Ion Implanter Market

Ion Implanter Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_708384 | Last Updated : September 15, 2025 |

Format : ![]()

![]()

![]()

![]()

Ion Implanter Market Size

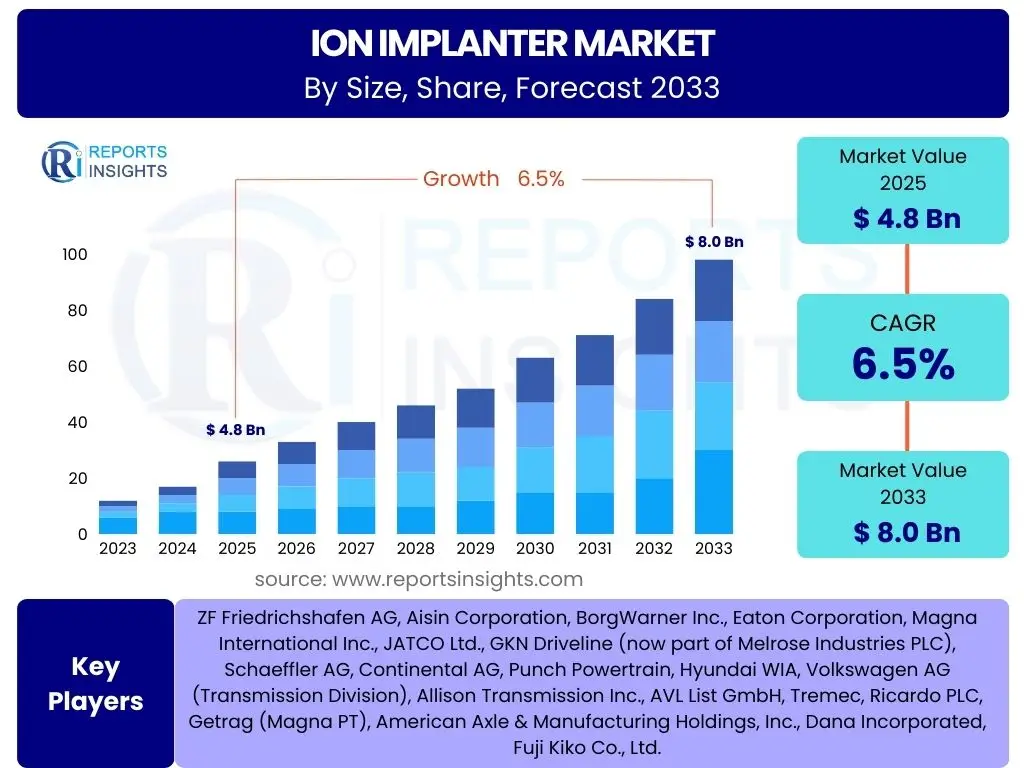

According to Reports Insights Consulting Pvt Ltd, The Ion Implanter Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.5% between 2025 and 2033. The market is estimated at USD 4.8 Billion in 2025 and is projected to reach USD 8.0 Billion by the end of the forecast period in 2033.

Key Ion Implanter Market Trends & Insights

User inquiries into the Ion Implanter market frequently highlight the escalating demand for advanced semiconductor devices, driven by the proliferation of artificial intelligence, 5G technology, and the Internet of Things (IoT). A key area of interest revolves around the continuous push for miniaturization and enhanced performance in integrated circuits, which directly necessitates more precise and efficient ion implantation techniques. Furthermore, there is significant attention on the development of novel materials and structures, such as wide-bandgap semiconductors like SiC and GaN, for which advanced ion implantation processes are critical for doping and device fabrication. Users are also keen to understand how geopolitical factors and regional initiatives influence manufacturing shifts and technological adoption within the global semiconductor supply chain.

The market is witnessing a strong trend towards higher energy and ultra-low energy implanters to meet diverse application requirements, from power devices to advanced logic and memory. There is also an increasing focus on process control and automation to improve yield and reduce operational costs. The integration of advanced diagnostics and real-time monitoring capabilities within ion implanter systems is becoming standard, ensuring greater precision and repeatability. Furthermore, the drive for sustainability within the semiconductor industry is influencing demand for energy-efficient implanters and processes that minimize material waste, reflecting a broader industry commitment to environmental responsibility.

- Increasing demand for advanced logic and memory chips.

- Rapid adoption of Wide Bandgap (WBG) semiconductors (SiC, GaN).

- Growing need for ultra-low energy and high-energy implantation.

- Emphasis on process control, automation, and real-time monitoring.

- Miniaturization and advanced packaging technologies.

- Expansion of implant applications beyond traditional silicon.

AI Impact Analysis on Ion Implanter

Common user questions regarding AI's impact on ion implanters often center on its potential to revolutionize process optimization, predictive maintenance, and overall manufacturing efficiency. Users are particularly interested in how AI algorithms can analyze vast datasets generated during implantation to fine-tune parameters, predict equipment failures before they occur, and enhance the consistency and yield of semiconductor fabrication. There is a strong expectation that AI will lead to smarter, more autonomous implanter systems capable of self-correction and continuous learning, thereby reducing human intervention and operational downtime. Furthermore, inquiries frequently touch upon AI's role in accelerating material science research and the development of new implantation recipes for emerging applications and novel materials, such as those used in quantum computing or advanced sensor technologies.

The application of AI in ion implanter technology extends beyond mere data analysis to truly transformative capabilities. Machine learning models are being deployed for advanced process control, allowing for real-time adjustments to dose, energy, and tilt angles to compensate for minor variations in wafer characteristics or environmental conditions, leading to significantly improved uniformity and device performance. AI-driven predictive maintenance systems analyze operational data from sensors across the implanter, identifying subtle anomalies that indicate impending component failure, thus enabling proactive servicing and minimizing costly unscheduled downtime. This not only enhances equipment reliability but also optimizes resource allocation and extends the operational lifespan of high-value components. The ultimate goal is to create highly intelligent manufacturing environments where ion implanters contribute to fully automated and self-optimizing semiconductor fabrication lines.

- Enhanced process optimization and control through machine learning.

- Predictive maintenance for reduced downtime and increased uptime.

- Automated anomaly detection and fault diagnosis in real-time.

- Improved yield management and quality control.

- Accelerated development of new implant recipes and material applications.

- Intelligent data analysis for deeper insights into implantation processes.

Key Takeaways Ion Implanter Market Size & Forecast

User queries about key takeaways from the Ion Implanter market size and forecast consistently highlight the robust growth trajectory driven by the insatiable demand for advanced electronics. A primary insight is the critical role of ion implantation as a foundational technology in semiconductor manufacturing, making its market performance a direct reflection of broader industry trends in computing, communication, and automotive sectors. Users often seek confirmation that the market is resilient to short-term fluctuations, demonstrating sustained growth powered by long-term technological shifts. Another significant takeaway is the increasing strategic importance of regional manufacturing hubs, especially in Asia-Pacific, which are not only driving demand but also fostering innovation in implanter technology. The market's future is inherently tied to continuous R&D investment and the capacity for rapid innovation in response to evolving device architectures and material requirements, ensuring its indispensable position in the semiconductor ecosystem.

The market's expansion is further underpinned by several distinct factors. The proliferation of IoT devices and the ongoing deployment of 5G infrastructure are creating substantial demand for integrated circuits that require precise doping and material modification, directly fueling the need for advanced ion implanters. Additionally, the automotive industry's pivot towards electric vehicles and autonomous driving necessitates a significant increase in power electronics and sensor technology, many of which rely on ion implantation for optimal performance, particularly in wide-bandgap materials. These applications, combined with the continuous evolution of consumer electronics and data centers, cement ion implanters as a vital component in the global technology landscape. The forecast underscores a period of sustained investment in fabrication capabilities worldwide, with a strong emphasis on achieving higher throughput, greater precision, and lower cost of ownership, all of which contribute to the market's positive outlook.

- Semiconductor industry growth is the primary driver for ion implanters.

- Significant investment in advanced fabrication facilities globally.

- High demand from AI, 5G, IoT, and automotive electronics sectors.

- Technological advancements in implanter capabilities are crucial for market expansion.

- Asia-Pacific maintains its dominant position in terms of demand and manufacturing.

- Continuous innovation in process control and new material applications expected.

Ion Implanter Market Drivers Analysis

The growth of the Ion Implanter market is primarily propelled by the exponential expansion of the global semiconductor industry. This growth is intrinsically linked to the escalating demand for high-performance computing, advanced connectivity (5G), and smart devices across various sectors, including consumer electronics, automotive, and industrial automation. As integrated circuits become more complex and dense, the need for precise and uniform doping, which ion implanters provide, becomes even more critical for achieving desired electrical characteristics and device reliability. The continuous innovation in chip design, leading to smaller feature sizes and more intricate 3D structures, directly necessitates advancements in ion implantation technology to meet stringent manufacturing specifications.

Furthermore, the emergence of new material systems and device architectures significantly drives market demand. Specifically, the rapid adoption of wide-bandgap semiconductors, such as Silicon Carbide (SiC) and Gallium Nitride (GaN), in power electronics and RF applications, creates a substantial market for specialized ion implanters capable of handling these materials effectively. These materials offer superior performance at higher temperatures and voltages, making them ideal for electric vehicles, renewable energy systems, and high-frequency communication. The ongoing research and development efforts in quantum computing, neuromorphic computing, and advanced sensor technologies also present new opportunities for ion implantation, pushing the boundaries of material modification and doping to enable future technological breakthroughs.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growth of Semiconductor Industry | +1.8% | Global (esp. APAC, North America) | 2025-2033 |

| Increasing Demand for Advanced ICs | +1.5% | Global | 2025-2033 |

| Miniaturization and Device Shrinkage | +1.2% | Global | 2025-2033 |

| Adoption of Wide-Bandgap Semiconductors | +0.9% | Global (esp. Asia, Europe) | 2025-2033 |

| Rise of AI, 5G, and IoT Technologies | +1.3% | Global | 2025-2033 |

Ion Implanter Market Restraints Analysis

Despite the robust growth, the Ion Implanter market faces several significant restraints that could temper its expansion. One primary challenge is the exceedingly high capital expenditure required for purchasing and maintaining these sophisticated machines. Ion implanters are among the most expensive pieces of equipment in a semiconductor fabrication plant, demanding substantial upfront investment, which can be a barrier for smaller players or new entrants. The operational costs, including specialized spare parts, consumables, and highly skilled labor for operation and maintenance, further add to the financial burden, potentially slowing down adoption rates in cost-sensitive regions or for specific applications.

Another critical restraint is the inherent technological complexity and rapid obsolescence cycles within the semiconductor industry. Ion implanters need to constantly evolve to keep pace with new device architectures, smaller process nodes, and novel materials, requiring continuous research and development investments. This rapid evolution means that existing equipment can quickly become outdated, necessitating frequent upgrades or replacements, which impacts profitability and investment returns for manufacturers and fabs alike. Furthermore, geopolitical tensions and trade restrictions can disrupt global supply chains for critical components and raw materials, leading to production delays and increased costs, creating significant market volatility and uncertainty. The ongoing talent shortage of highly specialized engineers and technicians required to operate and maintain these complex systems also poses a substantial hurdle, particularly in regions experiencing rapid expansion of manufacturing capabilities.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Capital & Operational Costs | -0.7% | Global | 2025-2033 |

| Technological Complexity & Obsolescence | -0.5% | Global | 2025-2033 |

| Geopolitical Tensions & Trade Barriers | -0.4% | Global (esp. Asia, North America, Europe) | 2025-2033 |

| Supply Chain Disruptions | -0.3% | Global | 2025-2033 |

| Shortage of Skilled Workforce | -0.2% | Global | 2025-2033 |

Ion Implanter Market Opportunities Analysis

The Ion Implanter market is poised to capitalize on several significant opportunities driven by emerging technological landscapes and strategic industry shifts. A prime opportunity lies in the burgeoning electric vehicle (EV) and autonomous driving sectors, which demand a substantial increase in power semiconductors and advanced sensor technologies. These applications heavily rely on ion implantation for precise doping of wide-bandgap materials like SiC and GaN, enabling higher efficiency and reliability in power conversion and management systems. As the automotive industry continues its rapid electrification, the demand for specialized ion implanters capable of processing these critical components will experience a significant uptick, opening new revenue streams for manufacturers.

Another compelling opportunity stems from the global expansion of fabrication capabilities, particularly in regions striving for semiconductor independence or resilience. Governments worldwide are investing heavily in establishing or expanding domestic semiconductor manufacturing facilities, creating a robust demand for new and advanced ion implanter systems. This includes initiatives in North America, Europe, and parts of Asia outside traditional manufacturing hubs. Furthermore, the relentless pace of innovation in advanced packaging technologies, such as 3D stacking and chiplets, offers avenues for ion implanters to play a role in inter-die connection and stress engineering. The ongoing research into novel materials for quantum computing, neuromorphic chips, and advanced displays also represents long-term growth opportunities, pushing the boundaries of existing implantation capabilities and fostering the development of next-generation implanter solutions. The push towards sustainable manufacturing also provides opportunities for implanter manufacturers to develop more energy-efficient and environmentally friendly systems, attracting customers who prioritize green fabrication processes.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Electric Vehicles & Automotive Electronics | +1.1% | Global (esp. Europe, North America, Asia) | 2025-2033 |

| Expansion of Global Fab Capacity | +1.0% | Global | 2025-2033 |

| Advanced Packaging Technologies | +0.8% | Global | 2025-2033 |

| Emerging Applications (Quantum Computing) | +0.6% | Global | 2028-2033 |

| Development of Sustainable Implantation Solutions | +0.4% | Global | 2025-2033 |

Ion Implanter Market Challenges Impact Analysis

The Ion Implanter market, while dynamic, faces several significant challenges that require continuous innovation and strategic adaptation. A primary challenge is the relentless pressure for higher precision and uniformity as semiconductor device geometries continue to shrink to atomic scales. Achieving consistent doping profiles across large wafers with extremely tight tolerances, especially for ultra-shallow junctions and complex 3D structures, pushes the limits of current implanter technology. Any deviation can lead to significant yield losses, making stringent process control and advanced metrology absolutely essential. The industry's rapid technological evolution means that maintaining a competitive edge requires substantial and ongoing investment in research and development to address these ever-increasing technical demands.

Another significant challenge is managing the complexities of diverse material processing. While silicon remains dominant, the increasing use of new materials like SiC, GaN, and various compounds for advanced applications presents unique implantation challenges, including potential material damage, activation issues, and contamination risks. Ion implanters must be versatile enough to handle a broad spectrum of ion species, energies, and doses while ensuring minimal damage to the substrate. Furthermore, ensuring intellectual property (IP) protection in a highly competitive and globally interconnected industry poses a constant challenge, particularly given the high value and strategic importance of semiconductor manufacturing equipment. Geopolitical factors also introduce uncertainty, potentially impacting market access, technology transfer, and supply chain stability, compelling companies to diversify manufacturing and R&D strategies to mitigate risks. Lastly, the environmental impact of manufacturing processes, including energy consumption and waste generation, presents an ongoing challenge, driving the need for more sustainable and efficient implanter designs.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Maintaining Precision & Uniformity for Advanced Nodes | -0.6% | Global | 2025-2033 |

| Handling Diverse & Novel Materials | -0.5% | Global | 2025-2033 |

| Rapid Technological Obsolescence & High R&D Costs | -0.4% | Global | 2025-2033 |

| Geopolitical Risks & Trade Barriers | -0.3% | Global | 2025-2033 |

| Environmental Compliance & Sustainability Pressure | -0.2% | Global | 2025-2033 |

Ion Implanter Market - Updated Report Scope

This report offers an updated and comprehensive analysis of the Ion Implanter market, providing detailed insights into its current size, growth drivers, restraints, opportunities, and challenges. It encompasses an in-depth examination of market trends, the impact of emerging technologies like Artificial Intelligence, and future projections across various segments and key regions. The scope includes a meticulous breakdown by implanter type, application, and end-use industry, designed to equip stakeholders with actionable intelligence for strategic decision-making and investment planning. The analysis covers the period from 2019 to 2033, with 2024 as the base year and forecasts extending through 2033.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 4.8 Billion |

| Market Forecast in 2033 | USD 8.0 Billion |

| Growth Rate | 6.5% |

| Number of Pages | 250 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Applied Materials Inc., Axcelis Technologies Inc., Sumitomo Heavy Industries Ion Technology Co. Ltd., Nissin Ion Equipment Co. Ltd., High Voltage Engineering Europa B.V. (HVE), Ulvac Inc., Intevac Inc., Kingstone Semiconductor Joint Stock Company Ltd., Advanced Ion Beam Technology Inc., PlasmaTherm LLC, Semilab Inc., KLA Corporation, Varian Semiconductor Equipment Associates (a business unit of Applied Materials), SEN Corporation, BeamReach Technology |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Ion Implanter market is segmented to provide a granular understanding of its diverse components and dynamics, reflecting the varied technological requirements and application landscapes. This comprehensive segmentation allows for a detailed analysis of market performance across different types of implanters, their specific applications in various industries, and the underlying technological approaches. Such a breakdown is crucial for identifying niche markets, understanding competitive landscapes within specific categories, and forecasting demand shifts driven by technological advancements or industry trends. Each segment represents a critical facet of the ion implantation ecosystem, collectively contributing to the overall market's growth and evolution.

Analyzing these segments offers strategic insights for market participants, enabling them to tailor product development, sales strategies, and market entry points effectively. For instance, the distinction between high-current and high-energy implanters highlights the different requirements for logic vs. power device fabrication, while the application-based segmentation reveals the growing importance of non-traditional semiconductor sectors like material science or displays. Understanding the end-use industries clarifies the impact of macro-economic trends and specific sector-driven demands. This detailed segmentation analysis is instrumental in uncovering key growth areas and potential challenges within the Ion Implanter market, providing a robust framework for strategic planning and competitive positioning.

- By Type: High Current Implanters, Medium Current Implanters, High Energy Implanters, Ultra Low Energy Implanters

- By Application: Semiconductor Manufacturing, Solar Cell Manufacturing, Material Science Research, Others (e.g., MEMS, Displays)

- By End-Use Industry: Electronics, Automotive, Healthcare, Aerospace & Defense, Industrial

- By Ion Source: Plasma Implanters, RF Implanters, Filament Implanters

Regional Highlights

- Asia Pacific (APAC) dominates the global Ion Implanter market, primarily driven by the presence of major semiconductor manufacturing hubs in countries like Taiwan, South Korea, China, and Japan. This region is witnessing significant investments in new fabrication plants and R&D, positioning it as a critical growth engine.

- North America holds a substantial market share, fueled by strong government initiatives to boost domestic semiconductor production, coupled with extensive research and development activities in advanced materials and computing technologies. The region's focus on innovation in AI, quantum computing, and high-performance computing drives demand for cutting-edge implanter solutions.

- Europe demonstrates steady growth, particularly in the automotive and industrial sectors, where demand for power electronics and specialty semiconductors is increasing. Investments in establishing a more resilient European semiconductor supply chain also contribute to market expansion.

- Latin America and the Middle East & Africa (MEA) are emerging markets, showing gradual adoption of semiconductor manufacturing technologies. While smaller in scale, increasing digitalization and industrialization efforts in these regions are expected to drive future demand, particularly for more accessible and versatile ion implantation solutions.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Ion Implanter Market.- Applied Materials Inc.

- Axcelis Technologies Inc.

- Sumitomo Heavy Industries Ion Technology Co. Ltd.

- Nissin Ion Equipment Co. Ltd.

- High Voltage Engineering Europa B.V. (HVE)

- Ulvac Inc.

- Intevac Inc.

- Kingstone Semiconductor Joint Stock Company Ltd.

- Advanced Ion Beam Technology Inc.

- PlasmaTherm LLC

- Semilab Inc.

- KLA Corporation

- Varian Semiconductor Equipment Associates (a business unit of Applied Materials)

- SEN Corporation

- BeamReach Technology

Frequently Asked Questions

Analyze common user questions about the Ion Implanter market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is an ion implanter and why is it important in semiconductor manufacturing?

An ion implanter is a crucial piece of equipment used in semiconductor manufacturing to introduce specific dopant impurities into a semiconductor material. This process, called ion implantation, precisely alters the electrical properties of the material, which is fundamental for creating transistors and other electronic components in integrated circuits. Its importance stems from its ability to achieve highly controlled doping profiles, essential for device performance and miniaturization.

What are the key types of ion implanters available in the market?

Key types of ion implanters include high current implanters, medium current implanters, high energy implanters, and ultra-low energy implanters. Each type is designed for specific applications, such as high current for mass production doping, high energy for deep implants like in power devices, and ultra-low energy for ultra-shallow junctions in advanced logic devices.

Which industries are the primary consumers of ion implanter technology?

The primary consumers of ion implanter technology are the semiconductor manufacturing industry, driven by demand from consumer electronics, automotive (especially electric vehicles), data centers, and telecommunications (5G). Other significant industries include solar cell manufacturing for doping photovoltaic materials, and material science research for modifying material properties.

What are the major factors driving the growth of the ion implanter market?

The major factors driving market growth include the increasing global demand for advanced integrated circuits, the continuous trend towards device miniaturization, the rapid adoption of wide-bandgap semiconductors (SiC, GaN), and the proliferation of emerging technologies such as AI, 5G, and IoT. Investments in new fabrication plants and R&D for novel materials also significantly contribute to growth.

What challenges does the ion implanter market face?

The ion implanter market faces challenges such as high capital and operational costs, the need for extreme precision and uniformity at advanced process nodes, the complexity of handling diverse and novel materials, and rapid technological obsolescence. Geopolitical factors affecting global supply chains and a shortage of skilled labor also pose significant hurdles.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted