Laser Drilling Machine for Aerospace Market

Laser Drilling Machine for Aerospace Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_705070 | Last Updated : August 11, 2025 |

Format : ![]()

![]()

![]()

![]()

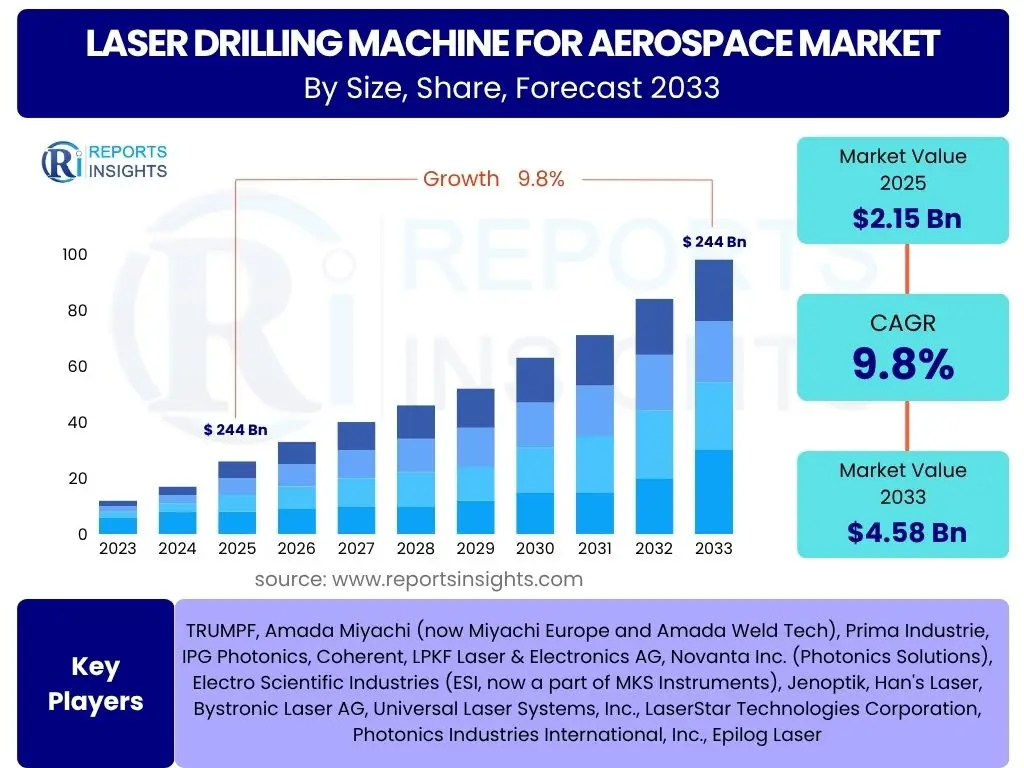

Laser Drilling Machine for Aerospace Market Size

According to Reports Insights Consulting Pvt Ltd, The Laser Drilling Machine for Aerospace Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 9.8% between 2025 and 2033. The market is estimated at USD 2.15 Billion in 2025 and is projected to reach USD 4.58 Billion by the end of the forecast period in 2033. This robust growth is primarily driven by the increasing demand for high-precision, efficient, and versatile manufacturing processes in the rapidly evolving aerospace sector. The shift towards lightweight materials and complex component designs further amplifies the need for advanced drilling technologies that traditional methods cannot adequately address.

Key Laser Drilling Machine for Aerospace Market Trends & Insights

User inquiries about the Laser Drilling Machine for Aerospace market frequently center on technological advancements, material processing capabilities, and integration with broader manufacturing trends. Analysis reveals a strong interest in the adoption of ultrafast lasers for improved precision and reduced heat-affected zones, crucial for sensitive aerospace components. Furthermore, the push towards automation and Industry 4.0 principles is a recurring theme, highlighting the desire for integrated, intelligent drilling solutions that enhance productivity and quality control. The market is also seeing a trend towards specialized systems capable of handling a diverse range of aerospace-grade materials, from advanced composites to superalloys, which demand highly adaptive and precise drilling techniques.

Another significant insight derived from common questions is the evolving landscape of aerospace manufacturing, characterized by a greater emphasis on sustainability and efficiency. This translates into a demand for laser drilling machines that not only offer superior performance but also reduce material waste and energy consumption. The drive for customized and on-demand manufacturing solutions is also pushing laser drilling technology towards greater flexibility and scalability, allowing for rapid prototyping and efficient production of both high-volume standardized parts and low-volume complex components. The integration of advanced diagnostics and real-time monitoring capabilities is another emerging trend, enabling predictive maintenance and enhanced process control.

- Adoption of ultrafast (picosecond and femtosecond) lasers for enhanced precision.

- Increased integration of laser drilling systems with automated production lines and robotics.

- Growing demand for multi-axis laser drilling systems for complex geometries.

- Emphasis on processing advanced materials like carbon fiber composites and nickel-based superalloys.

- Development of smart laser drilling solutions with real-time monitoring and adaptive control.

AI Impact Analysis on Laser Drilling Machine for Aerospace

Common user questions regarding AI's impact on the Laser Drilling Machine for Aerospace market revolve around its potential to optimize processes, improve quality, and enable predictive maintenance. Users are keen to understand how AI algorithms can enhance drilling accuracy, reduce cycle times, and minimize defects by analyzing vast datasets from the manufacturing process. There is significant interest in AI-driven vision systems for real-time quality inspection and automated parameter adjustment, ensuring consistent hole quality across large production batches. Furthermore, inquiries highlight the potential for AI to integrate disparate manufacturing data, leading to more efficient workflows and better decision-making in complex aerospace production environments.

The application of AI extends beyond process optimization to areas like predictive maintenance, where AI can analyze machine performance data to anticipate potential failures, thereby minimizing downtime and extending equipment lifespan. Users also express curiosity about AI's role in material science and design, envisioning a future where AI-powered simulations guide optimal laser parameters for new aerospace alloys and composite structures. This suggests a desire for AI to not only refine existing drilling operations but also to innovate the capabilities of laser technology for future aerospace challenges, ultimately contributing to higher operational efficiency and reduced manufacturing costs.

- Process Optimization: AI algorithms analyze drilling parameters and real-time sensor data to optimize laser power, pulse duration, and focus, leading to improved hole quality and reduced cycle times.

- Predictive Maintenance: AI-driven analytics monitor machine health, predicting potential component failures and scheduling maintenance proactively, minimizing unplanned downtime.

- Quality Control: AI-powered vision systems enable automated, high-speed inspection of drilled holes, detecting defects with superior accuracy and consistency compared to manual methods.

- Adaptive Manufacturing: AI allows laser drilling machines to adapt to variations in material properties or environmental conditions, maintaining optimal performance automatically.

- Design and Simulation: AI assists in simulating laser-material interactions, helping engineers determine optimal drilling strategies for new materials and complex designs, accelerating R&D.

Key Takeaways Laser Drilling Machine for Aerospace Market Size & Forecast

Analysis of common user questions regarding the Laser Drilling Machine for Aerospace market size and forecast consistently points to the criticality of precision and efficiency in aerospace manufacturing. Users are primarily concerned with understanding the market’s growth trajectory, driven by the increasing complexity of aircraft components and the adoption of advanced materials that necessitate non-conventional machining methods. The forecast indicates a strong upward trend, underscoring the indispensable role of laser drilling in meeting stringent aerospace quality and performance standards. Furthermore, the market's expansion is intrinsically linked to global aerospace production rates and the ongoing modernization of existing aircraft fleets.

Another key takeaway is the recognition that technological innovation, particularly in laser source development and automation, will be central to sustaining market growth. The shift towards higher power, faster pulse rates, and greater beam control is directly addressing the industry’s need for faster throughput without compromising quality. The market also reflects a strategic emphasis on solutions that can handle diverse material properties, from metallic alloys to carbon fiber reinforced polymers (CFRPs), signifying the importance of versatility for aerospace manufacturers. This comprehensive growth is expected across various applications, from engine components to airframes, highlighting the broad utility and increasing adoption of laser drilling technology.

- The market is poised for significant growth, driven by advanced material adoption and complex component designs.

- Precision, efficiency, and automation are paramount factors influencing market expansion.

- Ultrafast lasers and intelligent systems are key technological drivers for future growth.

- Aerospace industry's demand for reduced weight and enhanced performance fuels laser drilling adoption.

- North America and Europe currently dominate, but Asia Pacific is emerging as a rapid growth region.

Laser Drilling Machine for Aerospace Market Drivers Analysis

The increasing demand for advanced materials like composites and superalloys in modern aircraft manufacturing is a primary driver for the Laser Drilling Machine for Aerospace Market. These materials, essential for enhancing fuel efficiency and structural integrity, often prove challenging to machine using traditional methods due to their hardness and tendency to deform. Laser drilling offers a non-contact, high-precision solution, enabling the creation of intricate hole patterns with minimal material distortion. Furthermore, the global rise in commercial aircraft orders and defense spending directly correlates with the need for efficient and reliable drilling technologies for engine components, airframes, and structural elements.

The relentless pursuit of fuel efficiency and reduced emissions in the aerospace industry mandates the development of lighter, more aerodynamic components, which frequently incorporate complex geometries and require highly precise drilling for assembly and operational performance. Laser drilling provides the necessary accuracy and flexibility to meet these evolving design requirements, facilitating the adoption of innovative aircraft designs. Additionally, the growing emphasis on automation and Industry 4.0 principles within aerospace manufacturing pushes for integrated, high-throughput laser drilling systems that can reduce human error, improve repeatability, and streamline production processes, thereby contributing significantly to market growth.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing use of advanced materials (composites, superalloys) | +2.5% | Global, particularly North America, Europe, Asia Pacific | 2025-2033 |

| Growing demand for lightweight and fuel-efficient aircraft | +2.0% | Global | 2025-2033 |

| Technological advancements in laser sources and optics | +1.8% | Global | 2025-2030 |

| Rising adoption of automation and Industry 4.0 in aerospace manufacturing | +1.5% | North America, Europe, China | 2025-2033 |

| Expansion of aerospace manufacturing capacities globally | +1.0% | Asia Pacific, North America, Europe | 2025-2033 |

Laser Drilling Machine for Aerospace Market Restraints Analysis

The high initial capital investment required for advanced laser drilling machines poses a significant restraint on market growth, particularly for smaller and medium-sized enterprises (SMEs) in the aerospace supply chain. These sophisticated systems, along with their associated infrastructure and maintenance, represent a substantial upfront cost that can deter adoption, even given their long-term benefits. This financial barrier can limit the widespread deployment of laser drilling technology, especially in regions with less developed aerospace manufacturing ecosystems or in companies operating with tighter budgets.

Another considerable restraint is the complexity of operating and maintaining these high-precision machines, which necessitates highly skilled technicians and engineers. A shortage of such specialized labor, coupled with the need for continuous training to keep pace with evolving laser technologies, presents a challenge for manufacturers. Furthermore, the inherent material-specific challenges, such as delamination in composites or thermal damage in sensitive alloys if parameters are not precisely controlled, require extensive research and development, adding to the operational complexity and potentially hindering broader application across all aerospace materials.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High initial capital investment and operational costs | -1.5% | Global, especially emerging markets | 2025-2033 |

| Need for highly skilled labor and specialized training | -1.0% | Global | 2025-2033 |

| Technological limitations for certain complex material processes | -0.8% | Global | 2025-2030 |

| Stringent regulatory requirements and certification processes | -0.5% | North America, Europe | 2025-2033 |

Laser Drilling Machine for Aerospace Market Opportunities Analysis

The expansion of the Maintenance, Repair, and Overhaul (MRO) sector within aerospace presents a significant opportunity for laser drilling machine manufacturers. As aircraft fleets age and require more extensive maintenance, there is a growing demand for precise and efficient repair techniques for components like turbine blades, which frequently require hole drilling for cooling or structural integrity. Laser drilling offers a non-contact, low-force alternative to traditional methods, ideal for repairing delicate or complex parts without causing further damage, thus extending the lifespan of costly components and reducing overall operational costs for airlines and MRO providers.

The emergence of new aerospace programs, including next-generation commercial aircraft, advanced military platforms, and burgeoning urban air mobility (UAM) vehicles, offers substantial opportunities for market growth. These new programs often involve revolutionary designs and materials, pushing the boundaries of manufacturing capabilities and creating a demand for cutting-edge laser drilling solutions. Additionally, the increasing integration of additive manufacturing (3D printing) in aerospace production, which often creates parts requiring post-processing such as precise hole drilling, opens a new avenue for laser drilling machines as a complementary technology, ensuring the final product meets exacting aerospace standards.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growth in the aerospace MRO (Maintenance, Repair, Overhaul) sector | +1.8% | Global | 2025-2033 |

| Development of new aerospace programs and next-gen aircraft | +1.5% | North America, Europe, Asia Pacific | 2025-2033 |

| Integration with additive manufacturing post-processing | +1.2% | Global | 2027-2033 |

| Emerging markets' investment in domestic aerospace manufacturing | +1.0% | Asia Pacific, Middle East | 2025-2033 |

| Miniaturization trends in aerospace components | +0.8% | Global | 2025-2030 |

Laser Drilling Machine for Aerospace Market Challenges Impact Analysis

One of the primary challenges facing the Laser Drilling Machine for Aerospace Market is the ongoing material compatibility issues, particularly with the expanding use of diverse and complex aerospace-grade materials. While laser drilling excels with many materials, achieving optimal results across all composite types, specialized alloys, and ceramic matrix composites can be difficult. Ensuring consistent hole quality, avoiding delamination, and minimizing heat-affected zones requires precise parameter control and advanced laser sources, which can be challenging to implement universally across a broad material spectrum without extensive R&D and specialized system configurations.

Another significant challenge involves the stringent certification and regulatory compliance required for aerospace components. Any manufacturing process, including laser drilling, must meet rigorous industry standards and receive multiple certifications, a process that can be time-consuming and costly. This includes validating the integrity of drilled holes under extreme operating conditions and ensuring repeatability across all production batches. Additionally, the complexity of integrating advanced laser drilling systems into existing aerospace production lines, often involving legacy equipment and processes, poses a technical and logistical hurdle that requires substantial investment in infrastructure and re-training of the workforce.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Material-specific processing complexities (e.g., delamination in composites) | -1.2% | Global | 2025-2033 |

| Stringent quality control and certification requirements | -1.0% | Global, especially North America, Europe | 2025-2033 |

| High research and development investment for new applications | -0.7% | Global | 2025-2030 |

| Competition from alternative advanced machining technologies | -0.5% | Global | 2025-2033 |

Laser Drilling Machine for Aerospace Market - Updated Report Scope

This report provides a comprehensive analysis of the Laser Drilling Machine for Aerospace Market, offering insights into market size, growth drivers, restraints, opportunities, and challenges across various segments and key regions. It covers the technological landscape, examining the impact of advancements such as ultrafast lasers and AI integration on market dynamics. The report also details market segmentation by laser type, application, end-use, and regional distribution, alongside a profile of leading industry players, providing a strategic outlook for stakeholders.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 2.15 Billion |

| Market Forecast in 2033 | USD 4.58 Billion |

| Growth Rate | 9.8% |

| Number of Pages | 245 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | TRUMPF, Amada Miyachi (now Miyachi Europe and Amada Weld Tech), Prima Industrie, IPG Photonics, Coherent, LPKF Laser & Electronics AG, Novanta Inc. (Photonics Solutions), Electro Scientific Industries (ESI, now a part of MKS Instruments), Jenoptik, Han's Laser, Bystronic Laser AG, Universal Laser Systems, Inc., LaserStar Technologies Corporation, Photonics Industries International, Inc., Epilog Laser |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Laser Drilling Machine for Aerospace Market is meticulously segmented to provide a granular view of its diverse applications and technological nuances. This segmentation highlights the various types of laser technologies utilized, the specific components and applications they serve within aircraft, and the distinct end-use sectors driving demand. Understanding these segments is crucial for stakeholders to identify niche opportunities, tailor product development, and refine market strategies, reflecting the highly specialized nature of aerospace manufacturing requirements.

Segmentation by laser type reveals the ongoing shift towards more precise and efficient laser sources, such as ultrafast lasers, which are critical for processing advanced materials without thermal damage. Application-based segmentation clarifies the specific needs for drilling cooling holes in engine components versus fastener holes in airframe structures, each demanding different laser parameters and machine configurations. Furthermore, end-use and component segmentation underscores the varied requirements of commercial versus military aerospace, as well as the unique demands of MRO activities, providing a comprehensive framework for market analysis and strategic planning.

- By Laser Type:

- CO2 Laser

- Fiber Laser

- Nd:YAG Laser

- Excimer Laser

- Diode Laser

- Ultrafast Lasers (Picosecond, Femtosecond)

- By Application:

- Cooling Holes

- Fastener Holes

- Vents

- Access Holes

- Inspection Holes

- Assembly Holes

- Others (Micro-drilling, Shaped Holes)

- By End-Use:

- Commercial Aircraft

- Military Aircraft

- Spacecraft

- UAVs (Unmanned Aerial Vehicles)

- MRO (Maintenance, Repair, and Overhaul)

- By Component:

- Turbine Blades

- Combustion Liners

- Exhaust Nozzles

- Airframe Structures

- Wing Components

- Engine Casings

- Landing Gear

- Avionics

- Others

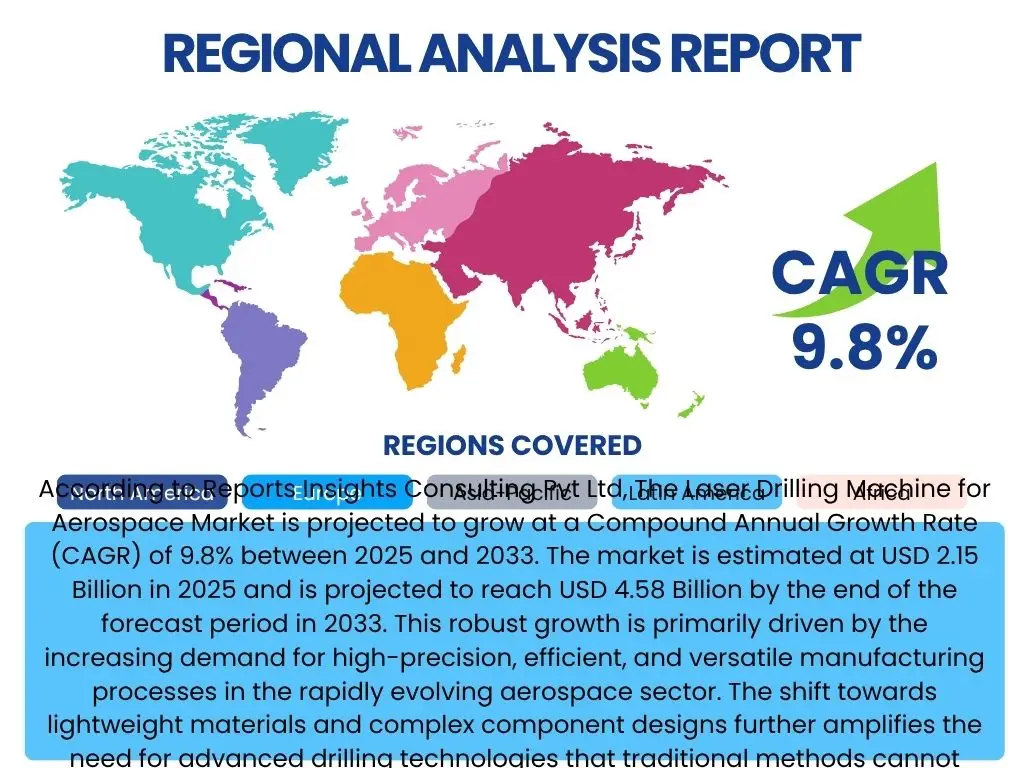

Regional Highlights

North America continues to be a dominant force in the Laser Drilling Machine for Aerospace Market, primarily due to the presence of major aircraft manufacturers, robust defense spending, and significant investments in aerospace R&D. The region benefits from a well-established supply chain and a strong focus on adopting advanced manufacturing technologies. The United States, in particular, drives much of the demand, fueled by large-scale commercial and military aircraft production, as well as pioneering efforts in space exploration and next-generation aerospace systems. This region’s commitment to innovation and high-quality production standards ensures a sustained demand for precise laser drilling solutions.

Europe also holds a substantial share in the market, driven by leading aerospace companies and a strong emphasis on collaborative research initiatives. Countries like Germany, France, and the UK are at the forefront of aerospace manufacturing and MRO activities, constantly seeking efficiency improvements and advanced material processing capabilities. The region's stringent quality regulations and push for sustainable aviation further accelerate the adoption of advanced laser technologies. Asia Pacific is projected to exhibit the highest growth rate, propelled by increasing commercial aircraft demand, expanding domestic aerospace manufacturing capabilities in countries like China and India, and rising investments in defense and space programs. This region's burgeoning middle class and rapid economic development are contributing to a surge in air travel, necessitating greater aircraft production and, consequently, more sophisticated manufacturing tools.

- North America: Leading market share driven by established aerospace giants, high defense expenditure, and significant R&D investments in advanced manufacturing technologies, particularly in the United States and Canada.

- Europe: Strong market presence attributed to major aircraft and engine manufacturers (e.g., Airbus, Safran), robust MRO activities, and a focus on integrating Industry 4.0 principles in aerospace production across countries like Germany, France, and the UK.

- Asia Pacific (APAC): Fastest-growing region due to burgeoning commercial aviation demand, increasing domestic aircraft production capabilities, and growing defense and space programs, notably in China, India, and Japan.

- Latin America, Middle East, and Africa (MEA): Emerging markets with growing aerospace investments, particularly in MRO and regional aviation, contributing to a gradual increase in demand for advanced drilling solutions.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Laser Drilling Machine for Aerospace Market.- TRUMPF

- Amada Miyachi (now Miyachi Europe and Amada Weld Tech)

- Prima Industrie

- IPG Photonics

- Coherent

- LPKF Laser & Electronics AG

- Novanta Inc. (Photonics Solutions)

- Electro Scientific Industries (ESI, now a part of MKS Instruments)

- Jenoptik

- Han's Laser

- Bystronic Laser AG

- Universal Laser Systems, Inc.

- LaserStar Technologies Corporation

- Photonics Industries International, Inc.

- Epilog Laser

Frequently Asked Questions

Analyze common user questions about the Laser Drilling Machine for Aerospace market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is the primary benefit of laser drilling for aerospace components?

The primary benefit is superior precision and the ability to machine complex geometries and advanced materials (like superalloys and composites) with minimal heat-affected zones and delamination, which is critical for aerospace safety and performance standards.

Which laser types are most commonly used in aerospace drilling?

Nd:YAG lasers, Fiber Lasers, and increasingly Ultrafast Lasers (picosecond and femtosecond) are commonly used due to their ability to deliver high precision, speed, and versatility across a range of aerospace materials.

How does laser drilling contribute to aircraft fuel efficiency?

Laser drilling enables the creation of highly precise and intricate cooling holes in turbine blades and other engine components, optimizing airflow and combustion efficiency. It also facilitates the use of lightweight advanced materials, which directly contributes to reduced aircraft weight and improved fuel economy.

What challenges exist in adopting laser drilling technology in aerospace manufacturing?

Challenges include the high initial capital investment, the need for highly skilled operators, material-specific processing complexities, and stringent aerospace certification requirements for newly adopted processes.

What is the role of AI in the future of laser drilling for aerospace?

AI is expected to significantly enhance process optimization, enable predictive maintenance, improve real-time quality control through advanced vision systems, and facilitate adaptive manufacturing, leading to higher efficiency and superior component quality.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted