI Co., Ltd.

- Panasonic Corporation

- SK Innovation Co., Ltd.

- Northvolt AB

- Farasis Energy, Inc.

- Guoxuan High-Tech Co., Ltd. (Gotion High-tech)

- Lishen Battery Co., Ltd.

- EVE Energy Co., Ltd.

- SVOLT Energy Technology Co., Ltd.

- BASF SE

- Umicore N.V.

- POSCO Chemical Co., Ltd.

- Livent Corporation

- Ganfeng Lithium Co., Ltd.

- ICL Group Ltd.

- Yunnan Phosphate Haikou Co., Ltd.

- Pulead Technology Industry Co., Ltd.

Frequently Asked Questions

What are the primary advantages of LFP cathode materials?

LFP cathode materials offer superior safety due to their thermal stability, reducing the risk of thermal runaway. They also boast a longer cycle life, making batteries more durable, and are generally more cost-effective as they do not require expensive and geopolitically sensitive materials like cobalt or nickel.

How is the LFP market projected to grow over the forecast period?

The LFP Cathode Material market is projected to grow at a Compound Annual Growth Rate (CAGR) of 18.5% between 2025 and 2033, expanding from an estimated USD 15.2 Billion in 2025 to USD 62.5 Billion by 2033, driven by increasing adoption in EVs and energy storage.

What are the main applications of LFP batteries?

The primary applications of LFP batteries include electric vehicles (passenger EVs, commercial EVs, and electric buses) due to their safety and cost efficiency. They are also extensively used in energy storage systems (grid-scale, residential, and commercial & industrial) for renewable energy integration and grid stabilization, as well as in consumer electronics and industrial equipment.

What challenges does the LFP market face?

Key challenges for the LFP market include a relatively lower energy density compared to NMC/NCA chemistries, which limits its use in certain long-range EV applications. Other challenges involve potential raw material price volatility, performance limitations in extremely cold temperatures, and the ongoing need for supply chain diversification to reduce geographical concentration risks.

How does LFP compare to other battery chemistries like NMC and NCA?

LFP batteries excel in safety, cost-effectiveness, and cycle life compared to NMC (Nickel-Manganese-Cobalt) and NCA (Nickel-Cobalt-Aluminum) chemistries. However, NMC and NCA typically offer higher energy density, providing longer range for EVs. LFP is often preferred for mass-market EVs and stationary storage where cost and safety are paramount, while NMC/NCA serve premium EV segments.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted