Graphite Felt Market

Graphite Felt Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_710304 | Last Updated : January 02, 2026 |

Format : ![]()

![]()

![]()

![]()

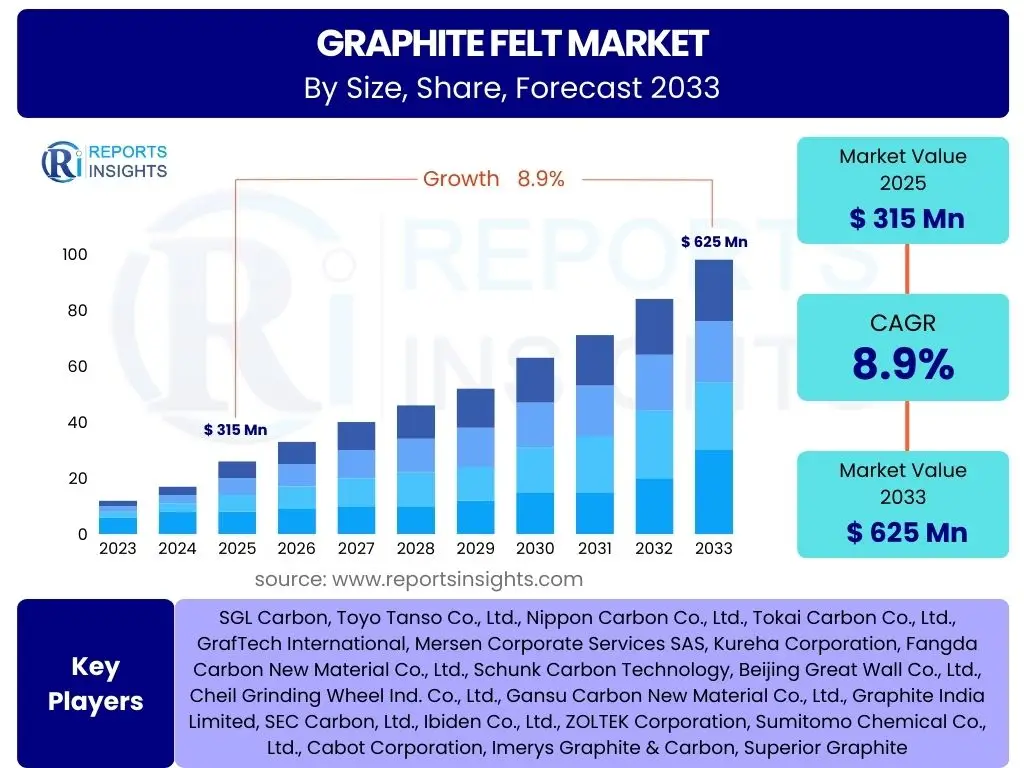

Graphite Felt Market Size

According to Reports Insights Consulting Pvt Ltd, The Graphite Felt Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 8.9% between 2025 and 2033. The market is estimated at USD 315 Million in 2025 and is projected to reach USD 625 Million by the end of the forecast period in 2033.

Key Graphite Felt Market Trends & Insights

The graphite felt market is experiencing significant transformation driven by advancements in energy storage technologies, particularly in redox flow batteries and hydrogen fuel cells. Users frequently inquire about emerging applications and the technological innovations propelling demand. The overarching trend indicates a shift towards high-purity, custom-engineered graphite felt solutions to meet the stringent requirements of these cutting-edge applications. Emphasis on sustainability and circular economy principles is also influencing product development, with manufacturers exploring greener production methods and recyclable materials.

Furthermore, the demand from traditional high-temperature industrial applications, such as vacuum furnaces and inert gas furnaces, remains robust, necessitating graphite felt with superior thermal stability and durability. The aerospace and defense sectors are increasingly adopting lightweight, high-performance materials, further diversifying the application landscape. Market participants are focusing on vertical integration and strategic partnerships to secure raw material supplies and enhance technological capabilities, ensuring resilience against supply chain volatilities and fostering innovation in product design and functionality.

- Energy Storage Expansion: Rapid growth in redox flow batteries and hydrogen fuel cells drives demand for high-performance graphite felt.

- Advanced Material Development: Focus on high-purity, functionalized, and engineered graphite felt for specific application requirements.

- Sustainability Focus: Increasing adoption of eco-friendly manufacturing processes and emphasis on recyclable materials.

- High-Temperature Industrial Demand: Continued strong demand from vacuum furnaces, sintering furnaces, and other high-temperature applications.

- Electrification Impact: Growing use in electric vehicle (EV) battery production infrastructure and charging solutions.

- Customization and Specialization: Shift towards tailored solutions for niche and high-value applications.

- Supply Chain Optimization: Efforts to enhance resilience and transparency in the raw material supply chain.

AI Impact Analysis on Graphite Felt

Users are increasingly curious about how artificial intelligence (AI) will revolutionize the graphite felt industry, particularly concerning manufacturing efficiency, material innovation, and supply chain management. AI is poised to significantly optimize production processes by enabling predictive maintenance, reducing downtime, and improving resource utilization. Through advanced algorithms, AI can analyze vast datasets from manufacturing operations, identifying patterns and anomalies that lead to enhanced quality control and cost reductions.

Beyond process optimization, AI is instrumental in accelerating material discovery and design. Machine learning models can predict the properties of novel graphite felt compositions, guiding research and development efforts and significantly shortening the time-to-market for new products with superior characteristics. Furthermore, AI-driven analytics are transforming supply chain logistics, offering predictive insights into demand fluctuations, inventory management, and potential disruptions, thereby enhancing the overall efficiency and resilience of the graphite felt value chain from raw material sourcing to final product delivery.

- Manufacturing Process Optimization: AI-driven analytics for real-time monitoring, predictive maintenance, and efficiency improvements in production lines.

- Predictive Quality Control: Machine learning algorithms enhance quality assurance by identifying defects early and optimizing material consistency.

- Accelerated Material Discovery: AI models predict properties of new graphite felt compositions, speeding up R&D and innovation cycles.

- Enhanced Supply Chain Management: AI-powered forecasting and logistics optimization improve inventory management and mitigate supply chain risks.

- Market Demand Forecasting: Advanced analytics provide precise predictions of market demand, enabling better production planning and resource allocation.

- Energy Efficiency Improvement: AI algorithms optimize energy consumption in manufacturing processes, reducing operational costs and environmental impact.

- Automation in Production: AI integration facilitates greater automation, leading to higher throughput and reduced human error.

Key Takeaways Graphite Felt Market Size & Forecast

Analysis of user inquiries concerning market size and forecast reveals a predominant interest in the drivers underpinning the projected growth and the segments expected to exhibit the most robust expansion. The market's strong growth trajectory is primarily attributed to the burgeoning demand for advanced energy storage solutions, particularly in the realm of redox flow batteries and hydrogen fuel cells, which critically rely on graphite felt for their electrode components. This segment is anticipated to be a pivotal growth engine, reflecting global efforts towards decarbonization and sustainable energy transitions.

Beyond energy storage, the consistent requirement for high-temperature insulation in industrial furnaces and thermal processing applications ensures a stable, albeit mature, demand segment. Geographically, Asia Pacific is projected to lead the market, driven by its expansive manufacturing base for electronics, electric vehicles, and renewable energy components. The forecast underscores the importance of strategic investments in research and development to capitalize on evolving technological requirements and to foster strategic partnerships that can navigate the complexities of raw material sourcing and market competition.

- Strong Growth Trajectory: The market is poised for substantial growth, driven by increasing applications in diverse high-tech industries.

- Energy Storage Dominance: Redox flow batteries and hydrogen fuel cells represent the most significant growth catalysts for graphite felt.

- High-Temperature Resilience: Sustained demand from industrial furnaces and thermal processing applications ensures market stability.

- Asia Pacific Leadership: The region is expected to remain the largest and fastest-growing market due to robust industrialization and energy initiatives.

- Strategic Partnerships Essential: Collaboration across the value chain is critical for innovation, supply chain stability, and market penetration.

- Technological Advancements: Continuous innovation in material properties and manufacturing processes is crucial for competitive advantage.

- Sustainability as a Driver: Increasing focus on green technologies and environmentally friendly production methods will shape future market dynamics.

Graphite Felt Market Drivers Analysis

The graphite felt market is significantly propelled by several key factors, chief among them being the escalating global demand for advanced energy storage systems. As the world transitions towards renewable energy sources and electric mobility, the necessity for efficient and durable battery and fuel cell components, where graphite felt plays a critical role, continues to grow. This surge is observed in both stationary energy storage projects and the expanding electric vehicle (EV) sector, underscoring the material's importance in the energy revolution.

Beyond energy, the material's exceptional thermal properties make it indispensable in high-temperature industrial applications, including vacuum furnaces, inert gas furnaces, and various thermal processing equipment. The aerospace and defense industries also contribute substantially to market growth, requiring lightweight, high-performance thermal insulation and structural components. Furthermore, the semiconductor manufacturing sector, with its demand for high-purity and stable materials, increasingly integrates graphite felt into its production processes, further diversifying and strengthening the market's demand base.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing Demand for Energy Storage (Redox Flow Batteries, Fuel Cells) | +2.5% | Global, particularly Asia Pacific (China, Japan, South Korea), North America, Europe | Medium to Long Term (2025-2033) |

| Expansion of High-Temperature Industrial Furnaces and Thermal Processing | +1.8% | Global, especially China, India, Germany, USA | Medium to Long Term (2025-2033) |

| Increasing Adoption in Aerospace and Defense Applications for Lightweighting and Thermal Management | +1.5% | North America, Europe, select Asia Pacific countries (e.g., Japan, South Korea) | Medium to Long Term (2025-2033) |

| Rising Demand from Semiconductor Manufacturing for High-Purity Materials | +1.0% | Asia Pacific (Taiwan, South Korea, Japan), North America (USA), Europe | Short to Medium Term (2025-2029) |

| Technological Advancements in Graphite Felt Production and Performance | +0.8% | Global | Medium to Long Term (2025-2033) |

Graphite Felt Market Restraints Analysis

Despite its robust growth prospects, the graphite felt market faces several significant restraints that could impede its expansion. One primary challenge is the high manufacturing cost associated with producing high-quality graphite felt, especially the high-purity variants required for advanced applications. The complex graphitization processes and the need for specialized equipment contribute significantly to these costs, making the final product relatively expensive compared to alternative materials.

Furthermore, the market is susceptible to the volatility of raw material prices, particularly for precursors like polyacrylonitrile (PAN) fiber or pitch. Fluctuations in these commodity prices can directly impact production costs and profit margins for manufacturers, leading to pricing instability in the market. Competition from alternative materials, such as ceramic fibers, metal foils, and other carbon-based insulation products, also poses a restraint, particularly in applications where the unique properties of graphite felt are not strictly essential or cost-effectiveness is a primary concern. The limited availability of specialized manufacturing expertise and stringent quality control requirements also act as barriers to entry for new players, concentrating market power among established producers.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Manufacturing Costs and Capital-Intensive Production Processes | -1.2% | Global | Medium to Long Term (2025-2033) |

| Volatility in Raw Material Prices (e.g., PAN Fiber, Pitch) | -1.0% | Global | Short to Medium Term (2025-2029) |

| Competition from Alternative Insulation Materials (Ceramic Fiber, Metal Foils) | -0.8% | Global, especially cost-sensitive markets | Medium Term (2025-2030) |

| Complex and Energy-Intensive Graphitization Process | -0.7% | Global | Medium to Long Term (2025-2033) |

| Environmental Regulations on Production Processes | -0.5% | Europe, North America, select Asia Pacific countries | Long Term (2029-2033) |

Graphite Felt Market Opportunities Analysis

Significant opportunities abound for the graphite felt market, primarily driven by the burgeoning demand for innovative energy solutions. The global push towards a hydrogen economy, coupled with advancements in fuel cell technology, presents a substantial growth avenue, as graphite felt is a critical component for gas diffusion layers and flow field plates. Similarly, the rapid development and deployment of redox flow batteries for grid-scale energy storage and renewable energy integration are opening up expansive new markets for high-performance graphite felt materials, offering long-duration storage capabilities.

Moreover, the increasing focus on lightweighting and advanced thermal management in critical industries like aerospace, defense, and high-performance automotive continues to generate demand for specialized graphite felt products. Niche applications in medical technology, such as biocompatible implants and advanced filtration systems, also offer promising, high-value opportunities. Furthermore, ongoing research and development into novel precursor materials and surface modification techniques are creating avenues for enhanced material properties, expanding the applicability and performance envelope of graphite felt in new and existing markets, solidifying its role as an advanced engineering material.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing Demand for Redox Flow Batteries and Hydrogen Fuel Cells | +2.8% | Global, particularly China, USA, Germany, Japan | Long Term (2028-2033) |

| Expansion into Niche Aerospace and Defense Applications (High-Performance Composites) | +1.5% | North America, Europe | Medium to Long Term (2025-2033) |

| Development of Advanced Materials with Enhanced Properties (e.g., Surface Modification, Hybrid Felts) | +1.2% | Global, driven by R&D hubs | Medium to Long Term (2025-2033) |

| Increasing Demand for High-Purity Graphite Felt in Semiconductor and Electronics Industries | +1.0% | Asia Pacific (Taiwan, South Korea), North America | Short to Medium Term (2025-2029) |

| Emerging Applications in Medical Technology and Environmental Filtration | +0.8% | North America, Europe, Japan | Long Term (2029-2033) |

Graphite Felt Market Challenges Impact Analysis

The graphite felt market faces several critical challenges that demand strategic responses from industry players. One significant hurdle is the vulnerability of the global supply chain for precursor materials, primarily PAN fiber and pitch, which are often subject to geopolitical tensions, trade disputes, and natural disasters. Such disruptions can lead to material shortages, price spikes, and production delays, directly impacting manufacturing schedules and profitability. Ensuring a stable and diversified supply chain remains a paramount concern for manufacturers.

Furthermore, the complex technical barriers associated with developing new, high-performance graphite felt products for cutting-edge applications, such as advanced fuel cells or extreme-temperature environments, represent another considerable challenge. Extensive research and development, coupled with significant capital investment, are required to overcome these hurdles. The market also contends with intense competition from established alternative materials and the emergence of new, potentially disruptive technologies, compelling manufacturers to continually innovate and differentiate their offerings. Regulatory hurdles, particularly concerning environmental compliance and material certification in diverse global markets, add another layer of complexity to market entry and expansion.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Supply Chain Vulnerabilities and Raw Material Dependency | -1.5% | Global | Short to Medium Term (2025-2029) |

| High Technical Barriers and R&D Costs for Advanced Applications | -1.0% | Global, particularly for innovative players | Medium to Long Term (2025-2033) |

| Intense Competition from Substitute Materials and Established Players | -0.9% | Global | Medium Term (2025-2030) |

| Stringent Regulatory Landscape and Certification Requirements | -0.7% | Europe, North America, Japan | Long Term (2029-2033) |

| Waste Management and Recycling Challenges for Used Graphite Felt | -0.6% | Global, especially in developed economies | Long Term (2029-2033) |

Graphite Felt Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the global graphite felt market, encompassing historical data, current market conditions, and future projections. It offers a detailed examination of market size, growth drivers, restraints, opportunities, and challenges across various segments and key geographical regions. The scope of the report includes a thorough understanding of the competitive landscape, profiling key market players, and analyzing their strategies to maintain market leadership. This analysis is designed to empower stakeholders with critical insights for strategic decision-making and sustainable growth within the dynamic graphite felt industry.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 315 Million |

| Market Forecast in 2033 | USD 625 Million |

| Growth Rate | 8.9% |

| Number of Pages | 245 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | SGL Carbon, Toyo Tanso Co., Ltd., Nippon Carbon Co., Ltd., Tokai Carbon Co., Ltd., GrafTech International, Mersen Corporate Services SAS, Kureha Corporation, Fangda Carbon New Material Co., Ltd., Schunk Carbon Technology, Beijing Great Wall Co., Ltd., Cheil Grinding Wheel Ind. Co., Ltd., Gansu Carbon New Material Co., Ltd., Graphite India Limited, SEC Carbon, Ltd., Ibiden Co., Ltd., ZOLTEK Corporation, Sumitomo Chemical Co., Ltd., Cabot Corporation, Imerys Graphite & Carbon, Superior Graphite |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The graphite felt market is meticulously segmented to provide a granular understanding of its diverse applications and material compositions. This comprehensive segmentation allows for a detailed examination of demand drivers and growth opportunities within specific product types, raw material sources, and end-use industries. Such an approach is critical for identifying high-growth niches and formulating targeted market strategies, reflecting the varied performance requirements and regulatory landscapes across different applications. By analyzing each segment, stakeholders can gain insights into material preferences, technological advancements, and regional consumption patterns, which are essential for product development and market expansion efforts.

- By Type: This segment differentiates between Flexible Graphite Felt, which includes both Carbon Felt and Graphite Felt, and Rigid Graphite Felt. Flexible felts are widely used for their conformability in various insulation and electrode applications, while rigid felts offer structural integrity in demanding high-temperature environments.

- By Raw Material: Categorization by raw material highlights the different precursors used in manufacturing, primarily PAN-based (polyacrylonitrile), Pitch-based, and Rayon-based graphite felts. Each precursor imparts unique properties to the final product, influencing its performance and cost-effectiveness for specific applications.

- By Application: This crucial segment delineates the primary uses of graphite felt, including Energy Storage (e.g., Redox Flow Batteries, Fuel Cells, Li-ion Batteries), High-Temperature Furnaces (e.g., Vacuum Furnaces, Inert Gas Furnaces, Sintering Furnaces), Chemical Processing, Aerospace & Defense, Semiconductor Manufacturing, Medical Technology, and other emerging applications.

- By End-Use Industry: The market is further segmented by the industries that consume graphite felt products, such as Automotive (e.g., EV components), Aerospace & Defense, Industrial (e.g., metallurgy, ceramics), Electronics & Semiconductors, Energy & Power (e.g., solar, nuclear), Chemical, Medical, and Research & Development. This provides insight into sector-specific demand.

- By Purity: Segmentation by purity level includes High Purity and Standard Purity graphite felt. High-purity variants are essential for sensitive applications like semiconductor manufacturing and advanced energy storage to prevent contamination, whereas standard purity suffices for less stringent industrial insulation.

- By Density: This segment classifies graphite felt by its density, encompassing Low Density, Medium Density, and High Density. Density significantly impacts thermal conductivity, mechanical strength, and electrical properties, allowing for tailored solutions based on application requirements.

Regional Highlights

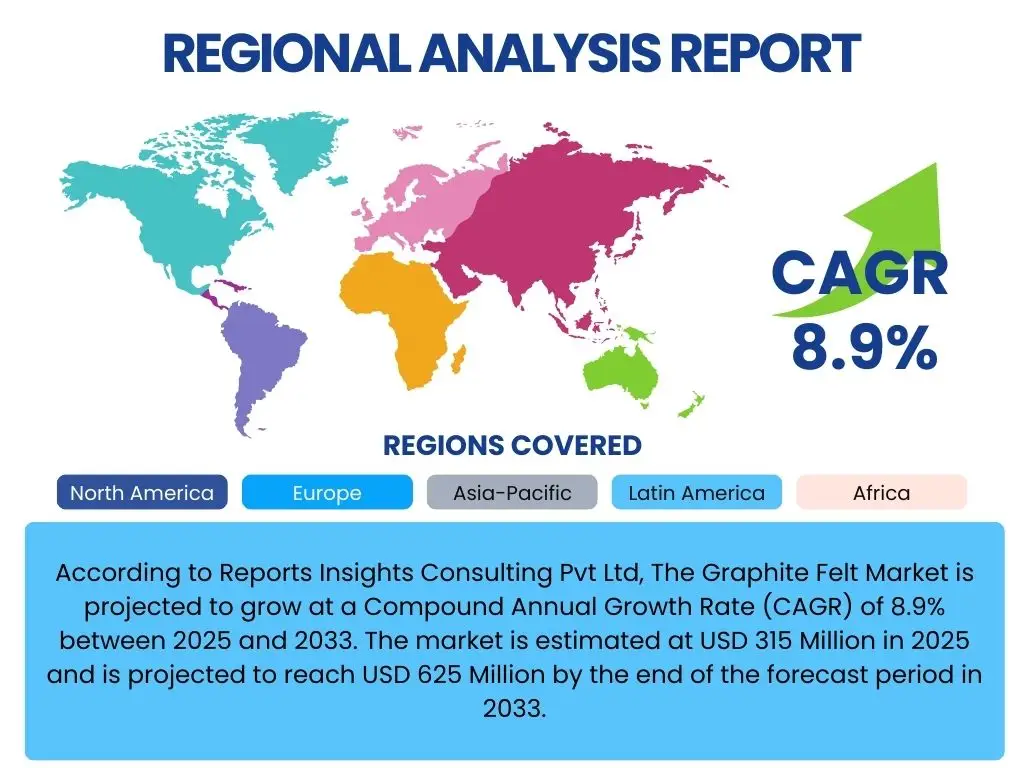

The global graphite felt market exhibits distinct regional dynamics driven by varying industrial landscapes, technological adoption rates, and governmental policies. Asia Pacific consistently emerges as the leading region, primarily due to its robust manufacturing base, particularly in electronics, electric vehicles (EVs), and renewable energy infrastructure. Countries like China, Japan, and South Korea are at the forefront of battery and fuel cell production, driving immense demand for graphite felt components. Furthermore, rapid industrialization and increasing investments in high-temperature processing across the region fuel its market dominance.

North America and Europe represent mature yet significantly innovative markets. North America’s demand is characterized by advanced applications in aerospace, defense, and semiconductor manufacturing, alongside growing investments in grid-scale energy storage and hydrogen technologies. Europe, with its strong emphasis on sustainability and circular economy, sees high adoption in fuel cells and advanced thermal insulation for industrial furnaces, further bolstered by stringent environmental regulations encouraging high-efficiency materials. Latin America, the Middle East, and Africa are nascent but promising markets, with gradual adoption rates as industrial development and energy transition initiatives gain momentum, presenting long-term growth opportunities.

- Asia Pacific: Expected to dominate the market due to extensive manufacturing capabilities in electronics, automotive (EVs), and renewable energy sectors, particularly in China, Japan, and South Korea. Rapid industrialization and investments in energy storage systems are key drivers.

- North America: A significant market driven by advanced applications in aerospace, defense, and semiconductors. Strong R&D activities and increasing adoption of hydrogen fuel cell technology contribute to steady growth.

- Europe: Characterized by a strong focus on sustainable energy solutions, high-temperature industrial processes, and stringent environmental regulations. Demand is robust from fuel cell development, vacuum furnaces, and specialized industrial applications.

- Latin America: Emerging market with growing industrialization and increasing investments in renewable energy infrastructure, offering long-term growth potential.

- Middle East and Africa (MEA): Gradually developing market with potential for growth in industrial applications, particularly in oil and gas and nascent renewable energy projects.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Graphite Felt Market.- SGL Carbon

- Toyo Tanso Co., Ltd.

- Nippon Carbon Co., Ltd.

- Tokai Carbon Co., Ltd.

- GrafTech International

- Mersen Corporate Services SAS

- Kureha Corporation

- Fangda Carbon New Material Co., Ltd.

- Schunk Carbon Technology

- Beijing Great Wall Co., Ltd.

- Cheil Grinding Wheel Ind. Co., Ltd.

- Gansu Carbon New Material Co., Ltd.

- Graphite India Limited

- SEC Carbon, Ltd.

- Ibiden Co., Ltd.

- ZOLTEK Corporation (a Toray Group Company)

- Sumitomo Chemical Co., Ltd.

- Cabot Corporation

- Imerys Graphite & Carbon

- Superior Graphite

Frequently Asked Questions

What is graphite felt used for?

Graphite felt is primarily used as a high-temperature insulation material in vacuum and inert gas furnaces due to its excellent thermal stability. It also serves as electrode material in advanced energy storage systems, notably redox flow batteries and hydrogen fuel cells, owing to its high electrical conductivity and chemical inertness.

What are the main types of graphite felt available?

The main types of graphite felt are flexible graphite felt and rigid graphite felt. Flexible graphite felt includes both carbon felt (carbonized but not fully graphitized) and pure graphite felt, offering pliability. Rigid graphite felt, conversely, provides structural integrity and is often used in furnace linings where mechanical strength is critical.

What are the key advantages of using graphite felt?

Graphite felt offers several advantages, including exceptional thermal insulation properties at very high temperatures, high electrical conductivity, excellent chemical inertness, low density, and high purity. These properties make it ideal for demanding applications in energy, aerospace, and high-temperature industrial processes.

How is graphite felt manufactured?

Graphite felt is typically manufactured from precursor fibers like polyacrylonitrile (PAN), pitch, or rayon. These fibers are first felted into a non-woven fabric, then subjected to carbonization (heating in an inert atmosphere to remove non-carbon elements) and subsequently graphitization (further heating to extremely high temperatures, up to 3000°C) to achieve a highly crystalline graphite structure.

What is the market outlook for graphite felt?

The graphite felt market is projected to experience robust growth, driven primarily by the escalating demand for energy storage solutions, including redox flow batteries and hydrogen fuel cells. Continued strong demand from high-temperature industrial furnaces and expanding applications in aerospace and semiconductor manufacturing also contribute to a positive long-term outlook.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted