Industrial Wireless Vibration Sensor Network Market

Industrial Wireless Vibration Sensor Network Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_701512 | Last Updated : July 30, 2025 |

Format : ![]()

![]()

![]()

![]()

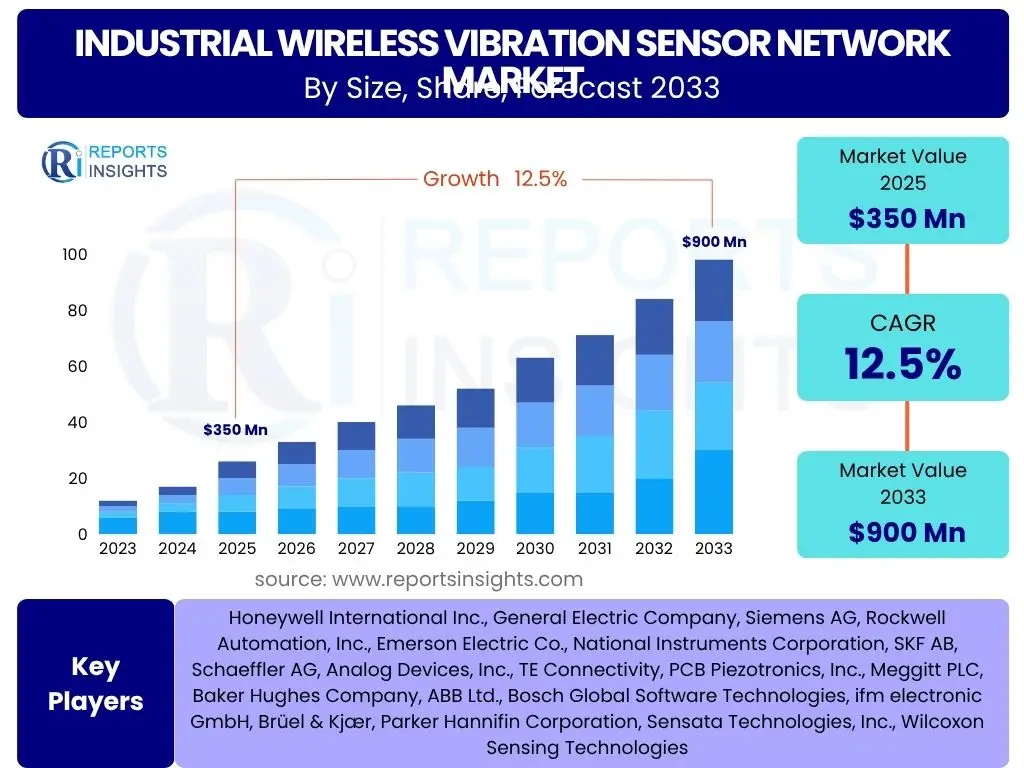

Industrial Wireless Vibration Sensor Network Market Size

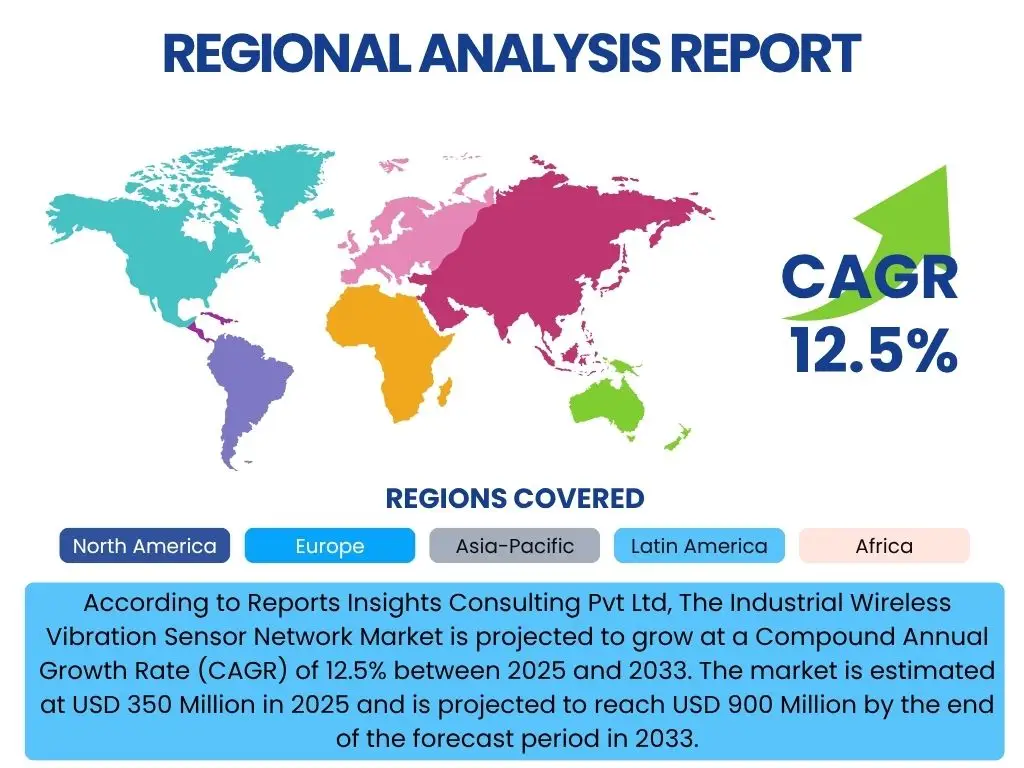

According to Reports Insights Consulting Pvt Ltd, The Industrial Wireless Vibration Sensor Network Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 12.5% between 2025 and 2033. The market is estimated at USD 350 Million in 2025 and is projected to reach USD 900 Million by the end of the forecast period in 2033.

Key Industrial Wireless Vibration Sensor Network Market Trends & Insights

The Industrial Wireless Vibration Sensor Network market is experiencing transformative growth, driven by an increasing focus on operational efficiency and predictive maintenance across various industries. A prominent trend is the widespread integration of these networks with broader Industrial Internet of Things (IIoT) ecosystems, enabling seamless data flow and enhanced real-time insights. This integration supports the shift towards proactive asset management, minimizing downtime and optimizing resource allocation.

Further, advancements in sensor technology, including improved accuracy, miniaturization, and energy efficiency, are expanding the applicability of wireless vibration monitoring in challenging industrial environments. The push for digitalization and the adoption of Industry 4.0 principles are fundamentally reshaping how companies approach asset health, making wireless vibration sensors indispensable tools for modern industrial operations. This evolution is also fostering a demand for more sophisticated analytics and user-friendly interfaces to interpret complex vibration data.

- Growing adoption of Industry 4.0 and IIoT for smarter factories.

- Increased focus on predictive maintenance strategies to reduce operational costs.

- Advancements in low-power wireless communication protocols like LoRaWAN and 5G.

- Development of miniaturized and more robust sensor designs for diverse environments.

- Rising demand for cloud-based data analytics and visualization platforms.

AI Impact Analysis on Industrial Wireless Vibration Sensor Network

The integration of Artificial Intelligence (AI) and Machine Learning (ML) is revolutionizing the Industrial Wireless Vibration Sensor Network market by significantly enhancing data analysis and predictive capabilities. Users are increasingly seeking solutions that move beyond simple data collection to deliver actionable insights, and AI is central to fulfilling this demand. By applying AI algorithms, sensor networks can more accurately identify anomalous vibration patterns, differentiate between various types of equipment faults, and predict potential failures with higher precision than traditional methods.

This transformative impact extends to optimizing maintenance schedules, reducing false positives, and providing deeper diagnostic insights, thereby maximizing asset uptime and extending equipment lifespans. However, user concerns often revolve around the complexity of AI model training, the need for large datasets, and the cybersecurity implications of highly integrated intelligent systems. Addressing these concerns through intuitive platforms and robust data security measures will be crucial for the widespread adoption of AI-powered wireless vibration sensor networks.

- Enhanced anomaly detection and fault diagnosis through pattern recognition.

- Improved predictive accuracy for equipment failures, optimizing maintenance windows.

- Reduced false alarms by differentiating normal operational variations from true issues.

- Automated data analysis and interpretation, simplifying complex vibration data for users.

- Enabling self-learning systems that adapt to equipment changes and environmental factors.

Key Takeaways Industrial Wireless Vibration Sensor Network Market Size & Forecast

The Industrial Wireless Vibration Sensor Network market is poised for substantial expansion, driven primarily by the global imperative for enhanced operational efficiency and asset reliability across diverse industrial sectors. The projected growth reflects a strong market shift towards proactive, data-driven maintenance strategies that leverage wireless technology to overcome traditional monitoring limitations. Stakeholders are increasingly recognizing the significant return on investment offered by these systems in terms of reduced downtime, extended asset lifespan, and optimized resource allocation.

A key insight from the market forecast is the accelerating adoption in rapidly industrializing regions, alongside continued maturation in established economies that are heavily investing in smart manufacturing initiatives. The interplay of technological advancements, supportive regulatory environments emphasizing safety and efficiency, and the growing demand for real-time asset insights will collectively underpin this robust market trajectory throughout the forecast period. This signifies a lucrative landscape for technology providers and a strategic necessity for end-users aiming for competitive advantage.

- Significant growth expected due to increasing industrial automation and digitalization.

- Predictive maintenance and condition monitoring remain primary growth catalysts.

- Asia Pacific is anticipated to be a leading region for market expansion.

- Integration with IIoT platforms is enhancing data utility and operational benefits.

- Return on Investment (ROI) from reduced downtime and maintenance costs is a key driver for adoption.

Industrial Wireless Vibration Sensor Network Market Drivers Analysis

The proliferation of Industry 4.0 initiatives and the broader adoption of the Industrial Internet of Things (IIoT) are acting as primary accelerators for the Industrial Wireless Vibration Sensor Network market. As industries increasingly integrate smart technologies into their operations, there is a heightened demand for connected sensors capable of providing real-time data for advanced analytics. Wireless vibration sensors fit seamlessly into this evolving ecosystem, facilitating data collection from previously inaccessible or costly-to-wire locations, thereby enhancing overall operational visibility and control.

Moreover, the escalating demand for predictive maintenance solutions represents another critical driver. Traditional reactive or time-based maintenance approaches often lead to unplanned downtime and higher operational costs. Wireless vibration sensors enable continuous monitoring of equipment health, allowing for the early detection of anomalies and the scheduling of maintenance activities precisely when needed. This shift from reactive to predictive strategies not only minimizes downtime but also optimizes maintenance expenditure and extends the lifespan of valuable industrial assets, directly contributing to the market's expansion.

Further supporting market growth is the continuous innovation in wireless communication technologies. Advancements in low-power, long-range wireless protocols such as LoRaWAN, Zigbee, and advancements in 5G for industrial applications are overcoming previous limitations related to battery life, signal range, and data transmission rates. These technological improvements make wireless vibration sensor networks more reliable, scalable, and cost-effective, broadening their applicability across a wider range of industrial settings and overcoming barriers to adoption.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing Adoption of Industry 4.0 & IIoT | +2.5% | Global, particularly North America, Europe, Asia Pacific | Short to Mid-term (2025-2030) |

| Rising Demand for Predictive Maintenance | +2.0% | Global, strong in Manufacturing, Oil & Gas, Power Generation | Short to Long-term (2025-2033) |

| Technological Advancements in Wireless Communication | +1.8% | Global | Short to Mid-term (2025-2030) |

| Emphasis on Operational Efficiency & Cost Reduction | +1.5% | Global, across all industrial sectors | Mid to Long-term (2027-2033) |

| Increased Focus on Workplace Safety | +1.0% | Europe, North America, industries with hazardous environments | Mid-term (2026-2031) |

Industrial Wireless Vibration Sensor Network Market Restraints Analysis

One significant restraint on the Industrial Wireless Vibration Sensor Network market is the substantial initial investment required for deployment. Implementing a comprehensive wireless vibration monitoring system involves not only the cost of sensors and network infrastructure but also expenses related to software integration, data storage, and personnel training. For many small and medium-sized enterprises (SMEs), these upfront costs can be prohibitive, acting as a barrier to adoption despite the long-term benefits of reduced maintenance costs and improved operational efficiency. This financial hurdle often necessitates a strong justification of ROI, which can prolong the sales cycle and limit market penetration in certain segments.

Another critical challenge impeding market growth is the prevalent concern over cybersecurity and data privacy. Industrial wireless networks, by their nature, transmit sensitive operational data, making them potential targets for cyber-attacks. Breaches could lead to intellectual property theft, operational disruption, or even physical damage to machinery. Industries with stringent security requirements, such as defense, energy, and critical infrastructure, often exhibit caution in adopting wireless solutions due to these risks. Ensuring robust encryption, secure protocols, and compliance with data protection regulations becomes paramount, adding complexity and cost to system implementation.

Furthermore, interoperability issues among various wireless protocols, sensor types, and software platforms present a notable restraint. The industrial automation landscape is fragmented, with numerous vendors offering proprietary solutions. This lack of standardization can make it difficult for end-users to integrate wireless vibration sensor networks with existing legacy systems or to scale their monitoring capabilities across different equipment types and manufacturers. The absence of universal communication standards often leads to vendor lock-in and limits flexibility, deterring companies that prioritize open architectures and future-proof solutions.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Initial Investment & Installation Costs | -1.5% | Global, more pronounced in SMEs and developing regions | Short to Mid-term (2025-2029) |

| Cybersecurity Concerns & Data Vulnerability | -1.2% | Global, particularly in critical infrastructure sectors | Short to Long-term (2025-2033) |

| Interoperability & Integration Challenges with Legacy Systems | -1.0% | Global, especially in mature industrial economies | Mid-term (2026-2031) |

| Sensor Battery Life & Maintenance Requirements | -0.8% | Global, for remote or hard-to-access assets | Short to Mid-term (2025-2028) |

Industrial Wireless Vibration Sensor Network Market Opportunities Analysis

The expansion of cloud-based platforms and edge computing presents a significant opportunity for the Industrial Wireless Vibration Sensor Network market. By leveraging cloud infrastructure, industrial data can be securely stored, processed, and analyzed on a much larger scale, enabling advanced analytics, AI-driven insights, and remote access to equipment health information from anywhere. Edge computing, on the other hand, allows for real-time data processing closer to the source, reducing latency and bandwidth requirements, which is crucial for critical applications requiring immediate feedback. This combination offers scalability, flexibility, and enhanced computational power, driving further adoption of wireless vibration monitoring solutions, especially for geographically dispersed operations.

Another key opportunity lies in the growing demand for remote monitoring and asset management, particularly exacerbated by global events that emphasize the need for remote operations and reduced on-site presence. Wireless vibration sensors are inherently suited for remote deployment in hazardous or inaccessible environments, enabling continuous data collection without human intervention. This capability supports a shift towards fully remote or minimally staffed facilities, improving safety, reducing operational costs, and ensuring business continuity. As industries continue to embrace digital transformation, the value proposition of remote, wireless asset monitoring will only strengthen, opening new market avenues.

Furthermore, the untapped potential within small and medium-sized enterprises (SMEs) represents a lucrative opportunity for market players. While larger corporations have been early adopters, many SMEs still rely on reactive maintenance or manual inspections. As the cost-effectiveness and ease of deployment of wireless vibration sensor networks improve, and as subscription-based service models become more prevalent, these solutions become more accessible to smaller businesses. Tailored solutions, simplified interfaces, and scalable deployment options can help unlock this segment, allowing SMEs to also benefit from predictive maintenance and enhance their competitive edge without requiring massive capital outlays.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Integration with Cloud & Edge Computing Platforms | +1.8% | Global, particularly in industries with large-scale operations | Short to Mid-term (2025-2030) |

| Growing Demand for Remote Monitoring & Asset Management | +1.5% | Global, driven by safety and operational efficiency needs | Short to Long-term (2025-2033) |

| Expansion into Small & Medium-sized Enterprises (SMEs) | +1.2% | Developing and emerging economies, as well as niche markets | Mid to Long-term (2027-2033) |

| Development of AI-Powered Predictive Analytics Services | +1.0% | Global, across all industrial sectors | Mid-term (2026-2031) |

Industrial Wireless Vibration Sensor Network Market Challenges Impact Analysis

One significant challenge confronting the Industrial Wireless Vibration Sensor Network market is the limited battery life of wireless sensors, particularly in demanding industrial environments where frequent battery replacement can be impractical, costly, and disruptive to operations. While technological advancements are continuously improving power efficiency, achieving several years of operational life without maintenance remains an ongoing hurdle. This limitation affects the total cost of ownership and can deter adoption in applications where sensors are deployed in remote, hazardous, or difficult-to-access locations, necessitating innovative power solutions like energy harvesting.

Another notable challenge stems from the inherent harshness of industrial environments. Wireless vibration sensors are often exposed to extreme temperatures, high humidity, corrosive chemicals, electromagnetic interference, and mechanical shocks. Ensuring the durability, reliability, and accuracy of these sensors under such severe conditions requires advanced material science and robust design, which can increase manufacturing costs and complexity. The need for sensors to withstand these elements while maintaining connectivity and data integrity poses a significant engineering and design challenge for manufacturers.

Furthermore, the complexity associated with data overload and the subsequent analysis of vast amounts of vibration data presents a considerable challenge. While wireless networks enable continuous data collection, effectively processing, storing, and deriving meaningful insights from this data deluge requires sophisticated analytical tools and skilled personnel. Without robust data management strategies and advanced AI/ML algorithms, the sheer volume of raw vibration data can become overwhelming, potentially obscuring critical information and undermining the value proposition of the entire monitoring system. This necessitates a focus on intuitive user interfaces and automated analytical capabilities.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Sensor Battery Life & Power Management | -1.0% | Global, particularly for long-term deployments in remote areas | Short to Mid-term (2025-2029) |

| Environmental Harshness & Sensor Durability | -0.9% | Global, especially in heavy industries (e.g., Mining, Chemical) | Short to Long-term (2025-2033) |

| Data Overload & Complexity of Analysis | -0.7% | Global, across all industrial sectors | Mid-term (2026-2031) |

| Lack of Standardized Protocols & Interoperability | -0.6% | Global, impacts broader market integration | Mid to Long-term (2027-2033) |

Industrial Wireless Vibration Sensor Network Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the Industrial Wireless Vibration Sensor Network market, encompassing historical data, current market dynamics, and future projections. It delivers critical insights into market size, growth drivers, restraints, opportunities, and challenges, offering a detailed understanding of the industry landscape for strategic decision-making and investment planning. The report covers various segmentation types and offers regional breakdowns, identifying key trends and profiling major market players.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 350 Million |

| Market Forecast in 2033 | USD 900 Million |

| Growth Rate | 12.5% |

| Number of Pages | 250 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Honeywell International Inc., General Electric Company, Siemens AG, Rockwell Automation, Inc., Emerson Electric Co., National Instruments Corporation, SKF AB, Schaeffler AG, Analog Devices, Inc., TE Connectivity, PCB Piezotronics, Inc., Meggitt PLC, Baker Hughes Company, ABB Ltd., Bosch Global Software Technologies, ifm electronic GmbH, Brüel & Kjær, Parker Hannifin Corporation, Sensata Technologies, Inc., Wilcoxon Sensing Technologies |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Industrial Wireless Vibration Sensor Network market is meticulously segmented to provide a granular view of its diverse applications and technological underpinnings. This segmentation allows for a comprehensive understanding of how different components, end-use industries, applications, and technologies contribute to the overall market landscape, enabling stakeholders to identify specific growth areas and tailor their strategies accordingly.

- By Component: Encompasses the hardware elements like sensors, transmitters, and receivers, along with critical software and supporting services that enable data acquisition, analysis, and system maintenance.

- By End-use Industry: Covers a wide array of sectors, including heavy industries such as Oil & Gas, Power Generation, Chemical & Petrochemical, alongside Manufacturing, Metals & Mining, Automotive, and Food & Beverage, each with unique vibration monitoring requirements.

- By Application: Focuses on the specific uses of these networks, primarily Condition Monitoring, Predictive Maintenance, Process Monitoring, and Asset Tracking, highlighting their roles in operational efficiency and reliability.

- By Technology: Differentiates based on the wireless communication protocols utilized, such as Bluetooth, Wi-Fi, Zigbee, LoRaWAN, Cellular (4G/5G), and various proprietary technologies, each offering distinct advantages in terms of range, power consumption, and data rates.

Regional Highlights

North America: This region stands as a significant market for Industrial Wireless Vibration Sensor Networks, driven by early adoption of advanced manufacturing technologies, robust industrial infrastructure, and a strong emphasis on smart factory initiatives. Countries like the United States and Canada are witnessing increased investments in automation and digitalization across sectors such as aerospace, automotive, and oil & gas. The presence of major technology providers and a high awareness among industries regarding the benefits of predictive maintenance further fuel market growth in this region. Regulatory pressures for operational safety and efficiency also contribute to the steady demand for these advanced monitoring solutions.

Europe: Europe represents a mature yet continually expanding market, characterized by stringent industrial regulations, a strong focus on sustainability, and significant investments in Industry 4.0. Nations such as Germany, the UK, and France are at the forefront of adopting industrial automation and smart manufacturing practices, creating a fertile ground for wireless vibration sensor networks. The region’s established manufacturing base, coupled with ongoing efforts to modernize industrial processes and reduce energy consumption, drives the demand for precise and efficient condition monitoring solutions. The emphasis on worker safety and environmental protection also encourages the deployment of remote monitoring technologies.

Asia Pacific (APAC): The Asia Pacific region is projected to exhibit the highest growth rate in the Industrial Wireless Vibration Sensor Network market during the forecast period. This rapid expansion is primarily attributed to rapid industrialization, burgeoning manufacturing sectors in countries like China, India, Japan, and South Korea, and increasing governmental support for digital transformation. Large-scale infrastructure projects, the expansion of the energy sector, and the growth of automotive and electronics manufacturing are leading to a significant uptake of advanced monitoring systems. The competitive industrial landscape in APAC compels companies to adopt efficient technologies to enhance productivity and reduce operational costs, making wireless vibration sensors a strategic investment.

Latin America: The Latin American market for industrial wireless vibration sensor networks is showing promising growth, albeit from a lower base compared to developed regions. This growth is primarily spurred by increasing industrial investments, particularly in the mining, oil & gas, and manufacturing sectors across countries like Brazil, Mexico, and Argentina. As these industries seek to optimize operations, improve safety, and reduce downtime, the adoption of predictive maintenance solutions becomes more prevalent. Economic development and the drive for greater efficiency are key factors propelling the market forward in this region, with a rising awareness of the long-term benefits of wireless monitoring.

Middle East & Africa (MEA): The MEA region is witnessing a steady uptake of Industrial Wireless Vibration Sensor Networks, largely driven by significant investments in the oil & gas, petrochemical, and power generation sectors. Countries in the Gulf Cooperation Council (GCC) are modernizing their industrial infrastructures and embracing digitalization to diversify their economies and enhance operational resilience. The harsh environmental conditions prevalent in these regions also make wireless and remote monitoring solutions particularly valuable for reducing human exposure to risks and ensuring asset integrity. Government initiatives aimed at industrial diversification and technological advancement are expected to further boost market penetration in the coming years.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Industrial Wireless Vibration Sensor Network Market.- Honeywell International Inc.

- General Electric Company

- Siemens AG

- Rockwell Automation, Inc.

- Emerson Electric Co.

- National Instruments Corporation

- SKF AB

- Schaeffler AG

- Analog Devices, Inc.

- TE Connectivity

- PCB Piezotronics, Inc.

- Meggitt PLC

- Baker Hughes Company

- ABB Ltd.

- Bosch Global Software Technologies

- ifm electronic GmbH

- Brüel & Kjær

- Parker Hannifin Corporation

- Sensata Technologies, Inc.

- Wilcoxon Sensing Technologies

Frequently Asked Questions

Analyze common user questions about the Industrial Wireless Vibration Sensor Network market and generate a concise list of summarized FAQs reflecting key topics and concerns.What are the primary benefits of implementing an Industrial Wireless Vibration Sensor Network?

Implementing an Industrial Wireless Vibration Sensor Network offers significant benefits, including enhanced predictive maintenance capabilities, which reduce unplanned downtime and maintenance costs. It improves operational efficiency, extends asset lifespan, enhances workplace safety by enabling remote monitoring, and provides real-time insights into equipment health, leading to optimized decision-making and improved overall productivity.

How does AI impact the performance and capabilities of these sensor networks?

AI significantly enhances Industrial Wireless Vibration Sensor Networks by enabling advanced data analysis, improved anomaly detection, and highly accurate fault diagnosis. AI algorithms can identify subtle patterns indicative of impending failures, optimize maintenance schedules, reduce false positives, and provide actionable insights from complex vibration data, transforming raw data into intelligent, predictive information for proactive asset management.

What industries are most likely to benefit from adopting wireless vibration monitoring?

Industries that rely heavily on rotating machinery and critical assets, such as Oil & Gas, Power Generation, Chemical & Petrochemical, Manufacturing, Metals & Mining, and Automotive, stand to benefit most. These sectors face high costs from downtime and asset failure, making predictive maintenance via wireless vibration sensors an invaluable tool for operational continuity, safety, and efficiency.

What are the main challenges associated with deploying wireless vibration sensor networks?

Key challenges include the initial investment costs, ensuring sensor battery longevity in demanding industrial settings, addressing cybersecurity concerns for data integrity and network security, overcoming interoperability issues with existing legacy systems, and managing the vast amounts of data generated to derive meaningful insights effectively.

What future trends are expected to shape the Industrial Wireless Vibration Sensor Network market?

Future trends include deeper integration with broader IIoT and Industry 4.0 platforms, increased adoption of AI and Machine Learning for predictive analytics, the proliferation of cloud and edge computing for data processing, advancements in low-power and long-range wireless communication technologies (e.g., 5G), and the expansion of these solutions into a wider range of industrial applications and SMEs.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted