Floating Production Storage and Offloading Market

Floating Production Storage and Offloading Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_701013 | Last Updated : July 29, 2025 |

Format : ![]()

![]()

![]()

![]()

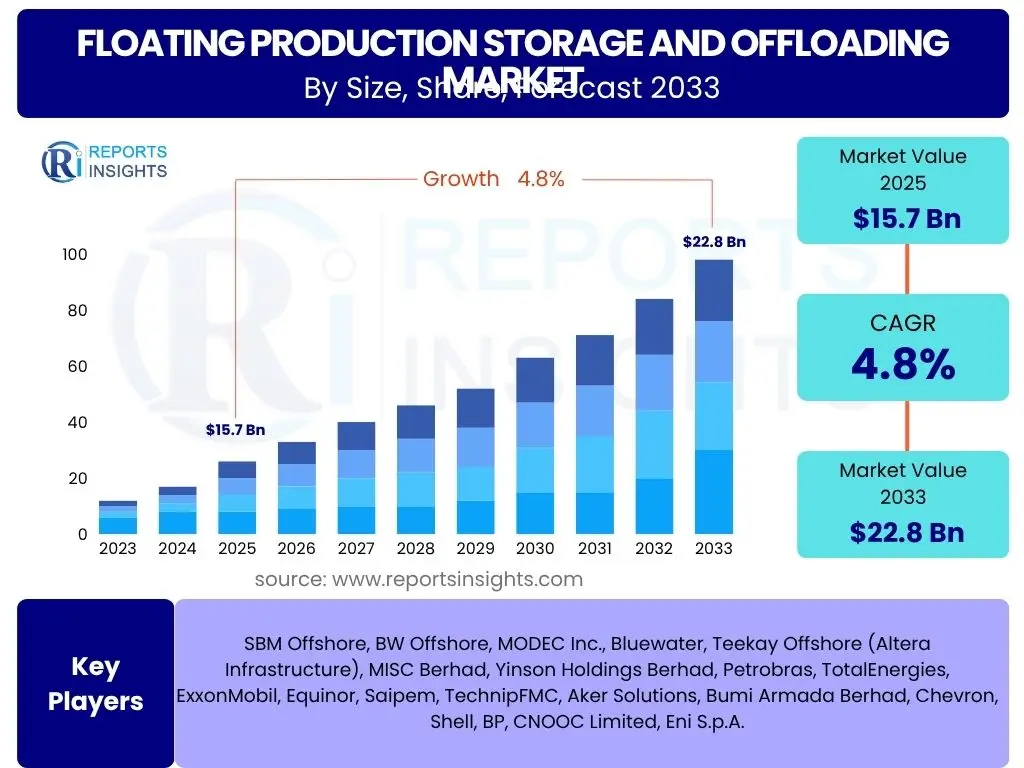

Floating Production Storage and Offloading Market Size

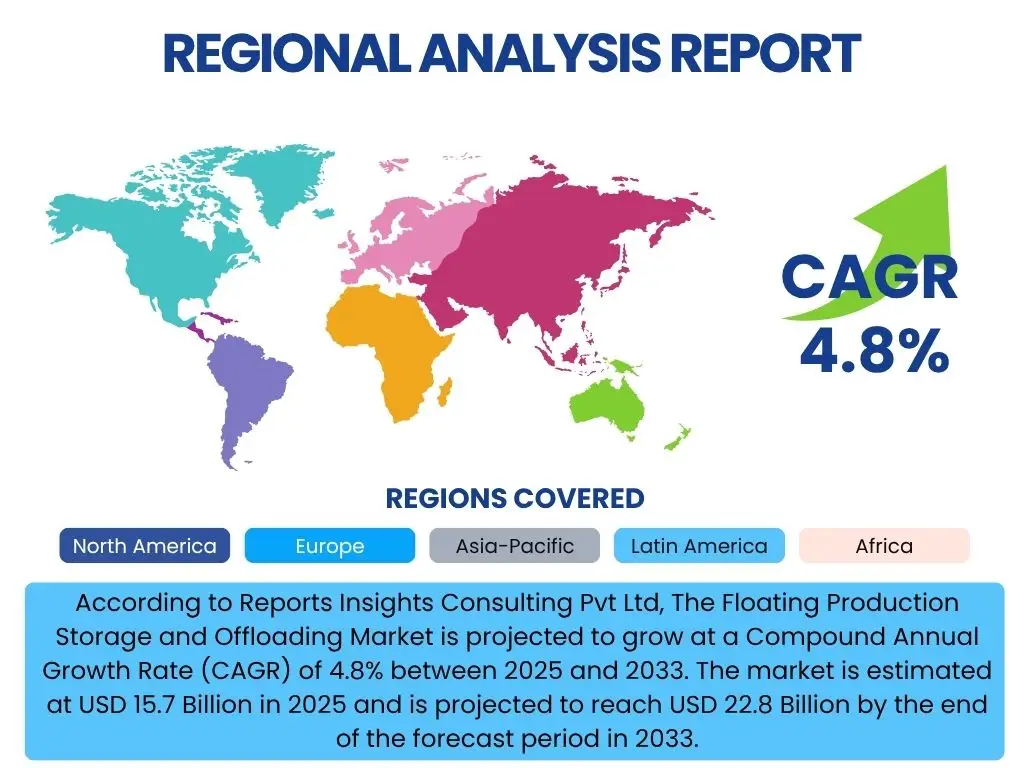

According to Reports Insights Consulting Pvt Ltd, The Floating Production Storage and Offloading Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 4.8% between 2025 and 2033. The market is estimated at USD 15.7 Billion in 2025 and is projected to reach USD 22.8 Billion by the end of the forecast period in 2033.

Key Floating Production Storage and Offloading Market Trends & Insights

The Floating Production Storage and Offloading (FPSO) market is undergoing significant transformation, driven by a confluence of factors including the global energy transition, advancements in offshore technology, and evolving regulatory landscapes. Users frequently inquire about how the industry balances the need for new hydrocarbon production with sustainability goals, the role of digitalization, and the geographic shifts in deepwater exploration. The market is witnessing a pivot towards more efficient, lower-emission operations and an increasing focus on gas monetization projects.

Technological innovation plays a pivotal role in shaping the market, with increasing adoption of remote monitoring, autonomous operations, and advanced data analytics to enhance efficiency and safety. Furthermore, the longevity of existing FPSO units and their potential for redeployment or conversion are key considerations for stakeholders. The industry is also grappling with the dual challenge of maximizing recovery from mature fields while simultaneously developing new frontier basins, necessitating flexible and adaptable FPSO solutions. This dynamic environment fosters a continuous drive for operational excellence and cost optimization across the lifecycle of FPSO assets.

- Emphasis on gas monetization projects and FLNG (Floating Liquefied Natural Gas) solutions.

- Increased deployment of redeployed or converted FPSOs for marginal field development.

- Technological integration of digital twins, AI, and remote operational capabilities.

- Growing focus on decarbonization and emission reduction technologies in FPSO operations.

- Development of standardized FPSO designs to reduce costs and accelerate deployment.

- Shift towards ultra-deepwater and harsh environment projects, particularly in pre-salt and frontier basins.

AI Impact Analysis on Floating Production Storage and Offloading

The integration of Artificial Intelligence (AI) within the Floating Production Storage and Offloading (FPSO) sector is a topic of considerable interest, with common user questions revolving around its potential to enhance operational efficiency, improve safety protocols, and optimize asset management. Stakeholders are keen to understand how AI can transform predictive maintenance, streamline complex processes, and enable more data-driven decision-making, ultimately leading to reduced downtime and operational costs. There is also a strong focus on the challenges associated with data integration from disparate systems and ensuring cybersecurity for AI-driven platforms.

AI's analytical capabilities are poised to revolutionize how FPSO operators monitor equipment health, predict potential failures, and schedule maintenance interventions with unprecedented precision. This shift from reactive to proactive maintenance minimizes operational disruptions and extends the lifespan of critical components. Furthermore, AI can optimize production processes by analyzing vast datasets related to reservoir performance, fluid dynamics, and environmental conditions, leading to improved hydrocarbon recovery rates and reduced energy consumption.

Beyond operational optimization, AI contributes significantly to enhancing safety on FPSO units through advanced anomaly detection, real-time monitoring of personnel, and automated response systems for emergencies. While the benefits are substantial, successful AI adoption requires robust data infrastructure, clear data governance policies, and a skilled workforce capable of developing, deploying, and managing AI solutions in complex offshore environments. Addressing these foundational elements will be crucial for realizing the full potential of AI in the FPSO market.

- Predictive Maintenance Optimization: AI algorithms analyze sensor data to predict equipment failures, reducing unplanned downtime and maintenance costs.

- Enhanced Operational Efficiency: AI optimizes production processes, energy consumption, and fluid management, leading to improved output and reduced emissions.

- Improved Safety and Risk Management: AI-powered surveillance and anomaly detection systems enhance safety protocols and emergency response.

- Data-Driven Decision Making: Advanced analytics from AI provides deeper insights into asset performance and market conditions for strategic planning.

- Remote Operations and Autonomy: AI facilitates increased automation and remote control of FPSO functions, improving operational flexibility and safety.

Key Takeaways Floating Production Storage and Offloading Market Size & Forecast

The Floating Production Storage and Offloading (FPSO) market is poised for steady expansion, driven by persistent global energy demand and strategic offshore investments. Key insights reveal that while traditional oil and gas projects continue to drive deployments, there is an increasing emphasis on gas monetization and projects with lower carbon footprints. Users frequently seek to understand the primary growth catalysts, the regional distribution of market activity, and the overarching opportunities that will define the market's trajectory over the forecast period. The market's resilience is underscored by ongoing exploration and development activities in deepwater and ultra-deepwater basins.

A significant takeaway is the strategic importance of flexibility and adaptability in FPSO designs, allowing for redeployment and customization to suit various field characteristics and regulatory environments. This approach helps mitigate risks associated with volatile commodity prices and long project lifecycles. Furthermore, the market is characterized by a drive towards integrating advanced digital technologies, which are critical for optimizing operations, enhancing safety, and improving overall asset performance. This technological adoption is not merely incremental but represents a fundamental shift in how FPSO projects are managed and executed, promising greater efficiency and sustainability.

- Steady Market Growth: The FPSO market is projected for consistent growth through 2033, driven by sustained offshore E&P.

- Deepwater Dominance: Deepwater and ultra-deepwater projects, particularly in Latin America and West Africa, remain key drivers for new FPSO deployments.

- Gas Monetization Focus: Increasing emphasis on natural gas and Floating LNG (FLNG) solutions to meet growing global energy demand and transition goals.

- Technological Integration: Digitalization, automation, and AI are crucial for operational efficiency, safety, and asset management in modern FPSOs.

- Sustainability Imperatives: Growing pressure for lower carbon emissions and environmentally responsible operations influences design and operational strategies.

Floating Production Storage and Offloading Market Drivers Analysis

The Floating Production Storage and Offloading (FPSO) market is significantly propelled by the continued global demand for energy, necessitating further exploration and production from offshore reserves. Deepwater and ultra-deepwater discoveries, often located in remote and challenging environments, increasingly rely on FPSO units due to their inherent flexibility, mobility, and ability to handle complex fluid compositions. These vessels provide a cost-effective and efficient solution for developing fields where fixed platforms are not economically or technically viable, particularly in regions with limited pipeline infrastructure.

Furthermore, advancements in subsea technology and drilling capabilities have opened up new frontiers for offshore development, making previously inaccessible hydrocarbon reservoirs commercially viable. The trend towards developing marginal and stranded fields also favors FPSO solutions, as they can be redeployed or customized for smaller reserves, thereby maximizing asset utilization and optimizing return on investment. The focus on gas monetization, including the development of Floating Liquefied Natural Gas (FLNG) and Floating Compressed Natural Gas (FCNG) facilities, is another strong driver, aligning with global energy transition efforts to reduce reliance on more carbon-intensive fuels.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Global Energy Demand and Offshore Exploration | +1.5% | Brazil, Guyana, Norway, West Africa, North Sea | 2025-2033 |

| Rise in Deepwater and Ultra-Deepwater Discoveries | +1.2% | Latin America, West Africa, Gulf of Mexico, Australia | 2025-2033 |

| Technological Advancements in Subsea and Drilling Technologies | +0.8% | Global, particularly advanced offshore basins | 2025-2033 |

| Growth in Marginal Field Development and Redeployment Strategies | +0.7% | Southeast Asia, North Sea, Gulf of Mexico | 2025-2030 |

| Focus on Gas Monetization and Floating LNG/CNG Projects | +0.6% | Australia, East Africa, North America | 2025-2033 |

Floating Production Storage and Offloading Market Restraints Analysis

The Floating Production Storage and Offloading (FPSO) market faces several significant restraints that could temper its growth trajectory. One primary concern is the inherent volatility of crude oil and natural gas prices. Prolonged periods of low commodity prices can lead to deferral or cancellation of new offshore projects, directly impacting demand for new FPSO units or conversions. The substantial capital expenditure required for FPSO projects, combined with long lead times, makes them highly sensitive to market fluctuations and investor confidence, often resulting in cautious investment decisions.

Additionally, stringent and evolving environmental regulations, particularly concerning emissions, flaring, and discharge, pose considerable challenges. While necessary for sustainability, these regulations often necessitate costly technological upgrades, operational modifications, and rigorous compliance measures, increasing the overall project cost and complexity. Geopolitical instability in key oil-producing regions can also disrupt supply chains, escalate operational risks, and deter investment, further restraining market expansion. The high operational costs associated with maintaining and operating FPSO units in harsh offshore environments, coupled with the need for specialized personnel, contribute to the economic hurdles.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Volatile Crude Oil and Natural Gas Prices | -1.0% | Global | Short to Medium Term |

| High Capital Expenditure and Long Project Lead Times | -0.8% | Global | 2025-2033 |

| Stringent Environmental Regulations and Emission Standards | -0.7% | Europe, North America, Brazil | 2025-2033 |

| Geopolitical Instability and Security Concerns in Offshore Regions | -0.5% | West Africa, Middle East, Southeast Asia | Short to Medium Term |

| Aging Infrastructure and Maintenance Challenges | -0.4% | North Sea, Gulf of Mexico, Mature Basins | 2025-2030 |

Floating Production Storage and Offloading Market Opportunities Analysis

The Floating Production Storage and Offloading (FPSO) market is ripe with opportunities driven by a convergence of technological innovation, evolving energy demands, and strategic re-evaluation of existing assets. A significant opportunity lies in the continued development of marginal and smaller offshore fields that were previously considered uneconomical. FPSOs, particularly those that can be redeployed or converted, offer a flexible and cost-effective solution for extracting value from these reserves, thereby extending the economic life of mature basins and unlocking new production possibilities.

The global shift towards natural gas as a cleaner transitional fuel presents a substantial opportunity for FLNG (Floating Liquefied Natural Gas) and FSRU (Floating Storage Regasification Unit) projects. These floating gas solutions enable the monetization of offshore gas reserves that lack pipeline infrastructure, particularly in emerging markets or remote locations. Furthermore, the increasing adoption of digital technologies, including Artificial Intelligence, Internet of Things (IoT), and digital twins, offers profound opportunities to optimize FPSO operations, enhance safety, reduce maintenance costs through predictive analytics, and improve overall asset performance and efficiency.

Lastly, the growing imperative for decarbonization within the oil and gas industry is creating opportunities for FPSO designs that integrate renewable energy sources (e.g., offshore wind power, solar PV), carbon capture and storage (CCS) technologies, and solutions aimed at reducing methane emissions and flaring. This trend aligns with environmental, social, and governance (ESG) goals, potentially attracting new investments and partnerships focused on sustainable offshore production practices. These strategic opportunities underscore the market's potential for innovation and diversification beyond conventional oil production.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development of Marginal and Small Offshore Fields | +0.9% | Southeast Asia, North Sea, West Africa | 2025-2033 |

| Increased Demand for Floating LNG (FLNG) and Gas Monetization | +1.0% | Australia, East Africa, North America, Southeast Asia | 2025-2033 |

| Integration of Digitalization, Automation, and AI Technologies | +0.7% | Global | 2025-2033 |

| Focus on Decarbonization and Lower Emission FPSO Solutions | +0.6% | Europe, North America, Brazil | 2027-2033 |

| Redeployment and Conversion of Existing FPSO Vessels | +0.5% | Global, especially mature basins | 2025-2030 |

Floating Production Storage and Offloading Market Challenges Impact Analysis

The Floating Production Storage and Offloading (FPSO) market, despite its growth prospects, faces a complex array of challenges that demand innovative solutions and strategic foresight. One significant hurdle is the escalating cost of compliance with increasingly stringent environmental regulations and safety standards. Adapting existing units and designing new ones to meet evolving emissions targets, flaring restrictions, and discharge limits often entails substantial capital outlays and operational adjustments, potentially impacting project economics and timelines.

Another critical challenge is managing the technical complexities inherent in ultra-deepwater and harsh environment operations. These environments present unique engineering, logistical, and operational demands, including extreme pressures, temperatures, and remote locations, which necessitate specialized equipment, advanced materials, and highly skilled personnel. Furthermore, maintaining the integrity and extending the lifespan of an aging FPSO fleet, particularly those operating beyond their original design life, introduces significant maintenance and integrity management complexities, coupled with the risk of unplanned downtime.

The industry also grapples with supply chain disruptions, which can lead to delays in project execution and increased costs for specialized components and services. The shortage of experienced technical talent, including engineers, operators, and maintenance specialists with offshore expertise, further exacerbates these issues, impacting project efficiency and safety. Successfully navigating these multifaceted challenges will require concerted efforts in technological innovation, workforce development, and collaborative industry partnerships to ensure sustainable and efficient FPSO operations.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Strict Environmental and Safety Regulations Compliance | -0.8% | Global, particularly developed regions | 2025-2033 |

| Technical Complexities of Deepwater and Harsh Environments | -0.7% | Latin America, Arctic Regions, West Africa | 2025-2033 |

| Aging Fleet and Asset Integrity Management | -0.6% | North Sea, Gulf of Mexico, Southeast Asia | 2025-2030 |

| Supply Chain Disruptions and Escalating Material Costs | -0.5% | Global | Short to Medium Term |

| Shortage of Skilled Workforce and Talent Acquisition | -0.4% | Global | 2025-2033 |

Floating Production Storage and Offloading Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the Floating Production Storage and Offloading (FPSO) market, offering a detailed assessment of its current status, historical performance, and future growth projections. The scope encompasses a thorough examination of market size, trends, drivers, restraints, opportunities, and challenges influencing the industry across various segments and key geographical regions. It also highlights the impact of emerging technologies like AI and digitalization, offering strategic insights for stakeholders to navigate the evolving market landscape.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 15.7 Billion |

| Market Forecast in 2033 | USD 22.8 Billion |

| Growth Rate | 4.8% |

| Number of Pages | 245 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | SBM Offshore, BW Offshore, MODEC Inc., Bluewater, Teekay Offshore (Altera Infrastructure), MISC Berhad, Yinson Holdings Berhad, Petrobras, TotalEnergies, ExxonMobil, Equinor, Saipem, TechnipFMC, Aker Solutions, Bumi Armada Berhad, Chevron, Shell, BP, CNOOC Limited, Eni S.p.A. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Floating Production Storage and Offloading (FPSO) market is comprehensively segmented to provide a granular understanding of its diverse components and dynamics. This segmentation allows for precise analysis of market trends, regional variations, and the specific technological or operational characteristics driving demand across different applications. By dissecting the market based on various criteria, stakeholders can identify niche opportunities, assess competitive landscapes, and formulate targeted strategies for market penetration and growth.

Each segment represents a unique dimension of the FPSO industry, from the fundamental distinction between new builds and converted units to the operational demands of different water depths and production capacities. The ownership model, whether contractor-owned or operator-owned, significantly influences investment patterns and project financing. Furthermore, the type of hull and mooring system employed dictates the FPSO's suitability for specific environmental conditions and operational requirements, such as harsh weather or disconnectable capabilities. This detailed segmentation is crucial for accurately forecasting market trajectories and understanding the interplay of technological advancements and operational efficiencies within each category, providing a holistic view of the FPSO value chain.

- By Type: This segment distinguishes between FPSO units that are newly constructed, those converted from existing tankers, and those redeployed from previous field operations. Each type has distinct cost structures, deployment timelines, and applicability.

- By Production Capacity: Categorization by the volume of hydrocarbons processed, typically divided into small, medium, and large capacities. This influences the scale of fields an FPSO can serve.

- By Water Depth: Segmentation based on the operational depth, including shallow water, deepwater, and ultra-deepwater. This impacts the complexity of subsea infrastructure and mooring systems.

- By Ownership: Differentiates between FPSOs owned and operated by contractors (leasing models), those held in joint ventures, and units directly owned by the oil and gas operators. This affects financial models and risk allocation.

- By Hull Type: Classified by the structural design of the vessel's body, such as traditional tanker hulls, ship-shaped hulls, or cylindrical hulls. Each offers unique stability and storage characteristics.

- By Mooring System: Divided by the method used to anchor the FPSO, including spread mooring, turret mooring (internal or external), tower mooring, and disconnectable mooring systems, crucial for harsh environments.

- By Application: This segment covers the primary use cases, including crude oil production, natural gas production, and the specific application in marginal field development, highlighting the flexibility of FPSOs.

Regional Highlights

- Latin America: This region is a dominant force in the FPSO market, primarily driven by Brazil's prolific pre-salt deepwater discoveries, Guyana's rapidly developing offshore basins, and ongoing exploration in other South American countries. Significant capital investments and long-term contracts for large-scale FPSO projects characterize this region.

- Africa: West Africa, particularly Angola, Nigeria, and Ghana, continues to be a key region for FPSO deployments due to substantial deepwater and ultra-deepwater oil and gas reserves. East Africa is emerging with significant natural gas discoveries, driving demand for FLNG solutions and associated FPSOs.

- North America: The Gulf of Mexico remains a mature but active basin for FPSO operations, driven by deepwater oil production. Canada's Atlantic offshore also contributes, focusing on harsh environment capabilities.

- Europe: The North Sea (Norway, UK) remains a significant market, with a focus on maximizing recovery from mature fields, decommissioning, and integrating decarbonization technologies into FPSO operations. New projects are highly scrutinized for environmental impact.

- Asia Pacific (APAC): This region is diverse, with activity in Australia (driven by large gas projects including FLNG), Malaysia, Indonesia, and Vietnam. The focus is on a mix of new developments, marginal field exploitation, and gas monetization.

- Middle East: While traditionally dominated by onshore and shallow-water fixed platforms, there is increasing interest in offshore field development, potentially leading to future FPSO opportunities in specific areas.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Floating Production Storage and Offloading Market.- SBM Offshore

- BW Offshore

- MODEC Inc.

- Bluewater

- Altera Infrastructure (formerly Teekay Offshore)

- MISC Berhad

- Yinson Holdings Berhad

- Saipem

- TechnipFMC

- Aker Solutions

- Bumi Armada Berhad

- Kongsberg Gruppen

- Siemens Energy

- Schlumberger Limited

- Baker Hughes Company

- Halliburton

- Petrobras

- TotalEnergies

- Equinor

- ExxonMobil

Frequently Asked Questions

What is the projected growth rate for the Floating Production Storage and Offloading market?

The Floating Production Storage and Offloading (FPSO) market is projected to grow at a Compound Annual Growth Rate (CAGR) of 4.8% between 2025 and 2033, reaching an estimated USD 22.8 Billion by 2033.

Which regions are leading the growth in the FPSO market?

Latin America, particularly Brazil and Guyana, along with West Africa, are key regions driving FPSO market growth due to significant deepwater discoveries and ongoing offshore development projects.

How are environmental regulations impacting the FPSO market?

Stringent environmental regulations are driving FPSO operators to adopt greener technologies, reduce emissions, and implement more sustainable operational practices, influencing new designs and costly upgrades to existing units.

What role does Artificial Intelligence (AI) play in FPSO operations?

AI is increasingly vital for optimizing FPSO operations through predictive maintenance, enhancing safety protocols, improving production efficiency, and enabling data-driven decision-making, leading to reduced downtime and operational costs.

What are the key opportunities in the FPSO market?

Key opportunities include the development of marginal offshore fields, growing demand for Floating LNG (FLNG) solutions, integration of digital technologies, and strategic focus on decarbonization efforts within FPSO operations.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted