Lactose Intolerance Food Market

Lactose Intolerance Food Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_705750 | Last Updated : August 17, 2025 |

Format : ![]()

![]()

![]()

![]()

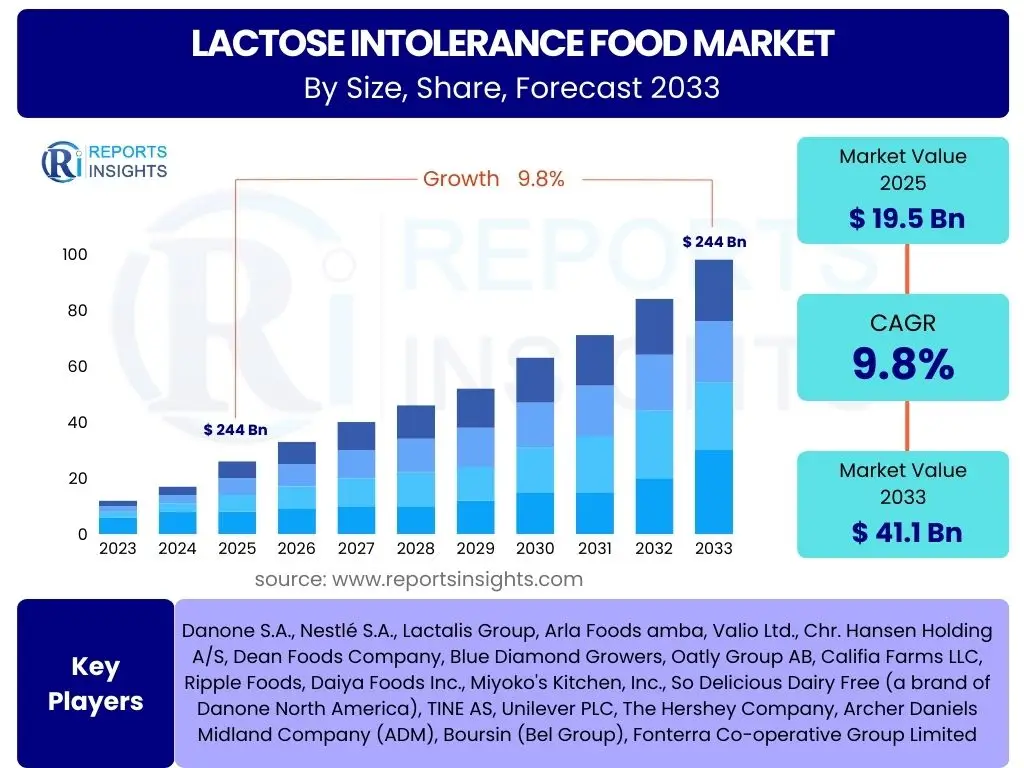

Lactose Intolerance Food Market Size

According to Reports Insights Consulting Pvt Ltd, The Lactose Intolerance Food Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 9.8% between 2025 and 2033. The market is estimated at USD 19.5 Billion in 2025 and is projected to reach USD 41.1 Billion by the end of the forecast period in 2033.

Key Lactose Intolerance Food Market Trends & Insights

The Lactose Intolerance Food market is experiencing significant transformation driven by shifting consumer preferences and growing health awareness. A primary trend involves the increasing demand for plant-based alternatives, as consumers not only seek lactose-free options but also products free from animal derivatives. This has led to a proliferation of almond, oat, soy, and pea-based milk, yogurt, and cheese products, pushing manufacturers to innovate beyond traditional dairy-free formulations. Furthermore, there's a notable movement towards clean label products, where consumers prioritize natural ingredients, minimal processing, and transparent sourcing, influencing product development towards simpler, healthier formulations without artificial additives.

Another crucial trend shaping the market is the expansion of product categories beyond basic milk alternatives. Manufacturers are now offering a wider array of lactose-free products, including ice creams, yogurts, cheeses, protein powders, and ready-to-eat meals, catering to diverse dietary needs and lifestyle choices. The rise of e-commerce and specialized online retailers has also made lactose-intolerant foods more accessible to a global consumer base, fostering market penetration and convenience. Additionally, advancements in enzyme technology are improving the taste and texture of lactose-reduced dairy products, making them more appealing to a broader audience who still desire the benefits of dairy without the discomfort.

- Increasing prevalence and diagnosis of lactose intolerance globally.

- Growing consumer preference for plant-based dairy alternatives.

- Innovation in product categories beyond traditional milk substitutes.

- Rising awareness about digestive health and well-being.

- Technological advancements in lactose-reduction processes.

- Expansion of distribution channels, including online retail and specialty stores.

- Demand for clean label and naturally sourced ingredients.

AI Impact Analysis on Lactose Intolerance Food

Artificial intelligence is poised to significantly transform the Lactose Intolerance Food market by enhancing precision in various stages, from product development to supply chain management and personalized consumer experiences. AI-powered analytics can process vast amounts of data related to consumer dietary patterns, genetic predispositions, and ingredient efficacy, enabling companies to identify emerging trends and formulate highly targeted lactose-free products. This capability supports the creation of more effective and palatable alternatives, addressing specific consumer needs and reducing the trial-and-error often associated with new product introductions. AI also facilitates the discovery of novel ingredients and processing methods that can improve the taste, texture, and nutritional profile of lactose-free options, overcoming traditional formulation challenges.

In terms of operations, AI can optimize supply chains for lactose-intolerant food products, predicting demand fluctuations, managing inventory levels, and streamlining logistics to minimize waste and ensure product freshness. This leads to greater efficiency and cost savings for manufacturers, which can be passed on to consumers, making specialized products more affordable. Furthermore, AI-driven platforms can offer personalized dietary recommendations and support to individuals with lactose intolerance, providing tailored meal plans, product suggestions, and real-time advice based on their unique health data and preferences. This level of personalized engagement can foster greater consumer loyalty and satisfaction, while also supporting improved health outcomes for individuals managing their lactose intolerance.

- AI-driven personalized nutrition recommendations for individuals with lactose intolerance.

- Optimization of supply chain and logistics for lactose-free product distribution.

- Enhanced R&D through AI for novel ingredient discovery and product formulation.

- Predictive analytics for consumer demand and market trends in lactose-free foods.

- Improved quality control and traceability using AI in manufacturing processes.

- Development of AI-powered diagnostic tools for precise lactose intolerance detection.

Key Takeaways Lactose Intolerance Food Market Size & Forecast

The Lactose Intolerance Food market is poised for robust growth, driven by an increasing global prevalence of lactose intolerance, rising health consciousness, and significant advancements in food technology. The projected Compound Annual Growth Rate (CAGR) of 9.8% signifies a rapidly expanding sector with substantial opportunities for innovation and market expansion. This growth is not merely incidental but a reflection of a fundamental shift in consumer dietary habits and an enhanced understanding of digestive health, propelling demand for specialized food products. Stakeholders should recognize the long-term potential of this market, characterized by sustained consumer interest in functional foods that address specific health needs.

Furthermore, the market's trajectory indicates a broadening scope beyond traditional dairy alternatives, encompassing a diverse range of food categories, from baked goods to snacks and prepared meals. This diversification underscores the need for manufacturers to adopt agile product development strategies, leveraging new ingredients and processing methods to meet evolving consumer expectations for taste, texture, and nutritional value. The forecast also highlights the critical role of geographical expansion, particularly into emerging markets, where awareness and accessibility of lactose-free products are growing. Investing in R&D, sustainable sourcing, and efficient distribution networks will be paramount for companies aiming to capitalize on this dynamic market segment and secure a competitive advantage in the coming years.

- Significant market expansion anticipated with a CAGR of 9.8% through 2033.

- Consumer awareness and diagnosis rates of lactose intolerance are major growth catalysts.

- Diversification of product offerings beyond basic milk substitutes is key to market innovation.

- Strong potential for market entry and expansion in developing regions.

- Technological advancements in food processing are crucial for product quality improvement.

- E-commerce and specialized retail channels are enhancing product accessibility.

Lactose Intolerance Food Market Drivers Analysis

The primary drivers of the Lactose Intolerance Food market are multifaceted, stemming from a global rise in the prevalence of lactose intolerance and increasing consumer awareness about digestive health. As diagnostic capabilities improve and information becomes more accessible, more individuals are identifying their intolerance, leading directly to a higher demand for suitable food options. This growing health consciousness also extends to general wellness, where consumers are proactively seeking foods that contribute to better digestion and overall well-being, even without a formal diagnosis, thereby expanding the potential consumer base for lactose-free products.

Technological advancements in food processing and ingredient innovation have also played a crucial role in enabling the development of better-tasting and more varied lactose-free products. This includes improved enzyme technologies for lactose hydrolysis in dairy, as well as sophisticated methods for creating plant-based alternatives that mimic the sensory profiles of traditional dairy. Additionally, robust marketing and awareness campaigns by manufacturers and health organizations are further educating consumers about lactose intolerance and the availability of diverse food choices, contributing significantly to market growth.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Prevalence of Lactose Intolerance | +2.5% | Global, particularly Asia Pacific, Africa, and Latin America | Short to Long Term (2025-2033) |

| Rising Health Consciousness & Wellness Trends | +1.8% | North America, Europe, Developed Asia Pacific | Medium to Long Term (2025-2033) |

| Product Innovation & Portfolio Expansion | +1.5% | Global, especially key innovation hubs like North America, Europe | Short to Medium Term (2025-2029) |

| Advancements in Food Technology & Enzyme Production | +1.2% | Global | Medium to Long Term (2027-2033) |

Lactose Intolerance Food Market Restraints Analysis

Despite significant growth, the Lactose Intolerance Food market faces several restraints that could impact its expansion. One major challenge is the relatively higher cost of specialized lactose-free products compared to their conventional counterparts. The specialized processing, unique ingredients (especially for plant-based alternatives), and smaller production scales often lead to elevated prices, which can deter price-sensitive consumers, particularly in developing economies. This cost disparity can limit market penetration and make these products less accessible to a broader demographic, hindering overall market volume.

Another restraint involves the taste and texture challenges associated with some lactose-free and dairy-alternative products. While significant improvements have been made, some consumers still perceive a difference in flavor or mouthfeel compared to traditional dairy, which can affect repeat purchases and overall consumer acceptance. Additionally, the fragmented nature of consumer awareness in certain regions, coupled with a lack of clear labeling standards in some markets, can lead to confusion and mistrust among potential buyers, slowing down adoption rates. The intense competition from an ever-growing array of general dairy alternative products, which may not explicitly target lactose intolerance but serve a similar need, also poses a competitive pressure on dedicated lactose-intolerance food brands.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Higher Cost of Specialized Products | -1.3% | Global, particularly emerging economies | Short to Long Term (2025-2033) |

| Taste and Texture Challenges of Alternatives | -0.8% | North America, Europe | Short to Medium Term (2025-2029) |

| Lack of Uniform Awareness & Labeling Standards | -0.5% | Certain developing regions, varied by country | Medium Term (2026-2031) |

Lactose Intolerance Food Market Opportunities Analysis

The Lactose Intolerance Food market presents significant opportunities for innovation and growth, particularly in expanding product offerings and exploring new geographic markets. The rising demand for personalized nutrition solutions offers a compelling avenue for manufacturers to develop highly customized lactose-free products that cater to individual dietary needs, preferences, and health goals, moving beyond a one-size-fits-all approach. This includes incorporating functional ingredients such as probiotics, prebiotics, and fortified vitamins, enhancing the health benefits of lactose-free options and appealing to a broader wellness-focused consumer base.

Emerging economies, particularly in Asia Pacific, Latin America, and Africa, represent untapped markets with significant growth potential. These regions often have a higher genetic predisposition to lactose intolerance combined with rapidly increasing disposable incomes and growing urbanization, leading to greater access to and demand for specialized food products. Strategic investments in developing appropriate distribution channels, localizing product flavors, and increasing consumer education in these regions could unlock substantial market share. Furthermore, the continuous evolution of plant-based technology and sustainable sourcing practices offers opportunities for brands to differentiate themselves and appeal to environmentally conscious consumers, integrating ethical considerations with dietary needs.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Expansion into Emerging Markets | +1.7% | Asia Pacific, Latin America, Middle East & Africa | Medium to Long Term (2026-2033) |

| Development of Functional & Fortified Lactose-Free Products | +1.4% | Global, particularly North America, Europe | Short to Medium Term (2025-2029) |

| Diversification into New Product Categories (e.g., snacks, ready meals) | +1.1% | Global | Short to Medium Term (2025-2030) |

| Leveraging E-commerce and Direct-to-Consumer Models | +0.9% | Global | Short to Medium Term (2025-2028) |

Lactose Intolerance Food Market Challenges Impact Analysis

The Lactose Intolerance Food market faces several challenges that require strategic navigation for sustained growth. One significant challenge is maintaining product quality and consistency across various lactose-free and dairy-alternative formulations, especially when dealing with complex sensory attributes like taste, texture, and mouthfeel. Achieving a parity or superiority with traditional dairy products is crucial for consumer acceptance and retention, yet it often demands advanced food science and careful ingredient selection. Moreover, ensuring a stable and cost-effective supply chain for specialized ingredients, particularly plant-based proteins or specific enzymes, can be complex, influenced by agricultural yields, climate conditions, and global trade dynamics.

Regulatory complexities and varying labeling requirements across different countries pose another considerable hurdle for international market expansion. Manufacturers must adhere to diverse food safety standards, allergen labeling rules, and marketing claims, which can increase operational costs and slow down market entry. Additionally, intense competition from a burgeoning number of new entrants, ranging from large multinational corporations diversifying their portfolios to innovative startups, puts pressure on pricing and market share. Brands must continuously innovate and differentiate their offerings to stand out in a crowded market, while also addressing consumer education regarding the benefits and differences of lactose-free products.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Maintaining Taste and Texture Parity with Traditional Dairy | -1.0% | North America, Europe | Short to Medium Term (2025-2029) |

| Supply Chain Volatility & Ingredient Sourcing | -0.7% | Global | Short Term (2025-2027) |

| Intense Competition from Mainstream & Niche Players | -0.6% | Global | Short to Long Term (2025-2033) |

| Regulatory Hurdles & Varied Labeling Standards | -0.4% | Global, varied by region | Medium Term (2026-2030) |

Lactose Intolerance Food Market - Updated Report Scope

This comprehensive report provides a detailed analysis of the Lactose Intolerance Food market, offering a granular view of market dynamics, segmentation, and regional landscapes. It encompasses historical data from 2019 to 2023, establishes 2024 as the base year, and projects market trends and growth forecasts up to 2033. The report meticulously examines key market drivers, restraints, opportunities, and challenges, providing a holistic understanding of the factors influencing market expansion and contraction. It also delves into the competitive landscape, profiling key players and their strategic initiatives, alongside an in-depth segmentation analysis across various product types, sources, forms, distribution channels, and applications, ensuring a complete market overview for stakeholders and investors.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 19.5 Billion |

| Market Forecast in 2033 | USD 41.1 Billion |

| Growth Rate | 9.8% |

| Number of Pages | 267 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Danone S.A., Nestlé S.A., Lactalis Group, Arla Foods amba, Valio Ltd., Chr. Hansen Holding A/S, Dean Foods Company, Blue Diamond Growers, Oatly Group AB, Califia Farms LLC, Ripple Foods, Daiya Foods Inc., Miyoko's Kitchen, Inc., So Delicious Dairy Free (a brand of Danone North America), TINE AS, Unilever PLC, The Hershey Company, Archer Daniels Midland Company (ADM), Boursin (Bel Group), Fonterra Co-operative Group Limited |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Lactose Intolerance Food market is extensively segmented to provide a granular view of its diverse landscape and consumer preferences. This segmentation allows for a detailed understanding of consumer behavior across various product categories, enabling manufacturers and retailers to tailor their strategies effectively. The market is primarily segmented by product type, encompassing a wide range of lactose-free and dairy-alternative options, including milk, cheese, yogurt, ice cream, and specialized infant formulas, reflecting the comprehensive nature of dietary shifts. Further breakdowns by the source of these products highlight the growing prominence of plant-based alternatives alongside traditional lactose-reduced dairy, showcasing evolving consumer choices and technological advancements in ingredient sourcing.

Additional segmentation by form (liquid, solid, powder, semi-solid) provides insights into product versatility and convenience, catering to different consumption occasions and culinary applications. The analysis of distribution channels, including supermarkets, online retail, and specialty stores, illuminates the most effective routes to market and consumer accessibility. Furthermore, segmenting by application (retail/household vs. foodservice) helps to identify key demand centers and growth opportunities in both consumer-facing and commercial sectors. This multi-dimensional segmentation is crucial for identifying niche markets, understanding competitive dynamics, and formulating targeted marketing and product development strategies in the lactose intolerance food sector.

- Product Type:

- Dairy-Free Milk (Almond Milk, Oat Milk, Soy Milk, Coconut Milk, Rice Milk, Pea Milk, Cashew Milk, Hemp Milk, etc.)

- Cheese (Shreds, Slices, Blocks, Spreads)

- Yogurt (Cups, Drinks)

- Ice Cream & Frozen Desserts

- Butter & Spreads

- Infant Formula

- Desserts & Confectionery

- Probiotic Drinks

- Baking & Cooking Ingredients

- Other Lactose-Free Foods

- Source:

- Cow's Milk (Lactose-Reduced/Lactase-Treated)

- Plant-Based (Almond, Soy, Oat, Coconut, Rice, Pea, Cashew, Hemp, etc.)

- Goat/Sheep Milk (Naturally Low Lactose)

- Form:

- Liquid

- Solid

- Powder

- Semi-Solid

- Distribution Channel:

- Supermarkets/Hypermarkets

- Convenience Stores

- Online Retail

- Specialty Stores

- Pharmacies

- Foodservice (Restaurants, Cafes, Institutions)

- Application:

- Retail/Household

- Foodservice Industry

Regional Highlights

- North America: The United States and Canada are leading markets due to high consumer awareness, widespread diagnosis of lactose intolerance, and a strong presence of key market players actively innovating in the plant-based and lactose-reduced dairy segments. High disposable incomes and a culture of health consciousness also contribute significantly.

- Europe: Countries like Germany, the UK, France, and Italy exhibit robust demand, driven by increasing prevalence of lactose intolerance, stringent food labeling regulations, and a well-established market for functional foods and beverages. Scandinavian countries are also notable for their advanced dairy-free offerings.

- Asia Pacific (APAC): This region is projected to be the fastest-growing market, primarily due to the high natural prevalence of lactose intolerance among Asian populations, coupled with rising disposable incomes, rapid urbanization, and growing Western influence on dietary habits in countries like China, India, and Japan. Increased access to diagnostic tools and awareness campaigns are further fueling demand.

- Latin America: Brazil, Mexico, and Argentina are key countries where increasing health awareness and improvements in product availability are driving market expansion. The region is witnessing a gradual shift towards healthier food options, including lactose-free alternatives.

- Middle East and Africa (MEA): While currently a smaller market, the MEA region is expected to show promising growth, influenced by rising health awareness, increasing incidence of digestive disorders, and expanding retail infrastructure. Cultural dietary preferences are also evolving, creating new opportunities.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Lactose Intolerance Food Market.- Danone S.A.

- Nestlé S.A.

- Lactalis Group

- Arla Foods amba

- Valio Ltd.

- Chr. Hansen Holding A/S

- Dean Foods Company

- Blue Diamond Growers

- Oatly Group AB

- Califia Farms LLC

- Ripple Foods

- Daiya Foods Inc.

- Miyoko's Kitchen, Inc.

- So Delicious Dairy Free

- TINE AS

- Unilever PLC

- The Hershey Company

- Archer Daniels Midland Company (ADM)

- Boursin (Bel Group)

- Fonterra Co-operative Group Limited

Frequently Asked Questions

Analyze common user questions about the Lactose Intolerance Food market and generate a concise list of summarized FAQs reflecting key topics and concerns.What defines lactose intolerance food?

Lactose intolerance food refers to products specifically formulated to be free from or significantly reduced in lactose, a sugar found in milk. This includes dairy products treated with lactase enzyme to break down lactose, as well as naturally lactose-free alternatives derived from plants (e.g., almond, oat, soy, coconut) or other animal milks (e.g., goat, sheep) that are naturally low in lactose.

What key factors are driving the growth of the lactose intolerance food market?

The market's growth is primarily driven by the increasing global prevalence of lactose intolerance, heightened consumer awareness regarding digestive health, continuous innovation in product development offering diverse and palatable options, and expanding distribution channels, particularly online retail and specialty stores.

Which regions are most significant for the lactose intolerance food market's expansion?

North America and Europe currently hold substantial market shares due to high awareness and established product availability. However, Asia Pacific is projected to be the fastest-growing region, driven by high inherent lactose intolerance rates in its population and rapidly improving economic conditions and consumer access.

What are the main types of lactose intolerance food products available?

The market offers a wide array of products including dairy-free milk alternatives (e.g., almond, oat, soy milk), lactose-free cheeses, yogurts, ice creams, and specialized infant formulas. There is also a growing segment of lactose-free spreads, desserts, and baking ingredients to cater to diverse culinary needs.

What challenges do manufacturers in the lactose intolerance food market face?

Key challenges include achieving taste and texture parity with traditional dairy products, managing the higher production costs of specialized ingredients, navigating complex and varied regulatory standards across different regions, and competing effectively within an increasingly crowded market with numerous new entrants.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted