Indoor Entertainment Center Market

Indoor Entertainment Center Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_703775 | Last Updated : August 05, 2025 |

Format : ![]()

![]()

![]()

![]()

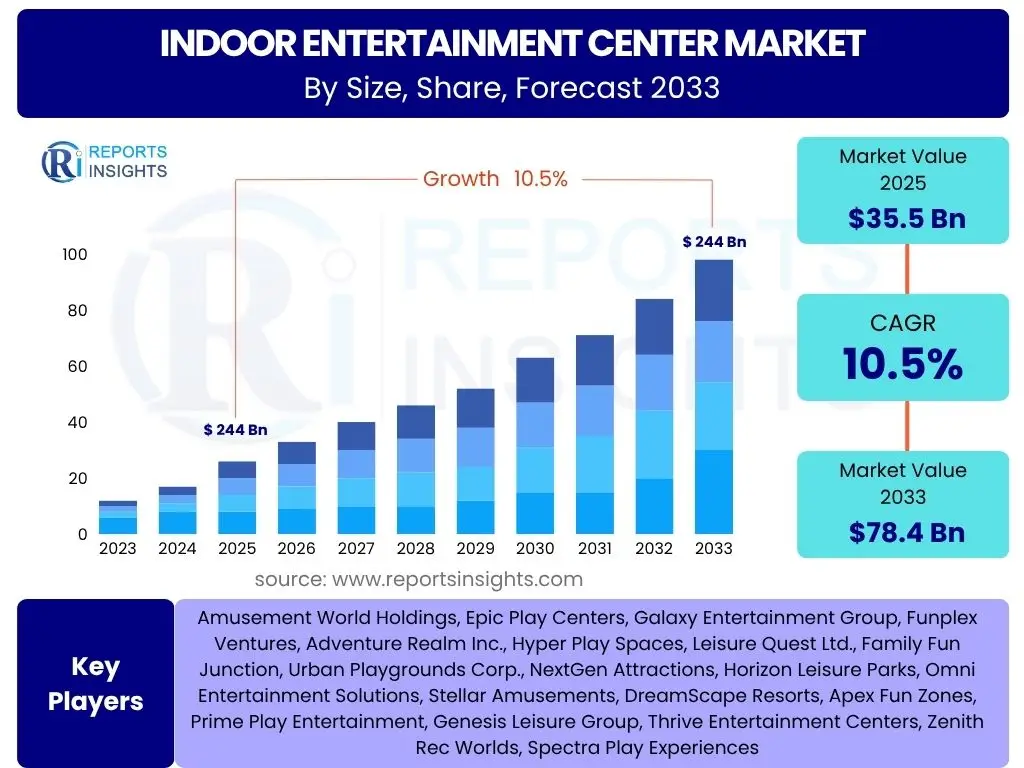

Indoor Entertainment Center Market Size

According to Reports Insights Consulting Pvt Ltd, The Indoor Entertainment Center Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 10.5% between 2025 and 2033. The market is estimated at USD 35.5 Billion in 2025 and is projected to reach USD 78.4 Billion by the end of the forecast period in 2033.

Key Indoor Entertainment Center Market Trends & Insights

The Indoor Entertainment Center market is undergoing significant transformation, driven by evolving consumer expectations for immersive and unique experiences. Users are increasingly seeking entertainment options that go beyond traditional arcades, embracing advanced technologies and diverse activity offerings. Key inquiries from the market highlight a strong interest in how centers are integrating virtual reality, augmented reality, and gamified social experiences to enhance visitor engagement. There is also a notable trend towards multi-generational appeal, with centers designing spaces and activities that cater to families and various age groups, fostering shared experiences. Furthermore, the emphasis on digital integration for seamless booking, personalized content delivery, and loyalty programs indicates a shift towards a more technologically sophisticated and user-centric operational model.

Another prominent trend observed is the growing demand for interactive and educational play, particularly for younger demographics. Parents are seeking environments where children can not only be entertained but also learn and develop new skills through playful engagement. This has led to the emergence of edutainment centers and activity-based learning zones within larger entertainment venues. Additionally, the market is seeing a rise in themed entertainment concepts, where entire centers are designed around a specific narrative or universe, providing a cohesive and deeply immersive experience. These themes often leverage popular culture, fantasy, or adventure elements to attract and retain visitors, creating a strong sense of escapism and novelty. The focus on customizable party packages and event hosting is also a significant trend, catering to social gatherings and celebrations, thereby diversifying revenue streams for these centers.

- Immersive Technology Integration: Widespread adoption of VR, AR, and interactive digital displays for enhanced gameplay.

- Multi-Generational Appeal: Design and activity offerings catering to diverse age groups, from young children to adults.

- Edutainment and Active Play: Increased focus on learning-through-play concepts and physical activity zones.

- Themed Entertainment: Development of centers around specific narratives, characters, or popular cultural franchises.

- Personalized Experiences: Use of data analytics and smart systems for customized visitor journeys and loyalty programs.

- Social and Competitive Gaming: Expansion of esports lounges, competitive gaming areas, and group challenge rooms.

- Hybrid Business Models: Combination of entertainment, dining, retail, and event spaces to maximize visitor spend.

- Health and Safety Emphasis: Implementation of advanced hygiene protocols and contactless solutions post-pandemic.

AI Impact Analysis on Indoor Entertainment Center

The integration of Artificial Intelligence (AI) within the Indoor Entertainment Center market is a topic of significant user interest, primarily focusing on its potential to revolutionize customer experience and operational efficiency. Common user questions revolve around how AI can personalize visitor interactions, from dynamic pricing based on demand to customized game recommendations. Users also inquire about AI's role in streamlining back-end operations, such as predictive maintenance for rides and equipment, optimizing staffing levels, and managing inventory. The overarching expectation is that AI will enable centers to offer more responsive, intuitive, and memorable experiences while simultaneously driving down operational costs and improving profitability.

Furthermore, there is keen interest in AI's capacity to create novel forms of entertainment. This includes AI-powered characters or simulations that interact dynamically with guests, adaptive game difficulties that adjust to individual skill levels, and generative AI for creating unique visual or auditory environments. Security and guest flow management are also areas where users anticipate AI will play a crucial role, utilizing computer vision for crowd analysis, anomaly detection, and enhancing overall safety. The discussions often highlight the balance between leveraging AI for technological advancement and maintaining the human element that contributes to the social and communal aspects of indoor entertainment.

- Personalized Guest Experiences: AI algorithms for tailored game recommendations, dynamic pricing, and customized content delivery.

- Operational Efficiency: AI-driven predictive maintenance for equipment, optimized staffing, and enhanced inventory management.

- Enhanced Security and Safety: AI-powered surveillance, crowd monitoring, and anomaly detection for improved venue safety.

- Interactive and Adaptive Gaming: AI-driven non-player characters, adaptive difficulty levels, and personalized challenges.

- Customer Service Automation: AI chatbots for FAQ, booking assistance, and real-time support.

- Data Analytics and Insights: AI for processing visitor data to understand preferences, peak times, and popular attractions, informing strategic decisions.

- Marketing and Promotion Optimization: AI-driven analysis of customer behavior for targeted advertising campaigns and promotional offers.

- New Content Creation: Generative AI tools assisting in the creation of unique digital environments, game scenarios, and soundscapes.

Key Takeaways Indoor Entertainment Center Market Size & Forecast

The Indoor Entertainment Center market is poised for robust expansion, indicating significant opportunities for investment and innovation over the next decade. Key user inquiries about market size and forecast often focus on identifying high-growth segments and regions, as well as understanding the underlying factors driving this growth. The consistent double-digit CAGR suggests a strong consumer appetite for out-of-home entertainment experiences, particularly those offering novelty, social interaction, and technological sophistication. This growth trajectory is supported by demographic shifts, increasing urbanization, and a continuous desire for unique leisure activities that provide a break from daily routines and digital screens at home.

Furthermore, the market's projected value reaching nearly double its current size within the forecast period underscores the importance of strategic planning for existing and new entrants. Key takeaways emphasize the necessity for businesses to adapt quickly to evolving consumer preferences, particularly concerning technology integration and experiential diversity. Operators who invest in advanced attractions, personalized services, and flexible business models are likely to capture a larger share of this expanding market. The forecast also highlights the resilience of the indoor entertainment sector, even in the face of economic fluctuations, as consumers prioritize leisure and family-oriented activities.

- Significant Growth Potential: The market is projected to more than double in size by 2033, indicating strong investor confidence and consumer demand.

- Experiential Focus: Growth is primarily driven by centers offering unique, immersive, and technology-driven experiences.

- Strategic Investment Required: Success necessitates continuous investment in new attractions, technology upgrades, and facility enhancements.

- Diversification of Offerings: Multi-faceted centers combining entertainment, F&B, and event hosting will lead the market.

- Consumer Behavior Shift: Increased preference for shared social experiences and active entertainment over passive alternatives.

- Regional Disparities: Growth will vary by region, with emerging economies and densely populated urban areas showing accelerated expansion.

- Technology as a Catalyst: Integration of AI, VR, AR, and IoT is crucial for market competitiveness and future innovation.

Indoor Entertainment Center Market Drivers Analysis

The Indoor Entertainment Center market is significantly propelled by several key drivers that reflect contemporary consumer preferences and societal trends. A primary driver is the increasing demand for out-of-home entertainment experiences that offer a break from digital consumption at home and foster social interaction. As urban populations grow and living spaces shrink, indoor entertainment centers provide accessible, weather-independent venues for leisure activities. Consumers are actively seeking novel and immersive experiences that cannot be replicated at home, leading to a surge in demand for facilities incorporating virtual reality, augmented reality, and other interactive technologies. This drive for unique experiences encourages centers to continuously innovate and upgrade their offerings, thereby sustaining market momentum and attracting diverse visitor segments.

Another significant driver is the rising disposable income in various regions, particularly in developing economies, enabling consumers to allocate more budget towards leisure and entertainment. This economic factor, coupled with the growing trend of families seeking shared recreational activities, contributes substantially to market expansion. The increasing focus on experiential consumption, where consumers prioritize experiences over material possessions, further fuels the market. Additionally, the strategic location of many indoor entertainment centers within shopping malls or mixed-use developments ensures high footfall and accessibility, turning them into convenient destinations for family outings, social gatherings, and corporate events. The consistent evolution of technology, making advanced gaming and simulation experiences more affordable and engaging, also acts as a crucial enabler for market growth.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Demand for Experiential Entertainment | +3.0% | Global, particularly North America, Europe, Asia Pacific | Short to Long Term |

| Rising Disposable Income and Urbanization | +2.5% | Asia Pacific, Latin America, Middle East | Medium to Long Term |

| Technological Advancements (VR, AR, Gamification) | +2.0% | Global, developed economies leading | Short to Medium Term |

| Growth in Family Entertainment and Social Outings | +1.5% | Global | Short to Long Term |

Indoor Entertainment Center Market Restraints Analysis

Despite the promising growth trajectory, the Indoor Entertainment Center market faces several significant restraints that could impact its expansion. A primary challenge is the substantial initial capital investment required for establishing and maintaining a state-of-the-art entertainment center. This includes costs associated with property acquisition or lease, construction, purchasing advanced gaming equipment, safety installations, and interior design. Such high entry barriers can deter new entrants and limit the pace of expansion for existing players, particularly smaller businesses. Furthermore, the operational costs, including maintenance, utilities, staffing, and continuous content updates, also pose a considerable financial burden, impacting profitability and sustainability.

Another notable restraint is the intense competition from alternative entertainment options, particularly the burgeoning home entertainment market. The widespread availability of high-quality streaming services, advanced home gaming consoles, virtual reality headsets, and online multiplayer platforms provides consumers with convenient and often more affordable entertainment within their own homes. This ease of access can reduce the frequency of visits to indoor entertainment centers, especially for younger demographics. Additionally, economic uncertainties, such as inflation or recessions, can lead to reduced discretionary spending on leisure activities, directly impacting visitor numbers and revenue for entertainment centers. The rapid obsolescence of technology also acts as a restraint, as centers must constantly invest in upgrades to remain appealing and competitive, leading to continuous capital expenditure and potential write-offs of older equipment.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Initial Investment and Operational Costs | -2.0% | Global | Long Term |

| Intense Competition from Home Entertainment | -1.5% | North America, Europe, Asia Pacific (developed markets) | Short to Medium Term |

| Rapid Technological Obsolescence | -1.0% | Global | Short Term |

| Economic Downturns and Reduced Discretionary Spending | -1.0% | Global, varying by regional economic stability | Short Term |

Indoor Entertainment Center Market Opportunities Analysis

The Indoor Entertainment Center market is ripe with opportunities that can significantly accelerate its growth trajectory. A major opportunity lies in the continuous innovation and integration of advanced technologies like virtual reality (VR), augmented reality (AR), and artificial intelligence (AI). These technologies enable the creation of highly immersive, personalized, and interactive experiences that cannot be replicated at home, thereby attracting a new generation of tech-savvy consumers. The development of next-generation VR attractions, full-body tracking systems, and AI-powered interactive characters presents avenues for centers to differentiate themselves and offer truly unique entertainment propositions. Furthermore, the increasing accessibility and affordability of these technologies will lower the barrier for adoption, making them viable for a broader range of centers.

Another significant opportunity is the expansion into untapped or underserved markets, particularly in emerging economies with growing middle-class populations and increasing urbanization rates. Regions such as Asia Pacific, Latin America, and parts of the Middle East and Africa present considerable potential for new indoor entertainment center development, as consumer leisure spending rises. Strategic partnerships with real estate developers, shopping mall operators, and tourism boards can facilitate this expansion. Additionally, the diversification of revenue streams beyond ticket sales offers a robust opportunity. This includes integrating premium food and beverage services, merchandise sales, hosting corporate events, private parties, and educational programs. Developing subscription models or loyalty programs can also foster repeat visits and enhance customer lifetime value, contributing to sustained growth and profitability for operators.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Integration of Advanced Immersive Technologies (VR/AR/AI) | +3.5% | Global | Short to Long Term |

| Expansion into Emerging and Underserved Markets | +2.8% | Asia Pacific, Latin America, Middle East & Africa | Medium to Long Term |

| Diversification of Revenue Streams (F&B, Events, Merchandise) | +2.2% | Global | Short to Medium Term |

| Strategic Partnerships and Collaborations | +1.5% | Global | Medium Term |

Indoor Entertainment Center Market Challenges Impact Analysis

The Indoor Entertainment Center market faces several challenges that require strategic navigation to maintain growth and profitability. One significant challenge is the rapid pace of technological advancements, which can lead to quick obsolescence of existing attractions and necessitate continuous, substantial investment in upgrades. Consumers constantly seek novelty, and centers must regularly introduce new games, experiences, and equipment to remain competitive and avoid visitor fatigue. This demand for constant innovation strains operational budgets and can be a barrier for smaller operators lacking significant capital reserves. The risk of investing in technologies that may not achieve widespread adoption or quickly become outdated further complicates strategic planning.

Another critical challenge is maintaining visitor engagement and ensuring repeat visits amidst a fragmented entertainment landscape. While initial novelty might attract visitors, sustaining their interest requires more than just new attractions; it demands exceptional customer service, a clean and safe environment, and a strong sense of community or belonging. Managing peak hours, staffing adequately, and ensuring smooth operational flow without long queues are persistent operational hurdles. Furthermore, health and safety concerns, especially post-pandemic, remain paramount. Operators face the challenge of implementing and communicating robust hygiene protocols, managing crowd density, and adapting to evolving public health guidelines, which can add to operational complexities and potentially deter some visitors. The increasing consumer demand for personalized experiences also poses a challenge for centers, as it requires sophisticated data management and adaptable service delivery models.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Maintaining Novelty and Continuous Innovation | -1.8% | Global | Short to Medium Term |

| High Operational Costs and Maintenance | -1.2% | Global | Long Term |

| Intensifying Competition and Market Saturation | -1.0% | North America, Europe | Medium Term |

| Ensuring Health, Safety, and Regulatory Compliance | -0.8% | Global, varying by local regulations | Short Term |

Indoor Entertainment Center Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the Indoor Entertainment Center market, covering historical data, current market dynamics, and future projections from 2025 to 2033. The scope includes a detailed examination of market size, growth drivers, restraints, opportunities, and challenges across various segments and key regions. It aims to offer strategic insights for stakeholders, including investors, market players, and new entrants, enabling informed decision-making in this rapidly evolving entertainment landscape. The report also integrates an analysis of the impact of emerging technologies like Artificial Intelligence on the sector.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 35.5 Billion |

| Market Forecast in 2033 | USD 78.4 Billion |

| Growth Rate | 10.5% |

| Number of Pages | 255 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Amusement World Holdings, Epic Play Centers, Galaxy Entertainment Group, Funplex Ventures, Adventure Realm Inc., Hyper Play Spaces, Leisure Quest Ltd., Family Fun Junction, Urban Playgrounds Corp., NextGen Attractions, Horizon Leisure Parks, Omni Entertainment Solutions, Stellar Amusements, DreamScape Resorts, Apex Fun Zones, Prime Play Entertainment, Genesis Leisure Group, Thrive Entertainment Centers, Zenith Rec Worlds, Spectra Play Experiences |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Indoor Entertainment Center market is segmented across various dimensions to provide a granular understanding of its diverse landscape and consumer preferences. These segmentations are critical for market players to identify niche opportunities, tailor their offerings, and develop targeted marketing strategies. Analyzing the market by activity type allows for understanding the popularity and revenue generation capabilities of different entertainment forms, from traditional arcade games to cutting-edge virtual reality experiences. The revenue model segmentation sheds light on consumer spending habits and preferred payment structures, whether pay-per-play, timed, or membership-based. Understanding the target age group is crucial for designing age-appropriate attractions and marketing campaigns, ensuring that centers cater effectively to children, teenagers, adults, or families as a whole.

Further segmentation by facility size helps categorize centers from small, local venues to large, mega-complexes, each with distinct operational requirements and market reach. This enables an assessment of the scalability and investment needed for different operational models. The ownership model differentiates between franchised, independent, and corporate-owned centers, providing insights into market consolidation, expansion strategies, and competitive dynamics. Each segment offers unique insights into consumer behavior, operational efficiencies, and market potential, guiding strategic decisions for both new entrants and established players in the indoor entertainment industry. This detailed breakdown facilitates a more precise market analysis and forecasting, identifying lucrative sub-segments and areas for growth.

- Activity Type:

- Arcade Games: Classic and modern video games, redemption games, prize games.

- VR & AR Games: Immersive virtual reality experiences, augmented reality interactive games, VR escape rooms.

- Sports & Physical Activities: Trampoline parks, climbing walls, laser tag, mini-golf, indoor sports simulators, bowling alleys.

- Edutainment: Interactive exhibits, STEM-focused play areas, educational workshops, discovery zones.

- Party & Events: Dedicated spaces for birthday parties, corporate events, private gatherings, team-building activities.

- Others: Escape rooms, soft play areas, interactive digital playgrounds, themed experiences.

- Revenue Model:

- Pay-per-play: Individual payment for each game or activity.

- Timed Play: Unlimited access to attractions for a specific duration.

- Membership/Subscription: Recurring fees for unlimited or discounted access.

- Hybrid: Combination of pay-per-play with timed or membership options.

- Target Age Group:

- Children (0-12): Soft play, age-appropriate arcade games, edutainment zones.

- Teenagers (13-17): Laser tag, VR games, competitive sports simulators, esports lounges.

- Adults (18+): Premium VR experiences, social gaming, escape rooms, adult-focused arcade games, F&B integration.

- Families: Mixed attractions appealing to all age groups, party packages.

- Facility Size:

- Small: Less than 10,000 sq ft, typically focused on a few core activities.

- Medium: 10,000 - 30,000 sq ft, offering a broader range of activities.

- Large: 30,000 - 100,000 sq ft, often multi-attraction venues.

- Mega: Over 100,000 sq ft, comprehensive entertainment complexes with diverse offerings.

- Ownership Model:

- Franchised: Operated under a brand license.

- Independent: Privately owned and operated single or multiple locations.

- Corporate-owned: Managed directly by a larger entertainment or leisure group.

Regional Highlights

- North America: North America represents a mature yet highly innovative market for Indoor Entertainment Centers, characterized by high consumer spending power and a strong culture of leisure and family entertainment. The region leads in the adoption of cutting-edge technologies like VR and AR, with centers continually investing in immersive experiences to cater to a tech-savvy audience. Urbanization and the presence of large suburban populations drive demand for accessible, high-quality indoor entertainment options. The market here is highly competitive, with a mix of large corporate chains and independent operators, focusing on diversified offerings including upscale F&B, event hosting, and premium experiences. Consumer preferences lean towards personalized experiences and venues that offer a blend of physical activity and digital interaction.

- Europe: The European Indoor Entertainment Center market is diverse, reflecting the varying cultural preferences and economic conditions across its sub-regions. Western European countries exhibit high demand for sophisticated and themed entertainment centers, often integrated with retail and dining concepts. There is a strong emphasis on family-friendly venues and activities that promote social interaction. Eastern Europe, while a developing market, shows significant growth potential driven by increasing disposable incomes and a growing interest in modern entertainment forms. Regulatory frameworks concerning safety and accessibility are stringent across Europe, requiring operators to adhere to high standards. Sustainability and environmentally conscious operations are also increasingly becoming a factor in consumer choice within this region.

- Asia Pacific (APAC): The Asia Pacific region is the fastest-growing market for Indoor Entertainment Centers, fueled by rapid urbanization, a burgeoning middle class, and high population density. Countries like China, India, and Southeast Asian nations are witnessing significant investments in large-scale entertainment complexes and themed attractions. There is a strong demand for immersive experiences, driven by a young and digitally native population. Edutainment centers and facilities focusing on skill development are particularly popular among parents. Strategic partnerships and localization of content are key trends in this highly dynamic market. Cultural nuances often influence the type and theme of entertainment offerings, leading to a vibrant and diverse market landscape.

- Latin America: The Latin American Indoor Entertainment Center market is experiencing steady growth, propelled by increasing urbanization, rising disposable incomes, and a youthful demographic. Brazil and Mexico are leading markets, with significant opportunities for new center development, particularly in metropolitan areas. Family-oriented entertainment and centers offering a mix of physical activities and arcade games are popular. While the adoption of advanced technologies is emerging, there's still a strong demand for traditional entertainment options. Investment in infrastructure and adapting business models to local economic conditions are crucial for success in this region. The market is also seeing a rise in franchised operations, bringing established international brands to the region.

- Middle East and Africa (MEA): The MEA region, particularly the Gulf Cooperation Council (GCC) countries, is a rapidly expanding market for Indoor Entertainment Centers, driven by significant government investments in tourism and entertainment infrastructure. High disposable incomes, a young population, and extreme climate conditions making indoor options highly appealing are key drivers. There is a strong preference for luxury, high-tech, and globally recognized entertainment concepts. Africa presents emerging opportunities, with increasing urbanization and a growing consumer class. However, varied economic development and infrastructure challenges exist across the African continent. The market in MEA is characterized by large-scale, often themed, entertainment venues that aim to attract both local residents and international tourists.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Indoor Entertainment Center Market.- Amusement World Holdings

- Epic Play Centers

- Galaxy Entertainment Group

- Funplex Ventures

- Adventure Realm Inc.

- Hyper Play Spaces

- Leisure Quest Ltd.

- Family Fun Junction

- Urban Playgrounds Corp.

- NextGen Attractions

- Horizon Leisure Parks

- Omni Entertainment Solutions

- Stellar Amusements

- DreamScape Resorts

- Apex Fun Zones

- Prime Play Entertainment

- Genesis Leisure Group

- Thrive Entertainment Centers

- Zenith Rec Worlds

- Spectra Play Experiences

Frequently Asked Questions

What is the projected growth rate of the Indoor Entertainment Center market?

The Indoor Entertainment Center market is projected to grow at a Compound Annual Growth Rate (CAGR) of 10.5% between 2025 and 2033, indicating robust expansion.

What key trends are shaping the Indoor Entertainment Center market?

Key trends include the integration of immersive technologies like VR and AR, a focus on multi-generational appeal, the rise of edutainment, and the development of themed entertainment concepts.

How is AI impacting the Indoor Entertainment Center industry?

AI is impacting the industry through personalized guest experiences, enhanced operational efficiency, improved security, and the creation of more interactive and adaptive gaming environments.

Which regions offer the most significant growth opportunities for Indoor Entertainment Centers?

Asia Pacific, Latin America, and the Middle East and Africa regions are identified as key areas for significant growth opportunities due to rising disposable incomes and urbanization.

What are the main challenges faced by Indoor Entertainment Centers?

Major challenges include the need for continuous innovation to maintain novelty, high operational and maintenance costs, intense competition, and ensuring stringent health and safety standards.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted