Industrial Rubber Market

Industrial Rubber Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_703692 | Last Updated : August 05, 2025 |

Format : ![]()

![]()

![]()

![]()

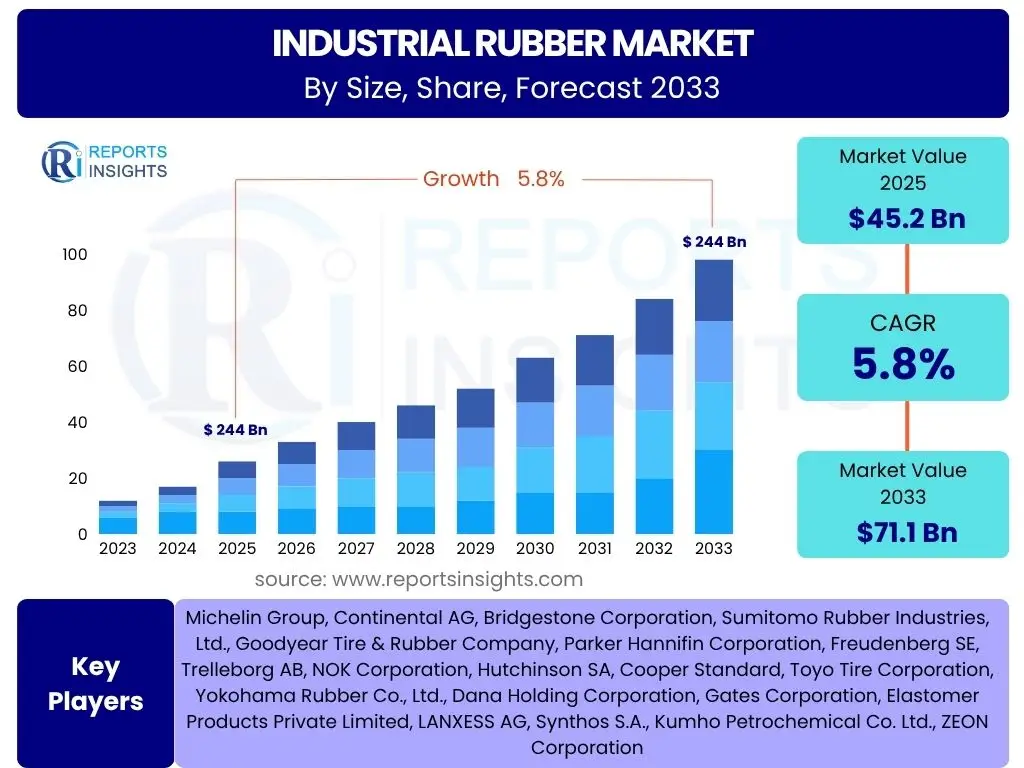

Industrial Rubber Market Size

According to Reports Insights Consulting Pvt Ltd, The Industrial Rubber Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.8% between 2025 and 2033. The market is estimated at USD 45.2 Billion in 2025 and is projected to reach USD 71.1 Billion by the end of the forecast period in 2033. This growth trajectory is underpinned by robust demand across various industrial sectors, including automotive, construction, and manufacturing, all of which heavily rely on industrial rubber products for critical applications. The expansion of emerging economies and continued advancements in material science are significant contributors to this sustained market progression.

Key Industrial Rubber Market Trends & Insights

The industrial rubber market is experiencing transformative shifts driven by technological innovation, sustainability imperatives, and evolving end-use industry requirements. Users frequently inquire about the leading trends shaping this sector, particularly regarding material advancements and application diversification. A prominent trend involves the development and adoption of high-performance elastomers capable of withstanding extreme conditions, such as high temperatures, harsh chemicals, and significant mechanical stress, thereby extending product lifespan and enhancing operational efficiency in demanding environments. Furthermore, there is a growing emphasis on sustainable rubber solutions, including recycled rubber content and bio-based polymers, to meet stringent environmental regulations and corporate social responsibility objectives.

Another significant trend is the increasing demand for customized and application-specific rubber products. Industries are moving away from generic components towards bespoke solutions that optimize performance, reduce downtime, and integrate seamlessly with advanced machinery and systems. This necessitates collaborative innovation between rubber manufacturers and their industrial clients to develop tailored compounds and designs. The integration of smart technologies, such as sensors within rubber components for predictive maintenance and real-time monitoring, is also emerging, promising to revolutionize asset management and operational reliability in industrial settings. These trends collectively underscore a dynamic market characterized by innovation, sustainability, and tailored solutions.

- Shift towards high-performance and specialty elastomers.

- Growing adoption of sustainable and recycled rubber materials.

- Increased demand for customized and application-specific rubber solutions.

- Integration of smart technologies for predictive maintenance.

- Expansion of industrial rubber applications in renewable energy and healthcare.

AI Impact Analysis on Industrial Rubber

The industrial rubber sector is beginning to explore the transformative potential of Artificial Intelligence (AI), addressing user queries about how this technology can enhance manufacturing processes, product development, and supply chain management. AI's immediate impact is most evident in optimizing production lines, where machine learning algorithms can analyze vast datasets from sensors to predict equipment failures, optimize material usage, and fine-tune curing processes. This predictive capability leads to significant reductions in downtime, waste, and energy consumption, thereby improving overall operational efficiency and product quality. Furthermore, AI-driven simulations can accelerate the design and testing of new rubber compounds, allowing manufacturers to quickly iterate on formulations and prototypes, reducing time-to-market for innovative products with enhanced properties.

Beyond manufacturing, AI is also poised to revolutionize demand forecasting and supply chain resilience within the industrial rubber market. By analyzing market data, economic indicators, and historical demand patterns, AI models can provide highly accurate predictions, enabling manufacturers to optimize inventory levels, mitigate risks associated with raw material price volatility, and respond more agilely to market fluctuations. Additionally, AI-powered quality control systems can identify defects with unprecedented precision, ensuring that only components meeting the highest standards reach the end-user. While the full integration of AI is still in its nascent stages for many players, its potential to drive efficiency, innovation, and strategic decision-making across the industrial rubber value chain is undeniable.

- Optimization of manufacturing processes and quality control.

- Enhanced predictive maintenance for machinery and equipment.

- Accelerated material R&D and product development cycles.

- Improved supply chain management and demand forecasting.

- Automation of repetitive tasks, leading to increased efficiency.

Key Takeaways Industrial Rubber Market Size & Forecast

Common inquiries regarding the industrial rubber market's future trajectory emphasize understanding its core growth drivers and the factors that will sustain its expansion through the forecast period. A primary takeaway is the consistent demand from resilient end-use industries, particularly the automotive sector's ongoing evolution and the global push for infrastructure development. These sectors are fundamental consumers of industrial rubber, ensuring a stable base for market growth. The market's projected Compound Annual Growth Rate (CAGR) of 5.8% signifies a steady and reliable expansion, reflecting the essential nature of rubber components in modern industrial applications and continuous innovation in material science.

Another crucial insight is the increasing emphasis on specialization and high-performance products. As industries demand more durable, efficient, and application-specific solutions, manufacturers are investing in research and development to produce advanced elastomers capable of operating under extreme conditions. This shift towards value-added products, coupled with an increasing focus on sustainability through recycled and bio-based materials, positions the market for not just quantitative growth but also qualitative improvement. The forecast of the market reaching USD 71.1 Billion by 2033 further underscores the substantial economic opportunity and the integral role industrial rubber will continue to play in global manufacturing and infrastructure.

- Robust demand sustained by key end-use industries like automotive and construction.

- Steady Compound Annual Growth Rate (CAGR) reflecting fundamental market necessity.

- Significant market value projected, indicating strong economic opportunity.

- Increasing focus on high-performance and specialized rubber products.

- Growing influence of sustainability and material innovation on market direction.

Industrial Rubber Market Drivers Analysis

The growth of the industrial rubber market is significantly propelled by several key drivers, each contributing to increased demand and technological advancement within the sector. One primary driver is the accelerating pace of industrialization and infrastructure development across emerging economies. As nations invest heavily in manufacturing facilities, transportation networks, and construction projects, the need for a wide array of industrial rubber components—such as hoses, belts, seals, and anti-vibration mounts—escalates proportionally. These components are critical for the efficient operation, safety, and longevity of industrial machinery and infrastructure.

Another substantial driver is the expansion and innovation within the automotive industry. Despite shifts towards electric vehicles, the fundamental requirement for rubber components in various automotive systems, including tires, sealing systems, engine mounts, and hoses, remains robust. Furthermore, the increasing complexity and performance demands of modern vehicles necessitate advanced rubber materials that can withstand harsher conditions and offer superior durability. Additionally, the growing focus on energy efficiency and environmental regulations is spurring demand for high-performance and specialized rubber products that can contribute to reduced friction, improved insulation, and overall system optimization in industrial applications, thereby indirectly driving market growth.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Rapid Industrialization & Infrastructure Development | +1.5-2.0% | Asia Pacific (China, India), Latin America | Long-term (2025-2033) |

| Growth in Automotive Production & Advanced Vehicle Systems | +1.0-1.5% | Global, particularly Asia, Europe, North America | Mid-term (2025-2029) |

| Technological Advancements in Material Science | +0.8-1.2% | Global | Long-term (2025-2033) |

| Increasing Demand for High-Performance & Specialty Elastomers | +0.7-1.0% | North America, Europe, Asia Pacific | Mid to Long-term (2025-2033) |

| Expansion of Mining and Heavy Machinery Sectors | +0.5-0.8% | Asia Pacific, Latin America, Africa | Mid-term (2025-2029) |

Industrial Rubber Market Restraints Analysis

While the industrial rubber market exhibits promising growth, it also faces several significant restraints that could temper its expansion. One major impediment is the volatility in raw material prices, particularly for crude oil derivatives used in synthetic rubber production, and the natural rubber supply which is susceptible to weather conditions and geopolitical factors. Fluctuations in these input costs directly impact manufacturing expenses, potentially compressing profit margins for producers and leading to higher end-product prices, which can deter demand in price-sensitive markets. This unpredictability makes long-term strategic planning challenging for market participants.

Another considerable restraint is the increasing stringency of environmental regulations worldwide, particularly concerning the production and disposal of synthetic rubber and associated chemicals. Compliance with these regulations often requires significant investments in cleaner production technologies and waste management systems, adding to operational costs. Furthermore, the emergence of alternative materials, such as advanced plastics and composites, in certain applications poses a competitive threat. While rubber remains indispensable for many uses, advancements in other material sciences offer substitutes that may provide comparable or superior performance characteristics at competitive costs, prompting a re-evaluation of material choices by end-users. These factors collectively present challenges that necessitate adaptive strategies from industrial rubber manufacturers.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Volatility of Raw Material Prices | -1.0-1.5% | Global | Short to Mid-term (2025-2028) |

| Stringent Environmental Regulations | -0.8-1.2% | Europe, North America, parts of Asia | Long-term (2025-2033) |

| Competition from Alternative Materials | -0.5-0.9% | Global | Mid to Long-term (2025-2033) |

| Economic Slowdowns and Industrial Production Declines | -0.7-1.0% | Region-specific (e.g., Europe, China) | Short-term (2025-2027) |

| High Energy Consumption in Production | -0.4-0.7% | Global | Long-term (2025-2033) |

Industrial Rubber Market Opportunities Analysis

Significant opportunities abound in the industrial rubber market, primarily driven by the ongoing shift towards sustainable practices and the expansion into niche, high-growth sectors. The increasing global awareness and regulatory pressure regarding environmental impact are creating a strong demand for eco-friendly rubber solutions, including recycled, bio-based, and biodegradable elastomers. Manufacturers who invest in developing and marketing these sustainable alternatives stand to gain a competitive edge and capture a growing segment of environmentally conscious consumers and industries. This trend also opens avenues for innovation in rubber processing technologies that reduce environmental footprints.

Furthermore, the rapid growth in industries such as renewable energy (wind turbines, solar panels), healthcare (medical devices, seals), and aerospace presents lucrative opportunities for specialized industrial rubber products. These sectors require highly durable, precise, and often custom-engineered rubber components that can withstand unique operating conditions and meet stringent performance standards. Developing tailored solutions for these high-value applications, coupled with advancements in additive manufacturing (3D printing) for rubber, can unlock new revenue streams and market segments. The digitalization of industrial processes and the increasing adoption of Industry 4.0 paradigms also create opportunities for smart rubber components, integrating sensors for real-time monitoring and predictive maintenance, thereby adding significant value to end-user applications.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development of Sustainable & Bio-based Rubber | +1.2-1.8% | Europe, North America, Japan | Long-term (2025-2033) |

| Growth in Niche Applications (Healthcare, Renewable Energy, Aerospace) | +1.0-1.5% | Global, especially developed economies | Mid to Long-term (2025-2033) |

| Advancements in Smart Rubber & Sensor Integration | +0.8-1.2% | North America, Europe, East Asia | Mid-term (2027-2033) |

| Expansion into Emerging Markets & Underserved Regions | +0.7-1.0% | Africa, Southeast Asia, Latin America | Long-term (2025-2033) |

| Strategic Collaborations and Mergers & Acquisitions | +0.5-0.8% | Global | Short to Mid-term (2025-2029) |

Industrial Rubber Market Challenges Impact Analysis

The industrial rubber market faces several complex challenges that necessitate strategic responses from market participants. One significant challenge is managing disruptions in the global supply chain, which can arise from geopolitical tensions, natural disasters, or pandemics. Such disruptions can lead to shortages of critical raw materials, increased logistics costs, and delays in delivery, impacting production schedules and customer satisfaction. The globalized nature of raw material sourcing and manufacturing makes the industry particularly vulnerable to these external shocks, requiring robust risk management and diversification strategies.

Another key challenge is the escalating cost of energy, which is a substantial input for rubber processing operations. High energy prices can erode profit margins, especially for manufacturers without access to renewable energy sources or energy-efficient technologies. Furthermore, the industrial rubber sector grapples with the need for a highly skilled workforce, from material scientists for R&D to specialized technicians for complex machinery operation. A growing skills gap in many regions poses a challenge to innovation, production quality, and expansion efforts. Overcoming these challenges will require continuous investment in technology, diversification of supply chains, and talent development initiatives to maintain competitiveness and ensure sustainable growth in the market.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Global Supply Chain Disruptions | -0.9-1.3% | Global | Short to Mid-term (2025-2028) |

| Volatile Energy Costs | -0.7-1.0% | Global | Mid-term (2025-2029) |

| Shortage of Skilled Labor and Talent Retention | -0.5-0.8% | North America, Europe, Japan | Long-term (2025-2033) |

| Intense Competition and Price Pressure | -0.4-0.7% | Global | Long-term (2025-2033) |

| Disposal and Recycling of Rubber Waste | -0.3-0.6% | Global, particularly developed regions | Long-term (2025-2033) |

Industrial Rubber Market - Updated Report Scope

This comprehensive report delves into the intricate dynamics of the global industrial rubber market, offering a detailed analysis of its size, segmentation, key trends, and future growth prospects. The scope encompasses an in-depth examination of various types of industrial rubber, their diverse applications across multiple end-use industries, and the geographical spread of demand and supply. It provides a strategic framework for understanding market opportunities, challenges, drivers, and restraints, facilitating informed decision-making for stakeholders navigating this evolving landscape.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 45.2 Billion |

| Market Forecast in 2033 | USD 71.1 Billion |

| Growth Rate | 5.8% |

| Number of Pages | 255 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Michelin Group, Continental AG, Bridgestone Corporation, Sumitomo Rubber Industries, Ltd., Goodyear Tire & Rubber Company, Parker Hannifin Corporation, Freudenberg SE, Trelleborg AB, NOK Corporation, Hutchinson SA, Cooper Standard, Toyo Tire Corporation, Yokohama Rubber Co., Ltd., Dana Holding Corporation, Gates Corporation, Elastomer Products Private Limited, LANXESS AG, Synthos S.A., Kumho Petrochemical Co. Ltd., ZEON Corporation |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The industrial rubber market is meticulously segmented to provide a granular understanding of its diverse components and their respective contributions to the overall market landscape. This segmentation allows for precise analysis of demand patterns, technological preferences, and regional consumption trends, offering a comprehensive view for strategic planning. The primary segmentation dimensions include the type of rubber, the specific end-use industry utilizing these materials, and the broad application categories of the final products.

Further granularity is achieved by considering the form in which rubber is supplied, such as solid compounds, liquid formulations, or latex, each serving distinct manufacturing processes and product requirements. This multi-dimensional segmentation facilitates a detailed assessment of market niches, enabling stakeholders to identify high-potential areas for investment, product innovation, and market penetration strategies. Understanding these segments is crucial for manufacturers, suppliers, and investors aiming to capitalize on specific market opportunities and navigate the competitive landscape effectively.

- By Type: Natural Rubber, Synthetic Rubber (Styrene Butadiene Rubber (SBR), Ethylene Propylene Diene Monomer (EPDM), Butyl Rubber (IIR), Nitrile Butadiene Rubber (NBR), Silicone Rubber, Fluoroelastomers (FKM), Polybutadiene Rubber (PBR), Chloroprene Rubber (CR), Others).

- By End-Use Industry: Automotive & Transportation, Industrial Machinery & Equipment, Construction, Electrical & Electronics, Consumer Goods, Healthcare, Oil & Gas, Mining, Agriculture, Aerospace & Defense, Others.

- By Application: Hoses, Belts, Seals & Gaskets, Anti-Vibration Mounts, Molded Products, Extruded Products, Rollers, Adhesives & Sealants, Other Industrial Components.

- By Form: Solid, Liquid, Latex.

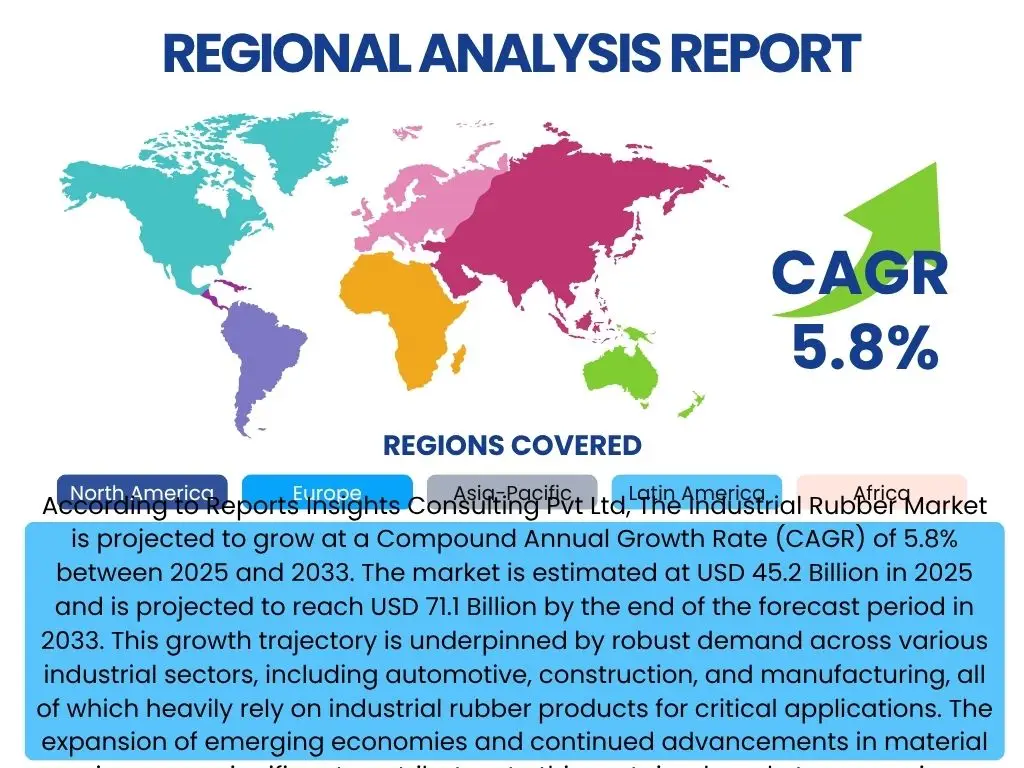

Regional Highlights

The industrial rubber market exhibits significant regional disparities in terms of demand, production capabilities, and growth dynamics. Asia Pacific (APAC) is projected to remain the dominant market, driven by its robust manufacturing sector, rapid industrialization, and substantial growth in automotive production, particularly in countries like China and India. The region's expanding infrastructure projects and increasing disposable incomes, which fuel demand for various consumer goods, further bolster the consumption of industrial rubber products. Localized production capabilities and access to raw materials also contribute to APAC's leading position.

North America and Europe represent mature markets characterized by stringent regulatory environments and a strong emphasis on high-performance and specialty elastomers. These regions are at the forefront of adopting advanced manufacturing technologies and sustainable rubber solutions, driven by innovation and environmental consciousness. While growth rates might be lower compared to APAC, the demand for sophisticated, durable, and customized rubber components in industries such as aerospace, healthcare, and precision engineering remains consistently high. Latin America, the Middle East, and Africa (MEA) are emerging as high-growth regions, propelled by industrial diversification, increasing foreign investments, and developing infrastructure, offering untapped potential for market expansion in the coming years.

- Asia Pacific: Dominant market share driven by industrialization, automotive production, and infrastructure development in China and India.

- North America: Significant demand for high-performance and specialty elastomers, driven by advanced manufacturing and aerospace industries.

- Europe: Focus on sustainable solutions and high-tech applications, with stringent regulatory frameworks influencing market trends.

- Latin America: Emerging growth spurred by industrial expansion and increasing investments in manufacturing and construction.

- Middle East & Africa: Growing opportunities due to diversification of economies, infrastructure projects, and developing industrial base.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Industrial Rubber Market.- Michelin Group

- Continental AG

- Bridgestone Corporation

- Sumitomo Rubber Industries, Ltd.

- Goodyear Tire & Rubber Company

- Parker Hannifin Corporation

- Freudenberg SE

- Trelleborg AB

- NOK Corporation

- Hutchinson SA

- Cooper Standard

- Toyo Tire Corporation

- Yokohama Rubber Co., Ltd.

- Dana Holding Corporation

- Gates Corporation

- Elastomer Products Private Limited

- LANXESS AG

- Synthos S.A.

- Kumho Petrochemical Co. Ltd.

- ZEON Corporation

Frequently Asked Questions

What is the projected growth rate of the Industrial Rubber Market?

The Industrial Rubber Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.8% between 2025 and 2033.

What are the primary drivers for the Industrial Rubber Market?

Key drivers include rapid industrialization and infrastructure development, growth in automotive production, and advancements in material science leading to demand for high-performance elastomers.

Which region holds the largest share in the Industrial Rubber Market?

Asia Pacific is expected to remain the largest market due to strong manufacturing bases and ongoing industrialization in countries like China and India.

How do environmental regulations impact the Industrial Rubber Market?

Stringent environmental regulations are a significant restraint, increasing production costs and driving demand for sustainable and eco-friendly rubber solutions, influencing R&D and market strategies.

What role does AI play in the Industrial Rubber Market?

AI is increasingly impacting the market through optimization of manufacturing processes, predictive maintenance, accelerated R&D for new materials, and improved supply chain management.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted