Satellite Bus Market

Satellite Bus Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_710395 | Last Updated : January 05, 2026 |

Format : ![]()

![]()

![]()

![]()

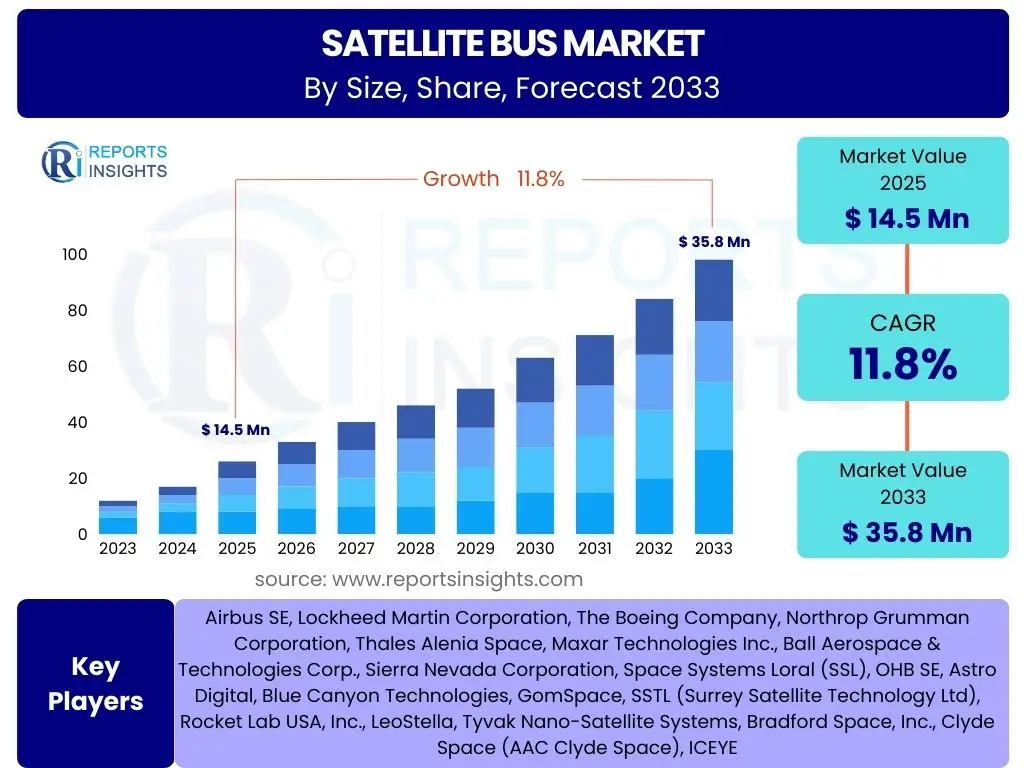

Satellite Bus Market Size

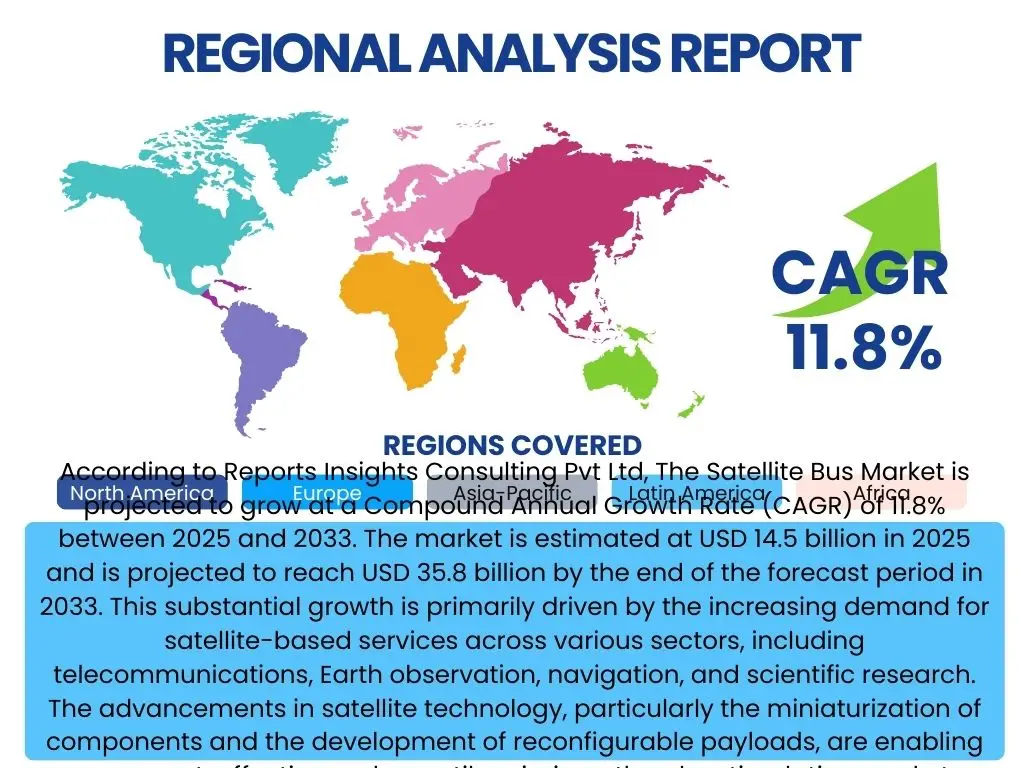

According to Reports Insights Consulting Pvt Ltd, The Satellite Bus Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 11.8% between 2025 and 2033. The market is estimated at USD 14.5 billion in 2025 and is projected to reach USD 35.8 billion by the end of the forecast period in 2033. This substantial growth is primarily driven by the increasing demand for satellite-based services across various sectors, including telecommunications, Earth observation, navigation, and scientific research. The advancements in satellite technology, particularly the miniaturization of components and the development of reconfigurable payloads, are enabling more cost-effective and versatile missions, thereby stimulating market expansion.

The upward trajectory of the satellite bus market also reflects a global shift towards commercial space endeavors and the proliferation of mega-constellations. Private investment in space infrastructure is surging, leading to increased manufacturing and deployment of satellites. Furthermore, government initiatives and defense spending on advanced satellite systems contribute significantly to market size, as these entities require robust and reliable platforms for national security, intelligence gathering, and public services. The forecast period anticipates continued innovation in propulsion systems, power generation, and structural materials, which will further enhance the capabilities and economic viability of satellite bus platforms.

Key Satellite Bus Market Trends & Insights

User inquiries frequently focus on the evolving landscape of satellite technology, particularly concerning efficiency, cost-effectiveness, and adaptability. Common questions revolve around the adoption of standardized platforms, the impact of small satellite proliferation, and the move towards more autonomous and intelligent satellite systems. These trends collectively underscore an industry-wide drive to lower the barriers to entry for space missions, accelerate deployment timelines, and enhance the overall utility and longevity of orbital assets.

- Standardization and Modularity: Increasing adoption of standardized satellite bus architectures and modular components to reduce manufacturing costs and lead times, facilitating quicker deployment for diverse missions.

- Small Satellite Proliferation: Rapid growth in the deployment of small satellites (CubeSats, microsatellites, nanosatellites) for various applications, including remote sensing, IoT, and broadband connectivity, leading to demand for compact and efficient bus designs.

- Electric Propulsion Systems: Growing integration of electric (ion/hall-effect) propulsion systems for enhanced fuel efficiency, extended mission lifespans, and greater maneuverability, particularly for geostationary and deep-space missions.

- In-Orbit Servicing and Manufacturing (IOSM): Emerging trend towards satellites designed for on-orbit refueling, repair, assembly, and manufacturing, requiring compatible bus interfaces and robust designs.

- Software-Defined Satellites: Development of flexible, software-defined satellite buses that can be reconfigured in orbit to adapt to changing mission requirements or accommodate new technologies.

- Mega-Constellations and Mass Production: Development of satellite buses optimized for mass production to support large-scale mega-constellations for global broadband internet and Earth observation, emphasizing economies of scale.

- Advanced Materials and Miniaturization: Use of lightweight, high-strength composite materials and further miniaturization of subsystems to improve payload capacity, reduce launch mass, and enhance overall satellite performance.

AI Impact Analysis on Satellite Bus

Common user questions regarding AI's impact on the satellite bus market center on its potential to enhance operational efficiency, enable autonomous capabilities, and improve mission reliability. Users are keen to understand how AI can optimize power management, facilitate predictive maintenance, and contribute to the overall intelligence of satellite platforms. There is significant interest in AI's role in autonomous decision-making for orbital maneuvers and anomaly detection, as well as its capacity to process vast amounts of onboard data to make satellites more self-sufficient and responsive.

The integration of artificial intelligence (AI) and machine learning (ML) is poised to significantly transform the design, operation, and capabilities of satellite buses. AI can enable advanced automation, allowing satellites to perform complex tasks with minimal human intervention, from autonomous navigation and collision avoidance to intelligent payload management. This shift towards more intelligent and self-governing systems can reduce operational costs, enhance responsiveness to dynamic environmental conditions, and extend mission durations by optimizing resource utilization.

- Autonomous Navigation and Control: AI algorithms enable satellites to autonomously execute orbital maneuvers, maintain constellations, and avoid collisions, reducing the need for ground-based intervention and enhancing operational efficiency.

- Predictive Maintenance: AI-powered analytics monitor satellite bus health in real-time, predicting potential component failures and enabling proactive measures to extend mission lifespan and prevent costly downtime.

- Intelligent Resource Management: AI optimizes power distribution, thermal control, and communication bandwidth allocation on the satellite bus, ensuring efficient use of onboard resources for maximum mission effectiveness.

- Onboard Data Processing: Edge AI capabilities allow satellites to process large volumes of sensor data onboard, reducing the need for extensive data downlink and enabling faster, localized decision-making for Earth observation or scientific missions.

- Anomaly Detection and Self-Correction: AI systems can rapidly identify anomalous behavior in satellite bus subsystems, diagnose issues, and initiate self-correction protocols, significantly improving mission reliability and resilience.

- Payload Optimization: AI can dynamically manage and optimize payload operations, reconfiguring instruments or adjusting parameters to meet evolving mission objectives or respond to specific environmental events.

- Swarm Intelligence for Constellations: For mega-constellations, AI facilitates coordinated behavior and communication among multiple satellites, optimizing resource sharing and collective mission performance.

Key Takeaways Satellite Bus Market Size & Forecast

Analysis of user questions regarding market size and forecast reveals a strong interest in the underlying factors driving growth, the economic implications of new space initiatives, and the expected trajectory of different market segments. Users commonly seek clarity on the long-term viability of satellite investments and the potential for disruption from emerging technologies. The overall sentiment suggests a market characterized by robust expansion, fueled by both technological innovation and a burgeoning commercial space sector.

The satellite bus market is experiencing a significant growth phase, underpinned by technological advancements and increasing global demand for satellite services. The forecast indicates sustained high growth, reflecting continued investment in space infrastructure by both governmental and private entities. This expansion is not uniform across all segments; specific areas like small satellite buses and those designed for mega-constellations are poised for particularly rapid development. Understanding these nuanced growth drivers is crucial for stakeholders positioning themselves within this dynamic market.

- Substantial Market Expansion: The market is projected for robust growth, indicating a high level of investment and development in satellite technologies and applications.

- Technological Innovation as Core Driver: Advances in propulsion, miniaturization, and material science are foundational to reducing costs and expanding capabilities, directly fueling market growth.

- Commercialization of Space: Increased private sector involvement and the proliferation of commercial mega-constellations are significant contributors to the escalating demand for satellite buses.

- Diversification of Applications: Growth is driven by diverse applications across telecommunications, Earth observation, navigation, and scientific research, broadening the market's reach.

- Emphasis on Cost Efficiency: Future market success will increasingly depend on the ability to deliver cost-effective and highly reliable satellite bus solutions, driving standardization and modularity.

- Strategic Importance: The satellite bus market remains strategically important for national security, economic development, and scientific exploration, ensuring continued government and defense spending.

Satellite Bus Market Drivers Analysis

The satellite bus market is propelled by a confluence of factors, prominently including the surging demand for satellite-based services across various industries. This demand is intrinsically linked to global digitalization trends, the expansion of internet connectivity into underserved regions, and the increasing reliance on satellite data for critical applications. Furthermore, the reduction in launch costs and the development of more efficient and powerful satellite platforms have made space access more economically viable, encouraging greater investment and innovation in satellite technologies. These drivers collectively create a fertile ground for sustained market expansion, as both established and emerging players vie for a share in this dynamic sector.

Technological advancements play a crucial role, with innovations in propulsion systems, power generation, and structural materials enhancing the performance and extending the lifespan of satellites. Miniaturization allows for smaller, more versatile satellites, opening up new mission possibilities and reducing overall project costs. Additionally, the strategic importance of space assets for national security, intelligence, and defense continues to drive significant government expenditure, providing a stable foundation for market growth. The ongoing shift towards commercial space activities, exemplified by private mega-constellations for global broadband, further amplifies the demand for sophisticated and mass-producible satellite bus solutions, reinforcing the market's upward trajectory.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Rising Demand for Satellite-based Services | +3.2% | Global, particularly APAC, North America | Short to Long-term |

| Proliferation of Small Satellite Missions & Constellations | +2.8% | North America, Europe, Asia Pacific | Medium to Long-term |

| Technological Advancements in Satellite Components | +2.5% | Global, especially US, Europe, China | Short to Medium-term |

| Decreasing Cost of Satellite Launches | +1.9% | Global | Medium-term |

| Increased Government and Defense Spending on Space Programs | +1.5% | US, Russia, China, India, EU Member States | Long-term |

| Growth in Earth Observation & Remote Sensing Applications | +1.3% | Global | Medium to Long-term |

| Expansion of Global Broadband & IoT Connectivity | +1.6% | Global, especially emerging economies | Short to Medium-term |

Satellite Bus Market Restraints Analysis

Despite robust growth, the satellite bus market faces several significant restraints that could impede its expansion. One primary concern is the high upfront capital expenditure required for satellite manufacturing and deployment. Developing and launching satellites involves substantial investment in research, development, specialized materials, and complex assembly processes, making it a high-risk, high-reward industry. This financial barrier can limit the entry of new players and slow down innovation, particularly for larger satellite systems. Moreover, the long lead times associated with satellite development, from design to launch, can result in technologies becoming partially outdated before deployment, posing a challenge in a rapidly evolving technological landscape.

Regulatory complexities and international space policies also present considerable hurdles. Export controls, orbital slot allocation, spectrum management, and debris mitigation guidelines vary significantly across jurisdictions, creating a convoluted operational environment for global satellite operators. Geopolitical tensions and national security concerns can further complicate international collaborations and technology transfers, impacting market reach and efficiency. The increasing risk of space debris, particularly with the proliferation of mega-constellations, necessitates stringent mitigation strategies, adding to design complexities and operational costs. While these restraints are substantial, continuous efforts in policy harmonization and technological innovation aim to address these challenges and mitigate their impact on market growth.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Upfront Capital Investment and Development Costs | -2.1% | Global | Short to Medium-term |

| Stringent Regulatory Frameworks and International Policies | -1.8% | Global, particularly EU, US, China | Medium to Long-term |

| Risk of Space Debris and Orbital Congestion | -1.5% | Global | Medium to Long-term |

| Long Development Cycles and Time-to-Market | -1.2% | Global | Short to Medium-term |

| Lack of Skilled Workforce and Expertise | -0.9% | North America, Europe | Medium-term |

| Vulnerability to Cyberattacks and Space Weather | -0.8% | Global | Short to Long-term |

| Dependency on Government Funding and Policies | -0.7% | Regions with nascent space programs | Short to Medium-term |

Satellite Bus Market Opportunities Analysis

The satellite bus market is rich with opportunities, primarily driven by the escalating demand for global connectivity and Earth observation data. The rollout of 5G networks and the expansion of the Internet of Things (IoT) create a significant need for satellite backhaul and direct-to-device communication, fostering the development of advanced communication satellite buses. Furthermore, the increasing awareness of climate change and environmental monitoring necessitates more sophisticated Earth observation satellites, pushing innovation in high-resolution imaging and data processing capabilities. These trends offer avenues for specialized satellite bus development tailored to specific industry needs, enabling market players to capture niche segments.

Emerging technologies such as in-orbit servicing, assembly, and manufacturing (ISAM) represent transformative opportunities. The capability to refuel, repair, upgrade, or even construct satellites in space promises to extend mission lifespans, reduce launch costs, and enable entirely new mission profiles, thereby increasing the value proposition of robust and adaptable satellite buses. Moreover, the growth of space tourism and lunar/Martian exploration initiatives, though nascent, signifies future demand for highly reliable and adaptable satellite buses capable of supporting deep-space missions and complex orbital logistics. Investment in these forward-looking areas could yield substantial long-term returns for companies that position themselves as pioneers.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Expansion of Global 5G and IoT Networks | +2.9% | Global, especially emerging markets | Short to Medium-term |

| Development of In-Orbit Servicing, Assembly, and Manufacturing (ISAM) | +2.7% | North America, Europe, Japan | Medium to Long-term |

| Growing Demand for High-Resolution Earth Observation Data | +2.4% | Global | Short to Medium-term |

| Space Tourism and Deep-Space Exploration Initiatives | +1.9% | North America, Europe | Long-term |

| Increased Investment in Private Commercial Space Ventures | +1.7% | Global | Short to Medium-term |

| Technological Advancements in Miniaturization & Standardization | +1.5% | Global | Short to Medium-term |

| Development of Quantum Communication & Advanced Navigation Systems | +1.3% | China, US, EU | Long-term |

Satellite Bus Market Challenges Impact Analysis

The satellite bus market faces numerous challenges, ranging from intense competition and pricing pressures to the critical need for robust cybersecurity measures. The increasing number of market entrants, including agile startups and well-funded commercial entities, intensifies competition, often leading to downward pressure on pricing and thinner profit margins for established players. This competitive landscape demands continuous innovation and cost-efficiency, forcing companies to invest heavily in R&D while simultaneously optimizing their production processes. Furthermore, geopolitical instability and evolving trade policies can disrupt supply chains, affecting the availability and cost of critical components, particularly those with highly specialized applications.

Another significant challenge is ensuring the long-term sustainability and resilience of satellite systems against environmental threats and malicious actors. The harsh space environment, coupled with the growing menace of space debris and potential cyberattacks, necessitates increasingly sophisticated and expensive protection mechanisms. Designing satellite buses that are resilient to radiation, extreme temperatures, and kinetic impacts, while also incorporating advanced cybersecurity protocols, adds complexity and cost to manufacturing. Attracting and retaining a highly specialized workforce with expertise in aerospace engineering, advanced materials, and software development also remains a persistent challenge, as the demand for such talent often outstrips supply, particularly in rapidly growing spacefaring nations.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Intense Competition and Pricing Pressure | -1.9% | Global | Short to Medium-term |

| Ensuring Cybersecurity and Data Integrity | -1.7% | Global | Medium to Long-term |

| Supply Chain Disruptions and Component Shortages | -1.5% | Global, particularly post-pandemic | Short to Medium-term |

| Managing Space Debris and Orbital Sustainability | -1.3% | Global | Medium to Long-term |

| Attracting and Retaining Skilled Workforce | -1.1% | North America, Europe, Asia Pacific | Long-term |

| Adapting to Rapid Technological Obsolescence | -0.9% | Global | Short to Medium-term |

| High Failure Rates in New Space Ventures | -0.8% | Global | Short to Medium-term |

Satellite Bus Market - Updated Report Scope

This report provides a comprehensive analysis of the global Satellite Bus Market, delving into market size, growth drivers, restraints, opportunities, and challenges across various segments and regions. It offers a detailed forecast from 2025 to 2033, incorporating historical data from 2019 to 2023 to provide a robust foundational understanding of market dynamics. The scope includes an in-depth examination of key technological trends, the impact of artificial intelligence, and a competitive landscape analysis featuring profiles of major market players. The report aims to furnish stakeholders with actionable insights to inform strategic decisions and navigate the evolving market environment.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 14.5 Billion |

| Market Forecast in 2033 | USD 35.8 Billion |

| Growth Rate | 11.8% |

| Number of Pages | 247 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Airbus SE, Lockheed Martin Corporation, The Boeing Company, Northrop Grumman Corporation, Thales Alenia Space, Maxar Technologies Inc., Ball Aerospace & Technologies Corp., Sierra Nevada Corporation, Space Systems Loral (SSL), OHB SE, Astro Digital, Blue Canyon Technologies, GomSpace, SSTL (Surrey Satellite Technology Ltd), Rocket Lab USA, Inc., LeoStella, Tyvak Nano-Satellite Systems, Bradford Space, Inc., Clyde Space (AAC Clyde Space), ICEYE |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The satellite bus market is extensively segmented to reflect the diverse range of applications, technological requirements, and operational scales within the space industry. This granular segmentation allows for a detailed understanding of specific market niches and their unique growth drivers and challenges. The primary segments include satellite mass, which differentiates between small, medium, and large platforms, each serving distinct mission profiles. Subsystem segmentation provides insight into the technological components that form the backbone of any satellite, highlighting areas of innovation such as propulsion, power, and attitude control systems.

Further segmentation by application categorizes satellite buses based on their intended use, such as Earth observation, communication, or scientific research, revealing demand patterns across different sectors. End-user segmentation distinguishes between commercial, government/military, and civil clients, reflecting varied procurement processes and requirements. Finally, orbit type segmentation (LEO, MEO, GEO) is crucial as it dictates the design specifications, propulsion needs, and mission durations of satellite buses. This comprehensive breakdown is vital for market participants to identify lucrative opportunities and tailor their offerings effectively.

- By Satellite Mass:

- Small Satellite (Less than 500 kg): Driven by the proliferation of mega-constellations and demand for cost-effective services.

- Medium Satellite (500 kg to 2,500 kg): Used for various applications requiring higher power and payload capacity than small satellites.

- Large Satellite (More than 2,500 kg): Predominantly for geostationary communication and large scientific missions, characterized by high performance and long lifespans.

- By Subsystem:

- Structure & Mechanism: The foundational framework, crucial for accommodating payloads and resisting launch forces.

- Electrical Power System (EPS): Responsible for power generation (solar arrays), storage (batteries), and distribution.

- Attitude Determination & Control System (ADCS): Ensures precise orientation and stability of the satellite.

- Propulsion System: Provides thrust for orbital maneuvers, station-keeping, and deorbiting.

- Thermal Control System (TCS): Manages internal temperatures to protect sensitive electronics.

- Telemetry, Tracking, and Command (TT&C): Facilitates communication and control between the satellite and ground stations.

- On-Board Data Handling (OBDH): Manages and processes data collected by the satellite.

- By Application:

- Earth Observation & Remote Sensing: For environmental monitoring, resource management, and intelligence.

- Communication & Navigation: Crucial for global connectivity, broadband, and GPS services.

- Scientific Research & Exploration: Supports astronomical observation, planetary missions, and fundamental physics experiments.

- Technology Demonstration & Verification: Used for testing new space technologies in orbit.

- Surveillance & Reconnaissance: For defense and intelligence gathering purposes.

- By End-User:

- Commercial: Includes telecommunication providers, satellite imagery companies, and IoT service providers.

- Government & Military: Encompasses national space agencies, defense ministries, and intelligence organizations.

- Civil: Primarily academic institutions and non-profit organizations for scientific and educational purposes.

- By Orbit Type:

- Low Earth Orbit (LEO): Preferred for small satellites, mega-constellations, and applications requiring low latency (e.g., Earth observation, broadband internet).

- Medium Earth Orbit (MEO): Used mainly for navigation (GPS, Galileo) and certain communication services.

- Geostationary Earth Orbit (GEO): Ideal for large communication and broadcast satellites due to its fixed position relative to the Earth's surface.

Regional Highlights

- North America: Dominates the satellite bus market due to the presence of major aerospace and defense contractors, significant government investment in space programs (NASA, DoD), and a thriving commercial space sector, including numerous startups and large constellation operators. The region benefits from robust R&D capabilities and a strong innovation ecosystem, particularly in the US.

- Europe: A key player, driven by strong institutional support from the European Space Agency (ESA) and national space agencies, alongside major satellite manufacturers. The region focuses on advanced scientific missions, Earth observation, and the development of resilient communication infrastructures. Germany, France, and the UK are prominent contributors.

- Asia Pacific (APAC): Expected to exhibit the highest growth rate, fueled by ambitious space programs in China, India, and Japan, increasing demand for satellite-based services (e.g., broadband, remote sensing) in rapidly developing economies, and growing government and private investments in space infrastructure. The region is witnessing a surge in small satellite manufacturing and launch capabilities.

- Latin America: An emerging market with growing interest in satellite technology for telecommunications, disaster management, and resource monitoring. Countries like Brazil, Argentina, and Mexico are investing in national satellite programs and collaborating with international partners to enhance their space capabilities, though on a smaller scale compared to other regions.

- Middle East and Africa (MEA): Gradually increasing its participation in the space sector, primarily driven by the need for enhanced communication infrastructure, broadcasting services, and national security applications. Countries like UAE, Saudi Arabia, and South Africa are developing their space programs and exploring partnerships to acquire satellite bus technologies.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Satellite Bus Market.- Airbus SE

- Lockheed Martin Corporation

- The Boeing Company

- Northrop Grumman Corporation

- Thales Alenia Space

- Maxar Technologies Inc.

- Ball Aerospace & Technologies Corp.

- Sierra Nevada Corporation

- Space Systems Loral (SSL)

- OHB SE

- Astro Digital

- Blue Canyon Technologies

- GomSpace

- SSTL (Surrey Satellite Technology Ltd)

- Rocket Lab USA, Inc.

- LeoStella

- Tyvak Nano-Satellite Systems

- Bradford Space, Inc.

- Clyde Space (AAC Clyde Space)

- ICEYE

Frequently Asked Questions

Analyze common user questions about the Satellite Bus market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is a satellite bus and its primary function?

A satellite bus is the foundational structure of a satellite, providing essential support services for the payload. Its primary function is to house and support the mission-specific payload, providing power, propulsion, attitude control, thermal management, and communication systems necessary for the satellite to operate effectively in space.

How is the satellite bus market segmented?

The satellite bus market is segmented by various factors, including satellite mass (small, medium, large), subsystem (e.g., propulsion, power, structure), application (e.g., communication, Earth observation, scientific research), end-user (commercial, government, civil), and orbit type (LEO, MEO, GEO). These segments reflect the diverse requirements and uses of satellite platforms across the industry.

What are the key trends shaping the satellite bus industry?

Key trends include the growing adoption of standardized and modular bus designs, the proliferation of small satellites for mega-constellations, the increasing use of electric propulsion systems for efficiency, and the development of software-defined satellites for enhanced reconfigurability. Additionally, in-orbit servicing capabilities are emerging as a significant future trend.

What role does Artificial Intelligence (AI) play in satellite bus technology?

AI is increasingly integrated into satellite bus technology to enable autonomous operations, such as navigation, collision avoidance, and resource management. It also facilitates predictive maintenance by monitoring system health, enhances onboard data processing capabilities, and allows for intelligent anomaly detection and self-correction, thereby improving mission reliability and efficiency.

Which regions are leading the growth in the satellite bus market?

North America currently leads the market due to significant government and commercial investments and strong technological capabilities. However, the Asia Pacific region is projected to experience the fastest growth, driven by ambitious national space programs, increasing demand for satellite services, and burgeoning private sector involvement in countries like China and India.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted