Data Center Liquid Cooling Market

Data Center Liquid Cooling Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_704439 | Last Updated : August 05, 2025 |

Format : ![]()

![]()

![]()

![]()

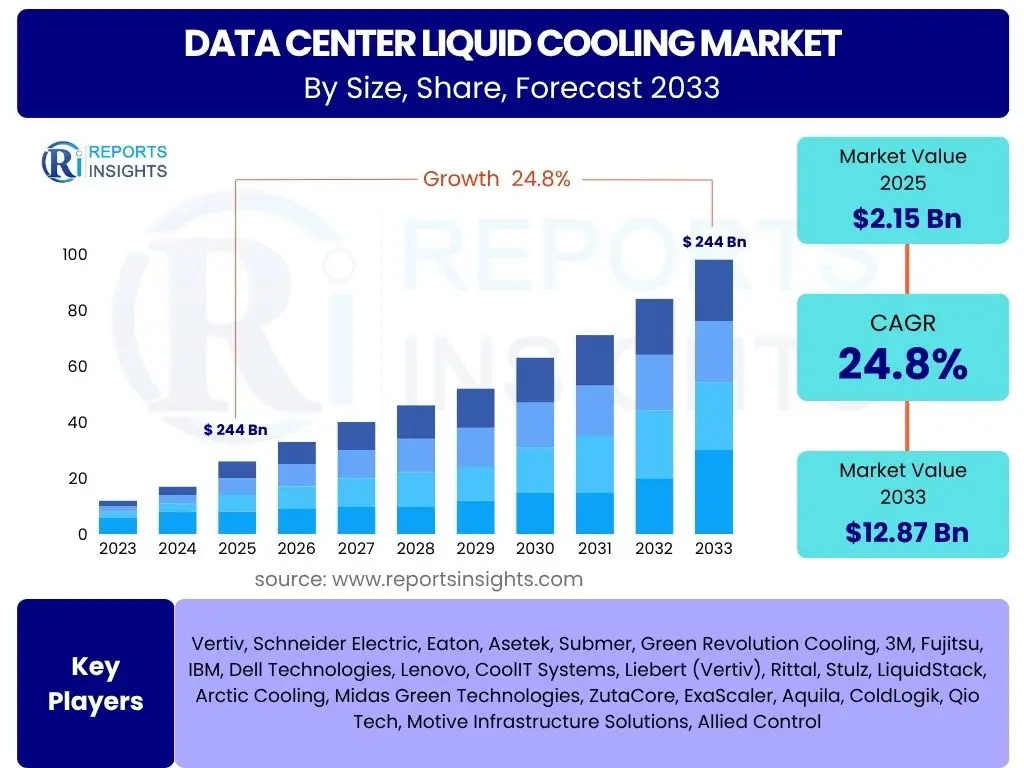

Data Center Liquid Cooling Market Size

According to Reports Insights Consulting Pvt Ltd, The Data Center Liquid Cooling Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 24.8% between 2025 and 2033. The market is estimated at USD 2.15 Billion in 2025 and is projected to reach USD 12.87 Billion by the end of the forecast period in 2033. This significant expansion is primarily driven by the escalating demand for high-density computing infrastructure, particularly with the proliferation of artificial intelligence (AI), machine learning (ML), and high-performance computing (HPC) workloads.

The imperative for enhanced energy efficiency and reduced operational expenditure (OpEx) also contributes substantially to this growth. As data centers continue to consume vast amounts of energy, traditional air-cooling methods are proving increasingly insufficient and costly for modern, densely packed server racks. Liquid cooling solutions offer a compelling alternative, capable of removing heat more effectively and often with a lower Power Usage Effectiveness (PUE) ratio, thereby enabling organizations to meet sustainability goals and manage rising energy costs.

Key Data Center Liquid Cooling Market Trends & Insights

User queries regarding data center liquid cooling trends frequently focus on the adoption drivers, technological advancements, and the overall shift from traditional cooling methods. Analysis reveals a clear trajectory towards more efficient, sustainable, and higher-density cooling solutions. Users are keenly interested in understanding how liquid cooling addresses the challenges posed by escalating heat loads from advanced processors and accelerated computing architectures. The increasing emphasis on environmental sustainability and carbon footprint reduction is also a prominent theme, driving interest in solutions that offer improved energy efficiency and lower operational costs.

The market is currently witnessing a paradigm shift from traditional air-cooling techniques to various liquid cooling methodologies. This transition is not merely about managing heat but also about optimizing data center footprint, enhancing equipment lifespan, and achieving ambitious sustainability targets. Hyperscale operators and enterprises deploying AI-intensive workloads are leading this adoption, setting precedents for the broader industry. Furthermore, the development of advanced cooling fluids and modular, scalable liquid cooling systems are key areas of innovation that frequently capture user attention, signaling a maturing market with diverse solution offerings.

- Increasing adoption of direct-to-chip liquid cooling for high-performance processors.

- Growing popularity of immersion cooling solutions (single-phase and two-phase) for ultra-dense deployments.

- Strong emphasis on energy efficiency and sustainability driving liquid cooling implementations.

- Development of modular and pre-fabricated liquid cooling infrastructure.

- Integration of advanced liquid cooling solutions with renewable energy sources.

- Rise of hybrid cooling systems combining air and liquid methodologies.

- Standardization efforts for liquid cooling components and interfaces.

- Enhanced monitoring and control systems for liquid cooling environments.

AI Impact Analysis on Data Center Liquid Cooling

Common user questions regarding AI's impact on Data Center Liquid Cooling primarily revolve around the increased thermal demands of AI/ML workloads and the necessity of specialized cooling solutions. Users seek to understand if existing cooling infrastructure can support the extreme heat generated by AI accelerators like GPUs and TPUs, and whether liquid cooling is becoming a mandatory requirement rather than an option. There is also significant interest in the cost implications and return on investment (ROI) associated with deploying liquid cooling for AI-driven data centers, alongside concerns about the complexity of integrating these advanced systems into current IT environments.

The proliferation of artificial intelligence, machine learning, and deep learning models is fundamentally reshaping data center infrastructure, placing unprecedented demands on cooling systems. AI accelerators generate significantly higher heat loads per rack unit compared to traditional CPUs, often exceeding the capabilities of conventional air cooling. This necessitates a shift towards more efficient and effective cooling methods, with liquid cooling emerging as the predominant solution. The energy efficiency and heat dissipation capabilities of liquid cooling make it indispensable for supporting the intense computational power and high-density deployments required for cutting-edge AI applications, thereby driving significant investment and innovation in this market segment.

- AI workloads generate extreme heat densities (e.g., 50 kW per rack or more), making air cooling insufficient.

- Liquid cooling is essential for maintaining optimal operating temperatures for AI accelerators (GPUs, TPUs).

- Increased adoption of direct-to-chip and immersion cooling specifically for AI/HPC clusters.

- Liquid cooling enables higher rack densities, optimizing data center footprint for AI infrastructure.

- Improved energy efficiency and reduced PUE for AI-intensive operations through liquid cooling.

- Minimizes thermal throttling, ensuring sustained peak performance of AI hardware.

- Accelerates the transition from traditional air-cooled facilities to advanced liquid-cooled designs.

Key Takeaways Data Center Liquid Cooling Market Size & Forecast

User queries concerning key takeaways from the Data Center Liquid Cooling market size and forecast often focus on the market's long-term viability, investment opportunities, and the critical factors driving its projected growth. There's a strong desire to understand the primary forces that will shape the market over the next decade, including technological advancements, regulatory pressures, and evolving data center demands. Users are also interested in identifying the segments with the highest growth potential and the overall strategic implications for data center operators and technology providers.

The market is poised for robust expansion, driven predominantly by the escalating thermal demands of high-performance computing, artificial intelligence, and hyperscale cloud environments. The increasing global focus on energy efficiency and environmental sustainability further cements liquid cooling's position as a critical infrastructure component. While initial investment costs and complexity remain considerations, the long-term benefits in terms of operational efficiency, space optimization, and enhanced performance are compelling. The market is transitioning from a niche solution to a mainstream necessity, presenting significant opportunities for innovation and widespread adoption across various end-user segments.

- Projected strong double-digit CAGR (24.8%) indicates rapid market expansion.

- High-density computing and AI/ML adoption are primary growth accelerators.

- Energy efficiency and sustainability mandates are driving widespread liquid cooling deployment.

- Immersion cooling and direct-to-chip technologies are leading the innovation curve.

- Hyperscale and colocation data centers are key early adopters and growth drivers.

- Significant investment opportunities exist across the value chain, from hardware to services.

- The market is maturing, with increasing standardization efforts and broader solution availability.

Data Center Liquid Cooling Market Drivers Analysis

The increasing power density of modern data center equipment, particularly servers housing advanced processors for AI, machine learning, and high-performance computing, is a paramount driver for the liquid cooling market. As rack power densities frequently exceed 20 kW and are projected to reach 50 kW or more, traditional air cooling struggles to efficiently dissipate the generated heat, leading to performance throttling and increased operational costs. Liquid cooling offers a far more effective and efficient mechanism for heat removal, enabling higher computing densities within existing footprints and optimizing new facility designs. This allows data center operators to deploy more powerful hardware, enhancing overall compute capacity and performance.

Beyond thermal management, the imperative for energy efficiency and sustainability is significantly propelling the adoption of liquid cooling. Data centers are major consumers of electricity, and liquid cooling solutions can dramatically reduce the energy overhead associated with cooling by minimizing the need for large chiller plants and extensive air handling units. This leads to lower Power Usage Effectiveness (PUE) ratios, translating into substantial operational cost savings and a reduced carbon footprint. Furthermore, the ability of liquid cooling to capture waste heat for reuse in district heating or other industrial processes aligns with global sustainability initiatives, providing an additional economic and environmental incentive for adoption.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Rack Power Density | +7.5% | Global, particularly North America, APAC, Europe | 2025-2033 |

| Growing Demand for Energy Efficiency and Sustainability | +6.2% | Global, with strong impetus in Europe, North America | 2025-2033 |

| Proliferation of AI/ML and HPC Workloads | +8.1% | Global, especially US, China, UK, Germany, Japan | 2025-2033 |

| Reduction in Data Center PUE (Power Usage Effectiveness) | +4.8% | Global | 2025-2033 |

| Space Optimization and Data Center Modernization | +3.5% | Urban areas, developed economies | 2025-2033 |

Data Center Liquid Cooling Market Restraints Analysis

Despite the compelling benefits, the data center liquid cooling market faces significant restraints, primarily stemming from the high initial investment costs associated with its deployment. Implementing liquid cooling infrastructure involves substantial capital expenditure for specialized equipment such as cooling distribution units (CDUs), manifolds, pumps, piping, and potentially new server racks designed for liquid integration. This upfront financial outlay can be a deterrent for many organizations, especially small to medium-sized enterprises (SMEs) or those with tighter budget constraints, hindering broader adoption across various data center tiers. The cost also extends to the specialized installation and commissioning required, adding to the total cost of ownership in the initial phases.

Another notable restraint is the perceived complexity of deployment and maintenance compared to traditional air-cooling systems. Liquid cooling systems introduce new variables, such as fluid management, leak detection, and plumbing intricacies, which demand specialized expertise for design, installation, and ongoing operation. Data center staff may lack the necessary training and experience to manage these systems, leading to apprehension and resistance to adoption. Concerns about potential leaks, although largely mitigated by modern technologies, also contribute to a cautious approach, as even minor incidents could result in significant downtime and equipment damage, despite the low probability with robust systems.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Initial Capital Expenditure | -4.0% | Global, particularly emerging economies | Short to Medium Term (2025-2029) |

| Complexity of Deployment and Maintenance | -3.5% | Global | Short to Medium Term (2025-2029) |

| Lack of Standardization Across Technologies | -2.8% | Global | Medium Term (2027-2031) |

| Perceived Risk of Fluid Leaks | -2.0% | Global | Short Term (2025-2027) |

Data Center Liquid Cooling Market Opportunities Analysis

The burgeoning adoption of liquid cooling in edge computing environments presents a significant growth opportunity for the market. Edge data centers, characterized by their smaller footprint and proximity to data sources, often face severe space constraints and require highly efficient cooling solutions. Liquid cooling, particularly immersion and direct-to-chip systems, can effectively manage the high-density compute loads at the edge while reducing the overall physical space required for cooling infrastructure. This makes liquid cooling an ideal choice for power-constrained and space-limited edge deployments, enabling the expansion of localized processing capabilities vital for applications like IoT, 5G, and autonomous systems. As edge computing continues its rapid expansion, the demand for compact and efficient liquid cooling solutions is expected to surge.

Another substantial opportunity lies in the retrofitting of existing data center infrastructure. While new hyperscale facilities are increasingly designed with liquid cooling in mind, a vast number of operational data centers still rely on traditional air cooling and are not optimized for modern high-density hardware. The ability to integrate liquid cooling solutions into these legacy environments, such as through rear-door heat exchangers, cold plates, or modular immersion tanks, allows operators to upgrade their thermal management capabilities without undertaking a complete facility overhaul. This opportunity is particularly attractive for enterprises looking to extend the lifespan of their current data centers, improve energy efficiency, and accommodate more powerful IT equipment for AI/HPC workloads without significant structural modifications or new builds.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Adoption in Edge Computing and 5G Infrastructure | +5.5% | Global, strong in North America, Europe, APAC | 2026-2033 |

| Retrofitting of Existing Data Centers | +4.0% | Global, especially developed economies with aging infrastructure | 2025-2033 |

| Development of Advanced Cooling Fluids and Technologies | +3.8% | Global | 2027-2033 |

| Emergence of Modular and Scalable Liquid Cooling Solutions | +3.0% | Global | 2025-2033 |

Data Center Liquid Cooling Market Challenges Impact Analysis

The scalability of liquid cooling solutions presents a significant challenge for widespread adoption, particularly for large-scale data center operators. While individual racks or clusters can be efficiently liquid-cooled, expanding these deployments across entire facilities or multiple sites requires careful planning, significant infrastructure investment, and robust management systems. Ensuring uniform cooling performance, managing complex fluid distribution networks, and integrating with existing facility management systems on a vast scale can be technically demanding and costly. This complexity can deter large enterprises and hyperscale providers from fully transitioning away from more established air-cooling methods, limiting the total addressable market in the near term.

Another key challenge involves the specialized infrastructure requirements and the need for skilled personnel. Implementing liquid cooling often necessitates modifications to existing data center layouts, including specialized plumbing, leak detection systems, and dedicated power infrastructure for cooling distribution units (CDUs). Furthermore, the operation and maintenance of these systems demand a workforce with expertise in fluid dynamics, thermal engineering, and specialized IT equipment. A shortage of such skilled professionals can impede deployment and efficient operation, increasing both risk and operational costs. Addressing this talent gap through training and education programs will be crucial for the sustained growth and maturity of the liquid cooling market.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Scalability of Liquid Cooling Solutions | -3.0% | Global, particularly for large enterprises and hyperscalers | Medium Term (2026-2030) |

| Specialized Infrastructure Requirements | -2.5% | Global | Short to Medium Term (2025-2029) |

| Limited Skilled Personnel for Deployment and Maintenance | -2.2% | Global | Short to Medium Term (2025-2029) |

| Compatibility with Existing IT Hardware | -1.8% | Global | Short Term (2025-2027) |

Data Center Liquid Cooling Market - Updated Report Scope

This comprehensive market research report offers an in-depth analysis of the global Data Center Liquid Cooling Market, encompassing market size estimations, growth projections, key trends, drivers, restraints, opportunities, and challenges influencing market dynamics. The report provides a granular segmentation analysis across various components, cooling types, end-user industries, and regional landscapes, offering a holistic view of the market's current state and future potential. It incorporates detailed insights into the impact of emerging technologies like Artificial Intelligence on cooling demands and explores strategic profiles of leading market players, facilitating informed decision-making for stakeholders across the ecosystem.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 2.15 Billion |

| Market Forecast in 2033 | USD 12.87 Billion |

| Growth Rate | 24.8% |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Vertiv, Schneider Electric, Eaton, Asetek, Submer, Green Revolution Cooling, 3M, Fujitsu, IBM, Dell Technologies, Lenovo, CoolIT Systems, Liebert (Vertiv), Rittal, Stulz, LiquidStack, Arctic Cooling, Midas Green Technologies, ZutaCore, ExaScaler, Aquila, ColdLogik, Qio Tech, Motive Infrastructure Solutions, Allied Control |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Data Center Liquid Cooling market is comprehensively segmented to provide a detailed understanding of its diverse components, types, and applications across various end-user industries. This granular segmentation aids in identifying specific growth pockets and technological preferences within the market. The analysis covers the various hardware and software components that constitute a liquid cooling system, ranging from cooling distribution units to specialized fluids and control software. It also differentiates between various liquid cooling methodologies, each suited for different data center architectures and thermal demands, providing clarity on the technological landscape.

Further segmentation by end-user industries highlights the varying adoption rates and specific requirements across sectors such as hyperscale, enterprise, colocation, and specialized high-performance computing (HPC) environments. The growing importance of edge data centers is also reflected in the segmentation, demonstrating their unique needs for compact and efficient cooling. By understanding these distinct segments, market participants can tailor their offerings to address specific pain points and capitalize on emerging opportunities, fostering targeted innovation and market penetration.

- By Component: Cooling Distribution Units (CDUs), Chillers, Pumps, Piping & Leak Detection Systems, Heat Exchangers (Rear Door, In-Rack), Cooling Plates, Racks & Containment, Cooling Fluids (Dielectric Fluids, Water), Control Systems & Software, Other Components.

- By Type: Direct-to-Chip Liquid Cooling, Immersion Cooling (Single-phase, Two-phase), Hybrid Liquid Cooling, Liquid-to-Air Cooling, Liquid-to-Liquid Cooling.

- By End-User: Hyperscale Data Centers, Enterprise Data Centers, Colocation Data Centers, Edge Data Centers, High-Performance Computing (HPC), Cloud Providers, BFSI, IT & Telecom, Government & Defense, Healthcare, Manufacturing, Research & Academia, Other End-Users.

- By Application: Servers, Storage, Networking, Power Infrastructure.

- By Service: Installation & Deployment, Maintenance & Support, Consultation & Design.

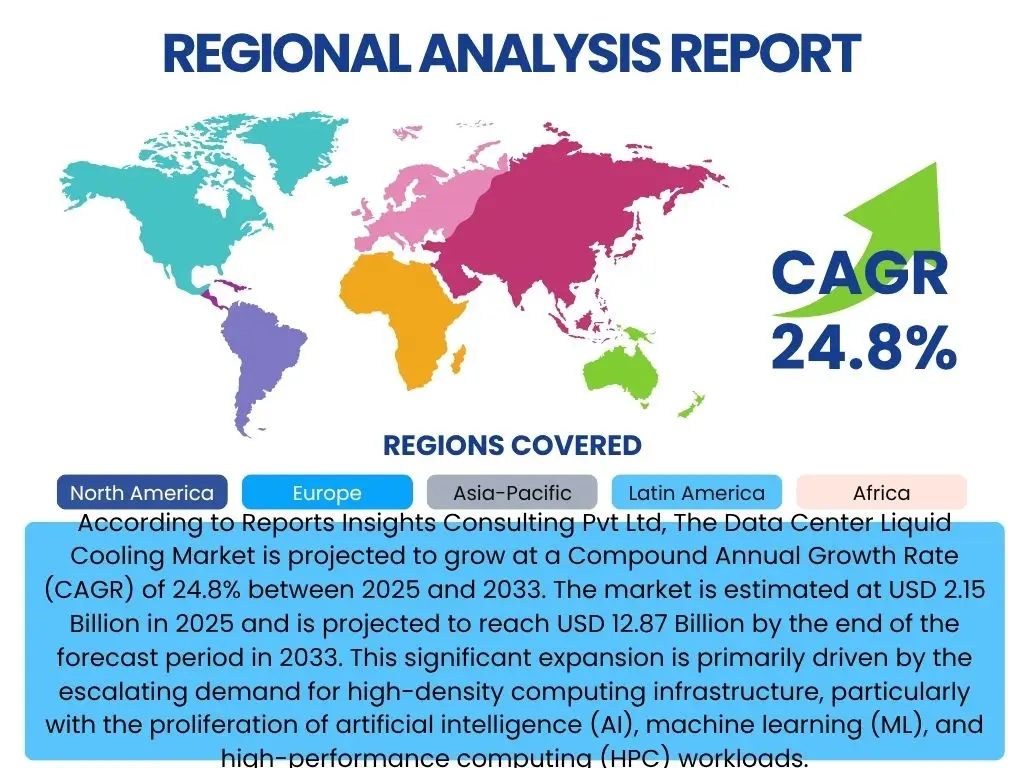

Regional Highlights

- North America: This region dominates the data center liquid cooling market, primarily driven by the presence of a large number of hyperscale data centers, major cloud service providers, and leading technology companies. The rapid adoption of AI and HPC workloads, coupled with stringent energy efficiency regulations and a strong focus on sustainability, fuels significant investments in advanced cooling solutions in countries like the United States and Canada. The region also benefits from a mature technological infrastructure and a high concentration of market innovators.

- Europe: Europe represents a significant market, propelled by strong regulatory pressure for energy efficiency, ambitious carbon reduction targets, and a growing emphasis on green data centers. Countries such as Germany, the UK, France, and the Nordics are leading the adoption of liquid cooling solutions, driven by a combination of high energy costs and a desire to implement sustainable IT infrastructure. The region also sees increased investment in colocation and edge data centers, further boosting the demand for efficient cooling.

- Asia Pacific (APAC): The APAC region is projected to be the fastest-growing market for data center liquid cooling. This growth is attributed to the rapid digital transformation, increasing internet penetration, and the booming construction of new data centers, especially in emerging economies like China, India, Japan, and Australia. The expansion of cloud computing, 5G deployments, and AI research in the region is creating immense demand for high-density, energy-efficient cooling solutions, making APAC a key investment hub.

- Latin America: While a nascent market, Latin America is experiencing gradual growth in data center liquid cooling, largely due to increasing digitalization, cloud adoption, and the establishment of new data centers to serve local demands. Countries like Brazil and Mexico are seeing investments, driven by the need for localized content delivery and data processing, which in turn necessitates more robust and efficient cooling infrastructures.

- Middle East and Africa (MEA): The MEA region is witnessing emerging opportunities, particularly in the UAE, Saudi Arabia, and South Africa, fueled by government-led digital transformation initiatives, smart city projects, and the rise of cloud regions. As these economies diversify and invest heavily in IT infrastructure, the demand for advanced and efficient cooling solutions for their growing data center footprint is expected to increase steadily.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Data Center Liquid Cooling Market.- Vertiv

- Schneider Electric

- Eaton

- Asetek

- Submer

- Green Revolution Cooling

- 3M

- Fujitsu

- IBM

- Dell Technologies

- Lenovo

- CoolIT Systems

- Rittal

- Stulz

- LiquidStack

- Arctic Cooling

- Midas Green Technologies

- ZutaCore

- ExaScaler

- Aquila

Frequently Asked Questions

Analyze common user questions about the Data Center Liquid Cooling market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is data center liquid cooling?

Data center liquid cooling is a thermal management technique that uses a liquid medium, such as water or dielectric fluid, to dissipate heat directly from IT components like CPUs, GPUs, and memory. It is a highly efficient alternative to traditional air cooling, particularly for high-density computing environments and high-performance workloads.

Why is liquid cooling becoming essential for data centers?

Liquid cooling is becoming essential due to the escalating heat generated by modern high-density processors (especially for AI/ML and HPC), the growing demand for energy efficiency, and the need to optimize data center space. It offers superior heat removal capabilities, leading to lower operating costs and a reduced environmental footprint.

What are the main types of liquid cooling?

The main types include Direct-to-Chip liquid cooling (where cold plates are attached directly to components), Immersion Cooling (submerging IT equipment in a dielectric fluid, either single-phase or two-phase), and Hybrid Liquid Cooling (combining liquid with air cooling).

What are the benefits of implementing liquid cooling?

Benefits include significantly improved heat dissipation for high-density racks, enhanced energy efficiency (lower PUE), reduced operational costs, optimized data center footprint, quieter operation, increased component reliability, and improved sustainability through lower carbon emissions and potential heat reuse.

What is the future outlook for the data center liquid cooling market?

The market is projected for robust growth, driven by the continuous demand for AI/ML, HPC, and cloud computing. It is transitioning from a niche solution to a mainstream necessity, with ongoing innovations in cooling fluids, modular systems, and increasing standardization, indicating a strong long-term growth trajectory and widespread adoption.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted