LDPE Packaging Market

LDPE Packaging Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_703219 | Last Updated : August 01, 2025 |

Format : ![]()

![]()

![]()

![]()

LDPE Packaging Market Size

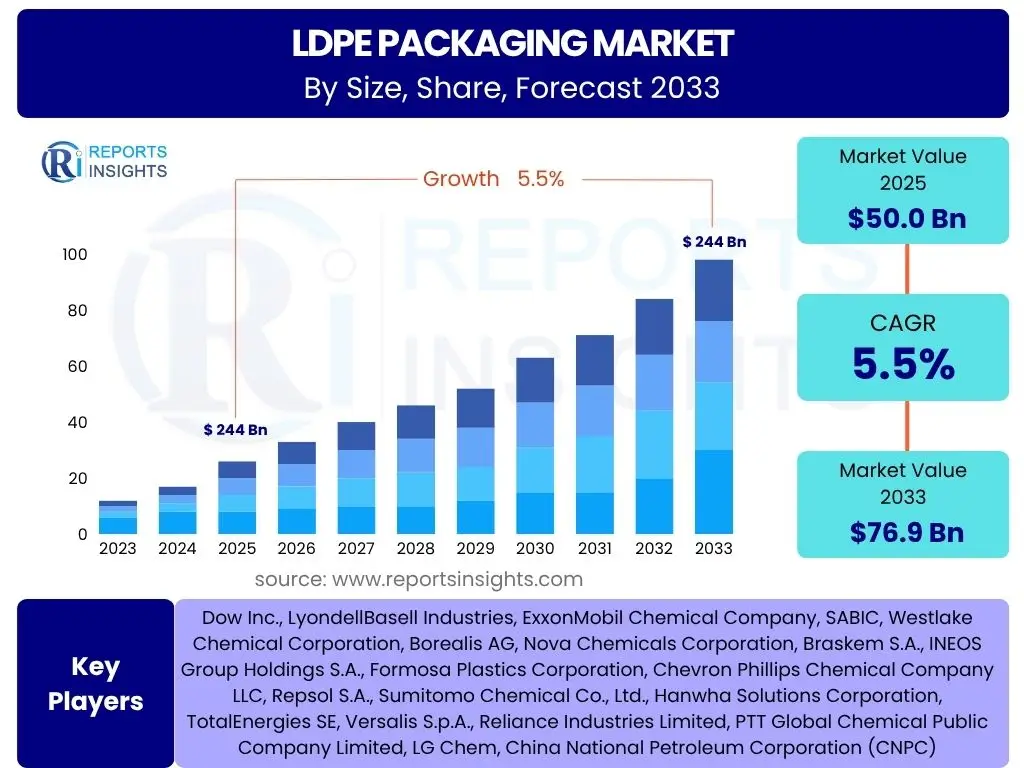

According to Reports Insights Consulting Pvt Ltd, The LDPE Packaging Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.5% between 2025 and 2033. The market is estimated at USD 50.0 Billion in 2025 and is projected to reach USD 76.9 Billion by the end of the forecast period in 2033.

Key LDPE Packaging Market Trends & Insights

The LDPE packaging market is experiencing dynamic shifts, largely influenced by the global imperative for sustainability and the evolving demands of various end-use industries. Key trends highlight a significant pivot towards circular economy principles, with increasing investment in recycling technologies and the integration of recycled content into new packaging solutions. This transformation is driven by consumer preference for eco-friendly products and stringent environmental regulations worldwide, pushing manufacturers to innovate beyond traditional linear models of production and disposal.

Furthermore, the proliferation of e-commerce has substantially amplified the demand for flexible, lightweight, and durable packaging, areas where LDPE excels due to its versatility and protective properties. Advances in material science are also enabling the development of LDPE films with enhanced barrier properties, extending product shelf-life and reducing food waste. This confluence of environmental consciousness, digital retail growth, and technological innovation is shaping the trajectory of the LDPE packaging sector, compelling stakeholders to adopt more sustainable practices and explore novel applications to maintain market relevance and competitive advantage.

- Circular economy initiatives and increased demand for recycled LDPE (rLDPE) content.

- Emphasis on lightweighting and source reduction to minimize material usage and transportation costs.

- Growing adoption of flexible packaging formats across diverse end-use sectors.

- Technological advancements leading to enhanced barrier properties and functional films.

- Expansion of e-commerce driving demand for protective and efficient packaging solutions.

- Integration of smart packaging features for traceability and consumer engagement.

AI Impact Analysis on LDPE Packaging

The integration of Artificial Intelligence (AI) is poised to significantly revolutionize the LDPE packaging value chain, addressing critical operational challenges and fostering sustainable practices. AI technologies offer transformative capabilities in optimizing production processes, enhancing efficiency, and ensuring stringent quality control. For instance, AI-driven predictive maintenance can forecast equipment failures in LDPE manufacturing plants, minimizing downtime and improving overall output, while machine learning algorithms can refine material formulations to achieve desired properties with greater precision and reduced waste.

Beyond manufacturing, AI holds immense potential in advancing the circularity of LDPE packaging. AI-powered sorting systems in recycling facilities can identify and separate different plastic types with unprecedented accuracy, dramatically improving the purity and yield of recycled LDPE. Furthermore, AI can optimize logistics and supply chain management by predicting demand fluctuations, streamlining inventory, and optimizing transportation routes, leading to reduced energy consumption and environmental footprint. The strategic application of AI is thus anticipated to drive operational excellence, bolster sustainability efforts, and unlock new avenues for innovation within the LDPE packaging industry.

- Optimization of manufacturing processes through predictive analytics and machine learning for efficiency and reduced waste.

- Enhanced quality control and defect detection in LDPE film and product manufacturing using computer vision.

- Improved supply chain visibility and demand forecasting, leading to optimized inventory and logistics.

- Advancements in automated sorting and recycling technologies for LDPE, increasing material recovery rates.

- Development of AI-driven tools for designing sustainable LDPE packaging with reduced material usage.

- Personalization and customization of packaging designs through AI-powered consumer insights.

Key Takeaways LDPE Packaging Market Size & Forecast

The LDPE packaging market is demonstrating robust and consistent growth, underscored by its indispensable role in various industries. A primary takeaway is the market's resilience, driven by the expanding demand for flexible packaging across sectors like food and beverage, healthcare, and consumer goods. While traditional applications continue to provide a solid foundation, the market's future growth is increasingly tied to its adaptability to modern consumer needs, such as convenience and product protection, particularly within the burgeoning e-commerce landscape.

Another crucial insight is the accelerating push towards sustainability, which is transforming the LDPE market. Stakeholders are actively seeking solutions that balance performance with environmental responsibility, leading to greater emphasis on recycled content, design for recyclability, and circular economy models. The forecast indicates that success in this market will increasingly depend on the ability of manufacturers to innovate in sustainable materials and processes, mitigate environmental concerns, and navigate evolving regulatory frameworks, ensuring LDPE remains a viable and preferred packaging material in a sustainability-conscious world.

- Consistent growth trajectory primarily fueled by the expansion of flexible packaging applications.

- Increasing significance of sustainability and circular economy principles in driving market innovation.

- Strong demand from the food and beverage, and e-commerce sectors significantly contributing to market expansion.

- Technological advancements in material properties and manufacturing processes are enhancing LDPE's versatility.

- Navigating environmental regulations and consumer perception remains a critical factor for market participants.

LDPE Packaging Market Drivers Analysis

The LDPE packaging market is propelled by a confluence of robust drivers, notably the escalating demand from the food and beverage sector for efficient and protective packaging solutions. LDPE's inherent properties, such as its excellent moisture barrier, flexibility, and cost-effectiveness, make it an ideal choice for preserving freshness and extending the shelf life of various food and beverage products. This consistent demand, coupled with population growth and changing dietary habits globally, forms a foundational driver for market expansion.

Furthermore, the unprecedented growth of the e-commerce industry has significantly bolstered the need for lightweight, durable, and secure packaging that can withstand the rigors of transit. LDPE is extensively utilized in protective films, mailing bags, and various flexible packaging solutions critical for online retail. Its versatility and ability to be easily processed into diverse forms cater effectively to the dynamic requirements of this fast-evolving sector, thus acting as a strong growth impetus for the LDPE packaging market.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing Demand from Food & Beverage Sector | +1.5% | Global | 2025-2033 |

| Expansion of E-commerce Industry | +1.2% | North America, Europe, APAC | 2025-2033 |

| Cost-Effectiveness and Versatility of LDPE | +0.8% | Global | 2025-2033 |

| Increasing Demand for Flexible Packaging | +1.0% | Global | 2025-2030 |

LDPE Packaging Market Restraints Analysis

The LDPE packaging market faces significant headwinds, primarily stemming from escalating environmental concerns related to plastic waste and its impact on ecosystems. Public perception and media scrutiny regarding single-use plastics have intensified, leading to strong calls for reduction and elimination of plastic packaging. This negative sentiment often overlooks LDPE's recyclability and functional benefits, creating a challenging operating environment for market participants and potentially dampening demand in certain applications.

Additionally, the imposition of stringent regulations and bans on single-use plastics across various regions, particularly in Europe and North America, presents a considerable restraint. Governments are increasingly implementing policies such as plastic taxes, extended producer responsibility (EPR) schemes, and outright bans on certain plastic items, compelling industries to seek alternative materials or significantly alter their packaging strategies. These regulatory pressures necessitate substantial investment in R&D for sustainable alternatives or advanced recycling infrastructure, adding to the operational costs and posing compliance challenges for LDPE manufacturers and users.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Environmental Concerns & Plastic Waste | -1.5% | Global | 2025-2033 |

| Stringent Regulations on Single-Use Plastics | -1.2% | Europe, North America, Oceania | 2025-2030 |

| Volatility in Raw Material (Naphtha) Prices | -0.7% | Global | 2025-2033 |

| Competition from Sustainable Alternative Materials | -0.8% | Global | 2027-2033 |

LDPE Packaging Market Opportunities Analysis

Despite existing challenges, the LDPE packaging market is poised for significant opportunities, primarily driven by the escalating demand for recycled content. As sustainability becomes a core business imperative, brands and consumers alike are actively seeking packaging solutions that incorporate post-consumer recycled (PCR) LDPE. This trend creates a lucrative avenue for investment in advanced recycling technologies and processes to produce high-quality rLDPE, thereby reducing reliance on virgin materials and fostering a more circular economy within the packaging industry.

Furthermore, the continuous innovation in LDPE film technology presents substantial growth prospects. Manufacturers are developing multi-layer films with enhanced barrier properties, improved strength-to-weight ratios, and greater versatility, allowing for applications in specialized packaging that require extended shelf life or superior protection. The exploration of biodegradable and compostable LDPE alternatives, while nascent, also represents a long-term opportunity to address environmental concerns and cater to niche markets with specific end-of-life requirements, thus diversifying the market portfolio and expanding its sustainable footprint.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing Demand for Recycled LDPE (rLDPE) Content | +1.8% | Europe, North America, APAC | 2027-2033 |

| Technological Advancements in Film Manufacturing | +1.0% | Developed Regions | 2025-2030 |

| Expansion in Emerging Economies with Growing Consumption | +1.1% | APAC, Latin America, MEA | 2025-2033 |

| Development of High-Performance Barrier Films | +0.9% | Global | 2027-2033 |

LDPE Packaging Market Challenges Impact Analysis

The LDPE packaging market is confronted by several complex challenges that could impede its growth trajectory. A significant hurdle is the persistent lack of comprehensive and robust recycling infrastructure, particularly in developing regions. Despite LDPE being recyclable, the collection, sorting, and processing capabilities often lag behind the volume of plastic consumed, leading to low recycling rates and contributing to plastic pollution. This infrastructure deficit limits the availability of high-quality recycled LDPE, hindering the industry's ability to meet ambitious sustainability targets and consumer demand for circular solutions.

Furthermore, managing the end-of-life of multi-layer LDPE packaging presents a considerable technical challenge. While multi-layer films offer superior barrier properties and performance, their composite nature makes them difficult to recycle efficiently using conventional methods, often leading to them being incinerated or landfilled. Addressing this complexity requires innovation in design for recyclability, advanced separation technologies, and the development of new recycling pathways, demanding significant collaborative efforts and investments across the value chain to overcome these inherent material complexities and enhance the overall sustainability profile of LDPE packaging.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Lack of Robust Recycling Infrastructure | -1.0% | Developing Regions | 2025-2033 |

| Complexities in Multi-Layer Packaging Recycling | -0.7% | Global | 2025-2030 |

| Shifting Consumer Preferences Towards Non-Plastic Materials | -0.6% | Europe, North America | 2027-2033 |

| Compliance with Evolving Extended Producer Responsibility (EPR) Schemes | -0.5% | Europe, North America | 2025-2033 |

LDPE Packaging Market - Updated Report Scope

This comprehensive report meticulously analyzes the LDPE Packaging Market, offering a detailed assessment of its current status and future outlook. It covers market size estimations, historical trends, and projections for growth, providing critical insights into the factors influencing the market. The scope extends to a thorough segmentation analysis across various parameters, identifying key growth areas and regional dynamics. Furthermore, the report profiles leading market players, offering a competitive landscape analysis essential for strategic decision-making.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 50.0 Billion |

| Market Forecast in 2033 | USD 76.9 Billion |

| Growth Rate | 5.5% |

| Number of Pages | 250 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Dow Inc., LyondellBasell Industries, ExxonMobil Chemical Company, SABIC, Westlake Chemical Corporation, Borealis AG, Nova Chemicals Corporation, Braskem S.A., INEOS Group Holdings S.A., Formosa Plastics Corporation, Chevron Phillips Chemical Company LLC, Repsol S.A., Sumitomo Chemical Co., Ltd., Hanwha Solutions Corporation, TotalEnergies SE, Versalis S.p.A., Reliance Industries Limited, PTT Global Chemical Public Company Limited, LG Chem, China National Petroleum Corporation (CNPC) |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The LDPE packaging market is extensively segmented to provide a granular understanding of its diverse applications and market dynamics. This segmentation facilitates a deeper analysis of specific industry requirements and consumer preferences that drive demand for LDPE in various forms and applications. By dissecting the market across applications, forms, grades, and end-use industries, this report offers a comprehensive view of where LDPE is utilized, its functional importance, and the specific growth drivers within each sub-segment.

Understanding these segmentations is crucial for stakeholders to identify lucrative opportunities, tailor product development, and devise effective market entry strategies. For instance, the demand for LDPE films in the food and beverage sector for flexible packaging differs significantly from its use in heavy-duty industrial bags or agricultural mulch films. Each segment presents unique challenges and growth avenues, influenced by regional regulations, technological advancements, and evolving consumer behavior, thereby shaping the overall market landscape.

- By Application: Food & Beverage, Healthcare & Pharmaceutical, Industrial, Personal Care & Cosmetics, Consumer Goods, Agriculture, Others.

- By Form: Films (Stretch Film, Shrink Film, Lidding Film, Agricultural Film, Barrier Film, Non-barrier Film), Bags & Pouches (Stand-up Pouches, Gusseted Bags, Reclosable Bags), Sheets, Bottles & Containers, Others (Liners, Closures).

- By Grade: Film Grade, Injection Molding Grade, Blow Molding Grade, Wire & Cable Grade, Extrusion Coating Grade.

- By End-Use Industry: Food & Beverage, Pharmaceutical & Healthcare, Industrial, Consumer Goods, Agriculture, Retail, Others.

Regional Highlights

- North America: This region is characterized by high consumption of packaged goods and a robust e-commerce sector, driving consistent demand for LDPE packaging. Innovation in sustainable packaging solutions and the adoption of recycled content are key trends, though regulatory pressures concerning plastic waste are also significant. The presence of major market players and advanced recycling initiatives contributes to market evolution.

- Europe: Europe is a leader in adopting circular economy principles and implementing stringent regulations on plastic waste, which profoundly impacts the LDPE packaging market. There is a strong emphasis on design for recyclability, increased use of recycled LDPE, and the exploration of bio-based alternatives. High consumer awareness regarding environmental issues further shapes market demand.

- Asia Pacific (APAC): APAC represents the largest and fastest-growing market for LDPE packaging, fueled by rapid urbanization, industrialization, rising disposable incomes, and the expansion of the food and beverage industry. Countries like China and India are major manufacturing hubs and consumption centers. While growth is robust, challenges related to waste management infrastructure are prominent.

- Latin America: This region is experiencing steady growth in LDPE packaging demand, driven by expanding retail sectors, increasing consumer spending, and the proliferation of packaged food products. Brazil and Mexico are key markets, benefiting from foreign investments and domestic industrial growth. Focus on cost-effective and flexible packaging solutions remains dominant.

- Middle East and Africa (MEA): The MEA region presents emerging opportunities for LDPE packaging, particularly with infrastructure development, population growth, and increasing demand from the food, beverage, and industrial sectors. Investments in manufacturing capabilities and improving logistics are contributing factors, though the market is still in a relatively nascent stage compared to developed regions.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the LDPE Packaging Market.- Dow Inc.

- LyondellBasell Industries

- ExxonMobil Chemical Company

- SABIC

- Westlake Chemical Corporation

- Borealis AG

- Nova Chemicals Corporation

- Braskem S.A.

- INEOS Group Holdings S.A.

- Formosa Plastics Corporation

- Chevron Phillips Chemical Company LLC

- Repsol S.A.

- Sumitomo Chemical Co., Ltd.

- Hanwha Solutions Corporation

- TotalEnergies SE

- Versalis S.p.A.

- Reliance Industries Limited

- PTT Global Chemical Public Company Limited

- LG Chem

- China National Petroleum Corporation (CNPC)

Frequently Asked Questions

What is LDPE packaging primarily used for?

LDPE packaging is extensively used for flexible applications such as films, bags, and pouches due to its flexibility, transparency, and excellent moisture barrier properties. It is a dominant material in the food and beverage sector for packaging fresh produce, frozen foods, and bakery items, as well as in industrial, agricultural, and consumer goods packaging for its protective and cost-effective nature.

Is LDPE packaging recyclable?

Yes, LDPE packaging is recyclable. It is typically identified by the resin code "4" triangle. However, the actual recycling rate depends on the availability and efficiency of local recycling infrastructure. Efforts are increasing globally to improve collection and processing of LDPE to facilitate its reintroduction into the circular economy.

How do environmental regulations impact the LDPE market?

Environmental regulations, including bans on single-use plastics, plastic taxes, and extended producer responsibility (EPR) schemes, significantly impact the LDPE market by driving demand for sustainable alternatives and recycled content. These regulations compel manufacturers to innovate in design for recyclability and invest in advanced recycling technologies, influencing production methods and material choices.

What are the key drivers for LDPE packaging market growth?

The primary drivers include the expanding food and beverage industry, the rapid growth of e-commerce necessitating flexible and protective packaging, LDPE's inherent cost-effectiveness and versatility, and increasing demand for films in various industrial and agricultural applications. These factors contribute to its consistent market expansion.

What innovations are expected in LDPE packaging?

Expected innovations in LDPE packaging include the development of high-performance films with enhanced barrier properties, increased integration of recycled content (rLDPE), the creation of mono-material structures to improve recyclability, and advancements in biodegradable or compostable LDPE alternatives. Smart packaging features and AI-driven production optimization are also emerging areas of innovation.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted