Ironless Motor Market

Ironless Motor Market Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_706795 | Last Updated : September 08, 2025 |

Format : ![]()

![]()

![]()

![]()

Ironless Motor Market Size

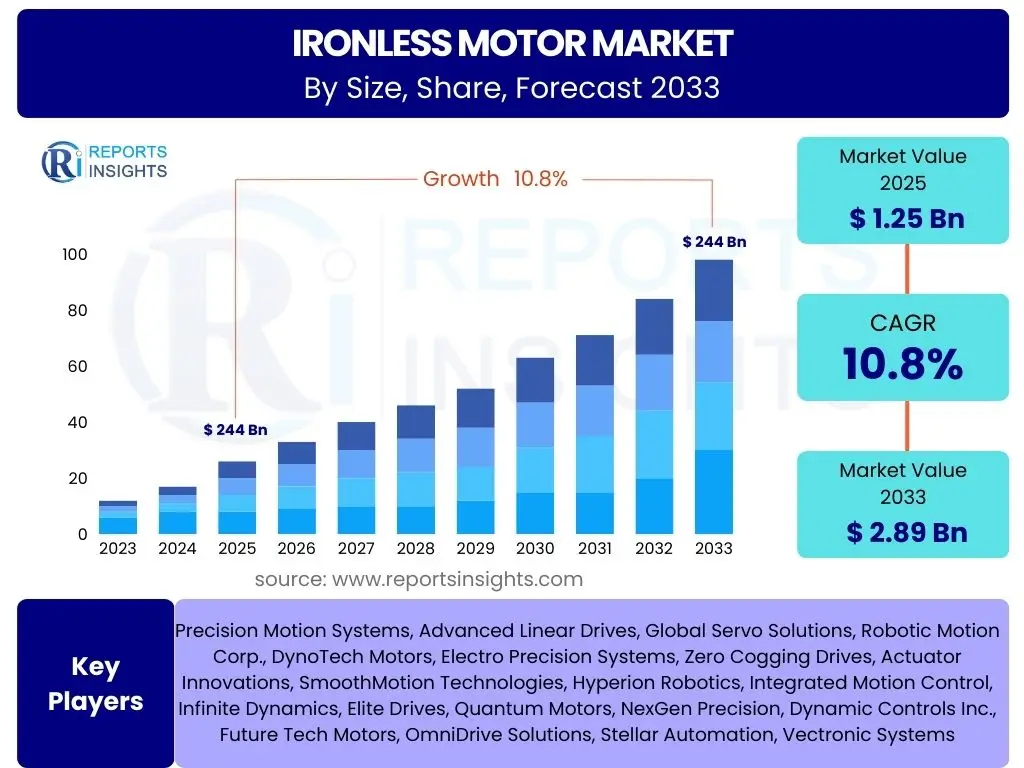

According to Reports Insights Consulting Pvt Ltd, The Ironless Motor Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 10.8% between 2025 and 2033. The market is estimated at USD 1.25 billion in 2025 and is projected to reach USD 2.89 billion by the end of the forecast period in 2033.

Key Ironless Motor Market Trends & Insights

User inquiries frequently focus on the evolving landscape of ironless motor applications, particularly regarding miniaturization, energy efficiency, and integration into advanced automation systems. A significant trend involves the increasing demand for high-precision motion control across various industries, necessitating motors that offer zero cogging and minimal force ripple. The integration of ironless motors into compact, high-performance devices, from medical instruments to consumer electronics, highlights a shift towards more sophisticated and discreet design requirements.

Another area of interest revolves around the adoption of ironless motors in emerging technologies such as humanoid robotics and advanced manufacturing processes, where smooth and accurate movement is paramount. Furthermore, the push for sustainable industrial practices is driving innovation in energy-efficient motor designs, positioning ironless motors as a preferred choice due to their inherent efficiency benefits compared to traditional iron-core counterparts. This trend is amplified by the global emphasis on reducing carbon footprints and optimizing operational costs in industrial settings.

- Growing demand for high-precision and smooth motion control in industrial automation and robotics.

- Increased adoption in medical devices and laboratory automation due to their quiet operation and absence of cogging.

- Miniaturization of electronic devices driving the need for compact and lightweight motor solutions.

- Rising focus on energy efficiency and low heat generation in motor applications.

- Emergence of new applications in aerospace, drones, and haptics requiring precise and efficient linear or rotary motion.

AI Impact Analysis on Ironless Motor

Common user questions regarding AI's impact on ironless motors often center on its role in design optimization, predictive maintenance, and enhancing operational efficiency. AI-driven simulation tools are transforming the design phase, allowing engineers to rapidly iterate and optimize motor parameters for specific performance criteria, such as maximizing efficiency or minimizing vibration. This computational approach significantly reduces development cycles and material waste, leading to more innovative and cost-effective ironless motor solutions.

Moreover, AI is playing a crucial role in the post-deployment phase. Machine learning algorithms can analyze real-time operational data from ironless motors to predict potential failures, optimize maintenance schedules, and identify opportunities for performance enhancement. This not only extends the lifespan of the motors but also reduces downtime in critical applications, thereby enhancing overall system reliability and productivity. The integration of AI for quality control in manufacturing processes also ensures higher consistency and precision in the production of these highly sensitive components.

- AI-driven generative design and optimization for enhanced motor performance and efficiency.

- Predictive maintenance analytics powered by AI to minimize downtime and extend motor lifespan.

- Intelligent control systems for real-time adjustments and precise motion control in complex applications.

- AI-assisted quality control and fault detection during the manufacturing process.

- Optimization of energy consumption and heat management through machine learning algorithms.

Key Takeaways Ironless Motor Market Size & Forecast

The ironless motor market is poised for substantial expansion, driven by an escalating demand for highly precise, efficient, and compact motion solutions across diverse industries. The forecast indicates robust growth, with a significant increase in market value over the next eight years. This trajectory is largely attributable to advancements in automation technologies, the increasing sophistication of medical devices, and the continuous innovation in consumer electronics, all of which benefit from the unique advantages offered by ironless motor designs. Market participants should focus on research and development to address specific application needs and technological integration challenges.

The market's resilience is further supported by its expanding utility in niche high-growth sectors such as advanced robotics, where the zero-cogging and low-inertia properties of ironless motors are indispensable. Strategic investments in manufacturing scalability and the development of new materials will be critical for companies aiming to capitalize on this growth. Furthermore, understanding regional demand patterns, particularly in Asia Pacific due to its manufacturing prowess, will be key to formulating effective market entry and expansion strategies to maximize market share.

- The market exhibits strong growth potential, driven by technological advancements and expanding application areas.

- High-precision and efficiency requirements in various industries are key growth accelerators.

- Asia Pacific is expected to be a dominant region due to manufacturing and automation sector growth.

- Continuous innovation in design and materials will be crucial for competitive advantage.

- Strategic partnerships and mergers & acquisitions are likely to shape the competitive landscape.

Ironless Motor Market Drivers Analysis

The global shift towards advanced automation and robotics across industrial sectors is a primary driver for the ironless motor market. Industries are increasingly adopting automated systems to enhance productivity, precision, and safety, leading to a surge in demand for motors that can deliver smooth, accurate, and repeatable movements without cogging. Ironless motors, with their inherent lack of iron core, offer superior performance in applications requiring high dynamic response and virtually zero force ripple, making them ideal for precise robotic arms, pick-and-place machines, and automated inspection systems.

Furthermore, the escalating demand for miniaturization and high-performance in medical devices, laboratory automation, and consumer electronics significantly propels market growth. Ironless motors are preferred in these sensitive applications due to their compact size, lightweight nature, quiet operation, and the absence of electromagnetic interference often associated with iron-core motors. This makes them indispensable for devices such as surgical robots, diagnostic equipment, and camera stabilization systems, where precision and reliability are non-negotiable. The continuous innovation in these high-growth sectors directly translates into increased adoption of ironless motor technology.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Demand for Precision and Automation | +2.5% | North America, Europe, Asia Pacific | 2025-2033 |

| Miniaturization in Medical Devices & Electronics | +2.0% | Global, particularly North America, Europe, Japan | 2025-2033 |

| Growth in Robotics and Semiconductor Industries | +1.8% | Asia Pacific (China, South Korea, Japan), North America | 2025-2033 |

| Emphasis on Energy Efficiency and Low Heat Generation | +1.5% | Global | 2025-2033 |

| Technological Advancements in Material Science | +1.0% | Global | 2027-2033 |

Ironless Motor Market Restraints Analysis

One of the primary restraints in the ironless motor market is the relatively higher manufacturing cost compared to traditional iron-core motors. The intricate design, specialized materials, and precise assembly processes required for ironless motors contribute to their elevated production expenses. This cost factor can be a significant barrier to adoption, particularly in price-sensitive applications or industries where a robust yet more affordable alternative is available. While their performance benefits often justify the higher initial investment, the initial capital outlay can deter smaller enterprises or applications with less stringent precision requirements.

Another significant challenge is the inherent susceptibility of ironless motors to demagnetization under extreme operating conditions, such as high temperatures or strong external magnetic fields. Unlike iron-core motors that have a robust iron structure to protect the magnets, ironless designs expose the magnets more directly. This vulnerability necessitates careful thermal management and shielding in demanding environments, adding to the complexity and cost of system integration. Furthermore, their lower inherent stiffness compared to iron-core motors can be a limitation in applications requiring very high force output or extreme mechanical rigidity, narrowing their scope in certain heavy-duty industrial contexts.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Higher Manufacturing Costs | -1.5% | Global, particularly emerging markets | 2025-2030 |

| Susceptibility to Demagnetization (Heat/External Fields) | -1.0% | Global, high-temperature/harsh environments | 2025-2033 |

| Challenges in Heat Dissipation at High Power | -0.8% | Global, high-duty cycle applications | 2025-2033 |

| Limited Force Density Compared to Iron-Core Motors | -0.7% | Global, heavy industrial applications | 2025-2033 |

| Complexity in System Integration and Control | -0.5% | Global, smaller enterprises | 2025-2028 |

Ironless Motor Market Opportunities Analysis

The burgeoning electric vehicle (EV) market presents a significant opportunity for ironless motors, particularly in applications beyond propulsion, such as steering systems, braking, and various auxiliary components where precise, efficient, and lightweight motion is crucial. As EVs continue to evolve with more sophisticated autonomous features and enhanced comfort systems, the demand for compact, low-noise, and highly responsive motors will naturally increase. Ironless motors can offer significant advantages in these areas by contributing to overall vehicle efficiency and performance, reducing weight, and enabling advanced haptic feedback systems.

Furthermore, the rapid advancement in advanced robotics, including collaborative robots (cobots) and humanoid robots, opens up new avenues for ironless motor adoption. These applications require motors with minimal or zero cogging, high accuracy, smooth motion, and low inertia for delicate manipulation and safe human-robot interaction. The continuous investment in smart factories and Industry 4.0 initiatives globally also creates a fertile ground for ironless motors in high-speed pick-and-place, vision systems, and precision assembly lines. The expansion into these highly specialized and performance-driven sectors will significantly bolster market growth and expand the technological frontiers for ironless motor development.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Expanding Applications in Electric Vehicles (Auxiliary) | +1.8% | North America, Europe, Asia Pacific (China) | 2026-2033 |

| Growth of Advanced and Collaborative Robotics | +1.7% | Global, particularly industrialized nations | 2025-2033 |

| Demand from Smart Factories and Industry 4.0 Initiatives | +1.5% | Europe, Asia Pacific, North America | 2025-2033 |

| Development of High-Precision Medical Implants and Devices | +1.2% | North America, Europe | 2027-2033 |

| Emergence of New Consumer Electronics Categories (AR/VR, Haptics) | +0.9% | Global | 2028-2033 |

Ironless Motor Market Challenges Impact Analysis

One notable challenge facing the ironless motor market is the inherent technological complexity involved in their design and manufacturing. Achieving the required levels of precision, reliability, and performance demands advanced engineering expertise, specialized production equipment, and rigorous quality control processes. This complexity can limit the number of manufacturers capable of producing high-quality ironless motors, leading to a concentrated supply chain and potential bottlenecks. Moreover, the continuous need for innovation to meet evolving application demands places a significant research and development burden on market players, necessitating substantial investment in new materials and manufacturing techniques.

Another significant hurdle is the intense competition from well-established traditional iron-core motor technologies, which often offer a more cost-effective solution for applications where the unique benefits of ironless motors (such as zero cogging or low inertia) are not strictly necessary. Convincing potential adopters to switch from conventional, proven motor designs to more expensive ironless alternatives requires robust demonstration of long-term total cost of ownership benefits and superior performance in specific, critical applications. This market education and justification process can slow down broader market adoption, particularly in industries with conservative technology adoption cycles. Furthermore, the limited availability of high-grade raw materials, such as rare earth magnets, can pose supply chain risks and price volatility, impacting overall production costs and market stability.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Technological Complexity and R&D Investment | -1.2% | Global | 2025-2033 |

| Intense Competition from Traditional Motor Technologies | -1.0% | Global, particularly industrial applications | 2025-2030 |

| Supply Chain Volatility for Key Raw Materials (e.g., Rare Earth Magnets) | -0.9% | Global, especially Asia Pacific | 2025-2033 |

| Integration Challenges with Existing Systems | -0.7% | Global, smaller enterprises | 2025-2029 |

| Lack of Standardization Across Different Applications | -0.5% | Global | 2025-2033 |

Ironless Motor Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the Ironless Motor Market, offering granular insights into its size, growth trends, competitive landscape, and future projections. The scope encompasses detailed segmentation by type, application, and end-use industry across key regional markets. It critically assesses the impact of emerging technologies, market drivers, restraints, opportunities, and challenges, providing a holistic view for strategic decision-making. The report is designed to assist stakeholders in understanding market dynamics, identifying growth avenues, and formulating effective business strategies within the rapidly evolving ironless motor sector.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 1.25 Billion |

| Market Forecast in 2033 | USD 2.89 Billion |

| Growth Rate | 10.8% |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Precision Motion Systems, Advanced Linear Drives, Global Servo Solutions, Robotic Motion Corp., DynoTech Motors, Electro Precision Systems, Zero Cogging Drives, Actuator Innovations, SmoothMotion Technologies, Hyperion Robotics, Integrated Motion Control, Infinite Dynamics, Elite Drives, Quantum Motors, NexGen Precision, Dynamic Controls Inc., Future Tech Motors, OmniDrive Solutions, Stellar Automation, Vectronic Systems |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Ironless Motor Market is comprehensively segmented to provide a detailed understanding of its diverse applications and technological categories. This segmentation enables a granular analysis of market dynamics, revealing specific growth pockets and demand trends across various industries and motor types. By dissecting the market along these lines, stakeholders can identify key areas for product development, strategic investment, and market penetration, ensuring that solutions are tailored to meet distinct industry requirements and technological specifications. This detailed view supports more precise forecasting and competitive positioning.

- By Type:

- Linear Ironless Motors: Primarily used for linear motion applications requiring high precision, speed, and zero cogging, such as in semiconductor manufacturing, flat panel displays, and metrology.

- Rotary Ironless Motors: Employed in applications demanding smooth, continuous rotary motion without torque ripple, common in medical imaging, robotics, and precision instruments.

- Voice Coil Motors (VCMs): Known for their fast response and high acceleration, often used in optical focusing, medical dosage, and scanning applications.

- By Application:

- Industrial Automation & Robotics: Includes robotic arms, assembly lines, automated guided vehicles (AGVs), and pick-and-place machines requiring high accuracy.

- Medical Devices: Covers surgical robots, diagnostic equipment, laboratory automation, and precision drug delivery systems.

- Semiconductor & Electronics: Essential for wafer handling, inspection equipment, and precision positioning stages in microelectronics manufacturing.

- Aerospace & Defense: Used in satellite systems, UAVs, flight simulators, and precise actuation systems.

- Packaging: Employed in high-speed, accurate packaging machinery.

- Printing: Utilized in precision inkjet printers and plotters.

- Optics & Photonics: Critical for camera auto-focus, laser scanning, and optical alignment systems.

- Others: Includes applications in textiles, material handling, and specialized consumer electronics.

- By End-Use Industry:

- Manufacturing: Encompasses various industrial processes and factory automation.

- Healthcare: Includes hospitals, clinics, and research laboratories utilizing medical devices.

- Automotive: Specific applications within vehicle manufacturing and some auxiliary vehicle systems.

- Consumer Electronics: Devices like cameras, smartphones, and wearable technology.

- Others: Cross-industry applications not falling under the primary categories.

Regional Highlights

- North America: This region is a significant market for ironless motors, driven by robust growth in the medical devices, aerospace, and advanced robotics sectors. The United States, in particular, leads in R&D and adoption of high-precision automation, fostering continuous innovation and demand. Canada and Mexico also contribute through manufacturing and specific industrial applications.

- Europe: Europe represents a mature market with a strong emphasis on industrial automation, precision manufacturing, and advanced healthcare technologies, particularly in Germany, Switzerland, and the Netherlands. The region's stringent quality standards and focus on energy efficiency further bolster the adoption of high-performance ironless motors.

- Asia Pacific (APAC): The APAC region is projected to be the fastest-growing market due to rapid industrialization, massive investments in smart factories, and the booming electronics and semiconductor industries in countries like China, Japan, South Korea, and Taiwan. India and Southeast Asian nations are also emerging as significant contributors to regional market expansion due to increasing manufacturing capabilities.

- Latin America: While smaller in market share, Latin America shows promising growth, primarily driven by increasing foreign investment in manufacturing and automation upgrades in countries like Brazil and Mexico. The adoption of advanced industrial solutions is gradually expanding, creating new opportunities for ironless motor deployment.

- Middle East and Africa (MEA): This region is an emerging market, with growth primarily influenced by diversification efforts in industrial sectors, investments in infrastructure, and developing healthcare facilities in countries like Saudi Arabia and UAE. The demand for precision motion control is nascent but expected to rise with ongoing economic development and technological adoption.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Ironless Motor Market.- Precision Motion Systems

- Advanced Linear Drives

- Global Servo Solutions

- Robotic Motion Corp.

- DynoTech Motors

- Electro Precision Systems

- Zero Cogging Drives

- Actuator Innovations

- SmoothMotion Technologies

- Hyperion Robotics

- Integrated Motion Control

- Infinite Dynamics

- Elite Drives

- Quantum Motors

- NexGen Precision

- Dynamic Controls Inc.

- Future Tech Motors

- OmniDrive Solutions

- Stellar Automation

- Vectronic Systems

Frequently Asked Questions

Analyze common user questions about the Ironless Motor market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is an ironless motor and how does it differ from traditional motors?

An ironless motor is a type of electric motor whose winding structure contains no iron core, meaning the coils are unsupported by a ferromagnetic material. This design eliminates cogging torque, eddy currents, and hysteresis losses, leading to extremely smooth motion, higher efficiency, and excellent dynamic response compared to traditional iron-core motors. They are typically lighter and more compact but can be more expensive to manufacture.

What are the primary applications of ironless motors?

Ironless motors are primarily used in applications demanding high precision, smooth motion, high acceleration, and minimal heat generation. Key applications include industrial automation and robotics, medical devices (e.g., surgical robots, diagnostic equipment), semiconductor manufacturing, optical systems, aerospace and defense, and high-end consumer electronics requiring compact, efficient motion solutions.

What are the key benefits of using ironless motors?

The key benefits of ironless motors include zero cogging (extremely smooth motion), high efficiency due to minimal iron losses, very low inertia for rapid acceleration and deceleration, quiet operation, and a compact, lightweight design. They also offer precise control, absence of magnetic attraction to the stator, and reduced heat generation, making them ideal for sensitive and high-performance applications.

What challenges are associated with ironless motor technology?

Despite their advantages, ironless motors face challenges such as higher manufacturing costs compared to traditional motors, potential susceptibility to demagnetization under extreme thermal or magnetic conditions, and complex heat dissipation in high-power applications. Additionally, their lower inherent stiffness can be a limitation for very high force applications, and integration into existing systems may require specialized engineering.

How is the ironless motor market expected to grow in the coming years?

The ironless motor market is projected to experience substantial growth, driven by increasing adoption in advanced automation, robotics, medical devices, and the semiconductor industry. Miniaturization trends and the rising demand for energy-efficient, high-precision motion solutions will further fuel this expansion. Asia Pacific is anticipated to lead growth due to its robust manufacturing sector and technological investments.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted