Internal Olefin Market

Internal Olefin Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_703281 | Last Updated : August 01, 2025 |

Format : ![]()

![]()

![]()

![]()

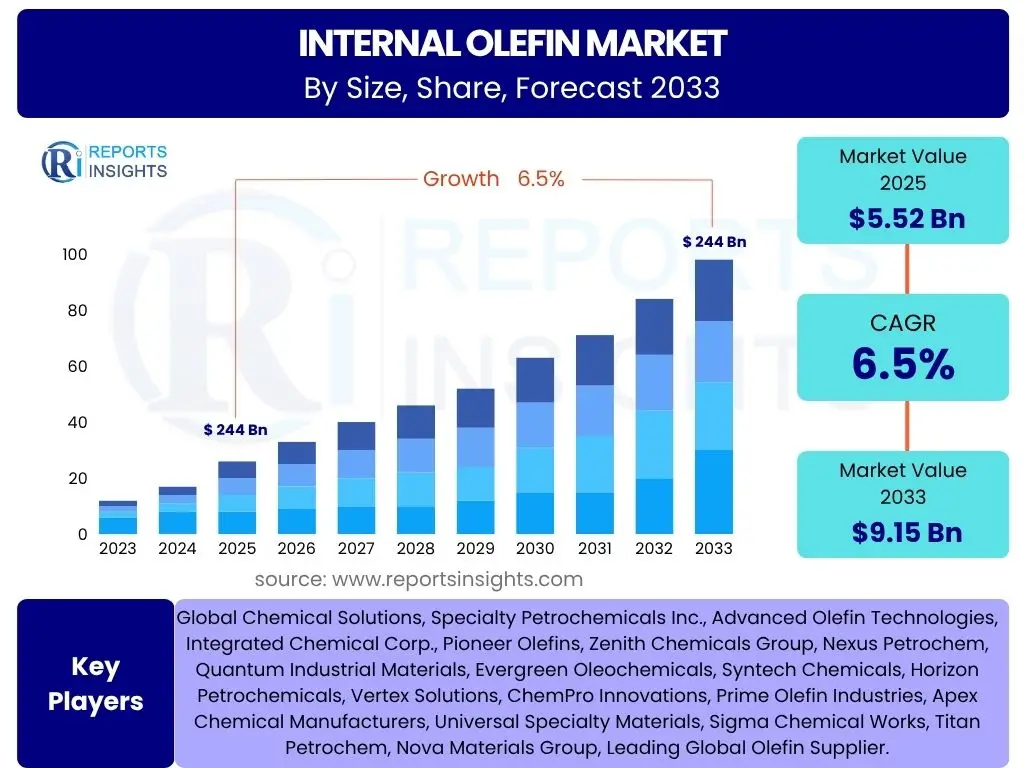

Internal Olefin Market Size

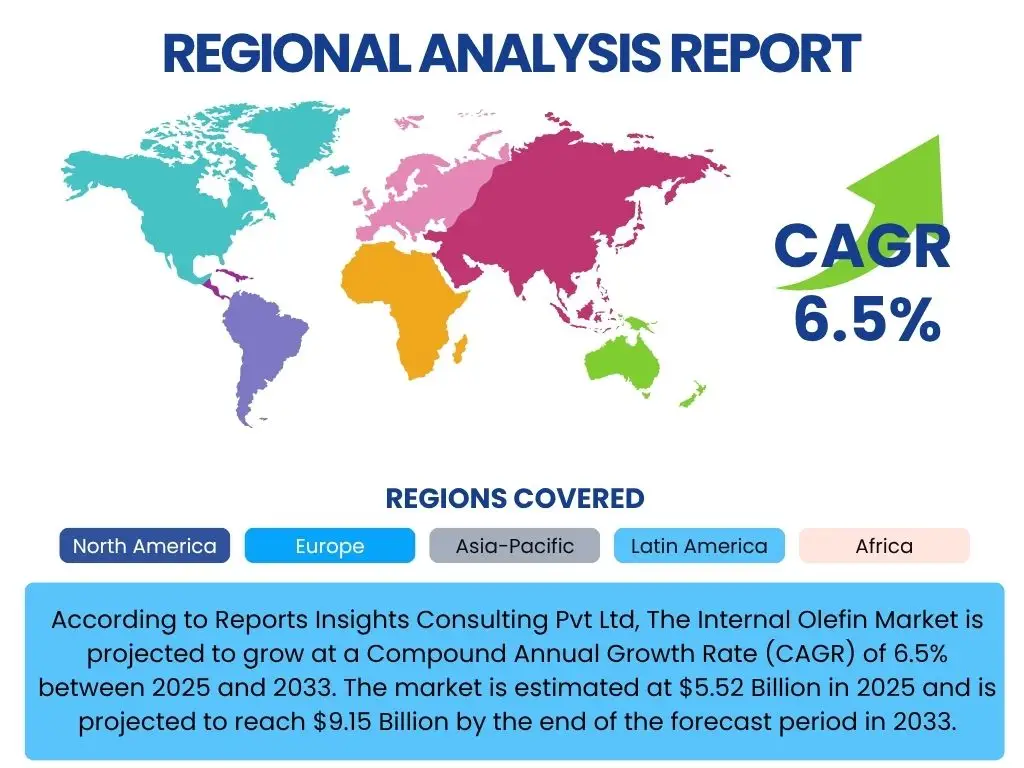

According to Reports Insights Consulting Pvt Ltd, The Internal Olefin Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.5% between 2025 and 2033. The market is estimated at $5.52 Billion in 2025 and is projected to reach $9.15 Billion by the end of the forecast period in 2033.

Key Internal Olefin Market Trends & Insights

The internal olefin market is currently experiencing dynamic shifts driven by evolving industrial demands and a heightened focus on sustainable solutions. A prominent trend involves the escalating adoption of internal olefins in specialized applications, particularly within the energy sector, where they enhance the efficiency of drilling fluids and lubricants. This trend is further supported by continuous innovation in product formulations that improve performance and broaden application scope across various industries, including detergents, plasticizers, and agricultural chemicals.

Another significant insight points towards the increasing emphasis on bio-based and sustainable internal olefins. As global environmental regulations tighten and consumer preferences shift towards eco-friendly products, manufacturers are investing heavily in research and development to produce internal olefins from renewable resources. This not only addresses environmental concerns but also offers a pathway to reduce dependency on fossil fuels, aligning with broader sustainability goals. The market is also witnessing a geographical expansion, with emerging economies in Asia Pacific and Latin America becoming pivotal growth hubs due to rapid industrialization and increasing infrastructure development.

- Growing demand from enhanced oil recovery (EOR) and drilling fluids sector.

- Increasing application in high-performance lubricants and synthetic oils.

- Rising adoption in specialty chemicals, including detergents, surfactants, and plasticizers.

- Shift towards bio-based and sustainable internal olefin production methods.

- Technological advancements leading to improved synthesis processes and product purity.

- Expansion of manufacturing capabilities in emerging Asian and Latin American markets.

AI Impact Analysis on Internal Olefin

The integration of Artificial Intelligence (AI) and machine learning technologies is poised to significantly transform the internal olefin market, primarily by optimizing production processes and enhancing supply chain efficiencies. Users frequently inquire about AI's potential to predict market demand fluctuations, streamline operational workflows, and improve the overall sustainability profile of chemical manufacturing. AI-driven predictive analytics can forecast raw material prices and demand for specific internal olefin grades, enabling producers to make more informed procurement and production decisions, thereby minimizing waste and reducing operational costs. This leads to more agile and responsive supply chains, capable of adapting quickly to market changes.

Furthermore, AI holds immense potential in accelerating research and development efforts for novel internal olefin applications and sustainable production pathways. Through advanced algorithms, AI can analyze vast datasets of chemical compounds, predict molecular interactions, and simulate reaction conditions, significantly shortening the time required for new product development and process optimization. This includes identifying greener catalysts, optimizing reaction parameters for higher yields, and developing new formulations for specialized industrial needs. The proactive monitoring and predictive maintenance capabilities of AI systems also ensure higher asset utilization and reduced downtime in manufacturing facilities, contributing to increased profitability and operational safety in the internal olefin sector.

- Predictive maintenance for internal olefin production facilities, minimizing downtime and optimizing equipment lifespan.

- Process optimization through AI algorithms to improve yield, energy efficiency, and product quality in synthesis.

- Demand forecasting and market trend analysis using AI, enabling more accurate production planning and inventory management.

- Supply chain optimization, enhancing logistics, reducing lead times, and improving raw material procurement efficiency.

- Accelerated research and development for new internal olefin applications and bio-based alternatives.

- Enhanced quality control and anomaly detection in product batches using machine vision and data analytics.

Key Takeaways Internal Olefin Market Size & Forecast

The internal olefin market is on a robust growth trajectory, driven by its indispensable role in high-performance industrial applications. A key takeaway from the market size and forecast analysis is the consistent demand stemming from the energy sector, particularly in enhanced oil recovery and drilling fluids, which continues to be a primary revenue generator. The market's resilience is further supported by diversified applications across lubricants, detergents, and specialty chemicals, cushioning it against fluctuations in any single end-use industry. This broad application base ensures a stable and expanding market landscape for internal olefins globally.

Another critical insight is the increasing strategic importance of sustainability and technological innovation in shaping future market dynamics. The forecast indicates that investments in bio-based solutions and advanced synthesis technologies will not only drive growth but also redefine competitive landscapes. Companies that prioritize eco-friendly production methods and continuous product improvement are poised to capture significant market share. Furthermore, the burgeoning industrialization in emerging economies, particularly within the Asia Pacific region, positions these areas as key contributors to market expansion, offering substantial opportunities for manufacturers and suppliers alike throughout the forecast period.

- The market exhibits strong growth potential, primarily fueled by expanding demand in the energy sector and diversified industrial applications.

- Enhanced Oil Recovery (EOR) and drilling fluids remain critical end-use segments driving significant market volume.

- Innovation in bio-based and sustainable production methods is becoming a pivotal factor for future market competitiveness.

- Asia Pacific is emerging as a high-growth region due to rapid industrial development and increasing chemical manufacturing activities.

- Investments in research and development for novel internal olefin applications are essential for long-term market sustainability and expansion.

Internal Olefin Market Drivers Analysis

The internal olefin market is propelled by a confluence of factors, primarily centered around the escalating demand from various industrial applications and continuous advancements in their utility. A significant driver is the robust growth in the energy sector, specifically the need for high-performance drilling fluids and enhanced oil recovery (EOR) agents, where internal olefins serve as crucial components for improving operational efficiency and yield. The ongoing global exploration and production activities, particularly in unconventional oil and gas reserves, directly translate into increased consumption of internal olefins.

Moreover, the versatility of internal olefins in the production of specialty chemicals, such as high-purity detergents, surfactants, and plasticizers, contributes substantially to market expansion. As consumer demand for high-performance cleaning agents and flexible plastic products continues to rise, so does the underlying need for internal olefins as key raw materials. Furthermore, the constant pursuit of efficiency and environmental compliance in industrial processes drives innovation in internal olefin formulations, leading to the development of products with superior performance characteristics and lower environmental impact, thus broadening their adoption across diverse industries.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing Demand from Enhanced Oil Recovery (EOR) & Drilling Fluids | +1.5% | North America, Middle East & Africa, Latin America | Short to Long Term |

| Increasing Application in Lubricants & Synthetic Oils | +1.2% | Global | Medium to Long Term |

| Rising Use in Detergents & Surfactants Production | +1.0% | Asia Pacific, Europe | Short to Medium Term |

| Technological Advancements in Olefin Synthesis | +0.8% | Global | Medium to Long Term |

| Expanding Chemical Manufacturing Industries in Emerging Economies | +0.9% | Asia Pacific, Latin America | Medium Term |

Internal Olefin Market Restraints Analysis

Despite robust growth prospects, the internal olefin market faces several significant restraints that could impede its expansion. One primary challenge is the volatility in crude oil prices, as crude oil derivatives serve as key feedstocks for internal olefin production. Fluctuations in these raw material costs directly impact production expenses and profit margins for manufacturers, leading to price instability in the end-product market and potentially affecting demand from price-sensitive applications. This dependency on fossil fuel prices introduces a degree of unpredictability into the market dynamics.

Furthermore, stringent environmental regulations worldwide pose a considerable restraint on market growth. Governments and regulatory bodies are increasingly implementing stricter norms regarding chemical emissions, waste disposal, and sustainable manufacturing practices, particularly in developed regions like North America and Europe. Compliance with these regulations often necessitates significant capital investment in advanced production technologies, waste treatment facilities, and certifications, which can increase operational costs and deter new market entrants. Additionally, the availability and competitive pricing of alternative chemicals or substitutes in certain applications could also limit the growth of the internal olefin market, forcing manufacturers to continually innovate to maintain their market position.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Volatile Raw Material Prices (Crude Oil Derivatives) | -1.3% | Global | Short to Medium Term |

| Stringent Environmental Regulations and Compliance Costs | -1.0% | Europe, North America | Medium to Long Term |

| Competition from Alternative Chemicals and Substitutes | -0.8% | Global | Medium Term |

| High Capital Investment for New Production Facilities | -0.7% | Global | Long Term |

Internal Olefin Market Opportunities Analysis

The internal olefin market is poised for significant growth through various emerging opportunities, primarily driven by innovation and expansion into untapped application areas. A key opportunity lies in the accelerating research and development of bio-based internal olefins derived from renewable resources. As industries worldwide pivot towards sustainable solutions, the ability to produce internal olefins from plant-based materials or other biomass offers a substantial competitive advantage, appealing to environmentally conscious consumers and meeting evolving regulatory requirements. This trend not only aligns with global sustainability goals but also diversifies feedstock sources, potentially reducing reliance on volatile fossil fuel markets.

Moreover, the expansion into emerging economies, particularly in Asia Pacific, Latin America, and parts of Africa, presents lucrative growth avenues. These regions are undergoing rapid industrialization, urbanization, and infrastructure development, leading to increased demand for chemicals across various sectors, including energy, construction, and consumer goods. Investing in local production capabilities and distribution networks within these regions can unlock significant market potential. Additionally, the continuous discovery of novel applications for internal olefins in niche and high-performance sectors, such as advanced materials, specialized lubricants, and next-generation additives, provides further opportunities for market participants to innovate and differentiate their product offerings, expanding their revenue streams beyond traditional applications.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development of Bio-based Internal Olefins | +1.8% | Global | Long Term |

| Expansion into Emerging Economies (e.g., APAC, Latin America) | +1.5% | Asia Pacific, Latin America, Middle East & Africa | Medium to Long Term |

| R&D for Novel and High-Performance Applications | +1.3% | Global | Medium to Long Term |

| Integration of Digitalization and AI in Value Chain Optimization | +0.9% | Global | Medium Term |

Internal Olefin Market Challenges Impact Analysis

The internal olefin market is not without its challenges, which can impact growth and profitability for market participants. One significant challenge pertains to managing complex global supply chains, especially in the face of geopolitical instability, trade disputes, or unforeseen events like pandemics. Disruptions in raw material supply, logistics bottlenecks, or sudden shifts in demand can lead to price volatility and production delays, directly affecting manufacturers' ability to meet market needs efficiently. Ensuring supply chain resilience and diversification becomes crucial to mitigate these risks.

Another pressing challenge involves waste management and the environmental impact associated with chemical production processes. As sustainability concerns intensify globally, companies face increasing pressure to adopt more eco-friendly manufacturing practices and reduce their carbon footprint. This often requires substantial investment in new technologies for waste reduction, recycling, and emission control, which can escalate operational costs. Furthermore, the need to scale up the production of sustainable and bio-based internal olefins while maintaining cost-effectiveness and performance parity with conventional products presents a significant technical and economic hurdle, requiring continuous innovation and substantial capital outlay in research and infrastructure.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Supply Chain Disruptions and Logistics Issues | -1.1% | Global | Short to Medium Term |

| Waste Management and Disposal Concerns | -0.9% | Global | Medium to Long Term |

| Difficulty in Scaling Up Sustainable Production Methods | -0.8% | Global | Long Term |

| Intensifying Price Competition | -0.7% | Global | Short Term |

Internal Olefin Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the global internal olefin market, offering valuable insights into its current state and future growth prospects. The report covers detailed market dynamics, including drivers, restraints, opportunities, and challenges, along with a thorough examination of market segmentation, regional landscapes, and competitive intelligence. It aims to empower stakeholders with the knowledge needed to make informed strategic decisions and capitalize on emerging market trends, ensuring a holistic understanding of the internal olefin industry from 2019 to 2033.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | $5.52 Billion |

| Market Forecast in 2033 | $9.15 Billion |

| Growth Rate | 6.5% |

| Number of Pages | 250 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Global Chemical Solutions, Specialty Petrochemicals Inc., Advanced Olefin Technologies, Integrated Chemical Corp., Pioneer Olefins, Zenith Chemicals Group, Nexus Petrochem, Quantum Industrial Materials, Evergreen Oleochemicals, Syntech Chemicals, Horizon Petrochemicals, Vertex Solutions, ChemPro Innovations, Prime Olefin Industries, Apex Chemical Manufacturers, Universal Specialty Materials, Sigma Chemical Works, Titan Petrochem, Nova Materials Group, Leading Global Olefin Supplier. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The internal olefin market is meticulously segmented to provide a granular understanding of its diverse components, allowing for targeted analysis of supply and demand dynamics across various product types, applications, and grades. This segmentation enables stakeholders to identify specific growth pockets, assess competitive landscapes within niche areas, and tailor business strategies effectively. By breaking down the market into its constituent parts, the report offers a comprehensive view of how different factors influence distinct segments, highlighting areas of high potential and those facing particular challenges.

The segmentation by type categorizes internal olefins based on their carbon chain length, reflecting their varied chemical properties and suitability for different industrial processes. Application-based segmentation illuminates the diverse end-use industries driving demand, from energy and automotive to consumer goods. Furthermore, the categorization by grade helps distinguish between internal olefins used as high-purity co-monomers in polymerization processes versus those employed as specialty chemicals for their functional properties. This detailed segmentation is crucial for understanding the intricate interdependencies within the market and for forecasting future trends with greater accuracy.

- By Type

- 1-Decene

- 1-Dodecene

- C16-C18 Internal Olefins

- C20-C24 Internal Olefins

- Other Higher Internal Olefins (e.g., C26+)

- By Application

- Enhanced Oil Recovery (EOR) & Drilling Fluids

- Lubricants & Additives

- Detergents & Surfactants

- Plasticizers

- Paper Chemicals

- Agricultural Chemicals

- Other Industrial Applications

- By Grade

- Polymer Grade

- Co-monomer Grade

- Specialty Chemical Grade

Regional Highlights

- North America: This region represents a mature and significant market for internal olefins, primarily driven by extensive enhanced oil recovery (EOR) and drilling activities within the oil and gas sector, particularly in the United States. Demand for high-performance lubricants and specialty chemicals also contributes substantially. Stringent environmental regulations necessitate advanced product formulations and sustainable manufacturing practices, fostering innovation in the region.

- Europe: Characterized by a strong emphasis on sustainability and stringent environmental regulations, Europe is a key market for specialty internal olefin applications, particularly in detergents, plasticizers, and industrial lubricants. The region's focus on green chemistry and circular economy principles drives the adoption of bio-based and environmentally friendly internal olefin solutions.

- Asia Pacific (APAC): Expected to be the fastest-growing market, driven by rapid industrialization, increasing energy demand, and expanding chemical manufacturing bases in countries like China, India, Japan, and South Korea. Investments in infrastructure development, rising disposable incomes, and the growth of end-use industries such as automotive, construction, and consumer goods are fueling significant demand for internal olefins across various applications.

- Latin America: This region offers considerable growth potential, largely due to ongoing oil and gas exploration projects, especially in countries like Brazil and Mexico, which boost demand for internal olefins in drilling fluids and EOR. Economic development and increasing industrial output also contribute to the rising consumption of internal olefins in various industrial and consumer applications.

- Middle East & Africa (MEA): Dominated by robust oil and gas activities, the MEA region is a substantial consumer of internal olefins for drilling and EOR applications. Significant investments in petrochemical industries and diversification efforts across various sectors in countries like Saudi Arabia and UAE are expected to drive sustained demand for internal olefins and their derivatives.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Internal Olefin Market.- Global Chemical Solutions

- Specialty Petrochemicals Inc.

- Advanced Olefin Technologies

- Integrated Chemical Corp.

- Pioneer Olefins

- Zenith Chemicals Group

- Nexus Petrochem

- Quantum Industrial Materials

- Evergreen Oleochemicals

- Syntech Chemicals

- Horizon Petrochemicals

- Vertex Solutions

- ChemPro Innovations

- Prime Olefin Industries

- Apex Chemical Manufacturers

- Universal Specialty Materials

- Sigma Chemical Works

- Titan Petrochem

- Nova Materials Group

- Leading Global Olefin Supplier

Frequently Asked Questions

What are internal olefins primarily used for?

Internal olefins are primarily used in enhanced oil recovery (EOR) and drilling fluids within the oil and gas industry. They are also critical components in manufacturing high-performance lubricants, synthetic oils, detergents, surfactants, plasticizers, and various specialty chemicals due to their unique properties.

How is the internal olefin market segmented?

The internal olefin market is segmented by type (e.g., 1-Decene, 1-Dodecene, C16-C18, C20-C24, Other Higher Internal Olefins), by application (e.g., EOR & Drilling Fluids, Lubricants & Additives, Detergents & Surfactants, Plasticizers), and by grade (e.g., Polymer Grade, Co-monomer Grade, Specialty Chemical Grade).

What are the main growth drivers for the internal olefin market?

Key growth drivers include increasing demand from the global oil and gas sector for EOR and drilling fluids, rising adoption in high-performance lubricants and detergents, and the expansion of chemical manufacturing industries, particularly in emerging economies.

What role does sustainability play in the internal olefin market?

Sustainability is playing an increasingly vital role, driving the development of bio-based internal olefins from renewable resources and the adoption of greener manufacturing processes to reduce environmental impact and meet stringent regulatory requirements.

Which region is expected to lead internal olefin market growth?

The Asia Pacific (APAC) region is expected to lead internal olefin market growth due to rapid industrialization, expanding manufacturing bases, significant investments in infrastructure, and rising demand from diverse end-use industries across countries like China and India.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted