InGaA PIN Photodiode Market

InGaA PIN Photodiode Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_705177 | Last Updated : August 11, 2025 |

Format : ![]()

![]()

![]()

![]()

InGaA PIN Photodiode Market Size

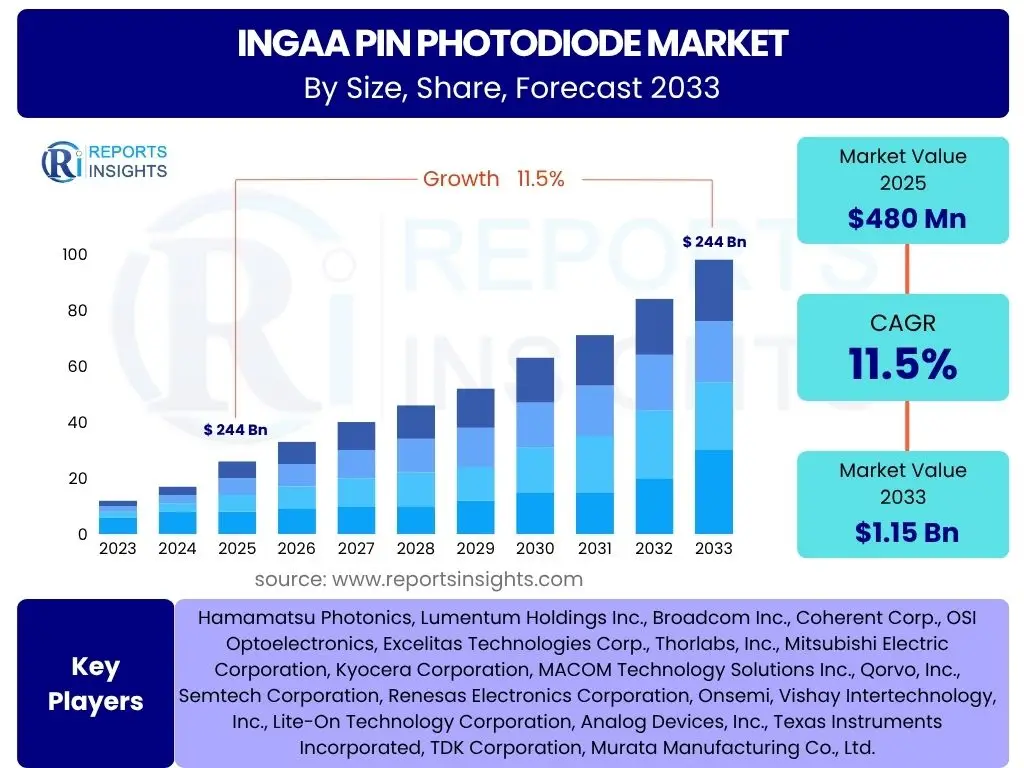

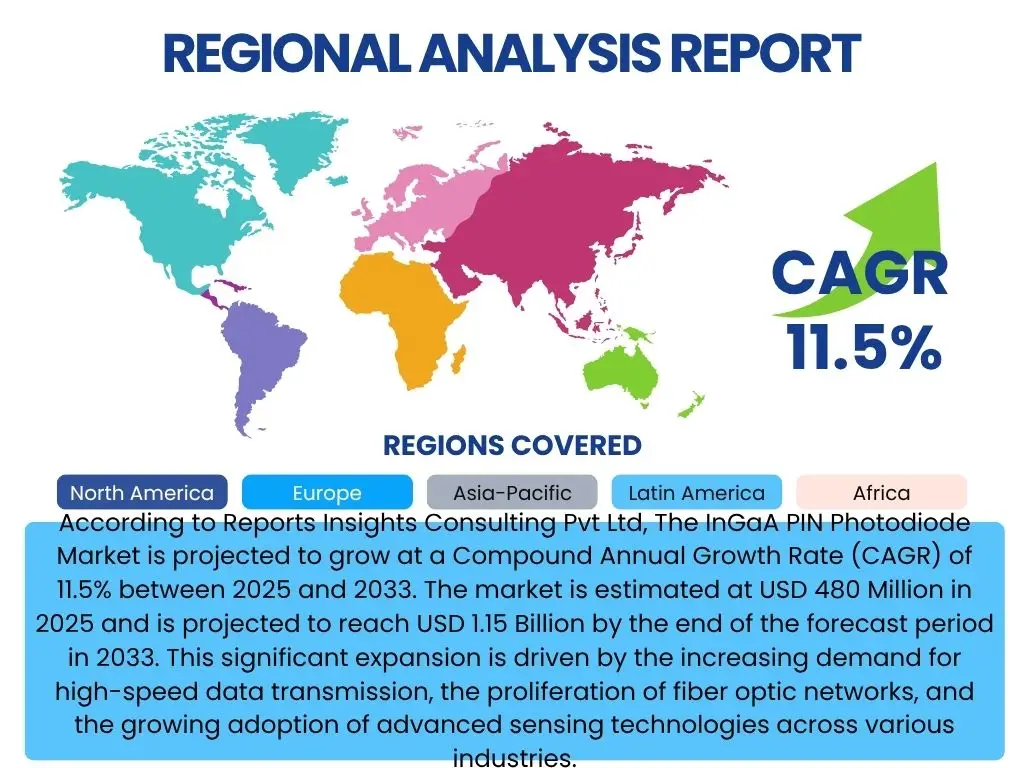

According to Reports Insights Consulting Pvt Ltd, The InGaA PIN Photodiode Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 11.5% between 2025 and 2033. The market is estimated at USD 480 Million in 2025 and is projected to reach USD 1.15 Billion by the end of the forecast period in 2033. This significant expansion is driven by the increasing demand for high-speed data transmission, the proliferation of fiber optic networks, and the growing adoption of advanced sensing technologies across various industries.

The market's robust growth trajectory reflects its critical role in modern communication infrastructure and emerging technological applications. InGaA PIN photodiodes are integral components in optical receivers, ensuring efficient conversion of optical signals into electrical signals with high sensitivity and reliability. Their superior performance characteristics, such as low noise, high responsivity, and broad spectral response, make them indispensable for next-generation telecommunications and data center operations.

Key InGaA PIN Photodiode Market Trends & Insights

The InGaA PIN Photodiode market is undergoing dynamic shifts driven by technological advancements and evolving application requirements. Current trends indicate a strong emphasis on miniaturization and integration, catering to the demand for compact and high-performance optical modules. Furthermore, the expansion of high-speed communication standards, such as 5G and beyond, is pushing the boundaries for photodiode performance, necessitating devices with higher bandwidth and lower power consumption. The market is also seeing increased adoption in non-traditional sectors like automotive LiDAR and medical imaging, diversifying its application landscape beyond conventional telecom uses.

Another significant insight points to the continuous innovation in material science and manufacturing processes, leading to enhanced device reliability and reduced production costs. This focus on efficiency and performance optimization is crucial for widespread adoption and market penetration. As data traffic continues its exponential growth, the demand for more robust and efficient optical components will intensify, solidifying the market's long-term growth prospects. These trends collectively shape the competitive landscape and technological roadmap for InGaA PIN photodiode manufacturers.

- Miniaturization and integration of photodiodes into compact modules for enhanced device density.

- Increased demand for high-speed (100G, 400G, 800G) and ultra-high-speed (terabit) optical communication systems.

- Growing adoption in automotive LiDAR systems for autonomous driving and advanced driver-assistance systems (ADAS).

- Expansion into new applications such as medical imaging, industrial sensing, and quantum computing.

- Development of photodiodes with enhanced responsivity, lower dark current, and broader spectral range.

- Emphasis on silicon photonics integration to reduce costs and improve performance for optical transceivers.

AI Impact Analysis on InGaA PIN Photodiode

Artificial intelligence (AI) is exerting a transformative impact on the InGaA PIN Photodiode market, primarily by driving the demand for high-performance data infrastructure that relies heavily on advanced optical components. AI and machine learning algorithms require vast amounts of data processing and transmission, leading to an increased need for high-bandwidth and low-latency communication networks. InGaA PIN photodiodes, with their superior speed and efficiency in converting optical signals, are fundamental to these AI-driven data centers and interconnected networks. The proliferation of AI applications, from cloud computing to edge AI, directly translates into a surging demand for these critical components, propelling market growth.

Beyond driving demand, AI is also influencing the design and manufacturing of InGaA PIN photodiodes. AI-driven optimization techniques are being employed to refine material composition, device structures, and fabrication processes, leading to improved performance characteristics and reduced production costs. Furthermore, AI's role in predictive maintenance and quality control within manufacturing facilities enhances the reliability and lifespan of these photodiodes. The integration of AI in optical networks also necessitates sophisticated monitoring and management systems that leverage data from photodiodes, creating a symbiotic relationship where AI both consumes and contributes to the advancement of optical technology.

- Increased demand for high-speed optical communication infrastructure to support AI data processing.

- AI-driven optimization in the design and manufacturing of photodiodes for improved performance and efficiency.

- Expansion of AI applications in autonomous vehicles and robotics boosting demand for LiDAR-specific photodiodes.

- Development of AI-powered sensor fusion systems integrating InGaA PIN photodiodes for enhanced data acquisition.

- The need for ultra-low latency and high-bandwidth networks for AI model training and inference.

Key Takeaways InGaA PIN Photodiode Market Size & Forecast

The InGaA PIN Photodiode market is poised for substantial expansion, with a significant compound annual growth rate projected through 2033, indicating a highly optimistic outlook for stakeholders. The primary drivers for this growth are rooted in the ever-increasing demand for high-speed data communication across various industries, including telecommunications, data centers, and consumer electronics. Emerging applications in automotive LiDAR and advanced medical imaging are also contributing substantially to market diversification and expansion beyond traditional optical networking. This multifaceted demand ensures sustained market momentum and innovation in photodiode technology.

Furthermore, technological advancements in material science and manufacturing processes are enhancing the performance and cost-effectiveness of these photodiodes, making them more accessible for a wider range of applications. The market's resilience is further supported by ongoing investments in fiber optic infrastructure globally, reinforcing the foundational role of InGaA PIN photodiodes in future communication paradigms. Companies investing in research and development for improved spectral response, higher data rates, and integration capabilities are strategically positioned to capitalize on these evolving market dynamics.

- Robust growth trajectory driven by surging demand for high-speed data communication.

- Emerging applications in automotive LiDAR and medical imaging diversifying market revenue streams.

- Technological advancements leading to improved performance and cost efficiency.

- Significant investments in global fiber optic infrastructure providing a strong foundation for market expansion.

- The critical role of InGaA PIN photodiodes in enabling next-generation communication and sensing technologies.

InGaA PIN Photodiode Market Drivers Analysis

The InGaA PIN photodiode market is significantly propelled by the escalating global demand for high-speed data transmission, primarily stemming from the rapid expansion of fiber optic networks and data centers. The proliferation of cloud computing, streaming services, and online gaming necessitates robust and efficient optical communication infrastructure capable of handling massive data volumes. InGaA PIN photodiodes, with their high responsivity and bandwidth, are indispensable components in these systems, enabling the conversion of optical signals to electrical signals at ever-increasing speeds. This foundational requirement for modern digital communication networks serves as a primary driver for market growth.

Another crucial driver is the burgeoning adoption of InGaA PIN photodiodes in non-communication sectors, notably automotive LiDAR systems and advanced medical imaging devices. In the automotive industry, LiDAR technology is pivotal for the development of autonomous vehicles and enhanced safety features, requiring highly sensitive and reliable photodiodes for accurate distance measurement and object detection. Similarly, in medical diagnostics, these photodiodes are utilized in high-resolution imaging and analytical instruments, offering superior performance over conventional detectors. The diversification of applications beyond traditional telecommunications broadens the market's reach and reduces its dependency on a single industry segment, contributing to its sustained growth trajectory.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Surging Demand for High-Speed Optical Communication | +3.5% | Global, particularly North America, APAC, Europe | 2025-2033 |

| Rapid Expansion of Fiber Optic Networks & Data Centers | +2.8% | Global, especially China, India, USA, Western Europe | 2025-2033 |

| Growing Adoption in Automotive LiDAR Systems | +2.0% | North America, Europe, Japan, South Korea, China | 2026-2033 |

| Advancements in Medical Imaging and Sensing Technologies | +1.5% | North America, Europe, Japan | 2025-2032 |

InGaA PIN Photodiode Market Restraints Analysis

Despite the optimistic growth projections, the InGaA PIN photodiode market faces certain restraints that could temper its expansion. One significant challenge is the relatively high manufacturing cost associated with these components, primarily due to the complex epitaxial growth processes and specialized material requirements of Indium Gallium Arsenide. This high cost can make InGaA PIN photodiodes less competitive in price-sensitive applications where alternative, albeit less performing, photodetectors might suffice. For mass-market adoption, particularly in consumer electronics or lower-tier communication equipment, cost-effectiveness remains a critical barrier that manufacturers must address through process optimization and economies of scale.

Another restraint is the intense competition from alternative photodetector technologies, such as silicon photodiodes and avalanche photodiodes (APDs), which may offer specific advantages in certain niches. While InGaA PIN photodiodes excel in the infrared spectrum vital for fiber optics, silicon photodiodes are more cost-effective and dominant in the visible and near-infrared range. APDs, on the other hand, offer higher sensitivity due to internal gain, which can be preferred in extremely low-light conditions, even if they introduce more noise. The continuous innovation in these alternative technologies poses a constant competitive threat, pressuring InGaA PIN photodiode manufacturers to continually enhance performance and reduce costs to maintain market relevance and share.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Manufacturing Costs of InGaA Photodiodes | -1.2% | Global | 2025-2030 |

| Competition from Alternative Photodetector Technologies (Silicon, APDs) | -0.8% | Global | 2025-2033 |

| Supply Chain Vulnerabilities and Geopolitical Tensions | -0.5% | Global, particularly APAC (China, Taiwan) | 2025-2028 |

InGaA PIN Photodiode Market Opportunities Analysis

Significant opportunities abound in the InGaA PIN photodiode market, particularly with the global rollout of 5G and future 6G communication technologies. These next-generation wireless networks demand an unprecedented level of data transmission speed and capacity, relying heavily on advanced fiber optic backbones where InGaA PIN photodiodes play a crucial role. The massive increase in data traffic generated by IoT devices, AI applications, and augmented/virtual reality experiences will necessitate continuous upgrades and expansion of optical infrastructure, thereby creating a sustained and robust demand for high-performance photodiodes. Manufacturers who can innovate to meet the stringent requirements of these evolving communication standards stand to gain significant market share.

Another promising opportunity lies in the accelerating trend of miniaturization and integration, especially within the context of silicon photonics. Integrating InGaA PIN photodiodes onto silicon chips allows for the creation of highly compact, energy-efficient, and cost-effective optical modules. This integration is crucial for smaller form-factor transceivers in data centers, compact sensors for consumer electronics, and sophisticated devices for medical applications. As industries push for higher performance in smaller footprints, the ability to seamlessly integrate InGaA technology with silicon platforms will unlock new design possibilities and expand the market into previously untapped segments. This technological synergy presents a compelling growth avenue for market participants.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Emergence of 5G and Future 6G Communication Technologies | +2.3% | Global, especially North America, China, Europe | 2025-2033 |

| Increasing Integration with Silicon Photonics Platforms | +1.8% | Global, R&D Hubs in USA, Europe, Japan | 2026-2033 |

| Growth in Quantum Computing and Advanced Sensing Applications | +1.0% | North America, Europe, APAC (select countries) | 2028-2033 |

InGaA PIN Photodiode Market Challenges Impact Analysis

The InGaA PIN photodiode market faces several technical and operational challenges that can impede its growth. One significant hurdle is the complexity associated with achieving high yield and consistency in manufacturing processes, particularly for advanced device structures. The epitaxial growth of InGaAs layers on Indium Phosphide (InP) substrates requires extremely precise control over material composition, thickness, and doping profiles to ensure optimal performance characteristics such as low dark current and high responsivity. Any deviation can lead to defects, reducing manufacturing yield and increasing production costs. Scaling up production while maintaining stringent quality standards remains a persistent challenge for manufacturers, especially as demand for higher-performance devices grows.

Another challenge stems from the rapid pace of technological obsolescence within the optical communication sector. As data rates continue to increase exponentially, there is a constant demand for photodiodes with higher bandwidth and lower power consumption. This necessitates continuous investment in research and development to keep pace with evolving industry standards (e.g., from 100G to 400G and 800G Ethernet). Manufacturers must innovate quickly to introduce new products that meet these evolving requirements, risking that current product lines may become obsolete relatively quickly. This short product lifecycle can strain R&D budgets and market planning, requiring agile strategies to stay competitive in a fast-moving technological landscape.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Complexity of Manufacturing Processes and Yield Optimization | -0.9% | Global | 2025-2031 |

| Rapid Technological Obsolescence and Need for Constant R&D | -0.7% | Global, particularly R&D intensive regions | 2025-2033 |

| Stringent Performance Requirements for Next-Gen Applications | -0.4% | Global | 2026-2033 |

InGaA PIN Photodiode Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the InGaA PIN Photodiode market, covering historical data, current market dynamics, and future projections. The scope encompasses detailed segmentation across various parameters, regional market insights, competitive landscape analysis, and an examination of key drivers, restraints, opportunities, and challenges influencing market growth. The report aims to offer strategic insights for stakeholders, enabling informed decision-making in this evolving technological landscape.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 480 Million |

| Market Forecast in 2033 | USD 1.15 Billion |

| Growth Rate | 11.5% CAGR |

| Number of Pages | 255 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Hamamatsu Photonics, Lumentum Holdings Inc., Broadcom Inc., Coherent Corp., OSI Optoelectronics, Excelitas Technologies Corp., Thorlabs, Inc., Mitsubishi Electric Corporation, Kyocera Corporation, MACOM Technology Solutions Inc., Qorvo, Inc., Semtech Corporation, Renesas Electronics Corporation, Onsemi, Vishay Intertechnology, Inc., Lite-On Technology Corporation, Analog Devices, Inc., Texas Instruments Incorporated, TDK Corporation, Murata Manufacturing Co., Ltd. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The InGaA PIN Photodiode market is broadly segmented by type, wavelength, application, and end-use industry, providing a granular view of market dynamics and opportunities across diverse categories. The segmentation by type primarily distinguishes between Planar Photodiodes and Mesa Photodiodes, each offering distinct advantages in terms of performance characteristics, manufacturing complexity, and suitability for specific applications. Planar photodiodes, known for their stable performance and ease of fabrication, often find use in standard optical communication systems, while Mesa photodiodes, with their higher speed and responsivity, are preferred for high-performance and high-bandwidth applications.

Further analysis by wavelength is critical as InGaA PIN photodiodes are optimized for specific spectral ranges, typically in the infrared region. The most common ranges include 850nm-1000nm, which is relevant for shorter-reach optical links, and 1000nm-1650nm, crucial for long-haul and metro fiber optic networks (1310nm and 1550nm). Application-based segmentation highlights the primary uses of these photodiodes across optical communication, medical, automotive, industrial, and consumer electronics sectors. Finally, the end-use industry segmentation provides insight into the adoption patterns and market penetration within specific verticals like telecommunications, IT, automotive, healthcare, and industrial sectors, revealing diverse growth drivers and competitive landscapes within each segment.

- By Type: Planar Photodiode, Mesa Photodiode

- By Wavelength: 850nm-1000nm, 1000nm-1650nm (e.g., 1310nm, 1550nm)

- By Application: Optical Communication, Medical, Automotive, Industrial, Consumer Electronics

- By End-Use Industry: Telecommunications, Information Technology, Automotive, Healthcare, Industrial, Aerospace & Defense

Regional Highlights

- North America: This region is a major hub for technological innovation and early adoption of advanced optical communication technologies, including 5G infrastructure and large-scale data centers. The presence of leading technology companies and significant investments in autonomous vehicle research also drives demand for InGaA PIN photodiodes in automotive LiDAR applications. The United States and Canada are key contributors to market growth.

- Europe: Characterized by strong industrial automation and automotive sectors, Europe exhibits significant demand for InGaA PIN photodiodes in industrial sensing, advanced manufacturing, and automotive LiDAR. Countries like Germany, France, and the UK are investing heavily in fiber optic network expansion and medical technology, further boosting regional market growth.

- Asia Pacific (APAC): The APAC region is projected to be the fastest-growing market due to massive investments in telecommunication infrastructure, including extensive fiber optic network deployments and the rapid rollout of 5G. Countries such as China, Japan, South Korea, and India are manufacturing powerhouses and have a burgeoning demand for high-speed data services, consumer electronics, and an emerging automotive LiDAR market.

- Latin America: While a nascent market compared to developed regions, Latin America shows promising growth driven by increasing internet penetration, expanding data center capacities, and investments in telecommunications infrastructure. Countries like Brazil and Mexico are emerging as key markets.

- Middle East and Africa (MEA): This region is experiencing growth in optical communication due to ongoing digitalization initiatives, smart city projects, and expanding network coverage. Investments in oil & gas and defense sectors also contribute to demand for specialized sensing applications utilizing InGaA PIN photodiodes.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the InGaA PIN Photodiode Market.- Hamamatsu Photonics

- Lumentum Holdings Inc.

- Broadcom Inc.

- Coherent Corp.

- OSI Optoelectronics

- Excelitas Technologies Corp.

- Thorlabs, Inc.

- Mitsubishi Electric Corporation

- Kyocera Corporation

- MACOM Technology Solutions Inc.

- Qorvo, Inc.

- Semtech Corporation

- Renesas Electronics Corporation

- Onsemi

- Vishay Intertechnology, Inc.

- Lite-On Technology Corporation

- Analog Devices, Inc.

- Texas Instruments Incorporated

- TDK Corporation

- Murata Manufacturing Co., Ltd.

Frequently Asked Questions

What is an InGaA PIN Photodiode and what is its primary function?

An InGaA PIN photodiode is a semiconductor device made from Indium Gallium Arsenide (InGaAs) that converts light signals into electrical current. Its primary function is in optical receivers where it detects optical signals, particularly in the infrared spectrum, and efficiently transforms them into electrical signals for processing in communication systems and various sensing applications.

What are the key applications driving the growth of the InGaA PIN Photodiode market?

The key applications driving market growth include high-speed optical communication (fiber optic networks, data centers, transceivers), automotive LiDAR systems for autonomous vehicles, advanced medical imaging and diagnostics, and various industrial sensing and spectroscopy applications.

How does the performance of InGaA PIN photodiodes compare to silicon photodiodes?

InGaA PIN photodiodes offer superior performance in the infrared wavelength range (typically 800nm-1700nm), exhibiting higher responsivity and lower noise compared to silicon photodiodes at these wavelengths. Silicon photodiodes are more cost-effective and perform well in the visible and near-infrared (up to 1000nm), but their efficiency drops significantly beyond this range, making InGaA preferred for fiber optic communication.

What impact does 5G technology have on the InGaA PIN Photodiode market?

5G technology significantly boosts the InGaA PIN Photodiode market by demanding extensive fiber optic backbones and advanced optical transceivers for its high-speed and low-latency requirements. The massive increase in data traffic and interconnected devices driven by 5G necessitates robust optical communication infrastructure, directly increasing the demand for high-performance InGaA PIN photodiodes.

What are the primary challenges faced by manufacturers in the InGaA PIN Photodiode market?

Manufacturers face challenges such as the high manufacturing costs associated with complex material growth processes, intense competition from alternative photodetector technologies, and the rapid pace of technological obsolescence which necessitates continuous investment in research and development to meet evolving performance requirements.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted