Industrial Dry Vacuum Cleaner Market

Industrial Dry Vacuum Cleaner Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_704212 | Last Updated : August 05, 2025 |

Format : ![]()

![]()

![]()

![]()

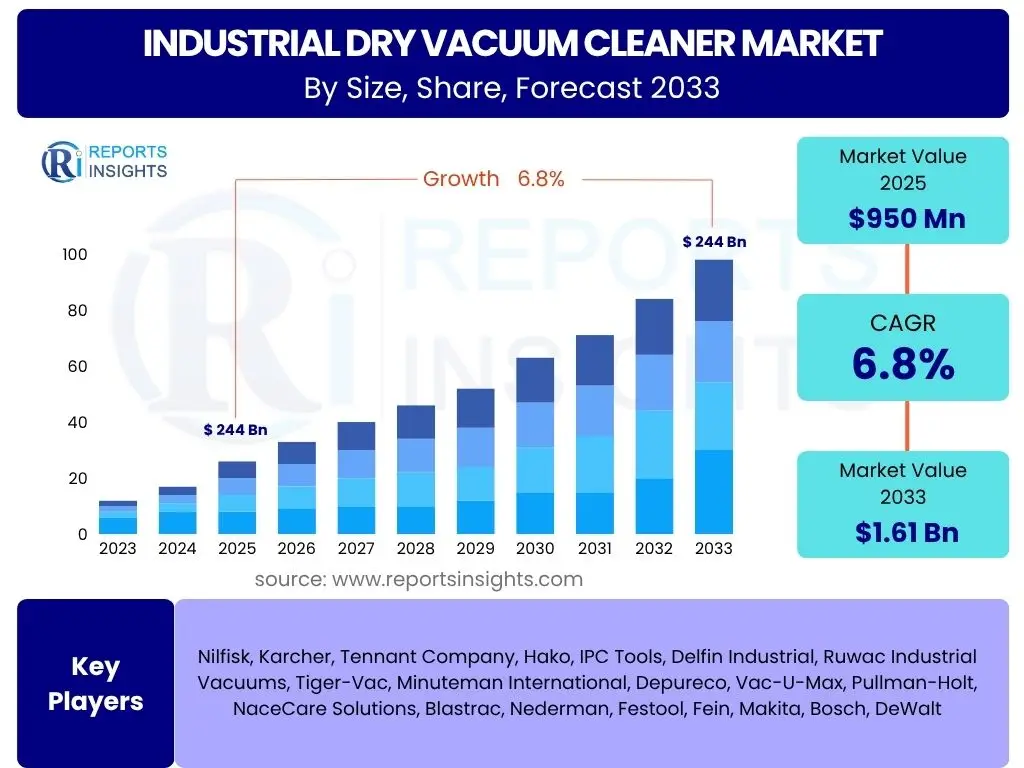

Industrial Dry Vacuum Cleaner Market Size

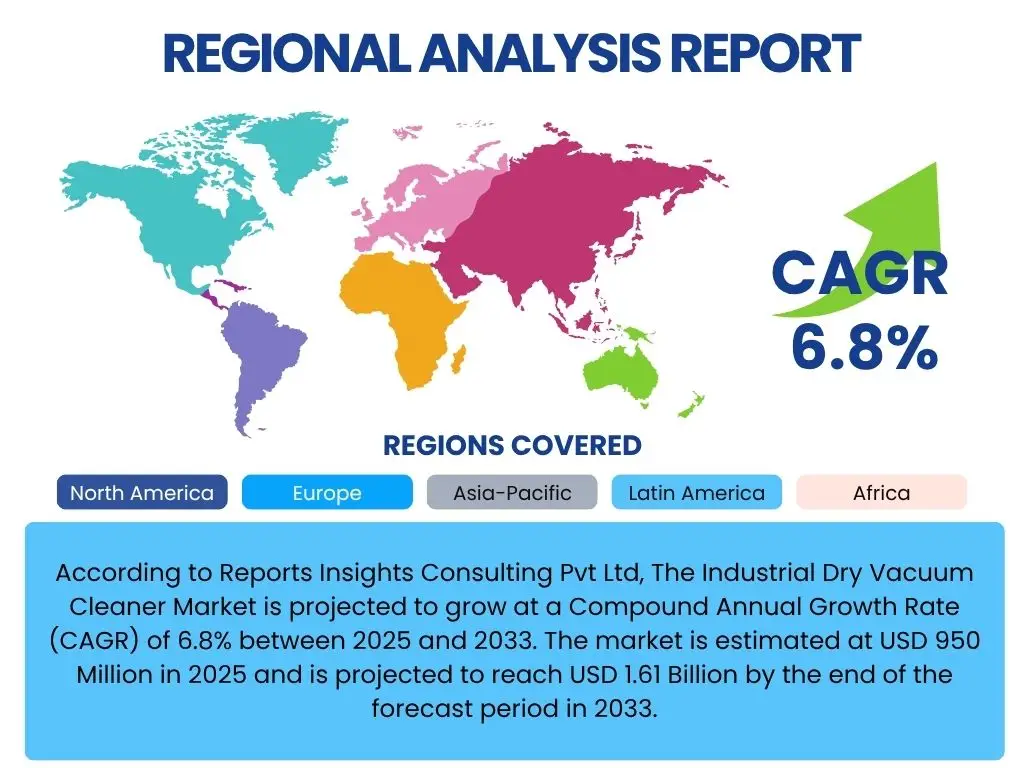

According to Reports Insights Consulting Pvt Ltd, The Industrial Dry Vacuum Cleaner Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2025 and 2033. The market is estimated at USD 950 Million in 2025 and is projected to reach USD 1.61 Billion by the end of the forecast period in 2033.

Key Industrial Dry Vacuum Cleaner Market Trends & Insights

The industrial dry vacuum cleaner market is experiencing significant shifts driven by technological innovation and evolving operational demands across various sectors. Users are actively seeking information on how new advancements are shaping the industry, particularly in terms of efficiency, connectivity, and specialization. Key themes include the integration of smart technologies, the demand for enhanced filtration systems, and the development of application-specific solutions that cater to the unique challenges of modern industrial environments. The focus is increasingly on solutions that not only improve cleanliness but also contribute to operational safety, productivity, and compliance with stringent industrial standards.

Furthermore, there is a growing interest in understanding how sustainability initiatives and ergonomic design principles are influencing product development. Industrial end-users are looking for durable, long-lasting equipment that reduces environmental impact and improves user comfort during extended operation. This holistic approach to product design and functionality is a defining characteristic of current market trends, reflecting a broader industry push towards more intelligent, eco-conscious, and user-centric cleaning solutions. The market is also seeing a diversification of power sources and form factors to meet a wider range of industrial needs, from compact portable units to large, integrated systems.

- Integration of IoT and Smart Features for remote monitoring and predictive maintenance.

- Increasing adoption of advanced filtration technologies, including HEPA and ULPA for enhanced air quality.

- Development of specialized vacuum cleaners for hazardous materials and sensitive environments (e.g., cleanrooms).

- Growing emphasis on ergonomic designs and lightweight materials to improve operator comfort and reduce fatigue.

- Shift towards battery-powered and cordless models for greater mobility and flexibility in large industrial spaces.

- Customization options for specific industry applications, such as manufacturing, pharmaceuticals, and food processing.

- Focus on energy efficiency and reduced noise levels in new product development.

AI Impact Analysis on Industrial Dry Vacuum Cleaner

The integration of Artificial Intelligence (AI) into industrial dry vacuum cleaner technology is a subject of growing interest, with users frequently inquiring about its potential to revolutionize cleaning operations. Common questions revolve around how AI can enhance vacuum performance, enable autonomous operation, and contribute to more efficient maintenance schedules. The primary expectation is that AI will move beyond basic automation, offering capabilities such as intelligent path planning, real-time debris identification, and adaptive cleaning protocols based on environmental sensing. This shift aims to reduce human intervention, optimize resource utilization, and improve overall cleaning effectiveness in complex industrial settings.

Concerns often center on the initial investment required for AI-enabled systems, data privacy, and the need for skilled personnel to manage and maintain these advanced machines. Despite these considerations, the market anticipates AI will play a crucial role in enabling predictive maintenance by analyzing usage patterns and identifying potential component failures before they occur, thereby minimizing downtime. Furthermore, AI could facilitate better energy management by optimizing power consumption based on cleaning needs and scheduling. The evolving landscape suggests a future where AI-powered industrial dry vacuum cleaners will not just clean, but intelligently manage and maintain cleanliness levels with minimal human oversight.

- Enables predictive maintenance through data analysis of usage patterns and component wear.

- Facilitates autonomous cleaning robots with intelligent navigation and obstacle avoidance.

- Optimizes vacuum power and suction based on real-time dirt detection and surface type.

- Improves operational efficiency by identifying optimal cleaning routes and schedules.

- Provides remote diagnostic capabilities and performance monitoring for troubleshooting.

- Contributes to better resource management, including energy consumption and filter lifespan.

Key Takeaways Industrial Dry Vacuum Cleaner Market Size & Forecast

The Industrial Dry Vacuum Cleaner market demonstrates robust growth, driven by increasing industrialization, stringent health and safety regulations, and continuous technological advancements. Users are keen to understand the core factors contributing to this market expansion and where the most significant opportunities lie. A key takeaway is the consistent demand for high-performance cleaning solutions across diverse industrial sectors, from manufacturing to healthcare, necessitating a broad range of specialized equipment. The market's resilience is also attributed to its critical role in maintaining operational efficiency and compliance in various production environments.

Another crucial insight is the growing emphasis on automation and smart features, which are not merely trends but essential components for future market competitiveness. The forecast period highlights a strong trajectory for adoption of more sophisticated systems that can integrate into broader industrial ecosystems. Investors and stakeholders should note the ongoing innovation in filtration technologies and the increasing preference for ergonomic, energy-efficient models. This indicates a market that is not only expanding in size but also evolving in complexity and sophistication to meet the advanced demands of modern industry.

- Steady market expansion driven by industrial growth and regulatory compliance.

- Increasing investment in advanced filtration technologies for superior air quality.

- Growing demand for specialized and application-specific industrial dry vacuum cleaners.

- Strong potential for growth in emerging economies due to developing industrial infrastructures.

- Technological advancements, including IoT and AI integration, will be key differentiators.

- Emphasis on sustainability and ergonomic design is shaping new product development.

Industrial Dry Vacuum Cleaner Market Drivers Analysis

The industrial dry vacuum cleaner market is significantly influenced by several key drivers that propel its growth and technological evolution. These drivers stem from fundamental shifts in global industrial practices, increasing regulatory pressures, and a heightened awareness of workplace safety and hygiene. The continuous expansion of manufacturing sectors worldwide, particularly in developing economies, creates a sustained demand for efficient and powerful cleaning equipment to maintain operational environments and product quality. Furthermore, the rising adoption of automation and precision manufacturing processes necessitates cleaner facilities to prevent equipment malfunction and product contamination.

Another major impetus is the global focus on occupational health and safety. Governments and regulatory bodies are implementing stricter standards for indoor air quality and dust control in industrial settings, compelling businesses to invest in high-performance vacuum systems capable of capturing fine particulate matter and hazardous substances. This regulatory environment not only boosts demand for advanced filtration systems, such as HEPA and ULPA, but also encourages the adoption of specialized vacuum cleaners for specific industrial applications, including those involving combustible dusts or toxic materials. The confluence of these factors ensures a consistent market trajectory.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Stricter Industrial Health & Safety Regulations | +1.5% | North America, Europe, Asia Pacific | Short to Medium Term (2025-2029) |

| Growth in Manufacturing and Industrial Sectors | +1.2% | Asia Pacific, Latin America, Middle East | Medium to Long Term (2027-2033) |

| Technological Advancements & Automation Integration | +1.0% | Global | Short to Medium Term (2025-2030) |

| Rising Demand for Cleanroom Applications | +0.8% | North America, Europe, China | Medium Term (2026-2031) |

| Increasing Awareness of Workplace Hygiene | +0.7% | Global | Short Term (2025-2028) |

Industrial Dry Vacuum Cleaner Market Restraints Analysis

Despite the positive growth trajectory, the industrial dry vacuum cleaner market faces several restraints that could impede its full potential. A primary limiting factor is the relatively high initial capital expenditure associated with high-performance industrial-grade vacuum cleaners, especially those equipped with advanced features like specialized filtration or autonomous capabilities. This cost can be a significant barrier for small and medium-sized enterprises (SMEs) or businesses operating on tighter budgets, leading them to opt for less capable or conventional cleaning methods that may not fully meet industrial standards. The long-term benefits of industrial vacuums, such as reduced labor costs and improved air quality, sometimes do not outweigh the immediate financial burden for some entities.

Another significant restraint is the availability of alternative cleaning methods and intense competition from conventional or multi-purpose cleaning equipment. While industrial dry vacuum cleaners offer specialized benefits, general-purpose vacuums or wet-dry vacuums might be perceived as sufficient for certain less demanding industrial applications, diluting the market share for specialized dry units. Furthermore, the complexity of maintenance and the requirement for skilled technicians to service advanced industrial vacuum systems can add to operational costs and present logistical challenges for end-users. Economic uncertainties and fluctuations in raw material prices also pose a threat, potentially impacting manufacturing costs and end-product pricing, thereby influencing purchasing decisions.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Initial Capital Investment | -0.9% | Global, particularly SMEs | Short to Medium Term (2025-2029) |

| Competition from Alternative Cleaning Methods | -0.7% | Global | Medium Term (2026-2031) |

| Maintenance Complexity and Service Costs | -0.5% | Global | Long Term (2028-2033) |

| Limited Awareness in Certain Emerging Markets | -0.4% | Latin America, Africa | Short Term (2025-2028) |

| Economic Slowdowns Affecting Industrial Spending | -0.3% | Global | Short to Medium Term (2025-2027) |

Industrial Dry Vacuum Cleaner Market Opportunities Analysis

The industrial dry vacuum cleaner market presents numerous opportunities for growth and innovation, driven by evolving industrial landscapes and emerging technological capabilities. A significant opportunity lies in the burgeoning industrialization and infrastructure development occurring in emerging economies across Asia Pacific, Latin America, and the Middle East. As these regions expand their manufacturing bases and adopt more sophisticated production processes, the demand for high-performance industrial cleaning equipment to ensure quality control and worker safety will inevitably rise. This demographic shift provides a vast untapped market for manufacturers and solution providers.

Furthermore, the increasing focus on sustainability and energy efficiency offers a fertile ground for product innovation. Manufacturers can capitalize on the growing corporate social responsibility (CSR) initiatives by developing eco-friendly industrial vacuum cleaners that consume less power and utilize recyclable materials. The expansion of smart factories and Industry 4.0 initiatives also creates opportunities for integrating industrial dry vacuum cleaners with broader IoT ecosystems, offering remote monitoring, predictive maintenance, and autonomous operation. Customized solutions tailored to niche industrial applications, such as pharmaceutical cleanrooms or hazardous waste management, represent another lucrative avenue, enabling manufacturers to differentiate their offerings and capture premium market segments.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Expansion in Emerging Industrial Economies | +1.3% | Asia Pacific, Latin America, Africa | Medium to Long Term (2027-2033) |

| Development of Eco-Friendly & Energy-Efficient Models | +1.0% | Global | Medium Term (2026-2031) |

| Integration with Smart Factory & IoT Ecosystems | +0.9% | North America, Europe, East Asia | Short to Medium Term (2025-2030) |

| Customization for Niche Industrial Applications | +0.8% | Global | Short Term (2025-2028) |

| After-Sales Service and Maintenance Contracts | +0.6% | Global | Long Term (2028-2033) |

Industrial Dry Vacuum Cleaner Market Challenges Impact Analysis

The industrial dry vacuum cleaner market faces several notable challenges that require strategic responses from manufacturers and stakeholders. Intense price competition, particularly from regional and local manufacturers offering more cost-effective solutions, exerts downward pressure on profit margins for established players. This competitive landscape necessitates continuous innovation and differentiation to justify premium pricing and maintain market share, compelling companies to invest heavily in research and development to stay ahead. Balancing advanced features with competitive pricing remains a critical hurdle for market participants.

Supply chain disruptions, as witnessed during recent global events, pose a significant challenge. Volatility in raw material prices, component shortages, and logistical complexities can severely impact production schedules and increase manufacturing costs. Ensuring a resilient and diversified supply chain is essential for mitigating these risks. Furthermore, the rapid pace of technological obsolescence demands continuous product updates and upgrades, which can strain R&D budgets and marketing efforts. Compliance with evolving international and regional safety standards, especially for hazardous material handling, also presents a complex regulatory burden for manufacturers operating in diverse geographical markets, requiring constant monitoring and adaptation of product specifications.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Intense Price Competition | -0.8% | Global | Short to Medium Term (2025-2029) |

| Supply Chain Disruptions and Raw Material Volatility | -0.6% | Global | Short Term (2025-2027) |

| Rapid Technological Obsolescence | -0.5% | Global | Medium Term (2026-2030) |

| Regulatory Compliance Burden (e.g., ATEX, OSHA) | -0.4% | Europe, North America | Long Term (2028-2033) |

| Skilled Labor Shortage for Operation & Maintenance | -0.3% | North America, Europe | Medium to Long Term (2027-2033) |

Industrial Dry Vacuum Cleaner Market - Updated Report Scope

This report provides a comprehensive analysis of the Industrial Dry Vacuum Cleaner Market, offering detailed insights into market dynamics, segmentation, regional trends, and competitive landscape. The scope encompasses a thorough examination of market drivers, restraints, opportunities, and challenges influencing industry growth from 2025 to 2033, building upon historical data from 2019 to 2023. It aims to furnish stakeholders with actionable intelligence to make informed strategic decisions regarding market entry, product development, and geographic expansion within this evolving sector.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 950 Million |

| Market Forecast in 2033 | USD 1.61 Billion |

| Growth Rate | 6.8% CAGR |

| Number of Pages | 245 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Nilfisk, Karcher, Tennant Company, Hako, IPC Tools, Delfin Industrial, Ruwac Industrial Vacuums, Tiger-Vac, Minuteman International, Depureco, Vac-U-Max, Pullman-Holt, NaceCare Solutions, Blastrac, Nederman, Festool, Fein, Makita, Bosch, DeWalt |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Industrial Dry Vacuum Cleaner Market is meticulously segmented to provide a granular view of its diverse landscape, enabling a deeper understanding of market dynamics and consumer preferences across various product types, technologies, filtration capabilities, power sources, applications, and end-use industries. This comprehensive segmentation allows stakeholders to identify specific growth areas and tailor their strategies to target particular market niches. Each segment represents distinct needs and operational requirements, from general debris collection to specialized hazardous material handling, reflecting the broad utility and adaptability of industrial vacuum solutions in different contexts.

Understanding these segments is crucial for manufacturers to innovate and develop products that precisely meet the demands of their target clientele. For instance, the distinction between corded and cordless technologies addresses varying mobility needs, while different filtration types cater to diverse air quality and safety standards. The application and end-use industry segments highlight the specialized nature of industrial cleaning, where a one-size-fits-all approach is often insufficient. This detailed market breakdown assists in forecasting demand, identifying competitive advantages, and formulating effective market entry and expansion strategies across the global industrial dry vacuum cleaner ecosystem.

- By Product Type: Upright, Canister, Backpack, Walk-behind, Ride-on

- By Technology: Corded, Cordless, Robotic/Autonomous

- By Filtration Type: HEPA, ULPA, Standard, Multi-stage

- By Power Source: Electric, Pneumatic, Battery

- By Application: General Cleaning, Hazardous Material Cleaning, Dust Collection, Liquid Spill Cleanup, Material Recovery

- By End-Use Industry: Manufacturing, Construction, Healthcare, Automotive, Food & Beverage, Pharmaceutical, Electronics, Woodworking, Metalworking, Logistics, Chemical, Mining

Regional Highlights

- North America: This region is characterized by high adoption of advanced cleaning technologies and stringent occupational safety regulations, particularly in manufacturing, healthcare, and electronics industries. The presence of key market players and a strong emphasis on automation contribute significantly to market growth.

- Europe: Driven by strict environmental and health standards (e.g., ATEX directives), Europe exhibits a strong demand for specialized and high-efficiency industrial dry vacuum cleaners. Germany, the UK, and France are prominent markets with significant industrial bases and a focus on sustainable cleaning solutions.

- Asia Pacific (APAC): Expected to witness the highest growth, APAC is fueled by rapid industrialization, expanding manufacturing sectors, and increasing foreign direct investment in countries like China, India, and Southeast Asian nations. Growing awareness of industrial hygiene and workplace safety also contributes to market expansion.

- Latin America: This region presents emerging opportunities with increasing industrial activities, particularly in Brazil and Mexico. Investment in infrastructure and manufacturing capabilities is gradually driving the demand for robust industrial cleaning equipment.

- Middle East and Africa (MEA): Growth in this region is propelled by investments in construction, oil & gas, and manufacturing sectors. The development of new industrial zones and a rising focus on occupational health and safety standards are creating new avenues for market penetration.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Industrial Dry Vacuum Cleaner Market.- Nilfisk

- Karcher

- Tennant Company

- Hako

- IPC Tools

- Delfin Industrial

- Ruwac Industrial Vacuums

- Tiger-Vac

- Minuteman International

- Depureco

- Vac-U-Max

- Pullman-Holt

- NaceCare Solutions

- Blastrac

- Nederman

- Festool

- Fein

- Makita

- Bosch

- DeWalt

Frequently Asked Questions

What is an Industrial Dry Vacuum Cleaner?

An industrial dry vacuum cleaner is a powerful, heavy-duty cleaning machine specifically designed for commercial and industrial environments to efficiently collect dry debris, dust, and fine particles. Unlike standard domestic vacuums, these units feature robust construction, larger capacities, enhanced filtration systems (e.g., HEPA, ULPA), and stronger suction capabilities to handle demanding industrial cleaning tasks, ensuring compliance with strict safety and hygiene standards in manufacturing, construction, and other sectors.

What are the primary benefits of using an Industrial Dry Vacuum Cleaner?

The primary benefits include superior cleaning efficiency for large areas and heavy debris, improved air quality through advanced filtration of fine and hazardous dust, enhanced workplace safety by reducing slip hazards and preventing dust explosions, increased operational uptime by keeping machinery clean, and compliance with stringent health and safety regulations. These vacuums significantly contribute to a healthier, safer, and more productive industrial environment.

How does an Industrial Dry Vacuum Cleaner differ from a regular vacuum cleaner?

Industrial dry vacuum cleaners are engineered for durability, power, and capacity, unlike regular household vacuums. They feature more robust motors, larger collection tanks, and specialized filtration systems capable of handling hazardous dust, fine particulates, and heavy debris. They are built for continuous, rigorous use in demanding environments, offering superior suction, longer operational life, and adherence to industrial safety standards that domestic models cannot provide.

What factors should be considered when selecting an Industrial Dry Vacuum Cleaner?

Key factors include the type and volume of debris (e.g., fine dust, heavy particles, hazardous materials), required filtration level (HEPA, ULPA), power source (electric, pneumatic, battery), capacity of the collection tank, mobility needs (portable, walk-behind, ride-on), noise levels, and specific industry regulations (e.g., ATEX for explosive atmospheres). Considering these elements ensures the selection of a unit that optimally matches the operational requirements and safety standards of the industrial environment.

What are the future trends shaping the Industrial Dry Vacuum Cleaner market?

Future trends include increased integration of IoT and AI for smart cleaning and predictive maintenance, a growing emphasis on autonomous and robotic cleaning solutions, continued development of advanced and specialized filtration technologies, expansion of ergonomic and battery-powered models for greater user convenience, and a rising focus on sustainable and energy-efficient designs. These trends reflect a market moving towards more intelligent, efficient, and environmentally conscious cleaning solutions.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted