IBC Container Market

IBC Container Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_708581 | Last Updated : September 15, 2025 |

Format : ![]()

![]()

![]()

![]()

IBC Container Market Size

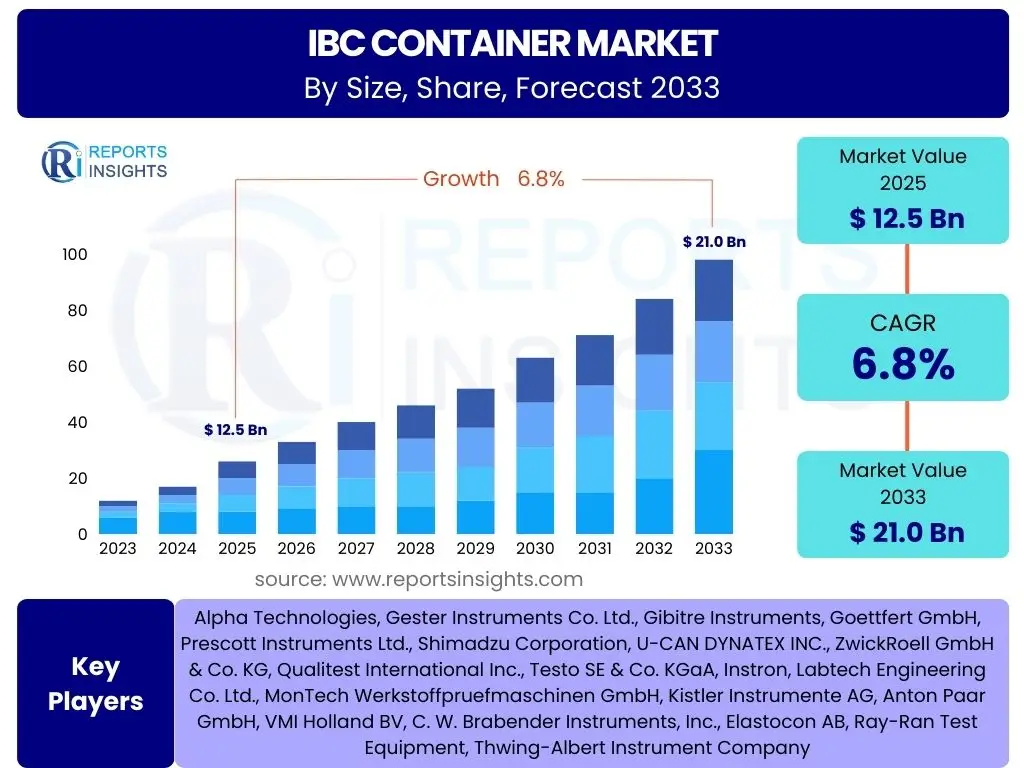

According to Reports Insights Consulting Pvt Ltd, The IBC Container Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2025 and 2033. The market is estimated at USD 12.5 Billion in 2025 and is projected to reach USD 21.0 Billion by the end of the forecast period in 2033.

Key IBC Container Market Trends & Insights

The IBC Container market is currently experiencing significant shifts driven by evolving industry demands and a heightened focus on sustainability. Users frequently inquire about the major innovations transforming this sector, such as advancements in material science for enhanced durability and chemical resistance, alongside the increasing adoption of smart technologies like IoT integration for real-time tracking and monitoring. These trends aim to optimize supply chain efficiency and improve product integrity, reflecting a broader industry push towards more intelligent and resilient logistics solutions.

Another prominent area of interest revolves around the environmental implications of IBCs, with a growing emphasis on reusable and recyclable options. The market is witnessing a strong demand for eco-friendly designs and materials that reduce waste and support circular economy principles. Furthermore, customization capabilities to meet diverse industry-specific requirements, from hazardous chemicals to delicate food ingredients, are becoming crucial, driving innovation in design and manufacturing processes to ensure optimal product protection and compliance with stringent regulations.

- Growing demand for sustainable and reusable packaging solutions.

- Integration of IoT and smart technologies for real-time tracking and monitoring.

- Increasing preference for customized IBC designs to meet specific industry needs.

- Advancements in material science leading to enhanced durability and chemical resistance.

- Shift towards aseptic IBCs for sensitive applications in food and pharmaceutical sectors.

AI Impact Analysis on IBC Container

Artificial intelligence is poised to revolutionize the IBC Container market by introducing unprecedented levels of efficiency, predictive capabilities, and operational optimization. Common user questions about AI's impact often center on how it can streamline logistics, enhance preventative maintenance, and improve overall supply chain visibility. AI algorithms can analyze vast datasets from sensors on smart IBCs to predict maintenance needs, optimize routing, and monitor environmental conditions, thereby minimizing product spoilage and operational downtime. This predictive intelligence significantly reduces costs associated with unexpected failures and inefficient resource allocation.

Furthermore, AI-driven solutions are expected to facilitate more precise demand forecasting, enabling manufacturers and users to manage inventory more effectively and reduce waste. The automation potential offered by AI, particularly in warehousing and material handling, will further enhance operational speed and accuracy. While initial implementation might present challenges related to data integration and infrastructure investment, the long-term benefits in terms of improved decision-making, reduced operational risks, and enhanced profitability are compelling, positioning AI as a critical enabler for the future of IBC container management.

- Predictive maintenance for IBC fleets, reducing downtime and operational costs.

- Optimized logistics and routing through AI-driven analytical insights.

- Enhanced inventory management and demand forecasting for better resource allocation.

- Automated quality control and integrity checks using computer vision and AI.

- Improved supply chain visibility and risk management through advanced data analysis.

Key Takeaways IBC Container Market Size & Forecast

An analysis of common user inquiries regarding the IBC Container market size and forecast reveals a strong interest in identifying the primary growth engines, understanding regional disparities in demand, and pinpointing key opportunities for investment. The overarching takeaway is the robust expansion predicted for the market, driven by the sustained growth of end-use industries such as chemicals, food and beverages, and pharmaceuticals. This growth is significantly bolstered by increasing international trade and a global emphasis on efficient, safe, and compliant bulk liquid and semi-solid transportation and storage solutions.

Furthermore, the market's trajectory is heavily influenced by technological advancements that enhance the functionality and sustainability of IBCs, alongside evolving regulatory landscapes that mandate specific packaging standards for various materials. The forecast underscores the importance of innovation in material science and smart container technologies, which are expected to unlock new application areas and improve operational efficiencies. Companies that can adapt to these shifts by offering versatile, durable, and eco-friendly IBC solutions are well-positioned to capitalize on the market's upward trend, particularly in high-growth emerging economies.

- Significant market expansion anticipated, driven by end-user industry growth.

- Increased adoption of IBCs due to their cost-effectiveness and efficiency in bulk transport.

- Technological innovations, including smart features and sustainable materials, are key growth catalysts.

- Emerging economies present substantial growth opportunities due to industrialization and infrastructure development.

- Stringent regulatory frameworks for product safety and environmental protection are shaping market demand.

IBC Container Market Drivers Analysis

The IBC container market is primarily propelled by the escalating demand from various end-use industries that require efficient and safe solutions for transporting and storing bulk liquids and semi-solids. Sectors such as chemicals, petrochemicals, food and beverage, pharmaceuticals, and industrial coatings are experiencing robust growth, directly translating into increased consumption of IBCs. The inherent advantages of IBCs, including their cost-effectiveness, reusability, and ability to optimize storage space compared to traditional drums, make them a preferred choice for these industries seeking operational efficiencies.

Moreover, the global expansion of international trade and complex supply chains necessitates reliable and standardized packaging solutions like IBCs to ensure product integrity across long distances and diverse environmental conditions. A growing focus on sustainable packaging practices also serves as a significant driver, with companies increasingly opting for reusable and recyclable IBC options to align with environmental goals and regulatory pressures. Innovations in IBC design, such as enhanced material durability and compatibility with a wider range of substances, further stimulate market growth by expanding their application scope and appeal.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growth in End-Use Industries (Chemicals, F&B, Pharma) | +2.1% | Global, particularly Asia Pacific, North America | Short to Mid-Term |

| Increasing Focus on Sustainable Packaging Solutions | +1.5% | Europe, North America, Developed Asian Markets | Mid to Long-Term |

| Rising Global Trade and Logistics Activities | +1.2% | Global, particularly Asia Pacific, Latin America | Short to Mid-Term |

| Advantages over Drums (Cost-Efficiency, Space Optimization) | +1.0% | Global | Short to Mid-Term |

| Stringent Regulations for Hazardous Material Transport | +0.8% | Europe, North America | Short to Mid-Term |

IBC Container Market Restraints Analysis

Despite the positive market outlook, several factors act as restraints on the growth of the IBC container market. A primary concern is the volatility of raw material prices, particularly for plastics (HDPE) and steel, which are essential components in IBC manufacturing. Fluctuations in these commodity prices directly impact production costs, potentially leading to increased pricing for end-users and dampening overall market demand. This unpredictability in material costs can create budgeting challenges for manufacturers and hinder long-term investment planning, especially for smaller market participants.

Another significant restraint involves the high initial capital investment required for establishing robust IBC cleaning, maintenance, and recycling infrastructure, particularly for reusable IBCs. While reusable IBCs offer long-term cost savings and environmental benefits, the upfront costs and logistical complexities associated with their return and refurbishment can be substantial. Furthermore, stringent environmental regulations regarding the disposal of certain materials and the cleaning of IBCs that have contained hazardous substances pose operational challenges, requiring specialized facilities and processes which add to the overall operational expenditure and complexity for market players.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Volatile Raw Material Prices (HDPE, Steel) | -1.5% | Global | Short to Mid-Term |

| High Initial Capital Investment for Reusable IBC Infrastructure | -0.9% | Developed Regions (North America, Europe) | Mid-Term |

| Logistical Challenges in Return and Cleaning of Reusable IBCs | -0.7% | Global | Short to Mid-Term |

| Stringent Environmental Regulations on Waste Management | -0.5% | Europe, North America, specific Asian countries | Long-Term |

IBC Container Market Opportunities Analysis

The IBC container market is characterized by several promising opportunities that are set to fuel future growth and innovation. A key opportunity lies in the expansion into emerging economies, particularly in Asia Pacific, Latin America, and the Middle East and Africa. Rapid industrialization, growing manufacturing sectors, and increasing consumer spending in these regions are driving significant demand for efficient bulk packaging solutions, offering untapped markets for IBC manufacturers and service providers. These regions are often characterized by developing infrastructure and evolving regulatory landscapes, presenting unique avenues for market penetration.

Technological advancements also present substantial opportunities, with the ongoing integration of smart technologies such as IoT sensors, RFID tags, and GPS tracking into IBCs. These innovations enable real-time monitoring of container location, fill levels, temperature, and pressure, significantly enhancing supply chain transparency and operational efficiency. Furthermore, the increasing demand for specialized IBCs for aseptic applications in the food and pharmaceutical industries, as well as high-barrier solutions for sensitive chemicals, creates niche market segments with high-growth potential, driving innovation in material science and design to meet these exacting requirements.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Expansion into Emerging Economies | +1.8% | Asia Pacific, Latin America, MEA | Mid to Long-Term |

| Technological Advancements (Smart IBCs, IoT Integration) | +1.5% | Global | Mid to Long-Term |

| Growing Demand for Specialized and Aseptic IBCs | +1.3% | North America, Europe, Developed Asian Markets | Short to Mid-Term |

| Development of Advanced Recyclable and Biodegradable Materials | +1.0% | Europe, North America | Long-Term |

IBC Container Market Challenges Impact Analysis

The IBC container market faces several formidable challenges that could impede its growth trajectory. One significant hurdle is the intense competition among both established global players and numerous regional manufacturers. This highly fragmented market often leads to pricing pressures and reduced profit margins, particularly for less differentiated products. Companies must continually innovate and find new ways to offer value to maintain competitiveness, which can be resource-intensive and challenging in a price-sensitive environment.

Another critical challenge involves the complex regulatory landscape surrounding the transportation and storage of various substances. Different regions and countries have varying standards and certifications for IBCs, particularly for hazardous materials, food-grade products, and pharmaceuticals. Adhering to these diverse and evolving regulations requires significant investment in compliance, testing, and documentation, posing a barrier to market entry and expansion. Furthermore, the operational challenges associated with ensuring the cleanliness, integrity, and safety of reusable IBCs across their lifecycle, including potential contamination risks and damage during transit, remain a constant concern for users and a focus area for manufacturers.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Intense Competition and Price Pressures | -1.3% | Global | Short to Mid-Term |

| Complex and Evolving Regulatory Landscape | -1.0% | Europe, North America, specific Asian countries | Long-Term |

| Maintaining Cleanliness and Integrity of Reusable IBCs | -0.8% | Global | Short to Mid-Term |

| Logistical Infrastructure Deficiencies in Emerging Markets | -0.6% | Latin America, MEA, parts of Asia Pacific | Mid-Term |

IBC Container Market - Updated Report Scope

This comprehensive market report provides an in-depth analysis of the IBC Container Market, encompassing current market dynamics, growth drivers, restraints, opportunities, and challenges. It offers a detailed segmentation analysis, regional insights, and profiles of key industry players, serving as a vital resource for strategic decision-making and market forecasting through 2033.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 12.5 Billion |

| Market Forecast in 2033 | USD 21.0 Billion |

| Growth Rate | 6.8% |

| Number of Pages | 255 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Mauser Packaging Solutions, Greif Inc., Schutz Container Systems, Snyder Industries, Thielmann, BWAY Corporation, Composite Containers Inc., Hoover Ferguson, TranPak, Inc., WERIT Kunststoffwerke, Precision IBC, Automation Plastics Corporation, Custom Metalcraft, Inc., Time Container, Peninsula IBC, Rotomoulding & Recycling, Fustiplast S.A., CDF Corporation, Drum & IBC Services Ltd, Astin Containers |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The IBC Container market is comprehensively segmented to provide a granular understanding of its diverse components and their respective growth trajectories. This segmentation allows for a detailed examination of market dynamics based on factors such as material type, container capacity, specific end-use industry applications, and design configurations. Each segment and subsegment exhibit unique demand characteristics and growth drivers, influenced by technological advancements, regulatory mandates, and evolving industrial preferences. Understanding these distinct segments is crucial for identifying targeted opportunities and formulating effective market strategies.

For instance, the material segmentation highlights the dominance of plastic and composite IBCs due to their versatility and durability, while metal IBCs retain importance for specialized and hazardous applications. Capacity segmentation reflects varying industrial needs, from smaller volumes for specialty chemicals to larger volumes for bulk commodities. The end-use industry breakdown reveals the significant reliance of sectors like chemicals and food & beverages on IBCs, whereas design variations cater to specific logistical and operational requirements, such as the space-saving benefits of folding IBCs or the flexibility of liner-equipped options. This detailed analysis ensures a holistic view of the market's structure and potential areas for innovation.

- By Material:

- Plastic (HDPE)

- Metal (Stainless Steel, Carbon Steel)

- Fiber

- Composite (Plastic bottle in steel cage)

- By Capacity:

- Up to 500 Liters

- 501 to 1000 Liters

- 1001 to 1500 Liters

- Above 1500 Liters

- By End-Use Industry:

- Industrial Chemicals

- Food & Beverages

- Pharmaceuticals

- Oil & Lubricants

- Paints & Coatings

- Other Industrial Applications

- By Design:

- Standard (Rigid)

- Folding

- Flexible (FIBCs – though generally distinct, can sometimes overlap in bulk handling context)

Regional Highlights

- North America: This region is a mature yet consistently growing market for IBC containers, driven by robust industrial output in the chemical, food and beverage, and pharmaceutical sectors. The presence of stringent environmental regulations and a strong emphasis on workplace safety also encourages the adoption of high-quality, compliant IBC solutions. Manufacturers in North America are increasingly investing in smart IBC technologies and reusable systems to enhance supply chain efficiency and reduce their environmental footprint. The demand for specialized IBCs, such as those for aseptic applications, continues to rise, reflecting sophisticated industrial needs.

- Europe: Europe stands as a pivotal region for the IBC container market, characterized by advanced manufacturing capabilities and a pioneering stance on sustainability. Strict environmental protection laws and regulations, particularly concerning waste reduction and recycling, strongly influence market dynamics, driving demand for reusable, returnable, and highly recyclable IBC solutions. Countries such as Germany, France, and the UK lead in adopting innovative packaging materials and smart technologies to optimize logistics and ensure product safety for a wide array of industries, including specialty chemicals, food processing, and pharmaceuticals.

The European market also benefits from a strong emphasis on food safety and hygiene, which fuels the demand for aseptic and high-grade IBCs, particularly in the beverage and dairy industries. Economic stability, coupled with a well-developed logistics network, facilitates the efficient distribution and recovery of IBCs, reinforcing the viability of reusable models. The region's commitment to reducing carbon emissions and promoting circular economy principles ensures sustained investment in environmentally friendly IBC container solutions and services.

- Asia Pacific (APAC): The Asia Pacific region is projected to be the fastest-growing market for IBC containers, primarily due to rapid industrialization, burgeoning manufacturing sectors, and increasing foreign direct investment across its developing economies. Countries like China, India, Japan, and South Korea are experiencing significant expansion in chemical production, food processing, and pharmaceutical manufacturing, leading to a substantial surge in demand for bulk packaging solutions. The region's vast population and growing consumer base also contribute to increased production volumes across various industries, necessitating efficient and cost-effective packaging.

- Latin America: The Latin American IBC container market is experiencing steady growth, driven by expanding industrial sectors and increasing trade activities within the region and globally. Countries such as Brazil, Mexico, and Argentina are key contributors, with growth primarily stemming from the agricultural, chemical, and food and beverage industries. The region's rich natural resources and agricultural output necessitate robust and reliable packaging solutions for transportation and storage, making IBCs an increasingly popular choice for bulk handling.

Infrastructure development and foreign investment are gradually improving logistics capabilities across Latin America, facilitating wider adoption of IBCs. While price sensitivity can be a factor, there is a growing recognition of the long-term cost benefits and environmental advantages of reusable IBCs. The market is also seeing an increase in demand for IBCs that can withstand diverse climatic conditions and meet evolving local regulatory standards, presenting opportunities for manufacturers to offer tailored solutions and expand their regional presence.

- Middle East and Africa (MEA): The IBC container market in the Middle East and Africa is witnessing growth fueled by significant investments in the petrochemical, oil and gas, and chemical industries, particularly in the GCC countries. The expansion of manufacturing capabilities and diversification efforts away from traditional oil economies are creating new demand for industrial packaging. Furthermore, increasing urbanization and a growing population contribute to the development of the food and beverage and pharmaceutical sectors, further propelling the need for efficient bulk liquid storage and transport.

While market penetration in some parts of Africa is still developing, the continent offers substantial long-term growth potential as industrialization and trade infrastructure improve. The adoption of IBCs is also influenced by increasing awareness of product integrity and supply chain efficiency, especially for sensitive or high-value goods. Challenges related to logistics infrastructure and regulatory harmonization exist, but ongoing government initiatives to promote industrial growth and attract investment are expected to accelerate the adoption of IBC container solutions in the coming years.

The United States and Canada represent the largest portions of the North American market, benefiting from well-established industrial infrastructure and a high adoption rate of advanced packaging solutions. Market growth is further supported by innovations in material science and an increasing focus on the circular economy, prompting greater utilization of recycled content in plastic IBCs and more efficient cleaning and refurbishment services for metal and composite units. This region remains a key area for technological innovation and premium product offerings within the IBC container market.

While cost-effectiveness remains a crucial factor, there is a rising awareness and adoption of sustainable and high-quality IBCs, especially in developed APAC nations and among multinational corporations operating in the region. Investments in infrastructure development, including logistics and warehousing, further support the growth of the IBC market. The diversity of industrial landscapes, from heavy industries to advanced electronics manufacturing, creates a broad spectrum of demand for various types of IBCs, from standard rigid plastic to specialized composite containers, making APAC a dynamic and high-potential market.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the IBC Container Market.- Mauser Packaging Solutions

- Greif Inc.

- Schutz Container Systems

- Snyder Industries

- Thielmann

- BWAY Corporation

- Composite Containers Inc.

- Hoover Ferguson

- TranPak, Inc.

- WERIT Kunststoffwerke

- Precision IBC

- Automation Plastics Corporation

- Custom Metalcraft, Inc.

- Time Container

- Peninsula IBC

- Rotomoulding & Recycling

- Fustiplast S.A.

- CDF Corporation

- Drum & IBC Services Ltd

- Astin Containers

Frequently Asked Questions

What are IBC containers?

Intermediate Bulk Containers (IBCs) are reusable industrial containers designed for the transport and storage of bulk liquids, semi-solids, pastes, or solids. They typically have a volume capacity ranging from 500 to 3,000 liters and are often constructed from plastic, metal, or composite materials, encased in a rigid outer frame.

Which industries primarily use IBC containers?

IBC containers are extensively utilized across a wide range of industries including industrial chemicals, food and beverages, pharmaceuticals, oil and lubricants, paints and coatings, and agriculture. Their versatility and capacity make them ideal for various bulk material handling needs.

What are the main advantages of using IBCs over traditional drums?

IBCs offer significant advantages over traditional drums, including greater capacity per unit, more efficient use of storage space (often stackable), reduced handling costs, enhanced safety features, and reusability, which contributes to lower environmental impact and long-term cost savings.

Are IBC containers reusable and recyclable?

Yes, many IBC containers, particularly those made from high-density polyethylene (HDPE) or metal, are designed for multiple uses and are highly recyclable. This reusability and recyclability contribute to their environmental sustainability and appeal within a circular economy framework.

What regulations apply to IBC container usage?

The usage of IBC containers is subject to various international and national regulations, particularly for the transport of hazardous materials. These include UN Recommendations on the Transport of Dangerous Goods, as well as regional regulations like DOT (North America) and ADR/RID (Europe), which cover design, testing, marking, and operational requirements.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted